Energy Efficient Materials Market Overview: Aerogels, VIPs and Advanced Insulation Accelerating to USD 61.7 Billion

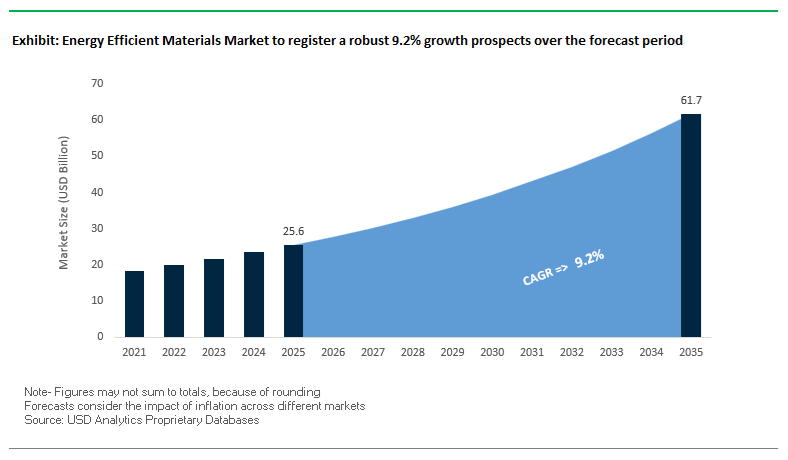

The global Energy Efficient Materials Market is projected to grow from USD 25.6 billion in 2025 to USD 61.7 billion by 2035, registering a robust CAGR of 9.2% (2025–2035). This growth is underpinned by aggressive building energy codes, electrification of infrastructure, and the thermal management needs of AI data centers, cold-chain logistics, and high-efficiency appliances. For manufacturers and vendors of insulation, aerogels, VIPs, and phase change materials, this market is shifting from niche, high-spec applications to mainstream building envelope and industrial process retrofits. Players that can balance ultra-low thermal conductivity, low embodied carbon, and cost-effective installation are best positioned to capture specification in next-generation building codes and OEM platforms.

Key technical and commercial insights for manufacturers and vendors include:

- Silica aerogels as premium insulation: Silica aerogel blankets with ultra-low thermal conductivity (~0.024 W/(m·K) at 20°C) enable ultra-thin, high-performance insulation for pipelines and building envelope retrofits where space is constrained.

- Fiberglass remains the baseline benchmark: Standard fiberglass batt insulation delivering R-3.0 to R-3.5 per inch remains the reference material for code compliance in residential and commercial construction, forcing new materials to demonstrate clear R-value and cost advantages.

- PCMs unlocking thermal storage in envelopes: Phase change materials with latent heat of fusion >120 kJ/kg allow thin layers to replicate the thermal inertia of thicker concrete, enabling peak cooling load reduction and enhanced NZEB performance.

- VIPs for extreme space-constrained applications: Vacuum insulated panels, offering 5–10x higher insulation efficiency than conventional materials, are becoming critical in refrigeration, cold-chain packaging, and compact high-performance building systems.

Energy Efficient Materials Market Analysis: NZEB Policies, Data Centers and Thermal Management Investments

Policy, capex, and M&A activity between 2024 and 2025 underline how energy efficient materials are moving from compliance-driven choices to strategic assets. In January 2024, researchers at MIT demonstrated a smart window coating capable of dynamically modulating solar heat gain (SHGC) by over 70%, reinforcing the role of advanced coatings and glazing as front-line levers for façade efficiency and daylight harvesting. In April 2025, the European Commission’s updated Energy Performance of Buildings Directive (EPBD) mandated that all new public buildings be Nearly Zero-Energy Buildings (NZEB) by 2026, directly accelerating demand for high-performance insulation, aerogels, VIPs, PCMs and low-emissivity glazing solutions across the EU institutional and commercial stock.

On the corporate strategy side, building products majors and advanced insulation specialists are restructuring portfolios around energy efficiency. In February 2025, Owens Corning’s divestiture of its Glass Reinforcements Business to Praana Group signaled a sharper focus on core insulation and roofing systems optimized for whole-building energy performance. In October 2024, Aspen Aerogels launched its next-generation Cryogel product targeting LNG and cryogenic pipelines, reducing thermal bridging and improving thermal protection for energy infrastructure—a critical differentiator as midstream operators chase lower boil-off and CO₂ intensity. Concurrently, a large Chinese VIP manufacturer expanded production capacity by 30% in March 2025, driven by surging demand from refrigerator OEMs and cold-chain logistics firms seeking higher Energy Star ratings and reduced panel thickness.

Thermal management for AI and cloud data centers is emerging as a new anchor demand segment. In November 2025, Jabil agreed to acquire Hanley Energy Group, aligning advanced enclosure design with liquid cooling solutions for AI data centers that rely on high-performance thermal interface materials, foams, and insulation assemblies. This was followed by a USD 500 million US manufacturing investment announced in June 2025, explicitly linked to supporting cloud and AI infrastructure, cementing energy efficient materials as a core enabler of digital economy uptime and power usage effectiveness (PUE) optimization. Meanwhile, Saint-Gobain’s September 2025 commitment to allocate around €100 million per year to net-zero and low-carbon materials R&D through 2030 underscores how energy efficient materials are converging with decarbonized chemistry, creating dual value propositions: lower operational energy and lower embodied carbon.

Breakthrough Thermal Management Materials and Next-Generation Energy Storage Innovations Accelerating Market Adoption

Market Trend 1: Mandatory Use of Vacuum Insulation Panels (VIPs) as Building Codes Push Ultra-Low Energy Performance Standards

Regulatory pressure to meet Passive House, Net-Zero Energy Building (NZEB), and nearly zero-energy construction mandates is rapidly increasing the reliance on Vacuum Insulation Panels (VIPs) as the next-generation high-performance insulation standard. VIPs achieve a central thermal conductivity of just 0.004–0.007 W/(m·K)—a level 3–6 times more insulating than polyurethane foam (≈0.024 W/(m·K)) and far superior to mineral wool (≈0.044 W/(m·K)). As a result, they deliver an R-value of R-25 to R-30 per inch, compared to only R-4.5–R-5.0 per inch for premium XPS foams, giving VIPs unmatched thermal efficiency in space-constrained applications.

To meet an R-40 wall requirement, VIP assemblies typically require only 10–30 mm total thickness, whereas traditional insulation materials need 3–6 times more thickness, significantly improving architectural space utilization in urban buildings. VIPs also offer a certified service life of ~25 years, with aged lambda values validating long-term performance. This combination of extreme thermal resistance, minimal thickness, and durability is making VIPs indispensable in advanced building envelopes for deep energy retrofits, cold-storage facilities, high-performance façades, and modular construction systems.

Market Trend 2: Rapid Commercialization of Dynamic Radiative Cooling (DRC) Coatings for Zero-Energy Building Skin Temperature Management

Dynamic Radiative Cooling (DRC) coatings and films represent one of the most disruptive material technologies in the energy-efficient materials landscape. Passive Daytime Radiative Cooling (PDRC) materials have demonstrated sub-ambient temperature drops averaging 5.5°C, with some achieving up to 9.8°C under full sunlight—crucial for reducing building cooling loads without external power. This high performance is driven by near-ideal optical characteristics:

- Solar reflectance ≥96% across the 0.3–2.5 μm spectrum

- Atmospheric window emissivity ≥97% in the 8–13 μm range

Such coatings routinely achieve net cooling power of 72–150 W/m², even during peak solar irradiance (~1,000 W/m²), effectively lowering HVAC demand in commercial and residential buildings.

Emerging DRC systems add another dimension by dynamically modulating their emissivity—shifting from ε≈0.9 (cooling) to ε≈0.2 (heat retention) using a small electrical or thermal signal. This enables real-time switching between radiative cooling and thermal conservation, unlocking a pathway toward smart building skins integrated into energy-autonomous façades and adaptive thermal envelopes. As global energy codes increasingly emphasize passive cooling solutions, DRC technologies are poised to become a cornerstone of sustainable architecture.

Market Opportunity 1: High-Temperature Insulating Materials (HTIMs) Enabling Industrial Electrification and Decarbonization

Industrial decarbonization strategies hinge on the electrification of high-temperature processes, creating substantial opportunities for advanced High-Temperature Insulating Materials (HTIMs). Ceramic fiber insulation remains one of the most effective HTIMs, achieving ultra-low thermal conductivity below 0.1 W/(m·K) at high service temperatures. Next-generation ceramic fibers operate reliably at up to 1,260°C, while premium carbon-based insulators remain stable at up to 3,200°C in non-oxidizing environments, making them indispensable for electric furnaces, hydrogen-ready kilns, metal processing, and glass manufacturing.

Upgrading furnace linings with advanced HTIMs can reduce shell temperatures by 100–200°C, dramatically cutting radiant heat loss while improving worker safety. Layered refractory solutions with HTIMs deliver fuel cost reductions of 15–25%, demonstrating direct, quantifiable improvements in process efficiency. As industries move toward zero-emission thermal processes, the need for materials that combine low conductivity, high thermal shock resistance, and long service life will accelerate HTIM adoption across heavy industry.

Market Opportunity 2: Phase Change Materials (PCMs) Integrated with Building Management Systems for Intelligent Thermal Storage

Phase Change Materials (PCMs) are unlocking new opportunities in active thermal storage, especially when integrated with building management systems (BMS). PCMs deliver significantly higher latent heat storage capacity than conventional sensible storage media, enabling compact thermal batteries for peak-shaving and load shifting. When integrated into heat pump systems and optimized via BMS algorithms, PCMs can achieve a 23.5% reduction in peak electrical load, enhancing both energy cost savings and grid flexibility.

Commercial PCM storage modules demonstrate large-scale capabilities—1.2 m³ PCM systems can discharge ~52 kWh of cooling energy, with a rapid 32.58 kW discharge rate during the first 30 minutes, effectively supporting sudden cooling spikes in commercial buildings. Enhancing PCM thermal conductivity from 0.2 to 0.6 W/(m·K) through engineered fillers increases system performance by over 3.5×, enabling rapid charge/discharge cycles essential for HVAC optimization.

As buildings transition into grid-interactive efficient buildings (GEBs), PCM-BMS integration is emerging as a critical technology for flexible energy storage, peak demand reduction, and HVAC load optimization.

Energy Efficient Materials Market Share Analysis

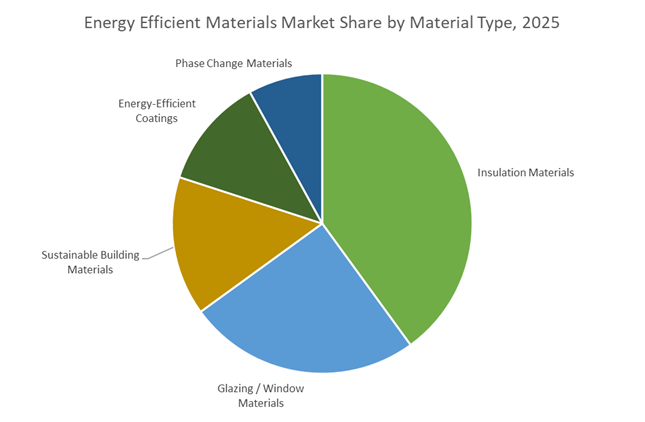

Market Share by Material Type: Insulation Materials Lead Due to Their Foundational Role in Reducing Building Energy Consumption

Insulation materials hold the largest share of the global energy-efficient materials market—approximately 40% in 2025—because they remain the most impactful and widely deployed solution for reducing heat transfer across building envelopes, which account for the majority of global heating and cooling energy losses. Materials such as fiberglass, mineral wool, EPS, XPS, spray polyurethane foam, and advanced solutions like aerogels and vacuum insulation panels (VIPs) directly improve thermal resistance (R-value) and lower U-factors, making them essential for meeting modern energy-efficiency codes. Their unparalleled ability to decrease HVAC loads by 20–40% creates immediate reductions in operational energy use and carbon emissions, aligning with government policies promoting green buildings and net-zero performance targets. Insulation is also one of the highest-volume materials used in the construction sector, integrated across walls, roofs, floors, mechanical systems, and building envelopes in both new construction and retrofits. As global regulatory frameworks—such as the EU’s EPBD, U.S. IECC compliance pathways, and Asia-Pacific’s tightening building efficiency standards—continue to elevate minimum thermal performance requirements, insulation materials remain the primary driver of revenue, volume, and adoption within the overall energy-efficient materials landscape.

Market Share by End-User Sector: Construction & Buildings Dominate Due to Massive Energy Use and Regulatory Pressures

The Construction & Buildings sector accounts for nearly 70% of the global energy-efficient materials market, driven by the sector’s disproportionate share of global energy consumption and the accelerating policy push toward climate-resilient, low-energy building infrastructure. Buildings represent 30–40% of global final energy use, with heating, cooling, and ventilation making up the largest portion, creating an urgent need for envelope-enhancing materials such as insulation, high-performance glazing, reflective and low-emissivity coatings, and sustainable building materials. With governments enforcing stringent performance codes, energy disclosure mandates, and carbon-neutral building frameworks, developers and property owners are prioritizing high-efficiency materials for both new projects and large-scale retrofits of aging building stock. The transition to green buildings, supported by LEED, BREEAM, DGNB, and national ECBC standards, further amplifies demand across commercial, residential, and institutional infrastructure. Because energy-efficient materials are integral across walls, roofs, facades, windows, and HVAC systems, the construction sector consumes the highest volume and variety of these materials—cementing its status as the dominant and most strategically important end-user sector in the global market.

Country Analysis: Global Drivers in Energy Efficient Materials Development

United States: Incentive-Backed Retrofits, PCM Deployment, and High-Value Thermal Management Materials

The United States remains one of the strongest global growth engines for the Energy Efficient Materials Market, driven by powerful federal policies, accelerated building envelope retrofits, and rapid commercialization of advanced thermal management materials. The Inflation Reduction Act (IRA) continues to be the single most influential driver, extending the 30% Investment Tax Credit (ITC) for clean energy systems under 1 MW, which includes Building Integrated Photovoltaics (BIPV), high-efficiency insulation, and thermal storage innovations. On the residential side, direct tax credits for energy efficient materials—spanning advanced insulation, Energy Star window systems, and high-performance heat pumps—have fueled a surge in demand for cost-effective, low-energy building upgrades across the U.S. construction sector.

A major national shift is also underway toward geothermal and electrification-based heating and cooling applications. The U.S. Department of Energy (DOE) launched new funding in 2024 to accelerate geothermal heat pump deployment, reinforcing demand for efficient materials used in heat exchangers, ground loops, and distribution systems. The U.S. is simultaneously emerging as a global leader in Phase Change Material (PCM) integration, with manufacturers embedding PCM-enhanced drywall and insulation boards in commercial buildings. These materials provide passive thermal energy storage, enabling peak cooling load shifting—a strategy the DOE projects could save up to 1.5 quadrillion BTUs annually by 2030. This combination of policy incentives, R&D momentum, and large-scale adoption in retrofits solidifies the U.S. as a prime contributor to innovation in energy efficient building materials, BIPV systems, and next-generation thermal management technologies.

European Union: Green Deal Compliance, Low-GWP Insulation, and Data Center Efficiency Mandates

The European Union remains the regulatory epicenter of the Energy Efficient Materials Market, driven by sweeping climate mandates that directly reshape building material procurement and industrial energy efficiency strategies. The revised Energy Efficiency Directive (EED) enforces the “energy efficiency first” principle and mandates at least 1.3% annual end-use energy savings for 2024–2025, compelling member states to prioritize high-performance building envelope materials such as insulated façades, low-U-value glazing, and next-generation reflective coatings. These requirements are backed by the EU’s broader Green Deal framework, which pushes decarbonization across commercial, residential, and public infrastructure.

Starting July 2025, new EU legislation requires large data centers to disclose detailed energy performance metrics, driving investment in high-efficiency cooling materials, advanced thermal interface technologies, and energy-optimized insulation. Meanwhile, environmental directives are accelerating the transition to low-GWP insulation materials, forcing producers like Saint-Gobain and Knauf to re-engineer XPS and PU foam lines using sustainable blowing agents. The EU’s evolving district heating rules—specifically the post-2030 ban on new fossil fuel capacity in efficient networks—are catalyzing demand for high-performance insulated pipes, cladding, and thermal distribution materials. Europe’s highly structured regulatory ecosystem ensures continuous, large-scale demand for high-specification energy efficient materials across both new construction and deep retrofit programs.

China: Zero-Carbon Building Standards, BIPV Scaling, and Microencapsulated PCM Innovation

China has become one of the world’s most influential markets for Energy Efficient Materials, shaped by aggressive carbon neutrality targets and large-scale adoption of high-performance construction technologies. The rollout of the country’s Nearly Zero Energy Building (NZEB) Standard marks a pivotal policy shift, emphasizing measurable carbon footprint reduction rather than basic energy consumption benchmarks. This mandates widespread use of superior insulation, advanced Low-E glazing, airtight envelopes, and optimized HVAC materials across both public and private developments. China also leads in global BIPV manufacturing, with landmark projects such as the Micro Emission Sun-Moon Mansion, which integrates 5,000 square meters of rooftop solar to achieve up to 88% energy savings. This showcases China’s capability to combine architectural elements with decentralized renewable generation at scale.

In the realm of thermal management, Chinese universities and research institutes are intensifying efforts on microencapsulated Phase Change Materials (PCMs) to stabilize indoor temperatures across its diverse climate zones. These PCM systems are being integrated into wallboards, concrete mixes, and roofing materials to provide passive thermal buffering, particularly in commercial and high-rise buildings. China’s dominance in sustainable construction is further evidenced by its volume of LEED-certified projects, totaling 1,583 certifications in 2023, reinforcing the country’s leadership in green building adoption. This rapid acceleration in high-efficiency materials and smart building technologies firmly positions China as a global powerhouse in energy efficient infrastructure.

Japan: Precision Thermal Management for Electronics and Advanced Composite Insulation Technologies

Japan’s role in the Energy Efficient Materials Market is defined by its leadership in high-performance electronics cooling materials and next-generation building insulation systems. With a globally dominant semiconductor and electronics manufacturing base, Japanese developers such as Toray Industries and Mitsubishi Chemical are investing heavily in ultra-thin graphite sheets, thermal interface materials (TIMs), and high-conductivity composites designed to enhance thermal efficiency in densely packaged electronic devices. These innovations are crucial for reducing energy loads in data centers, high-performance computing systems, and consumer electronics—sectors that increasingly rely on materials engineered for precision heat dissipation.

In parallel, Japan is advancing its development of Vacuum Insulated Panels (VIPs), which offer superior R-values in ultra-thin profiles, enabling energy efficient retrofits in urban environments where wall thickness constraints limit traditional insulation options. These VIPs are gaining traction in residential construction, refrigeration systems, and commercial envelopes, especially in cities enforcing stringent thermal efficiency standards. Japan’s dual focus on electronics thermal management and cutting-edge insulation materials continues to strengthen its competitive advantage in specialized, high-value energy efficient material markets.

South Korea: Smart Grid Efficiency Materials and Semiconductor Thermal Optimization

South Korea’s position in the Energy Efficient Materials Market is tightly linked to its leadership in smart grid development and advanced semiconductor manufacturing. The government continues to fund Smart Grid demonstration projects, integrating Advanced Metering Infrastructure (AMI) and next-generation power electronics that require high-efficiency conductors, superconducting materials, and low-loss components. These materials play a critical role in minimizing transmission losses and improving grid resilience—two core priorities of Korea’s national infrastructure roadmap.

Meanwhile, the country’s semiconductor fabs—operated by global leaders like Samsung and SK Hynix—are scaling their use of high-purity thermal interface materials, ultra-efficient chiller components, and next-generation heat spreaders to manage the extreme thermal loads in advanced chip production. As chip geometries shrink and energy densities rise, demand for specialized thermal management materials continues to surge. This makes South Korea a central contributor to innovation in energy efficient materials engineered for both grid modernization and semiconductor process optimization.

Competitive Landscape: Leading Insulation, Aerogel and High-Performance Materials Providers

The competitive landscape in the Energy Efficient Materials Industry is characterized by a mix of diversified construction materials majors, specialty chemical producers, and focused aerogel innovators. Global leaders are competing not only on R-value and lambda performance, but also on embodied carbon, circularity, and integration into system-level solutions such as insulated panels, airtightness systems, and EV battery thermal barriers. Companies that blend materials innovation with digital building performance data, design advisory, and strong distribution networks are increasingly winning specification in both new-build and retrofit markets.

Saint-Gobain Drives Sustainable Construction with High-Performance Insulation

Saint-Gobain positions itself as a global leader in light and sustainable construction, with brands such as ISOVER mineral wool, Rigips plasterboard, ECOPHON acoustic systems, and advanced glass solutions. Around 73% of group sales in 2024 already came from sustainable solutions, with a target of 75% by 2025, demonstrating how deeply energy efficient materials are embedded in its portfolio. The company’s dedicated capex and R&D budget of roughly €100 million annually to 2030 for decarbonization and energy performance solutions supports continuous innovation in low-lambda mineral wool, façade systems, and high-performance glazing, enabling compliance with NZEB and net-zero building roadmaps worldwide.

Owens Corning Builds North American Leadership in Fiberglass and Whole-Building Efficiency

Owens Corning remains a dominant North American player with its iconic PINK® Fiberglas™ insulation, FOAMULAR® XPS boards, and AeroBarrier air sealing systems. Its fiberglass batts provide R-values up to R-49 in attic systems, forming the baseline for residential and light-commercial energy code compliance. Following the planned divestiture of its Glass Reinforcements Business in February 2025, the company is doubling down on building envelope solutions that combine thermal resistance with air leakage control, moisture management, and code-ready assemblies. Owens Corning’s strategy emphasizes integrated offerings—insulation plus air-sealing and roof systems—that deliver measurable reductions in whole-building energy use for builders and retrofit contractors.

Kingspan Scales High-Performance Rigid Insulation and Insulated Panels

Kingspan Group is a global leader in rigid insulation and insulated panel systems for commercial and industrial buildings, with flagship products such as Kooltherm® phenolic foam, K-Roc® mineral fiber, QuadCore® insulated panels, and Optim-R® VIP systems. Its QuadCore panels achieve thermal conductivities as low as 0.018 W/(m·K), positioning Kingspan at the premium end of the high-performance envelope market. The company’s commitment to net-zero carbon manufacturing by 2030 is driving internal adoption of circular materials and low-embodied-carbon chemistries, making its solutions attractive to developers targeting green building certifications and corporate net-zero commitments.

BASF Leverages Chemical Integration for High-Efficiency EPS and PU Systems

BASF uses its deep backward integration in chemicals to supply Neopor® graphite-enhanced EPS, Elastopir® PU foam systems, and Lupraphen® polyurethane systems for building and industrial applications. Neopor® uses infrared absorbers to improve insulation performance by up to 20% over standard EPS, allowing thinner wall sections and higher thermal resistance. BASF also develops lightweight foam materials for EV battery thermal management, linking the energy efficient materials market to e-mobility growth. Its control over polystyrene and polyurethane precursors ensures supply stability and tailored formulations, supporting OEMs and system integrators seeking optimized thermal and mechanical performance with predictable long-term sourcing.

Aspen Aerogels Pioneers Aerogel Insulation and EV Thermal Barriers

Aspen Aerogels is a specialist in flexible silica aerogel insulation, with key brands Pyrogel®, Cryogel®, and PyroThin®. The next-generation Cryogel product launched in October 2024 targets LNG and cryogenic pipelines, significantly reducing thermal bridging and improving thermal protection in harsh process environments. Aspen’s PyroThin® thermal barrier is gaining traction as a critical safety component in lithium-ion EV battery packs, designed to limit thermal runaway propagation between cells and modules. By combining ultra-low thermal conductivity, thin profiles, and mechanical robustness, Aspen Aerogels sits at the intersection of industrial energy efficiency and e-mobility safety, giving it a differentiated position in the broader energy efficient materials ecosystem.

Energy Efficient Materials Market Report Scope

Energy Efficient Materials Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$25.6 Billion

|

|

Market Size (2035)

|

$61.7 Billion

|

|

Market Growth Rate

|

9.2%

|

|

Segments

|

By Material Type (Insulation Materials, Glazing/Window Materials, Phase Change Materials, Energy-Efficient Coatings, Sustainable Building Materials), By Function (Building Envelope & Structure, HVAC Systems, Thermal Energy Storage, Electronics Thermal Management, Lighting Technologies), By End-User Sector (Construction & Buildings, Automotive & Transportation, Consumer Electronics, Aerospace & Defense), By Functional Characteristic (Thermal Efficiency, Lightweight Materials, Resilience & Durability)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Saint-Gobain, BASF, Owens Corning, Rockwool, Dow, Kingspan, Sika, Knauf Insulation, JinkoSolar, Honeywell, Schneider Electric, SABIC, Vaisala, Covestro, Toray Industries

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Energy Efficient Materials Market Segmentation

By Material Type

- Insulation Materials

- Glazing / Window Materials

- Phase Change Materials

- Energy-Efficient Coatings

- Sustainable Building Materials

By Function

- Building Envelope & Structure

- HVAC Systems

- Thermal Energy Storage (TES)

- Electronics Thermal Management (Heat Sinks, TIMs)

- Lighting Technologies

By End-User Sector

- Construction & Buildings

- Automotive & Transportation

- Consumer Electronics

- Aerospace & Defense

By Functional Characteristic

- Thermal Efficiency

- Lightweight Materials

- Resilience & Durability

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Energy Efficient Materials Market

- Saint-Gobain

- BASF

- Owens Corning

- Rockwool

- Dow

- Kingspan

- Sika

- Knauf Insulation

- JinkoSolar

- Honeywell

- Schneider Electric

- SABIC

- Vaisala

- Covestro

- Toray Industries.

*- List not Exhaustive

Research Coverage

The USDAnalytics Energy Efficient Materials Market study delivers a rigorous, data-backed assessment of how next-generation insulation, aerogels, VIPs, PCMs and advanced coatings are reshaping building envelopes, industrial processes and electronics cooling. Spanning the full 2021–2034 timeline, this report investigates demand inflection points created by NZEB mandates, IRA- and Green Deal-driven retrofits, AI data center thermal management, and industrial electrification, while tracking breakthroughs in ultra-low-lambda insulation, dynamic radiative cooling and PCM-based thermal storage. Through deep-dive analysis reviews of technology performance metrics, capex programs, and regulatory shifts, it highlights where value pools are migrating across construction, automotive, electronics and aerospace, and how players are responding with low-GWP chemistries and circular material strategies. Benchmarking insulation materials against legacy fiberglass and XPS, and mapping adoption of HTIMs, smart façade solutions and BIPV-integrated systems, this report is an essential resource for product managers, strategy leaders, sustainability officers and investors seeking actionable insight into the global Energy Efficient Materials Market. By combining granular segmentation with competitive benchmarking and regional policy tracking, USDAnalytics equips decision-makers to prioritize R&D pipelines, refine go-to-market plays and capture long-term specification in high-growth, low-carbon applications.

Scope Highlights

- Segmentation

- By Material Type: Insulation Materials, Glazing / Window Materials, Phase Change Materials, Energy-Efficient Coatings, Sustainable Building Materials

- By Function: Building Envelope & Structure, HVAC Systems, Thermal Energy Storage (TES), Electronics Thermal Management (Heat Sinks, TIMs), Lighting Technologies

- By End-User Sector: Construction & Buildings, Automotive & Transportation, Consumer Electronics, Aerospace & Defense

- By Functional Characteristic: Thermal Efficiency, Lightweight Materials, Resilience & Durability

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Time Frame: Historic data from 2021 to 2025 and forecast data from 2026 to 2034.

- Companies Covered: Analysis / profiles of 15+ companies across insulation, aerogels, high-performance coatings, PCMs, glazing, and integrated energy efficient material systems.