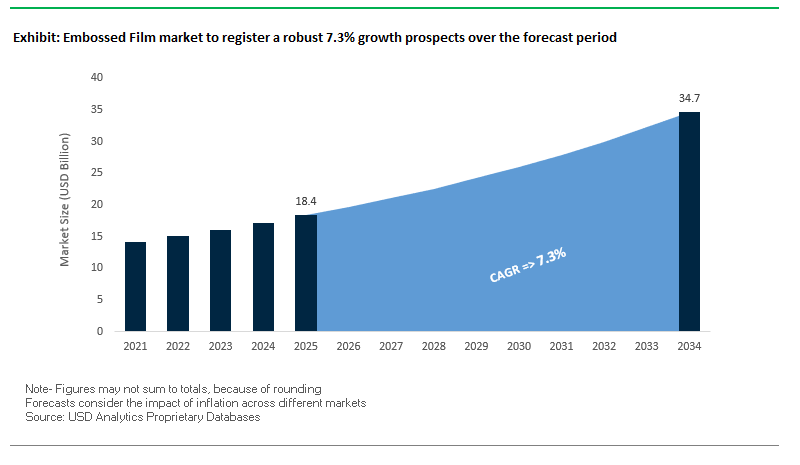

Market Overview: Embossed Film Market to Reach $34.7 Billion by 2034 at 7.3% CAGR

The global embossed film market is projected to expand from $18.4 billion in 2025 to $34.7 billion by 2034, reflecting a robust CAGR of 7.3%. Embossed films are increasingly valued for their dual role of visual appeal and functional performance, making them critical across packaging, automotive, hygiene, and personal care sectors. For industry professionals, the market is being reshaped by sustainability mandates, material science innovation, and enhanced end-use requirements.

Key Insights for decision-makers:

- Micro-embossing demand rising: Micro-embossed films dominate hygiene and medical applications, providing a natural touch and improved comfort compared to traditional embossing.

- Functionality beyond aesthetics: Over 50% of recent innovations in embossed films are focused on enhanced performance properties like adhesion control, anti-slip, light reflection, and anti-counterfeiting protection.

- Polyethylene leads materials: PE-based films are the backbone of innovation, particularly for industrial and chemical applications, where engineered performance is critical.

- Sustainability as a growth engine: Companies are pivoting to mono-materials, bio-based plastics, and recycled content to support the circular economy and align with global plastic reduction regulations.

Market Analysis: Strategic Expansions and Material Innovation Drive Global Growth

The embossed film industry is entering a transformative phase marked by strategic corporate moves, sustainability-driven innovations, and advanced production capabilities.

In August 2025, Mondi launched its Ad/Vantage Smooth Brown Semi Extensible paper, designed for industrial uses and serving as a base material for high-performance embossed films. This innovation highlights how new substrates are enabling better embossing textures and durability. Just a month earlier, in July 2025, Sigma Stretch Film announced a $39 million expansion in Georgia, U.S., building new facilities to scale its stretch and embossed film capacity, creating 100 jobs, and strengthening supply chains in North America.

Also in July 2025, Innovia Films launched new PPWR-compliant films, aligning with the EU Packaging and Packaging Waste Regulation, ensuring recyclable mono-material packaging solutions. Meanwhile, Jindal Poly Films approved a Scheme of Arrangement in the same month, signaling possible restructuring or business consolidation to enhance operational efficiency.

Earlier in June 2025, Mondi partnered with Saga Nutrition to develop sustainable embossed packaging for pet food, leveraging recyclability with custom textures for branding. At DRUPA 2024 (May 2025), Jindal Films displayed recyclable mono-material polypropylene solutions, emphasizing its sustainability-focused innovation pipeline. In April 2025, Innovia Films opened a new German production line equipped with LISIM technology, producing high-quality embossed films with superior mechanical performance.

On the restructuring front, Sonoco divested its Thermoformed and Flexibles division in December 2024 for $1.8 billion, refocusing capital on core industrial paper and consumer packaging, which include embossed film applications. Together, these developments illustrate how capacity expansion, regulatory compliance, and sustainable innovation are the central growth themes in the market.

Trends and Opportunities Reshaping the Embossed Film Market

Functional Performance Enhancement in Monomaterial Barrier Packaging

The embossed film market is undergoing a critical transformation as brand owners and converters pivot from multi-layer laminates toward recyclable monomaterial structures. Embossing has emerged as a strategic enabler, enhancing the barrier performance, stiffness, and handling properties of single-polymer films such as polyethylene (PE) and polypropylene (PP). This development is largely driven by the European Union’s Packaging and Packaging Waste Regulation (PPWR), effective from August 2026, which mandates that all packaging must be recyclable by 2030. To comply, manufacturers are investing in mono-material solutions while leveraging embossing to address functional gaps.

Research demonstrates that mechanical embossing can significantly improve the oxygen and water vapor barrier properties of recyclable films, making them suitable for sensitive food and pharmaceutical applications. Academic studies further reveal that embossing can reduce the surface friction of biopolymer blends, which improves machinability and handling. This is particularly important for high-speed automated packaging lines. Beyond barrier enhancement, embossed patterns add rigidity and grip, resulting in films that are more user-friendly and capable of withstanding demanding logistics environments. The result is a sustainable yet high-performance alternative to non-recyclable laminates, aligning with global sustainability mandates while preserving product protection.

Premiumization and Sensory Branding in Consumer Goods Packaging

In parallel, embossing is becoming a powerful marketing and branding tool in competitive consumer goods categories. Deep, tactile embossing on flexible films allows brands to differentiate through sensory appeal, creating a strong premium perception at the point of sale. Companies are commercializing embossed films with “paper-like” textures or luxury surface finishes, designed to elevate both the look and feel of packaging. These films are increasingly used in segments such as confectionery, personal care, and premium beverages, where packaging plays a direct role in influencing consumer purchase decisions.

Embossing also enhances visual aesthetics by integrating with advanced printing methods such as hot-stamping foil and holographic finishes. These techniques not only boost shelf appeal but also make the packaging more resistant to counterfeiting, as registered prints on embossed surfaces are difficult to replicate. Moreover, embossing allows brands to embed logos, icons, or storytelling motifs directly into the film, turning packaging into a tangible expression of brand identity. As consumer expectations shift towards luxury cues and sustainable value, embossing provides a unique convergence of functionality and brand-building capability.

Development of Embossed Biopolymer and Compostable Films

A significant opportunity for market expansion lies in biopolymer-based embossed films, where embossing can mitigate key performance limitations. While biopolymers such as PLA (polylactic acid) and PHA (polyhydroxyalkanoates) are inherently compostable, they often lack the durability, machinability, and barrier properties of traditional plastics. Embossing provides a practical solution by modifying surface properties to reduce stickiness, improve run-speed compatibility on automated lines, and enhance overall usability.

Academic research highlights that combining embossing with nanomaterial additives for example, embedding zinc oxide nanoparticles can significantly enhance the mechanical and thermal stability of biopolymer films. This dual approach not only improves durability but also enables biopolymers to compete with conventional plastics in performance-sensitive markets such as food packaging and personal care products. With strong regulatory and consumer pressure for compostable, PFAS-free, and plastic-free packaging, embossed biopolymer films represent a high-growth niche. Companies that commercialize solutions merging sustainability with high functionality will capture significant early-mover advantage.

Integration with Smart Packaging and Anti-Counterfeiting Features

Another major opportunity is the integration of embossing as a physical security and smart packaging feature. Micro-embossing technology allows the creation of microscopic text, patterns, or holographic surfaces that are nearly impossible to replicate using conventional printing techniques. For industries such as pharmaceuticals, luxury goods, and high-value food categories, this provides an effective anti-counterfeiting barrier.

Competitive Landscape: Key Players Driving Innovation in the Embossed Film Industry

The embossed film market is shaped by multinational packaging leaders and specialized film producers, competing on sustainability credentials, R&D pipelines, and global manufacturing networks.

Mondi plc Sustainability-Driven Embossed Film Leader

Mondi offers a broad portfolio of technical and functional embossed films for packaging, consumer goods, and industrial applications. Guided by its Mondi Action Plan 2030 (MAP2030), the company is innovating recyclable and bio-based films. Its recent launch of Ad/Vantage Smooth Brown Semi Extensible paper reinforces its role as a pioneer in material development. With a vertically integrated model spanning forestry, paper, and converting, Mondi ensures quality and traceability across the embossed film value chain.

Jindal Poly Films Limited Expanding with Mono-Material Innovation

Jindal Poly Films is a leading global producer of BOPP and PET films, offering embossed textures for flexible packaging and labeling. In July 2025, the company approved a Scheme of Arrangement, reflecting restructuring initiatives to strengthen competitiveness. At DRUPA 2024, Jindal showcased recyclable PP mono-material films, highlighting its strategic pivot toward sustainable flexible packaging. With production hubs in India and Europe, Jindal supports diverse global end-user needs.

Sigma Stretch Film Scaling U.S. Manufacturing with $39M Investment

Sigma Stretch Film specializes in stretch and embossed films for pallet wrapping and load stability. In July 2025, the company announced a $39 million expansion in Georgia, adding capacity and reducing lead times for North American customers. Sigma’s Rite-Gauging® program provides data-driven optimization, reducing film usage and waste while maintaining load security. Its focus on cost efficiency and sustainability positions it as a preferred supplier in logistics and industrial sectors.

Innovia Films Pioneering PPWR-Compliant Embossed Film Solutions

Innovia Films is a material science leader in BOPP and polyolefin films, widely used in labeling, flexible packaging, and security applications. In April 2025, the company inaugurated a new German line using LISIM technology, enabling advanced stretching and embossing capabilities. Its PPWR-compliant monomaterial films (July 2025) demonstrate regulatory foresight, helping European brands transition to recyclable packaging structures. Innovia’s Better Future strategy focuses on reducing carbon footprints and advancing circular economy materials.

Embossed Film market Share Insights

Packaging Applications Drive Largest Share in Embossed Film Market

In the embossed film market, packaging applications command 40% of the share in 2025, reflecting their dual role in food, beverage, and personal care products where embossing enhances grip, reduces film blocking, and elevates shelf appeal. Medical and hygiene follow with 25%, driven by diapers, incontinence products, and sterile medical pouches, where embossed textures improve functionality and user experience. Industrial tapes and liners, automotive interiors, and building & construction together make up the remaining share, each leveraging embossing for performance attributes like air egress, premium textures, and surface protection. The dominance of packaging and hygiene underscores how embossed films are positioned as both aesthetic enhancers and functional enablers, bridging consumer-facing differentiation with performance-driven industrial applications.

Mid-Range Thickness Leads Market Share by Film Category

By thickness, films in the 51–200 micron range capture 50% of the embossed film market in 2025, establishing themselves as the versatile workhorse across packaging, hygiene, and industrial applications. This segment strikes the balance between durability and cost, enabling deep embossing patterns without sacrificing flexibility. Thinner films below 50 microns serve cost-sensitive, high-volume packaging needs, while thick-gauge films above 200 microns cater to heavy-duty construction membranes and automotive interiors requiring superior strength and puncture resistance. The segmentation highlights how the mid-range category dominates mainstream adoption, while thinner and thicker films address specialized, niche demands that reinforce embossing’s adaptability across industries.

United States: Automotive and Personal Care Drive Embossed Film Innovation

The U.S. embossed film market is heavily driven by applications in the automotive and personal care sectors. In the automotive industry, embossed films are widely used for interior trims, dashboards, and door panels, enhancing both aesthetics and tactile appeal. Meanwhile, the personal care and hygiene segment leverages non-slip embossed films for packaging and premium product feel, offering differentiation in competitive markets.

Technological innovation is a major growth driver in the U.S., with manufacturers employing advanced extrusion and embossing processes to achieve precise patterns with depths ranging from 15 to 300 microns, ideal for high-end applications such as synthetic leather and luxury packaging. Sustainability is also a key trend, as companies integrate post-consumer recycled (PCR) content and explore bio-based alternatives, reducing the environmental footprint of embossed film production while meeting consumer demand for eco-friendly materials.

Germany: Industrial and Automotive Excellence Shaping Embossed Film Demand

Germany’s embossed film market is closely tied to its industrial and automotive sectors, where high-quality, durable, and visually appealing films are in high demand. Vehicle interiors and industrial applications require films that meet strict performance, durability, and aesthetic standards, supporting the country’s reputation for precision manufacturing.

Stringent EU regulations on environmental impact and product safety further drive innovation, encouraging manufacturers to develop recyclable films with controlled material composition. Strategic investments in automation and advanced production lines enhance manufacturing efficiency while enabling the production of embossed films with superior barrier properties, reinforcing Germany’s position as a European leader in high-value embossed film solutions.

China: Manufacturing Powerhouse Fuels Global Embossed Film Supply

China has established itself as a global manufacturing and export hub for embossed films, catering to both domestic and international demand. The country’s large-scale production supports critical applications such as cargo security for sea and rail transport, industrial packaging, and export logistics.

Domestic demand is rapidly growing due to the expansion of automotive and construction sectors, where embossed films are used for vehicle interiors, decorative laminates, and flooring applications. Manufacturers focus on delivering cost-effective and versatile solutions, utilizing polyethylene and polypropylene films with varied thicknesses and patterns to meet diverse industrial needs. China’s combination of high-volume manufacturing, affordability, and versatility ensures its continued dominance in the global embossed film market.

India: Domestic Growth and Specialized Applications Expand Market Potential

India’s embossed film industry is emerging strongly, supported by domestic manufacturers such as Alpha Plastomers and Daman Polymers, producing films for applications ranging from rubber processing to tire manufacturing. The market is witnessing innovation in specialized embossing patterns, such as diamond-shaped textures that improve air removal during rubber calendering, an essential process in tire production.

Customization is a key competitive advantage in India, with manufacturers offering films in varied colors, thicknesses, and embossing patterns to meet diverse customer requirements. This focus on flexibility, specialized applications, and domestic manufacturing capability positions India as a growing and strategic player in the global embossed film market.

Embossed Film Market Report Scope

Embossed Film market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$18.4 Billion

|

|

Market Size (2034)

|

$34.7 Billion

|

|

Market Growth Rate

|

7.3%

|

|

Segments

|

By Material Type (Polyethylene, Polypropylene, Polyethylene Terephthalate, Polyvinyl Chloride, Others), By Application (Packaging, Automotive Interiors, Building & Construction, Industrial Tapes & Liners, Medical & Hygiene, Other Applications), By Embossing Pattern (Diamond, Square, Other Patterns), By Thickness (Below 50 microns, 51-200 microns, Above 200 microns)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Sealed Air Corporation, Berry Global, Inc., Amcor plc, Jindal Poly Films Ltd., Uflex Ltd., Cosmo Films Ltd., Novolex Holdings, LLC, Coveris Holdings S.A., Mondi Group, Klöckner Pentaplast Group, Toray Plastics (America), Inc., Aintree Plastics Ltd., Sigma Plastics Group, Inteplast Group Corporation, Polyplex Corporation Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Embossed Film market Segmentation

By Material Type

- Polyethylene

- Polypropylene

- Polyethylene Terephthalate

- Polyvinyl Chloride

- Others

By Application

- Packaging

- Automotive Interiors

- Building & Construction

- Industrial Tapes & Liners

- Medical & Hygiene

- Other Applications

By Embossing Pattern

- Diamond

- Square

- Other Patterns

By Thickness

- Below 50 microns

- 51-200 microns

- Above 200 microns

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Embossed Film market

- Sealed Air Corporation

- Berry Global, Inc.

- Amcor plc

- Jindal Poly Films Ltd.

- Uflex Ltd.

- Cosmo Films Ltd.

- Novolex Holdings, LLC

- Coveris Holdings S.A.

- Mondi Group

- Klöckner Pentaplast Group

- Toray Plastics (America), Inc.

- Aintree Plastics Ltd.

- Sigma Plastics Group

- Inteplast Group Corporation

- Polyplex Corporation Ltd.

*List not Exhaustive

Research Coverage

This report investigates the global embossed film market, exploring technological breakthroughs, sustainability-driven innovations, and performance enhancements that are transforming applications across packaging, automotive, hygiene, and personal care sectors. USDAnalytics’ analysis reviews advances in mono-material and biopolymer films, micro-embossing for sensory and anti-counterfeiting purposes, and high-performance barrier films, highlighting their impact on product protection, machinability, and end-user experience. This report is an essential resource for packaging engineers, R&D specialists, production managers, and sustainability officers seeking actionable insights on market dynamics, regulatory compliance, and competitive strategies. It emphasizes recent corporate expansions, capacity-building initiatives, and regulatory-aligned innovations that are shaping global supply chains. Furthermore, it covers functional performance enhancements through embossing, premiumization and tactile branding, and the development of compostable and biopolymer-based embossed films, providing a detailed understanding of trends driving adoption in consumer and industrial segments. By incorporating historical data from 2021 to 2024 and forecasting trends through 2034, the study offers a comprehensive perspective on material preferences, application shifts, and technological adoption across leading companies in the sector.

Scope Highlights:

- Segmentation: By Material Type (Polyethylene, Polypropylene, Polyethylene Terephthalate, Polyvinyl Chloride, Others); By Application (Packaging, Automotive Interiors, Building & Construction, Industrial Tapes & Liners, Medical & Hygiene, Other Applications); By Embossing Pattern (Diamond, Square, Other Patterns); By Thickness (Below 50 microns, 51–200 microns, Above 200 microns)

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa

- Historical & Forecast Data: Historic data from 2021 to 2024 and forecast data from 2025 to 2034

- Companies Covered: Profiles and analysis of 15+ companies, including Sealed Air Corporation, Berry Global, Inc., Amcor plc, Jindal Poly Films Ltd., Uflex Ltd., Cosmo Films Ltd., Novolex Holdings, LLC, Coveris Holdings S.A., Mondi Group, Klöckner Pentaplast Group, Toray Plastics (America), Inc., Aintree Plastics Ltd., Sigma Plastics Group, Inteplast Group Corporation, Polyplex Corporation Ltd.

Methodology

This study employs a comprehensive methodology combining primary and secondary research to generate accurate, actionable insights into the embossed film market. Primary research included interviews with packaging engineers, production managers, material scientists, and sustainability officers to validate market trends, performance specifications, and adoption rates of mono-material and biopolymer films. Secondary research incorporated company annual reports, patent databases, regulatory filings, industry whitepapers, and trade publications to assess technological innovations, embossing techniques, and global expansion initiatives. Market sizing and forecasting were conducted using top-down and bottom-up approaches, considering production capacities, regional consumption trends, and regulatory mandates such as the EU Packaging and Packaging Waste Regulation (PPWR). Competitive benchmarking evaluates mergers, acquisitions, capacity expansions, and sustainability credentials. USDAnalytics ensures all insights are cross-verified, delivering precise guidance for industry professionals aiming to optimize operations, enhance product differentiation, and comply with evolving sustainability requirements.

Deliverables:

• Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

• Country-Specific Forecasts & Analysis.

• Segment-Wise Revenue Forecasts (2025–2034).

• Competitive Analysis, Benchmarking, and SWOT Profiles.

• Recent Developments & Innovation Tracker.

• Executive Summary & Analyst Commentary.

• Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.