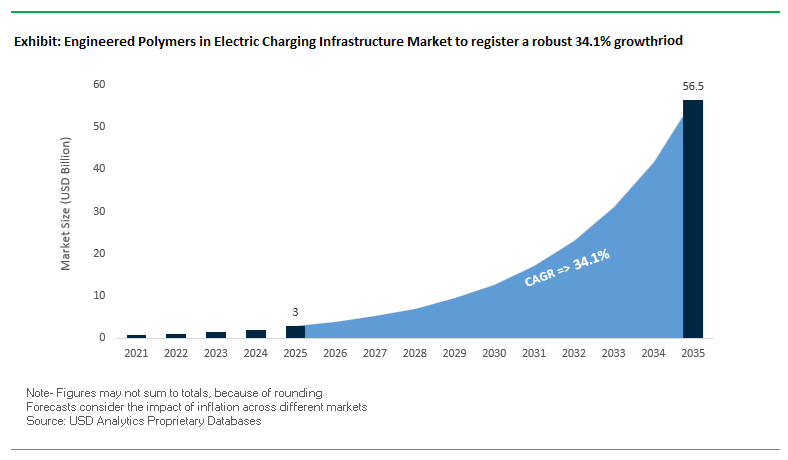

Engineered Polymers in EV Charging Infrastructure Market Overview: Rapid Scale-Up from USD 3 Billion to USD 56.4 Billion

The Engineered Polymers in Electric Charging Infrastructure Market is projected to grow from USD 3 billion in 2025 to USD 56.4 billion by 2035, registering an exceptionally high CAGR of 34.1% (2025–2035). This surge is driven by the global roll-out of high-power DC fast chargers, 800V EV architectures, and battery swapping systems, all of which require high-voltage, flame-retardant, and dimensionally stable polymers for connectors, housings, and internal EVSE components. For material manufacturers and compounders, the opportunity lies in developing UL 94 V-0, CTI ≥600 V, high-dielectric polymers that can withstand harsh outdoor environments, thermal cycling, and humidity over long lifetimes.

Key performance metrics underline why engineered thermoplastics and specialty resins are becoming the default for EV charging hardware. High CTI values are mandatory to prevent surface tracking in polluted or coastal environments; non-halogenated flame retardant systems are increasingly required by OEM specifications and regulations; and long-term dielectric strength retention at high temperature and humidity is now a critical design criterion for 800V platforms. In parallel, low-CTE materials such as PEI are enabling metal replacement in busbar and power electronics enclosures, improving lightweighting and simplifying manufacturing.

Key market insights for manufacturers and vendors:

- CTI ≥600 V becoming baseline for outdoor EVSE connectors – high tracking resistance is now a qualification gate for high-voltage polymer grades in public charging infrastructure.

- UL 94 V-0 at thin walls (~0.4 mm) after thermal aging is increasingly specified for internal EVSE components and battery housings, favouring advanced halogen-free flame-retardant polyamides, PBT, and PPA.

- Dielectric strength >10 kV/mm and volume resistivity >10¹⁰ Ω·cm after exposure to 95°C / high humidity environments makes PPS, PPA and similar materials preferred in hot/wet charging conditions.

- Low CTE engineered thermoplastics (e.g., PEI) are enabling reliable metal replacement in busbars and power electronic enclosures across –40°C to 80°C cycles, reducing stress and dimensional drift.

- OEMs and CPOs increasingly demand material platforms validated for 800V systems, ToD tariff-driven energy storage, and fast-charging architectures, pushing suppliers toward application-ready, certified material systems.

Engineered Polymers in EV Charging Infrastructure Market Analysis: Policy, Product Innovation and Capacity Expansion

The global engineered polymers in EV charging infrastructure industry is being reshaped by a combination of public policy, OEM platform roadmaps, and materials innovation. On the policy side, India’s Ministry of Power has emerged as a key catalyst: in September 2024, it issued the PM E-DRIVE Scheme with an outlay of ₹10,900 crore (≈USD 1.3 billion), including ₹2,000 crore ring-fenced for public charging stations. This was followed by technical standards and guidelines for battery swapping stations in January 2025, which explicitly push the market toward high-durability, electrically insulating polymers in cooled, high-cycle swapping hardware. In July 2025, the Tamil Nadu Electricity Regulatory Commission revised time-of-day EV charging tariffs, raising peak rates and thereby encouraging charge point operators (CPOs) to invest in on-site energy storage, which in turn accelerates demand for polymer battery enclosures and thermally stable housing materials.

On the industry innovation front, leading chemical and materials companies are aggressively positioning around 800V charging, metal replacement, and halogen-free safety performance. In April 2024, BASF co-developed the housing for LAPP’s Mobility Dock portable charging system, using Ultramid® polyamide for UV resistance, mechanical robustness and halogen-free flame retardancy, demonstrating how engineered polymers can meet consumer-grade EVSE requirements while still aligning with safety codes. In November 2025, SABIC launched its MEGAMOLDING platform at K 2025, integrating advanced materials with simulation tools to produce large, lightweight thermoplastic components for EV battery housings and structural charging units – a direct play on reducing weight and part count in charging infrastructure. EMS-GRIVORY’s first-place recognition at the 2025 SPE Awards (October 2025) for a sophisticated metal-replacement E&E component underscores how high-performance polyamides are displacing metals in complex EV powertrain and charging subsystems.

Materials innovations are also becoming more application-specific. In December 2025, BASF introduced Ultramid® Advanced N3U42G6, a PPA with non-halogenated flame retardancy and minimized electro-corrosion, addressing the reliability challenges of high-voltage connectors under condensation and salt-laden environments. At the same time, a key connector manufacturer announced a USD 30 million expansion of its Asian plant in May 2025 to ramp up 800V charging connector capacity, a move that will pull through more volume of long-fiber reinforced polyamides and other structural engineered polymers that can handle high thermal loads and mechanical abuse. Collectively, these developments signal a market transitioning from basic plastic enclosures to system-engineered polymer platforms optimized for CTI, UL fire performance, dielectric stability, and long-term outdoor durability.

High-Temperature Polymers, Flame-Retardant Thermoplastics, and Electrically Functional Compounds Reshaping the Engineered Polymers in Electric Market

Market Trend 1: Expansion of Liquid-Cooled, High-Temperature Cable Insulation to Enable 400 kW+ Ultra-Fast Charging Performance

The shift toward ultra-fast EV charging architectures is accelerating demand for engineered polymers that can survive extreme electrical and thermal stress environments. Liquid-cooled high-power charging cables now sustain continuous currents of 400–500 A, with some advanced designs exceeding 600 A, far surpassing the 250–300 A ceiling typical of air-cooled systems. This continuous high-current operation dramatically increases the thermal load on insulation materials, requiring polymers capable of withstanding coolant temperatures of ≥105–125°C, well above the 90°C rating of traditional XLPE insulation.

Liquid cooling modules further reduce conductor temperatures by 10–20°C, a critical improvement for maintaining dielectric strength and preventing insulation embrittlement or breakdown under repeated thermal cycles. These engineered insulation systems must also perform reliably under high-voltage stress, passing 1.5 kV DC requirements and dielectric withstand tests of 3.5 kVac for 15 minutes with zero breakdown. As ultra-fast charging becomes the backbone of national EV infrastructure, the market is increasingly prioritizing thermally resilient, high-dielectric polymer families—including advanced polyamides, high-temperature fluoropolymers, and engineered elastomer blends that allow safe and reliable scaling of cable amperage.

Market Trend 2: Adoption of Flame-Retardant, Weather-Resistant Thermoplastics for Outdoor Charging Cabinets and EV Station Enclosures

Outdoor DC fast-charging installations require structural polymers that remain stable under fire exposure, UV radiation, mechanical loads, and sub-zero temperatures. As a result, charging enclosure manufacturers are increasingly specifying thermoplastics that achieve the highest UL 94 flame ratings (5VA or V-0 at 1.5 mm), ensuring the material self-extinguishes and avoids flaming drips that can ignite nearby electronic modules.

These engineered thermoplastics must withstand 720 hours (10,000 kJ/m²) of Xenon Arc aging without cracking or significant degradation, a stringent benchmark for UV durability and weather resistance. Cold-climate resilience is also a decisive factor—specialized polycarbonate grades retain ductility at temperatures as low as −40°C, preventing cracking under impact loads such as accidental collisions with charging holsters or cable management arms. Additionally, high-strength sheathing materials must tolerate mechanical stresses above 11 kN, ensuring long-term structural integrity around cable protection conduits. As charge-point operators deploy networks in diverse climates, UV-stabilized, flame-retardant, high-impact polymers are becoming a strategic materials category for EV infrastructure OEMs.

Market Opportunity 1: Intrinsically Conductive Polymers (ICPs) for Lightweight EMI Shielding in Compact Fast-Charging Power Electronics

Miniaturization of fast-charging modules and the increasing integration of high-frequency power electronics create new pathways for engineered conductive polymers to replace metal EMI shields. To meet functional safety requirements, these materials must deliver ≥20 dB EMI shielding effectiveness, with premium applications requiring ≥30 dB in GHz-range frequencies used by DC-DC converters, SiC inverters, and control systems.

The shielding mechanism is primarily absorption-driven, enabled through conductive fillers such as CNTs, graphene, and metallic particles embedded within polymer matrices like polyaniline or polycarbonate blends. Once the percolation threshold is crossed, electrical conductivity increases sharply, yielding a step-change in EMI absorption capability. These polymer solutions offer compelling weight advantages: ICPs have 1/7 the density of steel and roughly half the weight of aluminum, significantly reducing system mass for wall-mounted or pole-mounted EV charger designs. This opportunity is expanding rapidly as charging OEMs seek lighter, corrosion-resistant, and easily moldable shielding materials for next-generation compact charging cabinets.

Market Opportunity 2: High-Track-Resistance, Thermally Conductive Potting Compounds for On-Board Charger (OBC) Miniaturization and Safety

The electrification trend is intensifying demand for high-track-resistance, thermally conductive potting polymers that ensure safety and thermal reliability in compact On-Board Chargers (OBCs). To support high-voltage miniaturized designs, polymers must achieve a Comparative Tracking Index (CTI) ≥600 V—placing them in Material Group I, per IEC 60112. A CTI in this range allows designers to reduce creepage distances, enabling smaller footprints for OBCs and high-voltage modules without compromising safety. This CTI threshold is also required for harsh-energy environments such as solar inverters and wind turbines.

For thermal management, engineered potting materials must provide ≥1.5 W/(m·K) thermal conductivity—far higher than the ≈0.2 W/(m·K) typical of standard resins—to extract heat from SiC MOSFETs and other high-power semiconductors. Maintaining dielectric strength of ≥10 kV/mm is critical to avoid partial discharge, particularly in confined OBC housings with dense power electronics. As EV platforms migrate to higher voltages (800–1,000 V systems), potting compounds engineered for thermal conduction, electrical insulation, and tracking resistance represent one of the most attractive innovation opportunities for polymer manufacturers.

Engineered Polymers in Electric Charging Infrastructure Market Share Analysis

Market Share by Polymer Type: Polyamides Lead Due to Superior Thermal Stability, Mechanical Strength, and Safety Compliance in High-Voltage EV Charging Systems

Polyamides (PA) hold the largest share of the global engineered polymers in EV charging infrastructure market—approximately 25% in 2025—because they deliver the robust thermal, mechanical, and electrical performance required for next-generation fast-charging systems. High-performance grades such as PA6, PA66, and polyphthalamides (PPAs) provide exceptional heat resistance, enabling them to withstand the intense thermal loads generated during DC Fast Charging (DCFC), where current levels can exceed 400–500 A and temperature spikes can compromise lesser materials. Their ability to maintain structural rigidity, dimensional stability, and dielectric strength under such demanding conditions makes them indispensable for high-voltage connectors, internal housings, and power electronic modules. Polyamides also achieve UL 94 V-0 flame-retardant ratings, often without halogen-based additives, aligning with global safety and environmental regulations. When reinforced with glass fibers, PAs offer the enhanced strength, stiffness, and fatigue resistance required for repeated mating cycles in public and commercial charging environments. The materials' inherent chemical resistance and durability under mechanical stress further secure their dominance as the preferred engineered polymer for critical EV charging components, especially as charging speeds increase and thermal management requirements intensify.

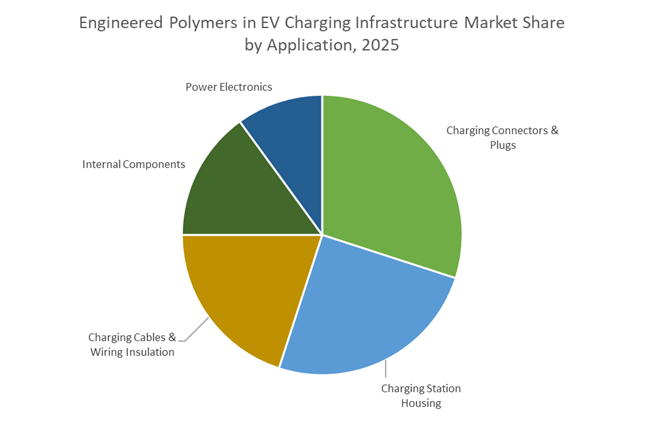

Market Share by Application: Charging Connectors & Plugs Dominate Due to Highest Component Stress, Safety Requirements, and Material Intensity

The Charging Connectors & Plugs segment accounts for roughly 30% of the engineered polymer demand in EV charging infrastructure because connectors are the most technologically complex and safety-critical polymer-intensive components in the entire charging ecosystem. These connectors must endure a combination of mechanical, thermal, and environmental stresses unmatched by other system elements: repeated insertion cycles, accidental impacts, exposure to UV and outdoor conditions, and sustained handling of up to 1,000 VDC during high-power charging. As the primary interface between the user and the high-voltage system, connectors rely heavily on advanced polymers—particularly reinforced PA, PBT, and PPS—to ensure electrical insulation, flame resistance, structural integrity, and ergonomic durability. Strict international standards such as IEC 62196, SAE J1772, and CCS requirements drive the use of certified engineering plastics capable of meeting demanding dielectric, tracking-resistance, and temperature performance thresholds. Because connectors require multiple high-precision molded parts, tight dimensional tolerances, and premium flame-retardant materials, their cost and material intensity are significantly higher per unit than housings, cables, or internal components. This combination of critical safety function, regulatory pressure, and high-performance material demand solidifies connectors and plugs as the largest and most revenue-intensive application segment in the market.

Country Analysis: Global Drivers in Engineered Polymers for Electric Charging Infrastructure

China: Ultra-Fast Charging Expansion Driving High-Performance Polymer Demand

China remains the world’s largest and fastest-scaling market for Engineered Polymers in Electric Vehicle Charging Infrastructure, propelled by unmatched deployment volume and rapidly evolving ultra-fast charging standards. The government’s aggressive push—such as Beijing’s goal to build 1,000 ultra-fast charging stations and Chongqing’s plan for 4,000 additional ultra-fast chargers by 2025—creates sustained, high-volume procurement of polymer components engineered for thermal, chemical, and electrical stability. These installations rely heavily on high-performance Polybutylene Terephthalate (PBT) and Polyamide (PA) in connector housings, busbars, and internal assemblies where demanding heat cycles and long-term electrical exposure are standard.

China’s OEM ecosystem further accelerates material innovation. Partnerships like XPeng–Volkswagen’s rollout of 20,000 ultra-fast chargers across 400+ cities require massive quantities of Flame-Retardant (FR) and UV-stabilized PC/ABS blends to ensure outdoor durability, vandal resistance, and compliance with public infrastructure codes. The rapid increase in high-current DC fast charging stations also intensifies demand for thermally conductive polymers capable of dissipating the 2.5 kW of thermal energy generated during a 150 kW charging cycle. As domestic polymer producers scale modified Polyphenylene Ether (PPE) resins to replace imported electrical-grade materials, China is advancing toward complete supply chain localization, enhancing dielectric performance while enabling lighter, safer charging components for mass deployment.

United States: NEVI Standards and Extreme-Environment Durability Shaping Polymer Specifications

The United States represents one of the most technical and compliance-driven regions for Engineered Polymers in EV Charging Infrastructure, shaped by stringent performance requirements under the NEVI (National Electric Vehicle Infrastructure) program. NEVI mandates consistent, nationwide standards for uptime, reliability, and environmental durability—directly driving demand for UV-resistant Polycarbonate (PC), impact-resistant ASA, and robust composite blends used in charging station housings deployed across climates ranging from Arizona’s extreme heat to the northern states’ deep winter conditions.

Parallel to this, the U.S. is becoming a major hub for advanced material systems enabling 800V High-Power Charging (HPC) architectures. Chemical suppliers such as Dow and H.B. Fuller are commercializing high-performance silicone elastomers, gap fillers, and polyurethane pottants engineered to manage the intense heat loads within power electronics modules. Connector manufacturers are simultaneously adopting glass-fiber reinforced PBT resins, offering superior wear resistance, dimensional stability, and chemical resilience required for high-cycle public charging applications. The market also shows growing adoption of halogen-free, flame-retardant (HFFR) polymers for cables and charging armatures, ensuring UL compliance and reducing fire risk in high-voltage DC environments. These material innovations position the U.S. as a leading developer of rugged, compliant, long-lifespan polymer systems for advanced charging infrastructure.

Germany / European Union: Interoperability-Driven Polymeric Engineering and Circular Material Mandates

Europe’s leadership in Engineered Polymers for EV Charging Infrastructure is shaped by the twin pressures of interoperability standardization and sustainability mandates under EU regulatory frameworks. With a dramatic 70–95% increase in Germany’s ultra-fast chargers (≥150 kW) in 2024, material demand has surged for engineered high-temperature Polyamide systems—such as Durethan PA—for use in liquid-cooled charging cables and HPC connector assemblies. These polymers must withstand elevated thermal loads while meeting the Combined Charging System (CCS) connector's stringent tracking resistance and dimensional precision requirements to guarantee seamless cross-brand compatibility.

At the same time, Europe’s Circular Economy Action Plan is redefining polymer development by prioritizing recyclability and renewable carbon feedstock. European manufacturers are accelerating the adoption of mechanically recyclable Thermoplastic Polyurethanes (TPU) for charging cables, ensuring mechanical endurance under frequent bending cycles while supporting closed-loop recovery pathways. The EU’s sustainability transition places additional emphasis on low-impact, durable polymer systems for housing components, insulation structures, and high-voltage interfaces. The region’s high regulatory clarity and environmental ambition make it a transformative global force in next-generation sustainable polymer systems for EV charging networks.

South Korea: High-Speed Charger Scale-Up and Polymer Engineering for Battery Swapping Infrastructure

South Korea’s rapid electrification strategy is reshaping demand for Engineered Polymers in Charging Infrastructure, driven by a substantial 40% increase in the national fast-charging budget, totaling KRW 620 billion (USD 425 million) for 2025. With 60% of this capital dedicated to fast chargers, material demand is sharply rising for high-spec polymer systems engineered for thermal resistance, chemical durability, and precise molding properties. These requirements are critical as Korea accelerates deployment of rapid-charging corridors across metropolitan and intercity networks.

Additionally, Korea’s unique emphasis on Battery Swapping Stations (BSS) is creating new polymer engineering challenges. Automated swap mechanisms require materials with exceptional chemical resistance to electrolytes, elevated fatigue strength, and stability under rapid mechanical cycling. High-performance Polyamides, Polycarbonates, and composite-reinforced polymers are increasingly utilized in clamps, trays, structural housings, and robotic assemblies within BSS environments. As Korean EV OEMs and materials companies expand R&D in solid-state battery interfaces and next-generation charging formats, South Korea is emerging as a specialized market segment for polymer systems designed for high-intensity operational cycles and automated mobility ecosystems.

India: PM E-DRIVE Funding Surge Fuels Domestic Polymer Manufacturing and Standardized Charging Components

India’s Engineered Polymers for EV Charging Infrastructure Market is entering a high-growth phase driven by transformative government initiatives, most notably the PM E-DRIVE Scheme, allocating ₹2,000 crore (USD 240 million) to deploy ~72,000 new chargers by FY 2025–26. This unprecedented infrastructure push is generating strong domestic demand for durable, cost-optimized polymer components, particularly for Level 2 chargers, DC fast chargers, and two-/three-wheeler charging systems—the dominant modes of electrification in India’s mobility landscape.

India’s broader industrial strategy reinforces this trajectory. Under the PLI-Auto (Production-Linked Incentive) scheme, manufacturers are localizing the production of polyamide, PBT, and other engineering polymers to supply Advanced Automotive Technology (AAT) components for EV charging hardware. This localization reduces dependence on imported resins while enabling tailored formulations suited to India’s harsh climatic conditions, including extreme heat, humidity, and dust exposure. Meanwhile, revised Ministry of Power (MoP) Charging Guidelines (2024) promote network interoperability via open protocols, creating demand for precision-molded, high-seal-integrity plug and socket components with superior dimensional stability. Together, these regulatory and manufacturing shifts are quickly positioning India as a rising production hub for engineered polymers optimized for high-reliability charging infrastructure.

Competitive Landscape in Engineered Polymers for EV Charging Infrastructure

The competitive landscape of the Engineered Polymers in Electric Charging Infrastructure Market is dominated by a small group of global material science leaders with deep expertise in high-voltage E&E applications, flame retardancy, and metal replacement. These companies are not only supplying polymer grades but also delivering application engineering, simulation, and co-development services with OEMs, connector manufacturers, and CPOs. Their portfolios span polycarbonate, PPE blends, PA/PBT/PPA, PPS, PEI, LCP, and long-fiber reinforced compounds, all tuned for 800V systems, outdoor exposure, and tight regulatory compliance. Strategic themes include circular polymers, halogen-free FR systems, LFT for structural components, and LCPs for miniaturized high-pin-density connectors used in power electronics and charging controls.

SABIC drives high-voltage EV charging solutions through BLUEHERO and MEGAMOLDING

SABIC positions itself as a full-stack materials provider for EV battery systems, power electronics, and charging infrastructure via its BLUEHERO electrification program. Its core offerings for charging systems include LEXAN™ polycarbonate, NORYL™ modified PPE resins, ULTEM™ PEI, and LNP™ thermally conductive compounds, all engineered for high voltage (up to ~800 V), outdoor weatherability, and impact resistance in charger housings and structural units. With the MEGAMOLDING platform launched in November 2025, SABIC integrates advanced materials with molding and simulation expertise to deliver large, lightweight thermoplastic components for EV battery housings and structural charging infrastructure. In parallel, the company’s TRUCIRCLE™ portfolio of certified circular and bio-based polymers allows OEMs and CPOs to lower the carbon footprint of EVSE components without compromising CTI, flammability, or mechanical performance.

BASF co-develops advanced PA/PBT/PPA systems for safe high-voltage connectors

BASF is a key chemical heavyweight in the EV charging materials ecosystem, leveraging its Ultramid® (PA), Ultradur® (PBT), Ultramid® Advanced (PPA), and Elastollan® (TPU) platforms. It differentiates through eMobility co-creation, offering Ultrasim® simulation tools and application engineering to optimize connector geometry, wall thickness, and processing for high-voltage systems. In April 2024, BASF’s collaboration on LAPP’s Mobility Dock housing showcased how Ultramid® can deliver UV stability, mechanical resilience, and halogen-free flame retardancy for portable EVSE. The December 2025 launch of Ultramid® Advanced N3U42G6, a PPA with non-halide FR and minimized electro-corrosion, directly targets HV connectors and busbar systems that need to maintain color stability and electrical integrity over long service lives. BASF also provides TPU sheathing materials for flexible fast-charging cables, supporting abrasion resistance and low-temperature flexibility.

DuPont leverages nylon, PBT and polyimide for system-level EV charging reliability

DuPont approaches the engineered polymers for EV charging segment from a system-level solutions perspective, matching Zytel® nylon (PA), Crastin® PBT, and Vespel® polyimide to specific positions in the electrification value chain. In charging infrastructure, Zytel® and Crastin® are widely used for connector housings, cable glands, and internal structural parts, providing a combination of CTI performance, dimensional stability, and UL 94 V-0 compliance. DuPont’s high-temperature Vespel® polyimide is applied to extreme friction and wear components in EV drivetrains and high-speed E&E assemblies, where it withstands temperatures above 400°C and continuous mechanical stress. The company’s growing portfolio of adhesives and structural foams for battery packs and enclosures complements its polymer resins, allowing OEMs to integrate mechanical support, thermal management, and electrical safety in a unified materials architecture for EV charging and power electronics.

EMS-GRIVORY specializes in high-temperature polyamides for 800V connectors and metal replacement

EMS-GRIVORY is a specialist in high-performance polyamides, notably Grivory® (PPA), Grilamid® (PA) and long-fiber thermoplastics (LFT), with a strong focus on metal replacement and high-voltage E&E parts. The company offers one of the broadest ranges of high-temperature polyamides globally, specifically tuned for 800V charging connectors, busbar systems, and structural EV components that require high stiffness, heat resistance, and impact strength. Its SPE Award-winning solution in October 2025 showcased how advanced PA LFT can substitute metal in a complex E&E component, reducing weight while maintaining mechanical reliability and CTI/flame-retardant performance. EMS-GRIVORY’s flame-protected LFT polyamides help OEMs design compact, lightweight, and durable connector bodies and housings, enabling faster assembly and higher power densities in public fast-charging infrastructure.

Celanese uses LCP and advanced polyamides to enable miniaturized high-density EV connectors

Celanese has built a strong position in engineered polymers for EV electronics and charging through brands such as Hostaform® acetal (POM), Vectra®/Zenite® liquid crystal polymers (LCP), and ForTii® polyamide. Its LCP portfolio is particularly critical for miniaturized, high-pin-density connectors and sensors inside EV power electronics and on-board chargers, where extreme flowability, dimensional stability, low warpage, and high solder-reflow resistance are essential. ForTii® polyamide complements these materials in high-voltage connector housings and structural parts, providing robust mechanical strength and elevated CTI ratings. Celanese’s acquisition of DuPont’s Mobility and Materials business significantly broadened its automotive E&E portfolio, allowing it to deliver integrated material sets for EV charging modules, junction boxes, and inverter/charger housings. In EV charging infrastructure, this positions Celanese as a key enabler of compact, reliable and thermally robust E/E architectures compatible with 800V platforms and fast-charging requirements.

Engineered Polymers in Electric Charging Infrastructure Market Report Scope

Engineered Polymers in Electric Charging Infrastructure Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$3 Billion

|

|

Market Size (2035)

|

$56.4 Billion

|

|

Market Growth Rate

|

34.1%

|

|

Segments

|

By Polymer Type (Polyamides, PBT, Polycarbonates, Polypropylene, PPS, Elastomers, Others), By Component Application (Charging Connectors & Plugs, Charging Cables & Wiring Insulation, Charging Station Housing, Power Electronics, Internal Components), By Charging Technology (AC Charging, DC Fast Charging, Wireless/Inductive Charging, Battery Swapping Stations), By Performance Requirement (Flame Retardance, Thermal Management, UV & Weather Resistance, Chemical & Hydrolytic Resistance)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

SABIC, BASF, Dow, DuPont, Covestro, Lanxess, LG Chem, Solvay, Celanese, Victrex, Mitsubishi Chemical Group, TE Connectivity, Phoenix Contact, Leoni, Heraeus

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Engineered Polymers in Electric Charging Infrastructure Market Segmentation

By Polymer Type

- Polyamides

- Polybutylene Terephthalate (PBT)

- Polycarbonates

- Polypropylene (PP)

- Polyphenylene Sulfide (PPS)

- Elastomers

- Others

By Component Application

- Charging Connectors & Plugs

- Charging Cables & Wiring Insulation

- Charging Station Housing

- Power Electronics

- Internal Components

By Charging Technology

- AC Charging

- DC Fast Charging (Level 3 / HPC)

- Wireless / Inductive Charging

- Battery Swapping Stations

By Performance Requirement

- Flame Retardance

- Thermal Management

- UV & Weather Resistance

- Chemical & Hydrolytic Resistance

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Engineered Polymers in Electric Charging Infrastructure Market

- SABIC

- BASF

- Dow

- DuPont

- Covestro

- Lanxess

- LG Chem

- Solvay

- Celanese

- Victrex

- Mitsubishi Chemical Group

- TE Connectivity

- Phoenix Contact

- Leoni

- Heraeus.

*- List not Exhaustive

Research Coverage: Engineered Polymers in Electric Charging Infrastructure Market

The USDAnalytics Engineered Polymers in Electric Charging Infrastructure Market study provides a technical yet practical roadmap for material strategists, as this report investigates how high-voltage, flame-retardant, and dimensionally stable polymers are enabling global scale-up of DC fast charging, 800V platforms, liquid-cooled cables, and battery swapping systems; it tracks breakthroughs in UL 94 V-0 halogen-free compounds, CTI ≥600 V grades, thermally conductive potting systems, and low-CTE metal-replacement resins that underpin safe, compact, and reliable EVSE architectures; the analysis reviews policy catalysts such as national fast-charging programs, OEM and CPO specifications, and standards for high-power connectors, while assessing how material science innovation is reshaping connector housings, enclosures, power electronics, and cable insulation; the narrative highlights competitive positioning of leading polymer suppliers in areas like 800V-ready platforms, EMI-shielding compounds, high-track-resistance materials, and outdoor-durable thermoplastics for public charging networks; by combining quantitative market modelling with qualitative engineering insight, this report is an essential resource for EV ecosystem decision-makers, polymer R&D leaders, sourcing managers, and investors seeking to align material portfolios with next-generation charging infrastructure demand across on-street, depot, highway corridor, and fleet applications.

Scope Highlights

- Segmentation: Detailed coverage by Polymer Type (Polyamides, Polybutylene Terephthalate (PBT), Polycarbonates, Polypropylene (PP), Polyphenylene Sulfide (PPS), Elastomers, Others); by Component Application (Charging Connectors & Plugs, Charging Cables & Wiring Insulation, Charging Station Housing, Power Electronics, Internal Components); by Charging Technology (AC Charging, DC Fast Charging (Level 3 / HPC), Wireless / Inductive Charging, Battery Swapping Stations); and by Performance Requirement (Flame Retardance, Thermal Management, UV & Weather Resistance, Chemical & Hydrolytic Resistance).

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa, capturing regional differences in fast-charging roll-out, policy frameworks, grid conditions, and component localisation.

- Time Frame: Market assessment based on historic data from 2021 to 2025, with scenario-based forecasts and growth outlooks from 2026 to 2034 aligned with EV penetration, DCFC density, and charging technology roadmaps.

- Companies: In-depth analysis and profiles of 15+ leading participants across the value chain, including polymer producers, compounders, connector specialists, cable manufacturers, and integrated EVSE solution providers.