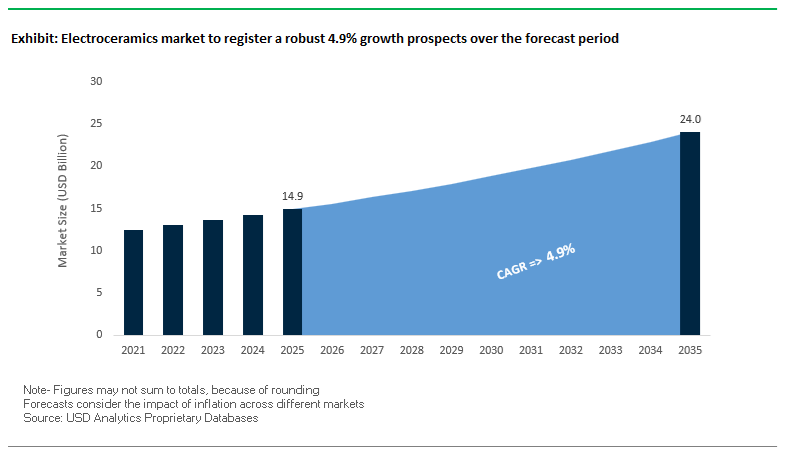

The Electroceramics Market, valued at USD 14.9 billion in 2025, is projected to reach USD 24 billion by 2035, advancing at a steady CAGR of 4.9% between 2025 and 2035. The market is undergoing a transformative phase driven by the rapid scaling of 5G/6G communication systems, electrification of mobility, semiconductor miniaturization, power electronics expansion, and the commercialization of solid-state batteries.

The global Electroceramics Market is experiencing accelerated innovation driven by telecommunications growth, automotive electrification, miniaturized semiconductors, and national initiatives aimed at strengthening supply chain resilience. The surge in 5G deployment and AI computing architectures is expanding demand for dielectric ceramics, MLCCs, LTCC components, and ceramic substrates capable of supporting high-frequency operation and thermal management. Simultaneously, EV and renewable energy sectors are fuelling demand for high-performance ceramic substrates capable of sustaining temperatures up to 200°C, allowing power electronics to reach 98% efficiency. These shifts reflect a broader industry movement toward materials that deliver reliability, precision, and superior energy density across compact architectures.

Recent market developments between January 2025 and December 2025 highlight a powerful combination of R&D investments, government-backed funding, and strategic corporate initiatives. In December 2025, South Korea announced a $68.1 million government R&D plan to advance core ceramic technologies essential for semiconductor and secondary battery supply chains—signaling national prioritization of ceramic self-reliance. In November 2025, India launched a landmark ₹1 lakh crore RDI Scheme targeting private innovation in EVs, clean energy, and electroceramics for solid-state batteries, sensor systems, and power electronics. Major corporations including Kyocera showcased advanced ceramic solutions for AI accelerators, 5G infrastructure, and EV systems during September 2025, reinforcing electroceramics’ pivotal role across high-reliability electronics.

Technology advancements are equally shaping market direction. A leading European specialty chemicals group announced a major low-temperature co-fired ceramic (LTCC) breakthrough in August 2025, reducing sintering temperatures by 15%—a significant step toward lowering production costs and energy consumption in RF component manufacturing. In May 2025, CeramTec expanded into piezoelectric sensing through a strategic acquisition, bolstering leadership in medical and industrial electroceramics. TDK responded to surging demand by raising MLCC production capacity in the Philippines by 20% in April 2025, while Murata introduced a new miniaturized high-voltage MLCC series in January 2025, reducing component volume by 45% for 5G and portable medical applications. These developments collectively demonstrate how innovation, state-backed investments, and aggressive capacity expansion are converging to reshape the electroceramics landscape.

Industry professionals increasingly seek electroceramic solutions that enable high-frequency signal integrity, withstand thermal stress, support micro-scale precision, and deliver reliability across mission-critical applications. As the electronics supply chain becomes more performance-intensive and energy-efficient, electroceramics—particularly dielectric ceramics, piezoelectric ceramics, ferrites, substrates, and solid-state electrolytes—are emerging as foundational materials for next-generation electronic systems. With emerging markets including AI accelerators, EV traction inverters, IoT sensor nodes, and medical imaging devices demanding superior ceramic performance, electroceramics remain integral to enabling faster data processing, higher power densities, and long device lifetimes.

- 5G infrastructure requires 10–15× more MLCCs and dielectric ceramics per unit area compared to 4G, driving exponential materials demand.

- AlN and SiC-based ceramic substrates support power electronics operating up to 200°C, enabling 98% power conversion efficiency in EV inverters.

- Piezoelectric ceramics achieve sub-nanometer precision, supporting MEMS, precision medical imaging, and industrial micro-actuation.

- Solid-state electrolyte ceramics increase lithium battery energy density by 25–50%, accelerating next-gen EV and storage technologies.

- High-purity alumina substrates (99.9%+) are essential for semiconductor packaging, ensuring insulation stability and high thermal conductivity for advanced chips.

Technology Driven Trends and Strategic Opportunities Transforming the Electroceramics Market

Trend 1 - Electroceramics Become a Cornerstone of Solid-State Battery Commercialization

Solid-state batteries (SSBs) have emerged as a key inflection point in next-generation energy storage, placing electroceramics at the center of EV innovation and high-density consumer electronics design. Automotive OEMs-including Toyota, BMW, Ford, and leading battery manufacturers-are aggressively pursuing electroceramic-based solid electrolytes to overcome safety and performance limitations of conventional liquid-electrolyte lithium-ion cells.

Commercial timelines underscore the seriousness of this shift. Samsung SDI’s S-Line pilot production, completed in 2023, targets mass production by 2027, signaling a strategic commitment to oxide- and sulfide-based ceramic electrolytes. These materials, particularly lithium argyrodite sulfides, offer ionic conductivity exceeding 10 mS/cm, rivaling or surpassing liquid electrolytes while enabling superior thermal stability.

The performance impact is substantial: inorganic ceramic electrolytes eliminate flammable solvents, enabling inherently safer architectures with 30–50% higher energy density at the pack level. Such gains directly address EV bottlenecks in driving range, fast charging, and thermal management.

Collaborative R&D partnerships further de-risk the supply chain. Companies like Solid Power have formalized alliances with BMW and Ford to accelerate sulfide-based electrolyte commercialization-indicating the growing integration of Tier 1 suppliers into vertically aligned electroceramics development pipelines. This convergence of OEM investment, material breakthroughs, and electrolyte safety advantages is rapidly positioning electroceramics as the foundation of future SSB platforms across automotive and consumer electronics sectors.

Trend 2 - Next-Generation Semiconductor Architectures Rely on Advanced Electroceramics (More-than-Moore Evolution)

The semiconductor industry’s progression toward More-than-Moore architectures is increasing reliance on tailored electroceramics to deliver breakthroughs in memory performance, RF functionality, transistor scaling, and energy-efficient computation. As traditional silicon-based scaling approaches its limits, electroceramic-enabled functionalities have become essential for enabling new device capabilities.

A major driver is the universal migration toward High-K Dielectrics, led by materials such as Hafnium Oxide (HfO₂) with dielectric constants around 25-significantly higher than SiO₂ (k=3.9). These materials enable reduced Equivalent Oxide Thickness (EOT) and suppress leakage currents by over 1000× at advanced nodes such as 45 nm and below, supporting transistor miniaturization without compromising insulation performance.

Emerging memory architectures further reinforce this demand. Ferroelectric RAM (FeRAM)-leveraging polarization properties of electroceramics such as PZT and SBT-offers non-volatile storage with ultra-low power consumption and fast switching, making it ideal for IoT, edge devices, and low-power embedded systems.

High-frequency communication platforms add another layer of growth. 5G and emerging 6G networks rely heavily on microwave dielectric ceramics and electroceramic thin films to deliver precise RF filtering, device miniaturization, and low-loss signal handling as data throughput requirements expand exponentially.

Meanwhile, the DRAM industry’s relentless cell-shrinking roadmap is accelerating the need for high-k dielectrics like Tantalum Pentoxide (Ta₂O₅, k≈25) and Barium Strontium Titanate (BST, k in the thousands). These materials enable reliable charge storage despite shrinking geometries, making them indispensable for future memory scaling. Collectively, these semiconductor-driven forces position electroceramics at the core of next-generation microelectronics innovation.

Opportunity 1 - Multifunctional Electroceramics Enabling Monolithic Smart Sensor-Actuator Systems

Demand for compact, multifunctional, self-sufficient components in IoT, soft robotics, wearable electronics, and biomedical systems is creating a high-value opportunity for integrated electroceramics capable of sensing, actuation, and energy harvesting within a single monolithic structure.

In soft robotics and biomedical devices, Dielectric Elastomer Actuators (DEAs) are gaining traction as flexible, electromechanically active materials. Their ability to self-sense changes in force, strain, or motion enables simplified architecture for exoskeletons, surgical tools, and precision robotic grippers, eliminating the need for external sensor arrays.

Energy-harvesting capabilities introduce an additional layer of system autonomy. Piezoelectric electroceramics embedded into monolithic designs can transform ambient vibration into electrical energy, allowing predictive-maintenance sensors to operate battery-free-a major breakthrough for industrial IoT deployment.

Innovation platforms such as Hydraulically Amplified Self-Healing Electrostatic (HASEL) actuators further illustrate the material evolution underway. These actuators use specialized flexible dielectric films to produce lifelike motion comparable to biological muscle, opening scalable opportunities in next-gen robotics, medical assistive devices, and high-dexterity automation systems. As multifunctional electroceramics converge sensing, actuation, and power generation, they present a transformative pathway for compact smart-material systems.

Opportunity 2 - Strengthening Domestic Supply Chains for Strategic Piezoelectric and Microwave Ceramics

Global governments are increasingly prioritizing domestic manufacturing of critical electroceramic materials due to rising geopolitical risk, defense requirements, and telecommunications dependency. These strategic materials-especially piezoelectrics and microwave dielectric ceramics-play indispensable roles across radar systems, precision actuators, 5G/6G communications, and advanced manufacturing.

The U.S. Department of Energy (DOE) has allocated over $3 billion through the Bipartisan Infrastructure Law to expand domestic capacity for extracting, refining, and processing critical minerals used in electroceramics. This funding directly supports supply security for high-purity piezoelectric ceramics and dielectric materials with defense and energy relevance.

National security agencies are reinforcing similar priorities. The U.S. Department of Defense (DoD) has committed more than $94 million to develop specialized manufacturing facilities for rare earth permanent magnets-materials that often operate alongside electroceramics in precision electromechanical systems. This investment underscores the strategic importance of a resilient electroceramics supply ecosystem.

However, supply risk remains high. The U.S. Geological Survey reports that the United States imports over 80% of its rare earth elements, which serve as dopants or core constituents for many high-performance electroceramics. This dependency exposes downstream sectors to geopolitical fluctuations, creating strong government and private-sector incentives to establish sovereign supply chains, recycling infrastructure, and domestic material processing hubs.

Electroceramics Market Share Analysis

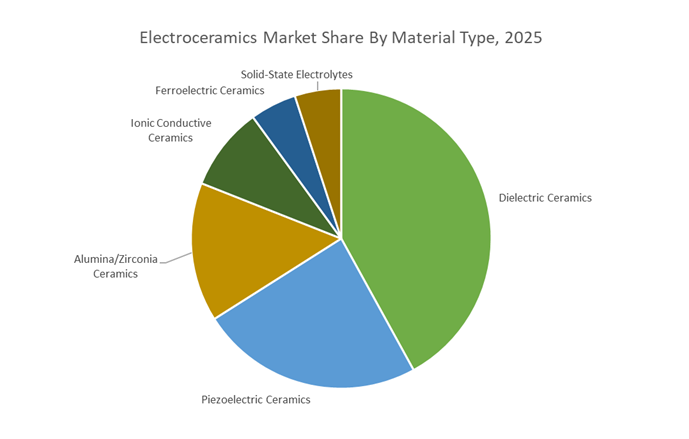

Market Share by Material Type: Dielectric Ceramics Maintain Dominance Through High-Volume Electronic Integration

Dielectric Ceramics account for the largest 42% market share within the Material Type segment, and their dominance reflects the foundational role they play in the global electronics ecosystem. Because dielectric materials—particularly barium titanate (BaTiO₃) formulations—form the core of multilayer ceramic capacitors (MLCCs), they directly align with the global push for miniaturization and high-density circuit design. Modern smartphones incorporate 800–1,000 MLCCs, and electric vehicles require 20,000+ MLCCs, creating a scale of demand unmatched by any other electroceramic family. Their exceptionally high dielectric constant (1,000–10,000× greater than air) enables greater charge storage in shrinking volumes, supporting the aggressive reduction in PCB footprint across consumer electronics, automotive electronics, and 5G infrastructure. At the same time, dielectric ceramics offer high thermal stability (e.g., meeting X7R or C0G performance profiles) and low dielectric loss, which are essential for preventing heat buildup and maintaining energy efficiency in MHz-range power management circuits. These performance attributes directly reinforce their market share leadership, as OEMs favor materials that simultaneously enable miniaturization, reliability, and power efficiency. While Piezoelectric Ceramics and structural materials like alumina and zirconia continue to grow with sensorization trends and electronic packaging demand, their scale remains significantly smaller, reinforcing dielectric ceramics as the backbone of the electroceramics market.

Market Share by Application: Consumer Electronics Lead Through Massive Device Production and High MLCC Consumption

Consumer Electronics command the highest 35% application share, driven by the segment’s unparalleled production volumes and continuous need for high-performance passive components. The global electronics sector ships billions of devices annually, including smartphones, wearables, earbuds, tablets, smart home devices, and portable gaming systems—each requiring hundreds to thousands of MLCCs, piezo devices, substrates, and insulating components manufactured from electroceramics. The sector’s emphasis on device miniaturization, where manufacturers work toward annual reductions in device thickness and PCB size, accelerates the integration of thin-film and high-density ceramic components that support compact power circuits and high-frequency signal processing. As switching frequencies in PMICs continue climbing into the MHz range, electroceramics become indispensable due to their fast charge–discharge capability, thermal stability, and extremely low ESR/ESL characteristics that support rapid power filtering. This positions the Consumer Electronics segment as the most intensive user of electroceramics worldwide. While automotive electronics, medical devices, and industrial automation are expanding rapidly—especially with EV adoption and ultrasound imaging growth—the sheer scale and replacement frequency of consumer devices sustain its leading market share and reinforce its long-term dominance in electroceramics demand.

Country Analysis: Global Electroceramics Innovation Hubs

China: Manufacturing Powerhouse Accelerating 5G Ceramic Filters and Lead-Free Piezoelectric Technologies

China maintains a commanding position in the global electroceramics market, fueled by its vast electronics manufacturing ecosystem and aggressive push for technological self-reliance under the “Made in China 2025” strategy. The country’s rapid deployment of 5G base stations and high-frequency communication infrastructure is driving extraordinary demand for dielectric ceramic filters, resonators, and RF components essential for ultra-fast signal processing. As these deployments scale, domestic manufacturers are intensifying R&D in high-purity alumina and zirconia ceramics used for advanced semiconductor packaging and next-generation high-frequency devices. A notable trend is China’s accelerated transition toward lead-free piezoelectric materials, particularly KNN-based ceramics, to align with global environmental regulations while sustaining high electromechanical coupling efficiencies.

China’s leadership in electric vehicle manufacturing—representing the world’s largest EV market—is pushing local suppliers to bolster capacity for multilayer ceramic capacitors (MLCCs), ferroelectric ceramics, and thermal-stable components required in high-voltage battery management systems and on-board charging units. Additionally, the country is making significant investments in additive manufacturing (3D printing) of technical ceramics, enabling complex electroceramic geometries for aerospace, robotics, and industrial automation while reducing material waste. China is also strengthening its upstream security by tightening control over raw materials, particularly high-purity barium titanate and niobium oxides, ensuring stable supply chains for high-performance electroceramic components. Together, these advances solidify China’s role as the largest and fastest-growing center for electroceramic innovation and production.

Japan: Global Leader in MLCC Miniaturization, Functional Ceramics, and High-Frequency Device Materials

Japan remains the pinnacle of global innovation in functional ceramics, MLCC miniaturization, and high-reliability materials for advanced telecommunications, EV power electronics, and aerospace systems. In February 2025, Kyocera Corporation unveiled a breakthrough series of high-frequency ceramic substrates engineered with enhanced dielectric performance and superior thermal dissipation, tailored specifically for 6G communications, AI server cooling, and high-speed computing architectures. Strategic expansion accelerated in March 2024 when Kyocera acquired H.C. Starck Ceramics for an estimated $320 million, significantly expanding access to premium Aluminium Nitride (AlN) substrates critical for SiC-based power modules used in next-generation electric vehicles and renewable energy systems. Japan’s leadership is further cemented through its pioneering work in ceramic solid-state electrolytes—notably garnet-type structures—for safer and higher-capacity solid-state batteries (SSB).

Japan’s electroceramics ecosystem thrives on its deep integration with defense, aerospace, and high-frequency markets. Companies such as Murata Manufacturing continue to lead in mission-critical piezoelectric materials, radar filters, and precision resonators, leveraging decades of advanced materials engineering expertise. Japanese manufacturers are also setting global benchmarks in MLCC innovation by radically shrinking component size while increasing capacitance, requiring unparalleled control over ferroelectric microstructures (e.g., PZT and advanced dielectric composites). Supporting this, Japan’s Moonshot R&D Program funds high-risk, high-impact ceramic innovations designed for extreme environments, energy harvesting, and ultra-high-frequency applications—reinforcing the country’s position as the undisputed epicenter of high-end electroceramics.

United States: Reshoring Aluminium Nitride Production and Advancing Defense-Grade Electroceramics

The United States is intensifying its efforts to secure domestic production of strategic electroceramics, especially Aluminium Nitride (AlN) substrates crucial for high-power GaN devices used in defense, aerospace, and next-generation power electronics. Federal incentives linked to the CHIPS Act, along with defense-funded procurement programs, are accelerating the reshoring of critical ceramics manufacturing, reducing dependency on foreign supply chains. The U.S. remains one of the world’s largest consumers of piezoelectric sensors, actuators, and resonators for military equipment, missiles, aircraft guidance systems, and high-vibration aerospace environments—applications that necessitate the highest performance and reliability standards.

Corporate expansion further strengthens the domestic ecosystem, highlighted by Morgan Advanced Materials’ May 2024 acquisition of ElectroCeramics LLC (estimated at $140 million), expanding U.S. capabilities in LED substrates, engineered ceramics, and thermal management components. Academic collaborations funded by the National Science Foundation (NSF) are accelerating the development of lead-free piezoelectric materials engineered to match or exceed traditional PZT performance. The rise of domestic EV manufacturing is driving innovation in ultra-high-thermal-conductivity dielectric ceramics designed to withstand extreme heat generated in modern power modules. Meanwhile, American research centers are advancing Structural Health Monitoring (SHM) technologies using piezoelectric wafer active sensors embedded into bridges, aerospace structures, and large-scale civil infrastructure—paving the way for intelligent, self-monitoring smart systems.

South Korea: High-Frequency Ceramics and EV-Centric MLCC Innovations for 5G/6G Growth

South Korea is rapidly emerging as a key innovation hub for 5G/6G electroceramics, advanced MLCCs, and EV battery components, driven by world-class electronics and automotive industries. The national focus on strengthening domestic production capabilities for electroceramics is supported by government-backed innovation grants and strategic investments aligned with Korea’s expanding semiconductor and telecom leadership. Korean manufacturers are scaling production of high-grade zirconia, alumina, and piezoelectric ceramics used in biomedical devices, RF components, and high-precision sensors for consumer electronics.

Automotive demand is a powerful accelerant, particularly through companies like Samsung Electro-Mechanics (SEMCO), which continues to expand capacity for high-reliability automotive MLCCs capable of withstanding extreme voltage and temperature fluctuations in EV propulsion systems. South Korean research institutions are also spearheading the development of high-permittivity dielectric ceramics to support miniaturized antenna modules and advanced RF front-end architectures. In semiconductor manufacturing, the country is prioritizing next-generation ceramic substrates engineered for enhanced thermal management and electrical performance in densely packed chipsets. As global demand for miniaturized, thermally stable, and high-frequency ceramic components grows, South Korea’s innovation ecosystem positions it as a leading supplier to the world’s most advanced electronics markets.

Germany: Precision Electroceramics for Industrial Automation, EV Sensors, and Advanced Manufacturing

Germany leverages its internationally renowned precision engineering capabilities and robust industrial automation sector to drive high-performance electroceramics development. German engineering firms are major adopters and developers of precision piezoelectric actuators, including stack and shear actuators essential for micro-dispensing, robotic alignment, and high-speed manufacturing processes where extreme accuracy is non-negotiable. The country is expanding its advanced materials capabilities through acquisitions such as CeramTec’s November 2023 purchase of AluCeram Technologies (valued at approximately $130 million), enabling integration of low-temperature sintering IP—a crucial step toward reducing energy-intensive ceramic fabrication costs while maintaining purity and density requirements.

Germany’s automotive sector continues to stimulate demand for custom piezoelectric sensors used in advanced driver-assistance systems (ADAS), hybrid powertrain monitoring, and precision engine management. Simultaneously, German R&D institutions are pioneering next-generation ferroelectric nanocomposites, unlocking enhanced dielectric and ferroelectric properties suitable for flexible electronics and high-density capacitors. Innovation also extends to energy generation, with researchers integrating piezoelectric energy harvesters into industrial systems to convert mechanical vibration into electrical power for IoT devices and wireless sensor networks. Supported by the Fraunhofer Institutes and leading technical universities, Germany remains a cornerstone of high-performance electroceramics for industrial, automotive, and advanced manufacturing applications.

Competitive Landscape: Strategic Evolution of Global Electroceramics Leaders

The competitive landscape of the Electroceramics Market is defined by aggressive capacity expansion, continual R&D investment, and the pursuit of materials innovations that support high-reliability electronics across 5G networks, EVs, AI servers, medical devices, and industrial automation systems. Market leaders are scaling capabilities in dielectric ceramics, piezoelectric materials, solid-state electrolytes, magnetic ceramics, LTCC platforms, and semiconductor-grade substrates. Each company is shaping its portfolio to address the rising complexity of power electronics, high-frequency communications, and miniaturized electronics.

Murata maintains its dominant position in the global MLCC market by delivering advanced dielectric ceramic materials optimized for 5G, IoT, and automotive electronics. The company’s innovation focus lies in boosting volumetric efficiency while shrinking form factors, allowing electronic devices to support higher power densities without compromising stability. Murata continues to lead miniaturization through its latest high-voltage MLCC series introduced in January 2025, specifically engineered for high-frequency base stations and compact medical systems.

Kyocera remains a pivotal supplier of fine ceramic components essential for semiconductor packaging, AI accelerators, EV systems, and next-generation data centers. The company expands its presence across Asia-Pacific, particularly India, to meet rising demand for ADAS electronics, power modules, and smart metering systems. Its September 2025 product showcase highlighted high-reliability ceramic packages tailored for server CPUs and mission-critical data infrastructure—cementing Kyocera’s role in advanced electronics ecosystems.

TDK continues to act as a major catalyst in magnetic ceramic innovation, supplying ferrites, inductors, piezoelectric ceramics, and sensor components used across automotive and industrial power systems. With strong integration capabilities in high-frequency filtering and power management, the company focuses on enhancing reliability for EV powertrains and industrial automation. TDK’s expansion of MLCC production capacity in April 2025 demonstrates its strategic alignment with global electrification and semiconductor growth.

CoorsTek specializes in engineered ceramic solutions tailored for high-temperature, high-wear, and high-voltage environments across aerospace, defense, semiconductor fabrication, and medical sectors. The company leverages proprietary alumina, zirconia-toughened alumina, and advanced ceramic formulations to deliver components capable of withstanding extreme operational stresses. Through continuous portfolio diversification and strategic acquisitions, CoorsTek expands its global manufacturing reach and reinforces its position in the engineered electroceramics market.

CeramTec holds a leading position in precision electroceramics used in medical implants, ultrasonic transducers, and industrial sensing systems. Its acquisition in May 2025 of a U.S. piezoelectric sensor provider strengthened its capabilities in medical imaging and smart sensing technologies. The company adheres to stringent European quality standards, ensuring reliability and high performance across clean energy equipment, surgical devices, and precision industrial instruments.

Samsung Electro-Mechanics continues to push the boundaries of MLCC miniaturization, developing ultra-small, high-capacitance components for premium smartphones, EVs, and 5G modules. The company aligns closely with South Korea’s national ceramic R&D initiatives, reinforcing supply chain stability for semiconductor materials. With strong substrate and MLCC portfolios, Samsung EM plays a critical role in meeting the surging demand for high-reliability components in advanced consumer and automotive electronics.

Electroceramics market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$14.9 Billion

|

|

Market Size (2035)

|

$24 Billion

|

|

Market Growth Rate

|

4.9%

|

|

Segments

|

By Material Type (Dielectric Ceramics, Piezoelectric Ceramics, Ferroelectric Ceramics, Solid-State Electrolytes, Ionic Conductive Ceramics, Alumina/Zirconia Ceramics), By End-Product (MLCCs, Actuators, Sensors, Filters & Resonators, Power Devices, Transducers, Solid-State Batteries), By Application (Consumer Electronics, Automotive, Telecommunications, Industrial Automation, Aerospace & Defense, Medical Devices), By Structure/Form (Bulk Ceramics, Thin Films, Thick Films, Powders/Nanoparticles, Composite Materials, Ceramic Substrates)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Murata Manufacturing Co. Ltd., Kyocera Corporation, TDK Corporation, CeramTec GmbH, Morgan Advanced Materials plc, CoorsTek Inc., Taiyo Yuden Co. Ltd., Samsung Electro-Mechanics Co. Ltd., CTS Corporation, PI Ceramic GmbH, NGK Insulators Ltd., Resonac, Littelfuse Inc., Vishay Intertechnology Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Electroceramics Market Segmentation

By Material Type

- Dielectric Ceramics (Barium Titanate, Titania, MLCC-Grade)

- Piezoelectric Ceramics (PZT, Lead-Free KNN, BTO)

- Ferroelectric Ceramics (BaTiO₃, PZT)

- Solid-State Electrolytes (Garnet-type, Perovskite-type)

- Ionic Conductive Ceramics (Zirconia, Ceria)

- Alumina/Zirconia Ceramics (Structural/Insulators)

By End-Product

- Multilayer Ceramic Capacitors (MLCCs)

- Actuators

- Sensors

- Filters & Resonators

- Power Devices

- Transducers

- Solid-State Batteries

By Application

- Consumer Electronics

- Automotive

- Telecommunications

- Industrial Automation

- Aerospace & Defense

- Medical Devices

By Structure/Form

- Bulk Ceramics

- Ceramic Thin Films

- Thick Films

- Powders/Nanoparticles

- Composite Materials

- Ceramic Substrates

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Electroceramics Market

- Murata Manufacturing Co., Ltd.

- Kyocera Corporation

- TDK Corporation

- CeramTec GmbH

- Morgan Advanced Materials plc

- CoorsTek, Inc.

- Taiyo Yuden Co., Ltd.

- Samsung Electro-Mechanics Co., Ltd. (SEMCO)

- CTS Corporation

- PI Ceramic GmbH

- NGK Insulators, Ltd.

- Hitachi Metals, Ltd. (Resonac)

- Littelfuse, Inc.

- Vishay Intertechnology, Inc.

*- List not Exhaustive