CIP Chemicals Market Outlook 2025–2034: $3 Billion to $6.3 Billion at 8.5% CAGR Driven by Biopharma Sterility and Sustainable Sanitation

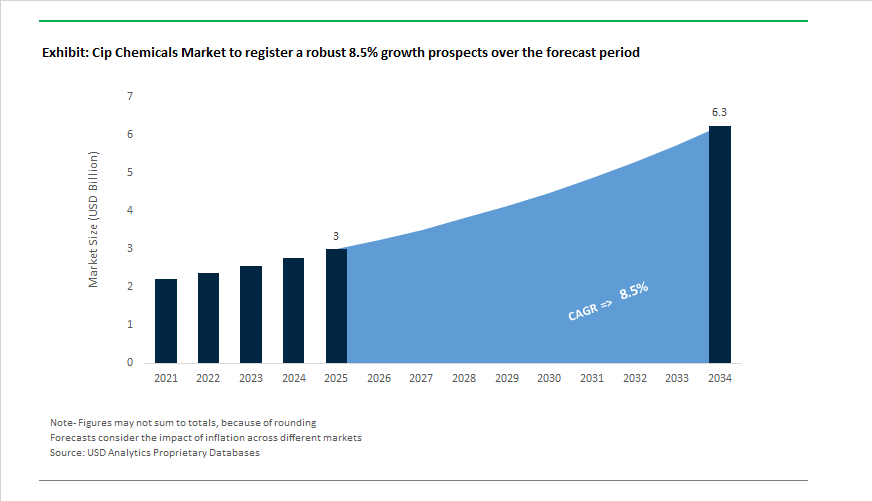

The global CIP Chemicals Market is projected to grow from $3 billion in 2025 to $6.3 billion by 2034, registering a CAGR of 8.5%. Clean-in-Place (CIP) chemicals remain mission-critical for hygienic process industries including food and beverage, dairy, brewing, pharmaceuticals, biotechnology, and industrial manufacturing. Increasing regulatory pressure on sterility validation, microbial risk management, and environmental compliance is reshaping demand for high-alkaline detergents, acid cleaners, peracetic acid disinfectants, enzymatic biofilm removers, and oxidizing sanitizers. Market growth is supported by rising automation in closed-loop CIP systems, greater adoption of digital water management platforms, and the transition toward low-carbon, bio-based cleaning chemistries.

Innovation and capacity expansion accelerated in 2024–2025. In February 2025, Diversey inaugurated a new European headquarters and R&D hub in the Netherlands, focused on developing automated and sustainable CIP formulations tailored for dairy, food processing, and pharmaceutical plants across Europe. In April 2025, the National Institute for Innovation in Manufacturing Biopharmaceuticals awarded $11.2 million in grants targeting advanced monoclonal antibody and cell therapy manufacturing, with a portion allocated to optimizing sterile CIP chemical protocols for high-value biologics. In January 2025, Ecolab introduced ReadyDose™, a compact solid-form cleaning technology that eliminates up to 98.8% of plastic packaging waste compared to conventional liquid CIP chemical drums. These initiatives demonstrate structural alignment between sustainability targets and industrial sanitation performance requirements.

Bio-based chemistry and enzyme-driven cleaning solutions are gaining measurable traction. Following the merger of Novozymes and Chr. Hansen to form Novonesis, the company opened an enzyme innovation center in California in February 2024, targeting low-temperature enzymatic CIP cleaners capable of degrading organic biofilms while reducing energy consumption in food and beverage facilities. In April 2024, BASF launched EcoBalanced biomass-based ingredients certified by TÜV Nord, enabling formulators to lower carbon intensity without compromising high-alkaline scale removal efficiency. Dow and LanzaTech introduced EcoSense™ 2470 biodegradable surfactant in September 2023–2024, derived from recycled carbon and designed for advanced wetting and emulsification in next-generation CIP formulations. Market data from 2024 through early 2025 confirmed peracetic acid as the fastest-growing disinfectant segment, driven by its broad-spectrum efficacy and environmentally benign breakdown profile. In 2025, Kersia Group expanded its peroxide- and organic acid-based CIP disinfectant range to reduce halogenated waste associated with chlorine-based sanitizers.

Strategic acquisitions and specialized system shifts are strengthening integrated sanitation ecosystems. In November 2024, Ecolab acquired Barclay Water Management, integrating monochloramine technology into its digital water safety platform to enhance Legionella control in industrial water systems linked to CIP operations. Henkel introduced Bonderite C-AK 14415 in the 2023–2024 period, a boron-free alkaline cleaner supporting environmentally compliant metal pretreatment CIP in automotive manufacturing. Summit Brands expanded mechanical cleaning complements through acquisition of the Pumie abrasive line in September 2023–2024, enhancing combined chemical-mechanical sanitation cycles. By early 2026, single-use CIP chemical systems gained significant adoption in U.S. and Indian biotech facilities, reducing cross-contamination risk and simplifying sterile validation. These technological shifts, regulatory mandates, and sustainability-driven formulation upgrades position the CIP chemicals market for sustained high single-digit growth through 2034.

CIP Chemicals Market Trends and Drivers

Enzymatic, Multi-Functional CIP Chemistries Driving Cycle Optimization and Sustainability Targets

A defining shift in the global CIP (Clean-In-Place) chemicals market is the substitution of legacy caustic/acid multi-step washes with multi-functional enzymatic formulations that remove protein, lipid, and polysaccharide residues at lower temperatures, enabling both resource efficiency and greater Operational Equipment Effectiveness (OEE).

Peer-reviewed research (Food Control Journal – February 2025) demonstrated that enzyme-based CIP protocols reduce microbial counts by >96%, while simultaneously cutting water consumption by 20–30% and lowering total facility-level carbon footprint by 10–20% due to reduced heat requirements.

Industry collaborations signal the scale of transition: In October 2025, BASF and IFF entered a multi-year strategic partnership to advance Designed Enzymatic Biomaterials™, accelerating the commercialization of bio-based, high-efficiency detergents engineered for dairy, beverage, nutraceutical, and fermentation-based production.

Ultra-Concentrated, Low-Foam Formulations Surging With AI-Enabled CIP Automation and IoT-Driven Sanitation

As manufacturers adopt AI-driven CIP skids, turbulence-enhanced cleaning, and real-time turbidity and conductivity sensors, CIP chemicals must increasingly support equipment—not interfere with it. Excessive foam causes cavitation, blocks optical detection windows, and destabilizes automated dosing, driving a shift toward low-foam, ultra-concentrated liquids optimized for digital control environments.

In September 2025, Ecolab launched CIP IQ™, an AI-powered platform using fluid-fingerprinting algorithms and inline sensors to dynamically adjust chemical dosing based on soil-load concentration. Early deployments indicate 15% faster cleaning cycle efficiency and 20% less water usage, illustrating how CIP chemistry is now a data-optimized performance function, not a static consumable.

Workforce shortages are also reshaping demand. PMMI automation reports (2025) indicate that engineering teams are prioritizing IoT-enabled chemical dosing systems to reduce operator dependency. This supports packaged solutions that are auto-metered, concentrated, and pump-compatible, replacing drum-based legacy detergents that require manual handling and rinse redundancy.

Real-Time Biofilm Monitoring and Proactive CIP Protocols Redefining Food Safety and Contamination Control

The persistence of biofilms is driving a pivot toward proactive CIP-led contamination prevention rather than reactive end-of-shift sanitation. Academic advances are now entering commercialization channels: In January 2025, University of California, Riverside researchers identified a plant-derived metabolite that prevents early-stage bacterial adhesion by disrupting fimbriae, setting the stage for biofilm-preventative CIP additives that could supplement or replace traditional biocides.

Simultaneously, real-time sensing is redefining cleaning logic. ALVIM biofilm sensors—capable of detecting fouling when only ~1% of surface area is colonized—enable predictive CIP activation, in which chemicals are dosed only when biological activity is confirmed. For high-risk dairy, infant nutrition, brewery, pet-food, and flavor ingredient processors, adoption of biofilm-triggered cleaning protects batch integrity, reduces recall risk, and minimizes chemical waste, directly impacting margin.

High-Purity, Compendial-Grade CIP Chemicals for Aseptic Pharma, CGT, and Sterile Injectable Production

A rapidly expanding premium segment is emerging in compendial-grade CIP chemicals for aseptic pharmaceutical facilities, cell-and-gene therapy suites (CGT), and sterile injectables. These operations require chemicals that meet cGMP, USP, and EP cleanability & residue-free standards, ensuring that cleaning agents do not introduce endotoxins, particulates, or extractables into sensitive biologics.

Between 2024–2025, FDA revisions to cleaning validation guidance heightened requirements for sterile-filterable, low-residue CIP formulations, which has already triggered procurement changes across U.S. and EU-based biologics facilities.

Material compatibility is also shaping purchase decisions. With pharmaceutical sites deploying high-performance elastomers—modified PTFE, FFKM—and single-use systems (SUS), demand is rising for chemistries that maintain cleaning efficacy without degrading seals, gaskets, or valves. Industry processing reports (December 2025) confirmed that capital expansion in sterile drug manufacturing is directly increasing demand for high-purity, non-aggressive CIP chemicals that extend asset lifecycle and reduce unplanned downtime.

CIP (Clean-in-Place) Chemicals Market Share and Segmentation Insights

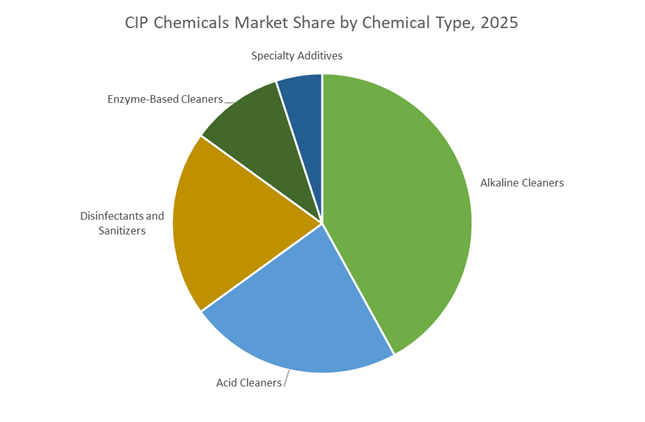

Chemical Type Segmentation: Alkaline Cleaners Anchor CIP Cycles as Enzyme-Based Solutions Accelerate

Alkaline cleaners lead the CIP chemicals market with about 42% share in 2025, serving as the primary agents for removing organic residues such as fats, proteins, and carbohydrates from stainless steel processing equipment. Sodium hydroxide and potassium hydroxide remain industry standards due to their effectiveness and compatibility with automated CIP systems. Acid cleaners follow as an essential second step, eliminating mineral scale and hard-water deposits while restoring surface passivation. Disinfectants and sanitizers, including peracetic acid and chlorine dioxide, represent a substantial portion of demand as manufacturers intensify microbial control in beverage, dairy, and pharmaceutical operations. Enzyme-based cleaners are the fastest-growing category, enabling low-temperature and low-pH cleaning that reduces energy consumption and extends membrane life. Specialty additives complement these chemistries by improving wetting, corrosion inhibition, and foam control across complex industrial cleaning environments.

End-Use Industry Distribution: Food and Beverage Leads While Pharma Compliance Sustains High-Value Demand

The food and beverage industry accounts for 55% of CIP chemical consumption, reflecting the high frequency of cleaning cycles required in dairy processing, breweries, and ready-to-eat production lines to prevent bacterial growth and cross-contamination. Pharmaceutical and biotechnology manufacturing represents a substantial share, driven by stringent cGMP compliance and FDA validation requirements that mandate zero cross-batch contamination in potent drug production. Industrial manufacturing relies on CIP chemicals to remove heavy residues from reactors, pipelines, and heat exchangers used in paints, lubricants, and specialty chemicals. Cosmetics and personal care form a specialized segment, where frequent CIP cycles are essential for handling viscous formulations and maintaining hygiene in water-based products. Together, these industries underpin consistent demand for alkaline cleaners, acids, sanitizers, and advanced enzymatic formulations across global automated cleaning infrastructure.

Competitive Landscape of the CIP Chemicals Market

The CIP Chemicals Market is characterized by vertically integrated water treatment leaders, specialty surfactant manufacturers, and oxygen-based disinfectant innovators serving food and beverage, pharmaceuticals, dairy processing, semiconductors, and biomanufacturing sectors. Competitive intensity centers on AI-enabled clean-in-place systems, bio-based surfactants, peracetic acid disinfection, and ultra-low residue formulations aligned with ESG and regulatory compliance. Market leaders are increasingly integrating IoT dosing systems, circular chemistry platforms, and high-concentration liquid technologies to reduce water, energy, and carbon intensity. Sustainability-driven metrics such as Zero Product Carbon Footprint and total value delivered models are reshaping premium pricing strategies across industrial cleaning ecosystems.

Ecolab leads AI-powered CIP optimization with integrated service and chemistry model

Ecolab remains the global pioneer in clean-in-place technology through its integrated Service plus Chemistry model. Its portfolio includes specialized alkaline and acid cleaners such as Exelerate™ and the Ecolab CIP IQ™ platform. During 2025 to 2026, Ecolab scaled its CIP IQ™ AI-enhanced solution, leveraging real-time analytics to detect over-cleaning and reduce water and energy consumption by up to 15 to 20%. The acquisition of Ovivo’s electronics ultrapure water business strengthened its footprint in semiconductor-grade cleaning. Strategically, Ecolab is advancing a Total Value Delivered eROI framework, aligning premium pricing with Planet Health and Business Health sustainability goals.

Solenis and Diversey create IoT-driven hygiene powerhouse after $4.6 billion merger

Following the $4.6 billion acquisition of Diversey, Solenis has emerged as a dominant force in water treatment and institutional hygiene. The combined portfolio now includes over 2,000 patents focused on water conservation and chemical efficacy optimization. In September 2025, the company launched a unified IoT-enabled CIP dosing system that automates hygiene compliance reporting for pharmaceutical facilities worldwide. Solenis maintains strong penetration in food and beverage and brewery sectors, especially across Asia-Pacific. Business expansion includes opening a state-of-the-art UK R&D center in 2025 dedicated to developing next-generation bio-based surfactants for industrial cleaning applications.

BASF drives green surfactant transformation with ZeroPCF cleaning chemistry

BASF plays a foundational role in the CIP chemicals market as a primary supplier of chlor-alkali derivatives, chelating agents, and high-purity surfactants under Lutensol® and Plurafac® brands. In early 2026, BASF extended its ZeroPCF initiative across its home and institutional cleaning portfolio using mass-balance renewable feedstocks. The company also developed loopamid®, a chemical recycling technology enabling circular reuse of polyamide-based cleaning components and filtration textiles. Strategically, BASF is accelerating its Green Transformation agenda, targeting a full transition from fossil-based surfactants to bio-based or circular alternatives by 2030.

Solvay strengthens oxygen-based disinfection with premium peracetic acid solutions

Solvay is a key player in oxygen-based disinfection for CIP systems, specializing in peracetic acid and hydrogen peroxide solutions used in dairy, beverage, and aseptic packaging lines. Peracetic acid is increasingly replacing chlorine cleaners due to its residue-free decomposition into water, oxygen, and acetic acid, aligning with environmental compliance mandates. In preparation for Q3 2026, Solvay announced optimization of soda ash capacity at its Torrelavega site to prioritize high-margin sodium bicarbonate for pharmaceutical and food industries. Through its Zeosil® circular silica strategy, Solvay integrates sustainable sourcing for specialty abrasives and cleaning agents.

Evonik advances bio-based surfactants and active hygiene ingredients

Evonik focuses on specialty additives and high-performance biocides that enhance the stability and shelf life of CIP chemical concentrates. Its portfolio includes high-purity hydrogen peroxide and AEROXIDE® additives that improve flow and cleaning efficiency in powdered formulations. In late 2025, Evonik launched TEGO® XP 32156, a 100% bio-based sophorolipid biosurfactant engineered for low-foam CIP applications in large industrial tanks. The company expanded its regional presence by opening a world-scale alkoxides plant in Singapore in August 2025, targeting Southeast Asia’s growing hygiene market while prioritizing pharmaceutical and biomanufacturing active ingredients.

Stepan scales biocatalytic surfactants and liquid concentrates for industrial CIP

Stepan is one of the world’s largest producers of anionic surfactants, forming the backbone of heavy-duty industrial and institutional cleaning formulations. In 2025, the company finalized expansion of its biocatalytic surfactant production line, emphasizing rhamnolipids for clean-label industrial markets. Stepan dominates supply for low-residue cleaners used in electronics and aerospace CIP operations where contamination control is critical. Strategically, the company is investing in Liquid Concentrate technology, delivering 10 times concentrated formulas for on-site dilution, reducing shipping volumes, logistics costs, and overall carbon footprint across global industrial cleaning supply chains.

United States: Digital-First Compliance and Water-Efficient CIP Chemistry

The United States CIP chemicals industry in 2025 and 2026 is being reshaped by a convergence of regulatory stringency, digitalization, and water-efficiency mandates. A pivotal inflection point came with the late-2025 expansion of the U.S. Environmental Protection Agency Safer Choice program, which for the first time introduced dedicated criteria for industrial Clean-in-Place formulations. This regulatory move elevated biodegradable surfactants such as alkyl polyglucosides into preferred formulation components, compelling chemical suppliers to re-engineer detergent portfolios for both environmental labeling and industrial performance. Parallel to this, heightened pharmaceutical hygiene oversight by the U.S. Food and Drug Administration, following record pharmaceutical imports in 2025, has driven demand for residue-free CIP chemicals validated under revised Annex 1 expectations. Pharmaceutical manufacturers are increasingly prioritizing low-foaming alkaline cleaners and ultra-pure acid rinses that minimize extractables and leachables risks.

Operational efficiency has emerged as a second strategic axis. Severe regional water stress, particularly under California’s 2025 Water Resilience Portfolio, has forced food and beverage processors to adopt single-pass chemical recovery and reuse systems. This shift has structurally increased demand for high-stability caustic regenerants and acids capable of maintaining cleaning efficacy across multiple cycles without degradation. At the same time, industrial innovation is accelerating through corporate consolidation. The post-acquisition integration of Diversey into Solenis enabled the launch of the first large-scale digital-chemical CIP service model in early 2025, combining IoT-based hygiene monitoring with automated chemical dosing. Complementing this trend, Ecolab Inc. expanded North American R&D to scale Exelerate™ TUF, a chemical optimized for dry CIP in snack processing, reflecting a broader industry pivot toward water-minimized cleaning architectures. Additionally, state-level PFAS restrictions across 13 states have accelerated the replacement of fluorinated wetting agents with silicone-free and eco-compliant alternatives, permanently altering the formulation landscape for U.S. CIP detergents.

India: Formalization of Hygiene Standards and Rapid CIP System Adoption

India’s CIP chemicals market is transitioning from fragmented, labor-intensive cleaning practices to standardized, automated systems, driven by regulatory enforcement and public-sector incentives. The 2025 rollout of the Clean Street Food & Industry mandate by the Food Safety and Standards Authority of India marked a structural shift. Dairy and beverage plants processing above 50,000 liters per day are now required to implement automated CIP validation, pushing demand for consistent, verifiable chemical cleaning protocols. This regulation has elevated the role of validated alkaline detergents, nitric and phosphoric acid blends, and disinfectants with documented residue profiles, particularly among mid-to-large processors.

Government-led sanitation initiatives have further accelerated adoption. Under Swachhata Hi Seva 2025, the Ministry of Commerce & Industry introduced a ₹320 crore incentive program to support SMEs transitioning away from manual cleaning toward semi-automated CIP systems by 2026. This policy intervention is expanding the addressable market for entry-level CIP chemical formulations designed for smaller skids and lower automation thresholds. In parallel, pharmaceutical modernization is reshaping technical requirements. Genome Valley in Hyderabad, one of India’s most advanced life sciences clusters, inaugurated a CIP Excellence Center in late 2025 focused on zero-residue chemical testing for biotherapeutics. This has intensified demand for ultra-low endotoxin cleaners and peroxide-based sanitizers compatible with sensitive biologics production.

Capital investment trends reinforce this trajectory. The Asian Development Bank reported a strong year-on-year rise in food processing capital expenditure in 2025, with high-precision chemical skids cited as a priority area. On the supply side, regional sourcing strategies are improving formulation availability. BASF commissioned a high-performance dispersant line in Nanjing serving the broader Asian market, including India, reducing reliance on imported specialty additives and improving consistency in advanced CIP formulations used across food and pharmaceutical facilities.

China: Regulatory Reformulation and Bio-Based CIP Chemistry Acceleration

China’s CIP chemicals industry is undergoing a rapid transformation driven by regulatory tightening, digital manufacturing policies, and sustainability-oriented feedstock transitions. A defining regulatory milestone occurred in March 2025 with the announcement of GB 31604.30-2025 by the National Health Commission of China, introducing stringent national methods for assessing phthalate migration in food-contact materials. This standard has forced widespread reformulation of CIP chemical lubricants and seal-compatible detergents, particularly in food and beverage plants where elastomer compatibility and low migration risk are now non-negotiable.

Simultaneously, the final phase of the Made in China 2025 initiative has prioritized digitalization within pharmaceutical manufacturing corridors. Provinces such as Jiangsu have seen a sharp increase in IoT-enabled CIP skids between 2024 and 2025, driving demand for chemically stable formulations that integrate seamlessly with sensor-driven dosing and real-time cleanliness verification. Regulatory pressure intensified further in July 2025 when China enacted a ban on 13 high-risk additives historically used in industrial cleaners. This ban has catalyzed a market-wide shift toward enzymatic detergents and peroxide-based sanitizers, particularly in export-oriented food processing facilities seeking regulatory resilience.

Sustainability considerations are now influencing upstream chemistry. BASF added ISCC EU certification to its biomass-balanced methanol portfolio in mid-2025, enabling Chinese producers to access lower-carbon feedstocks for green CIP solvents. To meet surging demand for bio-based surfactants, BASF also expanded alkyl polyglucoside capacity in Thailand in late 2025, strategically positioned to supply China’s rapidly evolving industrial cleaning sector. Collectively, these developments are repositioning China as a major adopter of next-generation, regulation-compliant CIP chemistries.

Germany: Export-Led Excellence and Circular Chemistry Integration

Germany continues to anchor the high-end segment of the global CIP chemicals industry through export leadership, regulatory compliance, and chemical innovation. In 2025, the country retained its position as the world’s largest exporter of industrial disinfectants, supported by strong international demand for high-purity CIP acids manufactured under stringent quality controls. This export strength is closely linked to regulatory evolution within the European Union. The August 2025 adoption of Regulation (EU) 2025/1731 under REACH Annex XVII restricted 16 additional CMR substances, triggering a systematic phase-out of certain ethoxylated surfactants in German CIP formulations. As a result, domestic producers have accelerated the development of safer, non-ethoxylated alternatives without compromising cleaning efficacy.

Innovation in process chemistry is reinforcing Germany’s competitive edge. In November 2025, BASF and ExxonMobil entered a joint development agreement to scale methane pyrolysis for green hydrogen production. The solid carbon byproduct is being piloted as a structural additive in corrosion-resistant CIP storage tanks, indirectly enhancing chemical stability and lifecycle performance. Concurrently, BASF’s launch of X3D® 3D-printed catalysts in 2025 optimized surfactant synthesis for specialized CIP wetting agents, with a new Ludwigshafen facility planned for 2026 to industrialize these advances.

Germany’s commitment to circular economy principles further differentiates its CIP ecosystem. BASF’s Winning Ways strategy achieved a 2025 milestone with textile-to-textile recycled polyamide processes that rely on specialized CIP-like cleaning cycles for industrial fiber recovery. This cross-sector application of CIP chemistry underscores Germany’s role not only as a formulation leader but also as a system innovator linking hygiene, sustainability, and advanced manufacturing.

Comparative Snapshot: Country-Level CIP Chemicals Evolution (2025–2026)

CIP (Clean-in-Place) Chemicals Market County Level Snapshot

|

Country

|

Primary Regulatory Driver

|

Dominant Industry Impact

|

Strategic Direction in CIP Chemicals

|

|

United States

|

EPA Safer Choice expansion and PFAS restrictions

|

Food processing and pharmaceuticals

|

Digital-chemical integration and water-efficient formulations

|

|

India

|

FSSAI automated hygiene mandates

|

Dairy, beverages, pharmaceuticals

|

Rapid shift from manual cleaning to validated automated CIP

|

|

China

|

Additive bans and food-contact standards

|

Food processing and pharma corridors

|

Enzymatic, peroxide-based, and bio-based reformulations

|

|

Germany

|

REACH Annex XVII revisions

|

Export-oriented industrial hygiene

|

High-purity, non-CMR, and circular-economy-aligned CIP chemistry

|

CIP (Clean-in-Place) Chemicals Market Report Scope

Cip Chemicals Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$3 Billion

|

|

Market Size (2034)

|

$6.3 Billion

|

|

Market Growth Rate

|

8.5%

|

|

Segments

|

By Chemical Type (Alkaline Cleaners, Acid Cleaners, Disinfectants and Sanitizers, Enzyme-Based Cleaners, Specialty Additives), By End-Use Industry (Food and Beverage, Pharmaceutical and Biotechnology, Cosmetics and Personal Care, Industrial Manufacturing), By Process Configuration (Single-Use CIP, Recovery and Reuse CIP, Multi-Tank CIP Systems), By Purity Grade (Food Grade, Pharmaceutical Grade, Industrial Grade)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Ecolab Inc., Solenis LLC, BASF SE, Kersia Group, Christeyns NV, Zep Inc., Evonik Industries AG, Kemira Oyj, Hydrite Chemical Co., Sealed Air Corporation, Stepan Company, Dow Inc., Clariant AG, LANXESS AG, Anderson Chemical Company

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

CIP Chemicals Market Segmentation

By Chemical Type

- Alkaline Cleaners

- Sodium Hydroxide

- Soda Ash

- Potassium Hydroxide

- Acid Cleaners

- Nitric Acid

- Phosphoric Acid

- Citric Acid

- Sulfamic Acid

- Disinfectants and Sanitizers

- Sodium Hypochlorite

- Peracetic Acid

- Chlorine Dioxide

- Hydrogen Peroxide

- Enzyme-Based Cleaners

- Proteases

- Lipases

- Amylases

- Specialty Additives

- Surfactants

- Sequestrants

- Chelating Agents

- Defoamers

By End-Use Industry

- Food and Beverage

- Pharmaceutical and Biotechnology

- Cosmetics and Personal Care

- Industrial Manufacturing

By Process Configuration

- Single-Use CIP

- Recovery and Reuse CIP

- Multi-Tank CIP Systems

By Purity Grade

- Food Grade

- Pharmaceutical Grade

- Industrial Grade

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in CIP Chemicals Industry

- Ecolab Inc.

- Solenis LLC

- BASF SE

- Kersia Group

- Christeyns NV

- Zep Inc.

- Evonik Industries AG

- Kemira Oyj

- Hydrite Chemical Co.

- Sealed Air Corporation

- Stepan Company

- Dow Inc.

- Clariant AG

- LANXESS AG

- Anderson Chemical Company

*- List not Exhaustive