Market Overview: Growth Driven by Sustainability and Performance Packaging

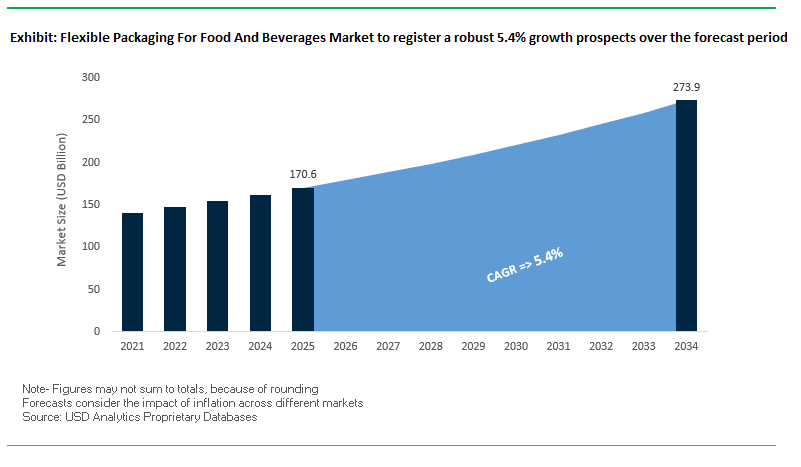

The Global Flexible Packaging for Food and Beverages Market is projected to grow from USD 170.6 billion in 2025 to USD 273.9 billion by 2034, advancing at a CAGR of 5.4%. This sector is one of the most critical enablers of the global food supply chain, ensuring food safety, extending shelf life, and supporting convenience-driven lifestyles. It is witnessing a strong transformation as consumer demands, sustainability regulations, and technological advancements reshape the market outlook.

A key growth driver is the shift toward sustainable and recyclable packaging solutions. With global regulations targeting single-use plastics, companies are investing heavily in compostable films, mono-material packaging, and PCR-based laminates. Alongside, the demand for high-performance barrier films continues to grow, protecting food and beverages from oxygen, moisture, and light exposure.

Lightweight materials are also accelerating adoption as they help reduce carbon footprint, shipping costs, and overall fuel consumption, making them vital in addressing climate change goals. Furthermore, the boom in e-commerce grocery delivery and meal-kit services is boosting demand for durable and protective flexible packaging formats that ensure food arrives safely at consumers’ doorsteps.

Key Insights for professionals and Buyers:

- Market expanding from USD 170.6B (2025) → USD 273.9B (2034), CAGR 5.4%.

- Sustainability-driven innovations: compostable, recyclable, PCR-based films.

- Barrier films essential for shelf life extension in fresh and processed foods.

- Lightweight materials driving logistics efficiency and reduced CO₂ emissions.

- E-commerce and home delivery fueling demand for durable flexible packaging.

Market Analysis: Recent Developments in Flexible Packaging for Food and Beverages

The Flexible Packaging for Food and Beverages Industry is characterized by high innovation, sustainability targets, and mergers reshaping competition.

In August 2025, ProAmpac announced plans to acquire PAC Worldwide, reinforcing its presence in e-commerce fulfillment and protective packaging, which overlap with food packaging requirements. In the same month, Amcor expanded its healthcare packaging network in Costa Rica and unveiled an upgraded recycling facility in the UK, underscoring its cross-sector sustainability strategy that also benefits food and beverage packaging.

Also in August 2025, a new report highlighted the rising role of smart packaging technologies such as QR codes, NFC, and RFID, which allow real-time freshness monitoring and product traceability. This technology integration is becoming a differentiator for food brands seeking transparency and consumer trust.

In July 2025, two major mergers reshaped the packaging landscape. The Amcor–Berry Global merger created a dominant global packaging leader with a strong footprint in flexibles and sustainable solutions. In parallel, Smurfit Kappa–WestRock completed their all-stock merger, positioning themselves as leaders in paper-based packaging, with likely implications for fiber-based flexible packaging applications.

Other companies are enhancing their sustainable offerings. In July 2025, Huhtamaki launched a compostable and recyclable packaging solution for the ice cream industry, while in May 2025, reports confirmed surging global demand for recyclable and compostable food packaging. This aligns with the broader trend of circular economy-driven innovation.

Emerging Trends and High-Impact Opportunities Shaping the Flexible Packaging for Food and Beverages Market

Strategic Pivot to Polyolefin-Based Mono-Material Structures

The flexible packaging for food and beverages market is witnessing a decisive shift as major brands and converters transition from multi-material laminates like PET/ALU/PE to mono-material structures primarily based on polyethylene (PE) or polypropylene (PP). This strategic pivot is driven by increasing recyclability mandates and extended producer responsibility (EPR) legislation, making mono-material packaging compatible with existing polyolefin recycling streams. Industry leaders such as Nestlé, Danone, and Mars Inc. have publicly committed to adopting mono-material flexible packaging globally, reflecting a robust industry-wide movement. This trend opens a high-value growth avenue for manufacturers that can deliver high-performance, compliant alternatives to traditional multi-material products. The shift also reshapes the value chain, requiring enhanced collaboration among raw material suppliers, converters, and CPG brands, along with investment in advanced machinery and R&D for high-performance mono-material solutions.

Integration of Digital Watermarking for Precision Recycling

To address the challenges of sorting complex flexible packaging in recycling streams, the industry is increasingly deploying digital watermarking technologies, exemplified by the HolyGrail 2.0 initiative. These imperceptible codes allow high-speed sorting cameras to accurately separate packages by polymer type and food vs. non-food usage, significantly increasing recycled material volume and quality. Industrial trials in Germany demonstrated detection efficiency rates between 87.9% and 93.8%, proving the technology’s commercial viability. By integrating digital watermarking, manufacturers can provide packaging that is fully compatible with advanced recycling, enabling the separation of food-grade from non-food-grade materials and unlocking more valuable recycled streams. This trend promotes a data-driven, circular supply chain, necessitating collaboration between packaging manufacturers, technology providers, and waste management companies to achieve a more sustainable ecosystem.

Development of High-Barrier Bio-Based Films for Compostable Applications

There is a compelling opportunity to develop high-performance, bio-based, and certified compostable films that meet barrier requirements for sensitive food and beverage products. This is particularly critical for applications such as fresh produce, snacks, and dry goods where recycling is limited. Academic research highlights the potential of materials like bacterial cellulose (BC), which can reduce water vapor permeability by up to 84% and provide strong oxygen barriers, effectively preserving perishable goods. R&D efforts, such as coating PLA films with chitosan and oregano oil, have demonstrated the ability to extend produce shelf life by 35 days. The commercialization of these films represents a high-value growth avenue, catering to environmentally conscious consumers and supporting brand sustainability goals. This opportunity is driving new collaborations between material science companies and packaging manufacturers to develop circular, eco-friendly packaging solutions.

Adoption of Active and Intelligent Packaging for Food Waste Reduction

Active and intelligent packaging technologies represent a significant opportunity to extend shelf life and provide real-time food quality information. Innovations include oxygen scavengers in liners, freshness indicators, and time-temperature indicators that directly reduce in-store and household food waste. The UN Food and Agriculture Organization reports that rich countries waste nearly 222 million tonnes of food annually—almost equivalent to the total net production of sub-Saharan Africa—highlighting the critical need for these solutions. Intelligent packaging is increasingly preferred by consumers over passive systems, creating a high-value growth avenue for flexible packaging manufacturers. This technology promotes cross-industry collaboration among packaging producers, technology firms, and food scientists, fostering an innovative, interconnected value chain designed to enhance food safety, reduce waste, and improve sustainability outcomes.

Competitive Landscape: Leading Companies in Flexible Food and Beverage Packaging

The Global Flexible Packaging for Food and Beverages Market is highly consolidated, with leading companies leveraging acquisitions, sustainable innovation, and global networks to strengthen their competitive positions.

Amcor plc leads with recyclable and lightweight flexible packaging solutions

Amcor is a global packaging leader, offering high-performance barrier films, vacuum bags, and recycle-ready pouches. In August 2025, it expanded operations in Costa Rica and opened a recycling facility in the UK. Its AmPrima® range highlights its goal of making all packaging recyclable or reusable by 2025.

Huhtamaki Oyj focuses on circular economy packaging innovations

Huhtamaki is a global food packaging specialist, emphasizing sustainable packaging. In July 2025, it unveiled a recyclable and compostable packaging solution for ice cream. Through its blueloop™ brand, it delivers circular-ready flexible packaging for ready meals, sauces, and on-the-go food products.

Sealed Air Corporation strengthens retail and protein sector packaging

Sealed Air, known for its Cryovac® brand, provides advanced barrier shrink films used widely in meat, poultry, and dairy. In August 2025, the company pivoted its protective packaging strategy toward the retail channel. Its solutions extend shelf life while reducing food waste.

ProAmpac expands with PAC Worldwide acquisition and recyclable films

ProAmpac announced its acquisition of PAC Worldwide in August 2025, strengthening its e-commerce packaging footprint. Its ProActive Recyclable® films are designed to replace hard-to-recycle laminates, widely adopted for snacks, pet food, and convenience foods.

Constantia Flexibles invests in sustainable mono-materials and acquisitions

Constantia Flexibles, a global producer of flexible packaging, completed its Aluflexpack acquisition in August 2025, boosting its presence in premium food packaging. Its Ecolutions® portfolio includes aluminum foil laminations and high-barrier films, with over €100 million invested in sustainable mono-material technology upgrades.

Flexible Packaging For Food And Beverages Market Share Insights

Pouches Hold the Largest Market Share by Packaging Type in Food and Beverages

Within flexible food and beverage packaging, pouches account for 35% of market share, reinforcing their position as the most versatile and innovation-driven format. Stand-up pouches (SUPs) with resealable zippers, spouts, and high-barrier laminates have become the industry standard, effectively replacing rigid formats by offering lightweight convenience, strong branding surfaces, and material efficiency. Bags remain the highest-volume category, particularly for staples like frozen vegetables, bread, and snacks, due to their cost-effectiveness and scalability for high-speed filling operations. Films and wraps, though often overlooked, serve as the foundation of the industry, functioning as substrates for laminates and as direct overwraps for fresh produce, meat, and cheese. Meanwhile, niche categories such as shrink sleeves, liquid cartons, and emerging compostable laminates carve out opportunities in specialized markets. The dominance of pouches underscores consumer preference for convenience and sustainability while ensuring manufacturers benefit from cost savings and extended shelf-life solutions.

Snacks & Savories Lead Application Share in Flexible Food Packaging

By 2025, snacks and savories represent the largest application in flexible food packaging with 25% share, reflecting strong consumer demand for convenient, single-serve formats and constant product innovation. Advanced adhesives play a pivotal role in ensuring barrier protection against oxygen and moisture, essential for maintaining freshness in chips, crackers, and nuts. Meat, poultry, and seafood packaging follows closely with 20% share, driven by the adoption of Modified Atmosphere Packaging (MAP) and high-barrier films to enhance food safety and reduce spoilage. Bakery, confectionery, beverages, and ready-to-eat meals form a diverse cluster, each requiring distinct adhesive and laminate solutions—from simple bread bags to retort pouches that withstand sterilization. Dairy and pet food packaging add further momentum, demanding durable, high-barrier formats for products like cheese, powdered milk, and large pet food packs. Collectively, this segmentation illustrates how snacks and proteins dominate the volume, while niche segments like beverages and ready meals push technological advancements in retort stability, barrier coatings, and resealable packaging features.

United States Flexible Packaging for Food and Beverages Market Driven by Sustainability and Smart Packaging Innovations

The U.S. flexible packaging for food and beverages market is navigating a complex regulatory environment, with growing adoption of Extended Producer Responsibility (EPR) laws, most recently in Maryland. These laws shift the responsibility for recycling and waste management from taxpayers to manufacturers, incentivizing the design of more recyclable, material-efficient, and mono-material packaging solutions. Technological advancements are a key growth driver, with innovations such as mono-material pouches for easier recycling and smart packaging integrating QR codes and NFC chips, enhancing supply chain traceability and consumer engagement through augmented reality experiences.

Corporate investments are strengthening production capabilities, exemplified by Sonoco Products Co.’s $30 million expansion to produce 100 million additional units of sustainable adhesive packaging for flexible formats. Demand is particularly strong in e-commerce and direct-to-consumer (DTC) segments, along with the food and beverage industries, driven by the need for robust, lightweight, and efficient packaging suitable for shipping. Sustainability remains a central business imperative, with eco-friendly materials, including bio-based films and recyclable paperboard, meeting growing consumer demand for environmentally responsible packaging solutions.

Germany Flexible Food Packaging Market Led by Circular Economy Practices and Regulatory Compliance

Germany’s flexible packaging for food and beverages market operates under stringent regulations, including the EU Packaging and Packaging Waste Regulation (PPWR) effective from February 2025. This mandates that all packaging be fully recyclable or reusable by 2030, with strict rules on recycled content and the elimination of hazardous chemicals such as PFAS. The country’s well-established Extended Producer Responsibility (EPR) system fosters innovation in recycling and sorting, incentivizing companies to create packaging that is easier to recycle, supported by strong consumer demand for reusable containers and trays for FMCG products.

Technological innovation is evident through the development of machinery capable of handling sustainable materials and digital product passports or watermarks to improve transparency and recyclability. Corporate initiatives, such as Amcor’s showcase of CleanStream technology at the Fachpack Expo 2025 in Nuremberg, highlight mechanically recycled polypropylene (PP) and sustainable flexible packaging innovations. Key applications include retail and food service sectors, with premium pouches and high-barrier films enhancing product shelf life while aligning with German consumers’ preference for high-quality, sustainable packaging solutions.

China Flexible Food Packaging Market Expanding under Green Policies and Domestic Manufacturing Focus

China’s flexible packaging for food and beverages market is propelled by governmental “dual carbon” goals and the March 2024 Action Plan for Large-Scale Equipment Updates and Consumer Goods Replacement, promoting sustainable materials and recycling practices. Regulatory reforms, such as the National Food Safety Standard for Adhesives in Food Contact Materials (GB 4806.15-2024), enforce safety limits on substances, ensuring consumer protection.

Technological advancements, including automation, AI, and “5G plus industrial internet” integration, optimize production efficiency and flexible capacity. A focus on domestic manufacturing is evident, with local companies expanding capabilities to substitute imported technologies and meet rising demand. The rapid growth of e-commerce and food delivery sectors drives market demand, with online grocery deliveries expected to contribute significantly to new flexible packaging volumes, reinforcing China’s position as a fast-growing hub for innovative food packaging solutions.

India Flexible Food Packaging Market Strengthened by Circular Economy Initiatives and Domestic Production

India’s flexible food packaging market benefits from government initiatives promoting a circular economy, including the Food Safety and Standards (Packaging) Regulations, 2018, which mandate food-grade materials while prohibiting the use of recycled plastics for food contact. Technological adoption is rising, with innovations like UFlex’s Electron Beam Coating Technology eliminating print carrier layers and offering Ascelpius™ BOPET film with up to 100% PCR content.

Corporate investments are robust, with UFlex operating over 100,000 TPA and maintaining four R&D laboratories approved by the Ministry of Industries. Key applications span the growing food and beverage and personal care sectors, with e-commerce expansion and sustainability trends fueling demand for high-performance flexible packaging. The “Make in India” initiative further supports domestic manufacturing, driving technological advancement and enabling local companies to meet rising national demand efficiently.

Japan Flexible Food Packaging Market Shaped by High-Performance Films and Technological Collaborations

Japan’s flexible packaging for food and beverages market leverages precision manufacturing and sustainability-driven innovations. In September 2024, Toppan Inc., in collaboration with RM Tohcello Co. Ltd. and Mitsui Chemicals Inc., developed a recycled BOPP film primed for mass production, reflecting a shift toward circular materials. Regulatory guidance under the Plastic Resource Circulation Act (April 2022) promotes environmental design and reduces single-use plastics, targeting 2 million tonnes per year of bio-based plastics by 2030, influencing packaging materials.

The market focuses on specialty and value-added films with superior barrier properties and IoT-enabled tracking, enhancing functionality for aging populations and single-person households. Innovations like easy-open tear notches and resealable closures improve usability, while strategic mergers and acquisitions, such as Sika AG’s acquisition of Hamatite from Yokohama Rubber Co. in 2022, have strengthened market presence and technological capabilities, particularly in automotive and construction segments, positioning Japan as a global leader in advanced flexible food packaging solutions.

Flexible Packaging for Food and Beverages Market Report Scope

Flexible Packaging For Food And Beverages Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$170.6 Billion

|

|

Market Size (2034)

|

$273.9 Billion

|

|

Market Growth Rate

|

5.4%

|

|

Segments

|

By Packaging Type (Pouches, Bags, Films & Wraps, Other Packaging Types), By Material Type (Plastics, Paper & Paperboard, Foils, Bioplastics), By Application (Bakery & Confectionery, Dairy Products, Meat, Poultry & Seafood, Ready-to-Eat Meals, Snacks & Savories, Pet Food, Beverages, Other Applications)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, Mondi Group, Huhtamaki Oyj, DS Smith plc, Smurfit Kappa Group plc, Sonoco Products Company, Sealed Air Corporation, Crown Holdings Inc., Graphic Packaging Holding Company, International Paper Company, WestRock Company, TC Transcontinental Packaging, UFlex Ltd., Constantia Flexibles Group, Berry Global Group, Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Flexible Packaging For Food And Beverages Market Segmentation

By Packaging Type

- Pouches

- Bags

- Films & Wraps

- Other Packaging Types

By Material Type

- Plastics

- Paper & Paperboard

- Foils

- Bioplastics

By Application

- Bakery & Confectionery

- Dairy Products

- Meat

- Poultry & Seafood

- Ready-to-Eat Meals

- Snacks & Savories

- Pet Food

- Beverages

- Other Applications

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Flexible Packaging For Food And Beverages Market

- Amcor plc

- Mondi Group

- Huhtamaki Oyj

- DS Smith plc

- Smurfit Kappa Group plc

- Sonoco Products Company

- Sealed Air Corporation

- Crown Holdings Inc.

- Graphic Packaging Holding Company

- International Paper Company

- WestRock Company

- TC Transcontinental Packaging

- UFlex Ltd.

- Constantia Flexibles Group

- Berry Global Group, Inc.

* List Not Exhaustive

Methodology

USDAnalytics adopted a comprehensive, multi-source research methodology to develop a robust analysis of the Global Flexible Packaging for Food and Beverages Market. Our approach integrated primary research through interviews with packaging manufacturers, converters, CPG brand representatives, sustainability experts, and regulatory bodies, along with secondary research using corporate filings, industry reports, regulatory databases, patent literature, and trade publications. The methodology evaluated market dynamics across packaging types, materials, and applications, focusing on trends such as mono-material packaging, high-barrier bio-based films, smart and active packaging, and sustainability-driven innovations including recyclable, compostable, and PCR-based solutions. Regional regulatory impacts from the EU, U.S., China, India, and Japan were assessed to understand compliance requirements and market adoption. USDAnalytics also examined mergers and acquisitions, technology integration, supply chain shifts, and digital watermarking initiatives to provide actionable, professional-grade insights for stakeholders seeking growth strategies, innovation opportunities, and sustainable packaging solutions in the food and beverage sector.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.