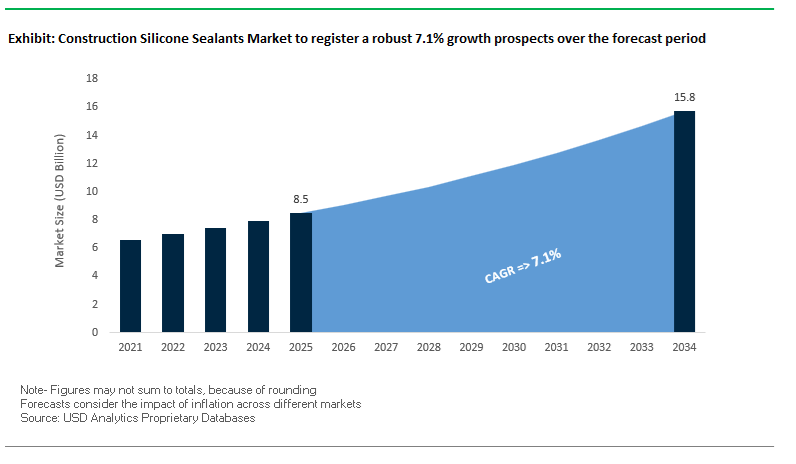

The global construction silicone sealants market is assuming strategic importance as building envelopes become larger, more glazed, and subject to stringent performance and sustainability criteria. Forecast to grow from USD 8.5 billion in 2025 to USD 15.8 billion by 2034 at a CAGR of 7.1%, the market reflects increasing specification of neutral-cure silicone chemistries in structural glazing, curtain walls, expansion joints, and high-movement façade systems. Structural silicones underpin façade integrity and long-term weatherproofing, translating material selection decisions into measurable outcomes for durability, energy performance, and lifecycle maintenance in both commercial and residential construction.

A core structural shift reshaping demand is the systematic replacement of traditional acetoxy and low-performance elastomeric sealants with advanced neutral-cure silicone systems engineered to meet rigorous facade engineering standards and installer expectations. Leading product lines such as DOWSIL™ 795 and DOWSIL™ 995 deliver ±50% movement capability under ASTM C719, enabling façades to absorb thermal expansion, wind loads, and seismic drift without cohesive failure, while one- and two-component structural glazing silicones such as DOWSIL™ 983/993N are tested to ASTM C1184 for safe load transfer in glass-to-frame assemblies, underscoring manufacturer-verified performance across substrates. Sika’s Sikasil® SG range similarly combines neutral curing with high elongation and adhesion to diverse materials, aligning with façade system requirements for condensation-curing silicone sealants in high-performance architectural applications.

This substitution is driven by performance metrics that deliver direct business value: high elastic recovery and sustained adhesion reduce façade maintenance cycles and water ingress risk, while structural silicones’ broad service temperature tolerance supports envelope reliability in extreme climates. Silicone sealants’ compatibility with substrates from glass and aluminum to masonry and concrete enhances installation flexibility and reduces field failures, improving uptime on complex façade projects. At the same time, the market trend toward low-VOC and low-odor formulations with emissions below typical green construction thresholds aligns with LEED, BREEAM, and WELL Building Standard mandates, and neutral-cure alkoxy systems minimize corrosive by-products on sensitive metals and natural stone. Over the forecast period, competitive differentiation in the construction silicone sealants market will hinge on verified performance through standards compliance, carbon-accountable manufacturing, and supply continuity for large-scale, high-specification façade programs across global regions.

The global construction silicone sealants industry is experiencing accelerated innovation, facility expansions, and regulatory alignment aimed at supporting sustainable, high-performance construction worldwide.

In February 2024, Dow Inc. announced the launch of a next-generation DOWSIL™ weathering silicone sealant, designed for extreme façade applications requiring advanced UV protection and movement accommodation. The new product expands Dow’s leadership in architectural silicone systems, supporting large-scale curtainwall, glazing, and cladding projects. Around the same period, Sika AG inaugurated a major sealant and adhesive manufacturing facility in Pune, India (January 2024), strengthening its local supply network amid India’s infrastructure boom. This facility serves high-demand applications including roofing, façade sealing, and precast concrete joints, underscoring Sika’s regional growth strategy in Asia-Pacific construction materials.

In January 2024, Wacker Chemie AG announced a new production site in Karlovy Vary, Czech Republic, marking a low triple-digit million-euro investment in room-temperature-vulcanizing (RTV) silicones. The facility complements its German operations at Nünchritz, enabling faster supply of RTV and alkoxy silicone sealants across Europe. The company’s expansion aligns with megatrends in renewable energy, electromobility, and sustainable building, which increasingly rely on high-durability silicone bonding systems. Earlier, in October 2023, Wacker also expanded its Jincheon, South Korea plant to meet regional demand for construction and automotive silicone sealants, showcasing its strategic balance of European and Asian capacity growth.

Sustainability remains a top-tier market driver. In December 2023, leading manufacturers advanced their portfolios of biomethanol-based sealants, such as ELASTOSIL® eco, replacing fossil feedstocks with certified sustainable biomass. This aligns with the global shift toward low-carbon construction materials. Additionally, March 2023 marked Wacker’s €20 million investment in expanding alkoxy silicone and cartridge-filling capacity in Germany, targeting environmentally safe, neutral-cure sealants for sensitive architectural applications. Industry-wide, Q1 2023 saw growing adoption of alkoxy-curing systems due to low odor, non-corrosive curing, and compliance with stringent indoor air quality standards, especially in interior glazing and modular housing.

The architectural move toward expansive glass façades, unitized curtain walls, and minimal framing systems is fueling the rapid adoption of high-modulus, neutral-cure structural silicone sealants. These high-performance materials are engineered to transfer wind and dead loads effectively while maintaining long-term weather resistance and eliminating the corrosion and acetic odor typical of traditional acetoxy silicones.

According to specialized industry technical specifications, high-modulus structural silicones for curtain wall systems are frequently rated with tensile strengths ≥0.60 MPa, underscoring their ability to bear heavy façade loads without structural failure. The growing prevalence of unitized façade systems further amplifies the demand, as their modular nature requires reliable, durable bonding systems capable of sustaining structural loads under thermal cycling and seismic movement.

A recent academic façade engineering analysis highlights that under extreme wind loads exceeding 5 kPa, the sealant “bite” — or bonding width — can exceed 30 mm when using conventional adhesives rated at 140 kPa. The use of high-modulus silicone sealants, therefore, becomes critical to maintain optimal design dimensions and avoid oversized aluminum profiles, reducing both structural complexity and material costs.

In addition, neutral-cure silicone formulations have proven long-term durability, offering movement capabilities of ±25% to ±50%, depending on the modulus category. These sealants maintain elasticity across decades of exposure to temperature variations, UV radiation, and dynamic façade movement, making them indispensable in modern skyscraper and curtain wall projects. Their ability to adhere to glass, metal, and composite substrates without primer simplifies façade fabrication and enhances on-site productivity, firmly establishing neutral-cure, high-modulus silicones as the benchmark for structural glazing performance.

With sustainability regulations tightening globally, the construction silicone sealants market is pivoting toward low-VOC, neutral-cure, and odorless formulations that align with indoor environmental quality (IEQ) goals and green certification systems such as LEED, WELL, and BREEAM. The trend directly supports the decarbonization and health-conscious construction goals emphasized in both commercial and institutional sectors.

In the United States, regulatory frameworks such as California’s SCAQMD Rule 1168 have imposed some of the world’s strictest VOC emission caps — 250 g/L for standard sealants and below 25 g/L for “super compliant” formulations — driving manufacturers toward waterborne and reactive silicone systems. Similarly, European REACH and Deco-Paint Directive (2004/42/EC) requirements have accelerated the adoption of solvent-free silicone technologies, creating a pan-European market where low-VOC products are the de facto standard.

Global leaders in silicone chemistry, including Dow, Momentive, and Wacker, are investing heavily in low-emission production technologies. Product lines launched in 2024 feature formulations optimized for indoor applications such as hospitals, cleanrooms, laboratories, and schools, combining very-low odor neutral-cure mechanisms with antimicrobial additives that prevent bacterial growth in sensitive environments.

Sustainability innovation continues to expand, with industry press releases from 2024 confirming that manufacturers are developing bio-silicone formulations and closed-loop production methods to minimize environmental impact. The innovation surge positions low-VOC and odorless silicone sealants as a cornerstone of sustainable construction, aligning high-performance bonding with global ESG and net-zero carbon objectives.

The global acceleration in solar energy adoption—fueled by government-backed investment programs and corporate decarbonization commitments—is creating a massive market opportunity for specialty silicone sealants used in photovoltaic (PV) system assembly and building-integrated photovoltaics (BIPV). These applications demand silicone-based adhesives capable of long-term UV resistance, temperature tolerance, and structural stability across decades of exposure.

In a landmark case, the Government of India’s PM Surya Ghar: Muft Bijli Yojana (2024–2027) allocates ₹75,021 crore ($9 billion USD) toward residential solar installation subsidies, with ₹65,700 crore reserved for rooftop applications. The program directly translates into demand for UV-resistant, high-durability silicone sealants that protect solar module joints, mounting systems, and peripheral glazing against extreme weather conditions.

Further reinforcing market potential, residential customers installing rooftop systems up to 2 kWp qualify for a ₹30,000 per kWp subsidy, driving large-scale adoption of small modular PV systems. Each installation necessitates precision-applied, weatherproof silicone sealants for edge encapsulation, backsheet protection, and structural fixation, especially for BIPV glass façade installations that merge energy generation with building envelope aesthetics.

Manufacturers such as Dow Silicones and Wacker Chemie are already commercializing solar-grade silicones formulated for long-term adhesion stability (up to 25 years), high transparency, and exceptional UV resistance. The drives a rapidly expanding vertical where silicone sealants are not just ancillary materials but critical enablers of clean energy infrastructure and sustainable architectural design.

The rise of mass timber construction, especially Cross-Laminated Timber (CLT) and Glue-Laminated Timber (Glulam) structures, represents a transformative opportunity for silicone sealant manufacturers. Wood’s hygroscopic nature—its tendency to absorb and release moisture—introduces unique challenges for joint movement and airtightness, positioning flexible, high-elongation silicone sealants as essential components for the next generation of sustainable building envelopes.

Unlike metals and concrete, whose thermal expansion typically demands ±25% joint movement capability, CLT systems require sealants that can stretch ±50% or more to accommodate wood’s natural dimensional variation due to moisture cycling. Industry and academic research has consistently identified moisture-induced swelling and shrinkage as key risk factors for joint failure and water ingress in CLT envelopes. These studies confirm that exterior-grade silicone sealants, designed with superior elasticity and hydrophobic characteristics, are essential to preserve the long-term integrity and appearance of exposed timber facades.

Further, monitoring studies of U.S.-made CLT structures have recorded moisture saturation at multiple depths within unsealed joints, emphasizing the importance of high-flexibility, vapor-permeable sealants capable of preventing trapped moisture while allowing the wood to breathe. The balance of airtightness and moisture management is becoming a defining characteristic of next-generation silicone technology for wood construction.

The aesthetic dimension also presents a premium growth niche. With architects increasingly specifying exposed timber interiors and façades, the need for non-staining, UV-resistant silicone sealants is expanding rapidly. These sealants preserve the natural hue and texture of timber surfaces while providing fire-rated performance compliant with ASTM C920 for hybrid construction systems.

Construction Silicone Sealants Market Share Insights, 2025-2034

Neutral-cure silicone sealants hold the largest share of the global construction silicone sealants industry, commanding 53.2% of the market by 2025, primarily due to their superior substrate compatibility, long-term durability, and non-corrosive nature. Unlike acetoxy formulations, neutral-cure sealants release neutral byproducts such as alcohol or oxime during curing, which prevents corrosion on sensitive materials like aluminum, galvanized steel, concrete, and natural stone. This makes them indispensable for structural glazing, façade sealing, and curtain wall applications, where material integrity and adhesion longevity are paramount. Their flexibility, high UV stability, and resistance to extreme temperature fluctuations make them ideal for modern architectural designs that emphasize glass and metal façades.

The shift toward high-performance and low-VOC construction materials globally has further strengthened the dominance of neutral-cure silicone sealants. They meet the stringent environmental and safety regulations across Europe and North America, where LEED and BREEAM certifications promote low-emission sealant usage. Additionally, neutral-cure systems are preferred for industrial and electronic assembly applications, where minimal byproduct release and precise curing control are necessary. The segment’s growth is bolstered by increasing demand from high-rise urban projects and modular construction, which require long-life, non-yellowing sealants compatible with a wide variety of substrates.

Acetoxy-cure silicone sealants remain a significant and resilient segment, representing 31.2% of the global market, owing to their fast curing speed, low cost, and excellent adhesion to non-porous substrates like glass, glazed ceramics, and tiles. They are the traditional choice for sanitary, kitchen, and glazing applications, where quick installation and early strength are valued more than substrate versatility. Their strong mechanical properties and resistance to mold and mildew make them particularly popular in bathroom and kitchen sealing in both residential and light commercial buildings.

The acetoxy segment benefits from a massive presence in the global DIY market, driven by retail availability, easy application, and lower price points compared to neutral-cure formulations. However, acetoxy silicones are limited by their release of acetic acid during curing, which restricts their use on metals and concrete due to potential corrosion. The segment continues to grow in emerging economies where cost efficiency and rapid construction turnaround take precedence over long-term chemical stability. Despite regulatory pressure toward low-odor, low-VOC materials, the acetoxy segment maintains its position through continuous improvements in fungicide formulations, cure control, and aesthetics, making it an enduring part of the market mix.

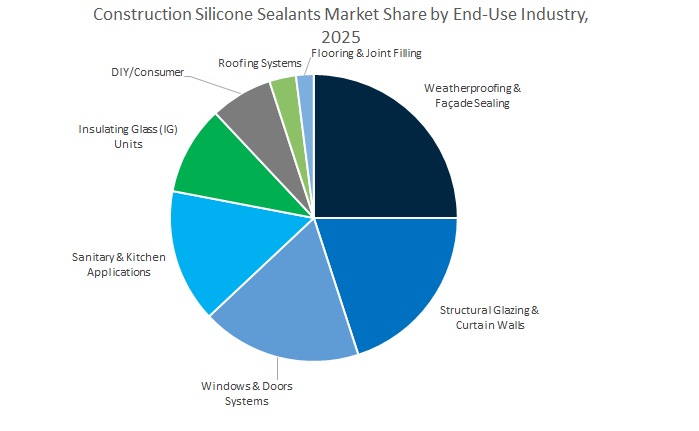

The Weatherproofing and Façade Sealing segment holds the dominant position in the global construction silicone sealants market, accounting for 25.8% of global demand by 2025. This leadership is driven by the rapid growth of high-performance building envelopes featuring glass façades, metal claddings, and composite panels, which demand long-lasting, flexible, and UV-resistant sealing solutions. Neutral-cure silicone sealants are the industry standard in this segment due to their exceptional elasticity, adhesion, and resistance to extreme temperature fluctuations and environmental exposure. They form a critical part of the air and moisture barrier systems essential for modern energy-efficient and green-certified buildings.

In the commercial construction sector, silicone sealants are integral to the structural glazing of skyscrapers and curtain wall systems, where they provide both load transfer and weatherproofing capabilities. Their ability to maintain elasticity over decades without cracking or discoloration ensures low maintenance costs and structural safety. The growth in urban infrastructure and smart city projects across Asia-Pacific, the Middle East, and North America continues to fuel this segment, as builders increasingly specify high-performance sealants for durability and energy performance.

The Windows & Doors and Sanitary & Kitchen segments represent a significant portion of the construction silicone sealants market, driven by massive volume consumption in residential and light commercial construction. Windows and door sealing relies heavily on silicones for their ability to bond dissimilar materials—aluminum, PVC, wood, and glass—while ensuring long-term flexibility and resistance to weathering. As energy-efficient construction codes gain traction, the use of silicone sealants for airtight and thermally efficient installations continues to expand.

The Sanitary & Kitchen segment is dominated by acetoxy-cure silicone sealants due to their fast curing, cost-effectiveness, and excellent mold resistance, making them the preferred choice for wet area applications like bathrooms, sinks, and countertops. This segment benefits from ongoing residential remodeling activity and a strong DIY retail market presence in both developed and emerging economies. Additionally, the introduction of antimicrobial and low-odor formulations has broadened their appeal among consumers and professional contractors alike.

The construction silicone sealants market is dominated by global chemical leaders that combine R&D excellence, diversified product portfolios, and large-scale production capabilities. Key players such as Dow Inc., Wacker Chemie AG, and Sika AG are setting new benchmarks in structural glazing performance, environmental compliance, and material innovation through sustained investments and next-generation product launches.

Dow Inc. continues to lead the global façade and glazing sealants market through its DOWSIL™ portfolio, including flagship products DOWSIL™ 995 and DOWSIL™ 993N, both renowned for exceptional tensile strength and weathering durability in large-scale architectural projects. The company’s sustainability roadmap includes the introduction of Low Embodied Carbon DOWSIL™ Silicones, providing project-specific PAS 2060 Carbon Neutrality Certificates. Dow also offers specialized solutions such as DOWSIL™ 790 Ultra-Low Modulus Sealant, ideal for high-movement expansion joints on porous substrates like concrete and stone. Its Primer-C OS technology enables fluorescent quality control inspection, ensuring application consistency in critical glazing systems. Through a strong combination of engineering validation, sustainability, and aesthetics, Dow has solidified its leadership in structural glazing and façade weatherproofing solutions.

Wacker Chemie AG remains one of the most vertically integrated manufacturers of RTV (room-temperature-vulcanizing) and alkoxy silicone sealants. With a €20 million expansion at its Nünchritz plant (2023), Wacker increased both production and cartridge filling capacities to meet the surging demand for neutral-cure, low-odor silicone sealants in Europe. Its ELASTOSIL® eco line—certified under REDcert²—represents a milestone in biomass-balanced silicone technology, replacing fossil-based feedstocks with renewable sources. The company also focuses on specialty silicones for electromobility and renewable energy, showcasing R&D synergies between its sealant and industrial materials divisions. Wacker’s strategy highlights its role as a sustainability-driven leader, emphasizing traceability, low emissions, and cross-sector material innovation.

Sika AG has significantly expanded its footprint in Asia-Pacific, opening a production facility in Pune, India (January 2024) to meet rising demand for high-performance construction sealants. Its SikaSeal® range features high-quality silicone sealants with superior sag resistance and smooth extrusion properties, ideal for vertical façade applications. Sika also leads with Sikaflex® polyurethane and STP (Silane-Terminated Polymer) systems, offering a comprehensive elastic jointing portfolio. Consistent with its sustainability vision, Sika prioritizes low-emission sealant formulations, ensuring compliance with interior air quality standards such as EC1+. Its product portfolio spans glazing, roofing, and wet-room sealing, offering long-term durability, adhesion, and UV stability.

China remains the largest consumer and producer in the global construction silicone sealants market, driven by large-scale urbanization, infrastructure upgrades, and domestic raw material manufacturing capacity. The National Development and Reform Commission (NDRC) has allocated CNY 4 trillion (USD 0.56 trillion) through 2030 for “hidden infrastructure” upgrades, including underground utility pipelines and transport networks. The applications increasingly prefer silicone-based sealants over acrylics or polysulfides for their UV stability, flexibility, and long-term adhesion in both exposed and high-humidity environments.

In 2024, Sika AG inaugurated a state-of-the-art specialty chemicals plant in Northeast China, significantly boosting the local supply of high-performance construction sealants and adhesives. Simultaneously, China’s chemical sector investment rose 8.9% year-on-year in 2024, securing the domestic supply of critical silicone resins, crosslinkers, and filler materials used in structural glazing and façade applications.

With expanding urban centers, high-rise glazing, solar façade integration, and prefabricated construction techniques, demand for neutral-cure and hybrid silicone formulations is surging. The sealants play a pivotal role in energy-efficient building envelopes—a core component of China’s green construction policies under the 14th Five-Year Plan. As local R&D emphasizes sustainability and VOC compliance, China continues to anchor global silicone innovation and production scalability.

India’s construction silicone sealants market is experiencing strong upward momentum, propelled by large-scale infrastructure investments, government housing programs, and foreign direct investment (FDI) in industrial manufacturing. In 2024, Henkel invested in expanding its Kurkumbh site, its largest production facility in India, reinforcing its capacity to supply high-performance silicone and hybrid sealants for infrastructure and industrial applications.

In parallel, Sika AG’s inauguration of its Pune facility in January 2024 marks a key milestone in India’s transition toward localized manufacturing of f, aligning with the government’s “Make in India” initiative. The facility caters to a broad spectrum of sectors—from commercial real estate to heavy infrastructure—addressing the rapidly expanding domestic demand for high-durability silicone products.

India’s affordable housing megaprojects, such as Pradhan Mantri Awas Yojana (PMAY), are significantly influencing the adoption of silicone weatherproofing sealants that deliver superior moisture resistance, flexibility, and thermal insulation. In humid and coastal regions like Kerala, Mumbai, and Chennai, the demand for UV-stable, mildew-resistant, and elastomeric silicone formulations has outpaced traditional acrylic alternatives.

The developments, combined with ongoing urban redevelopment initiatives and private investment in smart cities, solidify India’s role as a strategic regional hub for silicone sealant innovation and manufacturing scalability.

The United States construction silicone sealants industry is undergoing a major transformation driven by green building regulations, LEED certifications, and increasing investment in façade modernization. In metropolitan hubs such as New York, Chicago, and Los Angeles, eco-friendly and low-VOC silicone sealants are standard for both new construction and renovation projects targeting LEED Platinum and WELL Building Standards.

In 2024, Novagard introduced a portable version of its two-component Qwik-Set neutral-cure silicone glazing sealant, capable of achieving 15 psi tensile strength in under 20 minutes—a breakthrough for rapid onsite applications in curtain wall repairs and field installations. Similarly, Dow Inc. launched the DOWSIL™ 993 Weathering Silicone Sealant (February 2024), engineered for high-UV environments and long-term façade durability, particularly for commercial skyscrapers and energy-efficient glazing systems.

The push toward carbon-neutral construction materials has accelerated R&D in bio-based and low-emission silicone formulations, while AI-assisted Product Carbon Footprint (PCF) calculators are gaining traction among architects and contractors to quantify embodied carbon in sealant applications. Furthermore, the data center construction boom—driven by hyperscale projects across Texas and Virginia—is fueling demand for firestop and waterproofing silicone systems designed for mission-critical environments.

Germany remains the technological nucleus of the European construction silicone sealants market, underpinned by stringent energy efficiency mandates, industrial renovation projects, and automotive integration of advanced silicones. As part of the EU’s Green Deal, national renovation programs are boosting demand for structural glazing, joint insulation, and façade bonding sealants that meet high mechanical and environmental standards.

Major automotive manufacturers—BMW, Audi, and Volkswagen—are also adopting silicone sealants for EV chassis assembly, vibration control, and heat management, spurring R&D synergies between construction and mobility sectors. However, REACH restrictions on cyclic siloxanes (D4, D5, D6), with enforcement beginning June 2026, are compelling sealant manufacturers to accelerate development of compliant, high-performance alternatives that maintain adhesion strength and elasticity.

German producers are heavily investing in R&D for low-isocyanate, non-toxic silicone formulations, and AI-assisted quality assurance systems to monitor real-time curing and mechanical properties. The national focus on energy retrofit projects underlines the demand for low-VOC, sustainable sealants supporting Passive House and DGNB-certified constructions. Germany’s adherence to eco-labelling, transparency, and recyclability continues to set global quality benchmarks for silicone sealant formulation.

Japan and South Korea are emerging as critical innovation hubs for specialty silicone sealants driven by high-value construction, automotive, and marine applications. In January 2025, Wacker Chemie AG inaugurated two new specialty silicone production plants in both countries to enhance supply for construction, automotive, and electronics industries—marking a pivotal expansion in the Asia-Pacific silicone value chain.

In December 2024, Soudal reinforced its East Asian footprint by acquiring a majority stake in Sharp Chemicals, a prominent Japanese adhesive manufacturer. The acquisition strategically positions Soudal to capture the premium construction sealants market characterized by precision-engineered, low-VOC formulations used in façade glazing, structural joints, and waterproofing systems.

Japan’s marine and shipbuilding sectors, represented by the Ship Builders Association of Japan, continue to rely on high-performance weather-resistant silicone sealants for port and harbor infrastructure—applications that often overlap with civil engineering and high-rise construction. In South Korea, heavy investment in EV and electronics manufacturing is indirectly strengthening the local demand for industrial-grade silicone polymers suitable for both construction façades and semiconductor facility bonding.

Construction Silicone Sealants Market Report Scope

Construction Silicone Sealants Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$8.5 Billion

|

|

Market Size (2034)

|

$15.8 Billion

|

|

Market Growth Rate

|

7.1%

|

|

Segments

|

By Chemistry (Acetoxy-Cure Silicone Sealants, Neutral-Cure Silicone Sealants, Oxime-Cure, Alkoxy-Cure, Other Neutral-Cure), By Product Type (One-Component Silicone Sealants, Two-Component Silicone Sealants, Specialty Silicone Sealants), By End-User (Structural Glazing & Curtain Walls, Weatherproofing & Façade Sealing, Insulating Glass Units, Windows & Doors Systems, Sanitary & Kitchen Applications, Flooring & Joint Filling, Roofing Systems, DIY/Consumer), By Technology (Room Temperature Vulcanizing, Thermoset or Heat-Cured, Radiation Cured, Pressure Sensitive

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Dow Inc., Wacker Chemie AG, Sika AG, Henkel AG & Co. KGaA, Shin-Etsu Chemical Co. Ltd., H.B. Fuller Company, Momentive Performance Materials Inc., Bostik, Soudal N.V., Tremco Incorporated, 3M Company, Elkem ASA, Mapei S.p.A., Novagard, Huntsman International LLC

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Chemistry

- Acetoxy-Cure Silicone Sealants

- Neutral-Cure Silicone Sealants

- Oxime-Cure

- Alkoxy-Cure

- Other Neutral-Cure

By Product Type

- One-Component Silicone Sealants

- Two-Component Silicone Sealants

- Specialty Silicone Sealants

By End-Use Industry

- Structural Glazing & Curtain Walls

- Weatherproofing & Façade Sealing

- Insulating Glass Units

- Windows & Doors Systems

- Sanitary & Kitchen Applications

- Flooring & Joint Filling

- Roofing Systems

- DIY/Consumer

By Technology

- Room Temperature Vulcanizing

- Thermoset or Heat-Cured

- Radiation Cured

- Pressure Sensitive

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

- Dow Inc.

- Wacker Chemie AG

- Sika AG

- Henkel AG & Co. KGaA

- Shin-Etsu Chemical Co. Ltd.

- H.B. Fuller Company

- Momentive Performance Materials Inc.

- Bostik

- Soudal N.V.

- Tremco Incorporated

- 3M Company

- Elkem ASA

- Mapei S.p.A.

- Novagard

- Huntsman International LLC

*- List not Exhaustive

Research Coverage

Prepared by USDAnalytics, this report investigates the Construction Silicone Sealants Market through a performance-and-compliance lens, delivering analysis reviews that benchmark joint movement, adhesion spectra, and durability against modern façade and glazing requirements; it highlights neutral-cure and alkoxy curing advances, low-VOC/low-odor formulations, and weathering resilience that sustain envelope integrity across extreme climates; and it maps breakthroughs in structural glazing validation, warranty-backed longevity, and code-aligned indoor air quality. By linking chemistry to field performance, lifecycle risk, and specification pathways, this report is an essential resource for architects, façade engineers, contractors, OEM system fabricators, and sourcing leaders seeking safer, greener, and structurally robust sealing solutions for high-rise, modular, and retrofit applications.

Scope Highlights

Segmentation:

- By Chemistry: Acetoxy-Cure Silicone Sealants; Neutral-Cure Silicone Sealants; Oxime-Cure; Alkoxy-Cure; Other Neutral-Cure.

- By Product Type: One-Component Silicone Sealants; Two-Component Silicone Sealants; Specialty Silicone Sealants.

- By End-Use Industry: Structural Glazing & Curtain Walls; Weatherproofing & Façade Sealing; Insulating Glass Units; Windows & Doors Systems; Sanitary & Kitchen Applications; Flooring & Joint Filling; Roofing Systems; DIY/Consumer.

- By Technology: Room Temperature Vulcanizing; Thermoset or Heat-Cured; Radiation Cured; Pressure Sensitive.

Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

Time Frame: Historic data 2021–2024 and forecasts 2025–2034.

Companies: Analysis/profiles of 15+ companies including strategies, product benchmarking, capacity moves, and innovation pipelines.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.