Market Overview: Home Care Packaging Market to Hit $168.1 Billion by 2034 on Refill Systems, Smart Labels, and Lightweighting

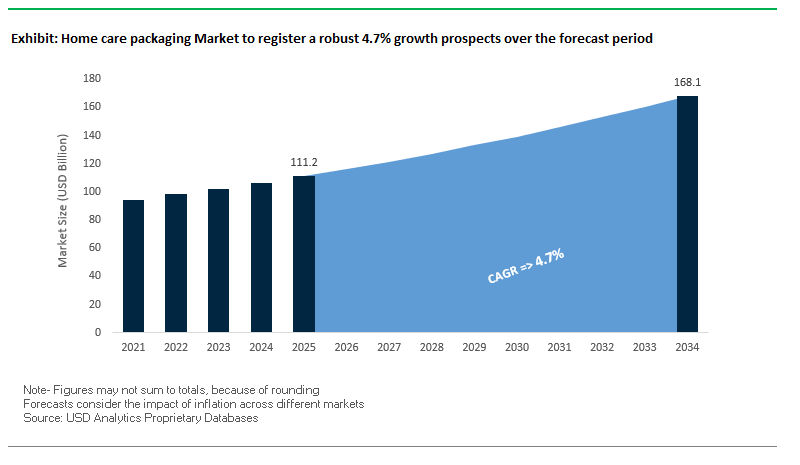

The global home care packaging market is valued at $111.2 billion in 2025 and is projected to reach $168.1 billion by 2034, expanding at a CAGR of 4.7%. Packaging in household care (laundry, dish care, surface cleaners, air care) must deliver chemical resistance, consumer safety, and convenience while meeting escalating circularity and carbon-reduction goals. The competitive edge now depends on recyclable mono-materials, reusable/refill formats, and digital engagement that drives loyalty and basket size.

Brands are shifting to refillable systems and single-material flexible pouches to reduce plastics; P&G’s paper-based bottle pilot for dishwashing liquid in Germany (2025) aims to cut plastic by ~30%. Smart packaging QR codes and interactive IDs improves transparency, while lightweighting trims resin use and freight emissions (e.g., Aptar’s lighter closures, Aug 2024). Despite new materials, plastic bottles remain the dominant primary pack for liquids; pouches and sachets are the fastest-growing formats due to low material intensity, ship-in-product efficiency, and affordability.

Key Insights for buyers and technical leaders

- Refill & reuse economics: Refillable packaging and mono-material PE/PP pouches cut plastic and enable curbside or store-drop recycling where systems exist.

- Smart engagement & traceability: QR-enabled packs unlock usage tips, SDS access, authenticity checks, and promotions that lift retention.

- Lightweighting ROI: Mass reductions across bottles/closures lower freight emissions and resin cost without compromising performance.

- Format evolution: Bottles lead, but pouches/sachets post the fastest growth on cost, convenience, and e-commerce handling.

Market Analysis: M&A Scale-Ups, Mono-Material Pouches, and AI-Driven Quality (2024–2025)

The home care packaging landscape has been reshaped by portfolio-consolidating M&A, recycle-ready film systems, and factory digitalization.

In August 2025, Amcor reported strong Q4 FY2025 with +43% YoY net sales, reflecting scale benefits after acquiring Berry Global (deal closed April 2025) and deeper penetration in home and personal care. Converters and material suppliers are simultaneously pushing recyclable mono-materials: Mondi flagged new solutions (e.g., FlexiBag Reinforced) at FACHPACK (Aug 2025), while Amcor & Mespack (Nov 2024) launched a 2L AmPrima recycle-ready stand-up pouch, designed for home care refills.

Hardware and inspection are also inflecting. Aptar (Aug 2025) introduced a 2 Disc Top Lite closure in PP with PCR, enabling lower part weight for medium-to-high viscosity cleaners. Upstream, Krones’ acquisition of Netstal (Apr 2025) advances closed-loop PET relevant for HD blow-mold lines that coexist with PET in chemicals and cleaners. Unilever’s AI vision system upgrade in Poland (Oct 2024) improved packing accuracy and cut waste by 22%, underscoring the ROI of automation and in-line QA. On metal lines, Sonoco’s acquisition of Eviosys (Dec 2024) deepens capabilities in aerosols and metal packaging for home and pet/home-chem segments. These moves, coupled with Smurfit Kappa–WestRock’s merger (Jul 2025) on the fiber side, signal a market converging on design-for-recycling, lighter components, and digital process control to reduce cost-to-serve and emissions.

Trends and Opportunities Transforming the Home Care Packaging Market

Strategic Shift to Refillable and Concentrated Solutions to Reduce Plastic Use

The home care packaging market is undergoing a fundamental shift as refillable systems and concentrated product formats emerge as the cornerstone of corporate sustainability strategies. Global FMCG companies are accelerating the rollout of refill-and-reuse programs that reduce virgin plastic consumption, lower packaging waste, and reshape consumer behavior around product replenishment.

Unilever is leading with over 50 refill pilot programs launched since 2018, including more than 1,000 refill stations in Indonesia, collectively eliminating more than 6 tonnes of plastic waste through sales of 91,000 liters of product. Concentrated solutions are another fast-scaling model. For example, OMO’s 6x concentrated laundry liquid in Brazil reduced plastic use by 70% and eliminated approximately 1,500 tonnes of virgin plastic. Similarly, direct-to-consumer disruptors such as Blueland are gaining traction with tablet-based cleaning products shipped in compostable refills, reporting over 1 million homes transitioned to plastic-free cleaning systems. These examples highlight how refill and concentrate formats are reshaping packaging design while addressing regulatory, environmental, and consumer expectations for sustainability.

Integration of Post-Consumer Recycled (PCR) Content as an Industry Standard

Post-consumer recycled content has moved from an optional feature to an industry-wide requirement in home care packaging. Regulatory mandates, corporate ESG commitments, and consumer pressure for sustainable packaging are converging to make rPET and rHDPE bottles a market standard.

Global leaders are driving this transformation. Unilever aims to achieve 100% recyclability for rigid plastic packaging by 2030, while Procter & Gamble (P&G) targets a 50% reduction in virgin plastic use by the same deadline. Suppliers are scaling up accordingly: a European division of a major packaging company reported a 36% YoY increase in PCR polyethylene (PE) use in 2024, signaling strong infrastructure investment. Partnerships are also key Berry Global’s collaboration with The Bio-D Company enabled the launch of 100% PCR reusable bottles, demonstrating how supplier-brand alliances are critical to achieving circularity goals. These efforts are not only meeting regulatory thresholds but also creating consumer-facing sustainability narratives, where packaging plays a direct role in brand differentiation.

Development of Advanced Monomaterial and Polymer-Lite Pouches

The growing demand for refill pouches and regulatory scrutiny of non-recyclable laminates are creating a clear opportunity to innovate monomaterial and polymer-lite structures. The next generation of refill packaging is expected to combine recyclability with barrier performance, enabling large-scale adoption by FMCG brands.

Mondi Group has pioneered a mono-material retort pouch using high-barrier film instead of aluminum, recyclable in polyolefin streams. Similarly, ProAmpac’s ProActive Recyclable PE-based pouches target the home care sector with enhanced sustainability while maintaining shelf-life protection. By reducing the polymer mix to a single substrate, these pouches overcome the recycling challenges of multi-layer films and are compatible with existing waste infrastructure. Furthermore, ongoing R&D investments into barrier performance and reduced material intensity are positioning monomaterial pouches as regulatory-compliant, cost-competitive, and brand-friendly solutions that can scale across detergent, surface cleaner, and air care categories.

Incorporating Connected Packaging for Supply Chain Transparency and Consumer Engagement

The digitalization of packaging is opening new frontiers for home care brands, transforming containers from static vessels into interactive consumer engagement platforms. The integration of QR codes, NFC chips, and unique identifiers enables a dual function offering consumers transparent product information and empowering brands with data-driven insights.

A smart packaging trends report notes that scanning a QR code allows consumers to instantly access ingredient transparency, usage tutorials, promotional offers, and recycling instructions. This strengthens consumer trust and loyalty while aligning with regulatory pushes for digital labeling. Additionally, connected packaging enhances supply chain transparency, giving consumers visibility into a product’s carbon footprint, ethical sourcing credentials, and recyclability profile. Anti-counterfeiting is another emerging use case, particularly relevant for premium or eco-labeled home care products, where unique identifiers ensure product authenticity. This opportunity positions connected packaging as a value-added tool for compliance, consumer education, and brand protection, reinforcing packaging’s role at the center of digital transformation in FMCG.

Competitive Landscape: Scale, Circular Materials, and Dispensing Performance Define Leaders

The global home care packaging market is led by multinationals that blend materials science, dispensing hardware, and automation-friendly formats. Success is defined by PCR content integration, bio-based resins, mono-material pouches, and precision closures/pumps that survive aggressive chemistries and high-cycle use.

Vendors that pair recycle-ready films, PCR-rich rigid formats, and e-commerce validated closures stand out. Differentiation comes from M&A-enabled breadth, lab-to-line application support, and localized manufacturing to cut lead times and scope-3 emissions.

Amcor PLC Scale leader in recycle-ready pouches and rigid-flex portfolios

Amcor commands a broad range of flexible and rigid solutions for detergents, dish care, surface and toilet cleaners. The Berry Global acquisition (Apr 2025) markedly expands bottles, closures, films, and healthcare adjacencies driving operational scale in home care. Innovation centers underpin AmPrima recycle-ready films and the 2L stand-up pouch (Nov 2024), targeting refill stations and large-format e-commerce. With global R&D and barrier know-how, Amcor aligns performance with retailer recyclability specs and brand CO₂ targets.

Berry Global, Inc. PCR leadership and circular resin platforms

Now part of Amcor (2025), Berry contributes deep expertise in rigid bottles, closures, and specialty containers for household/industrial cleaners. It is introducing high-quality PCR polymers for non-contact-sensitive home/industrial packaging and advancing “More Together” circularity initiatives across recyclability-by-design and bio-based resins. Berry’s footprint and tooling depth sustain fast SKU proliferations and regional supply assurance.

Silgan Holdings Inc. Engineered rigid plastics and custom container programs

Silgan Custom Containers supplies highly engineered rigid polymer packs for home and industrial care, focusing on PCR and bio-resin integration and material down-gauging. A long-standing North American footprint (22 plants) supports speed-to-market and tooling agility; 2024 custom-container sales of ~$650M reflect steady growth. As a member of the New Plastics Economy, Silgan partners with brands on recyclability and resin reduction without compromising stress-crack resistance or chemical compatibility.

Sonoco Products Company Metal aerosols + fiber & flexible breadth

Sonoco spans rigid paper, flexibles, rigid plastics, and metal. The Eviosys acquisition (Dec 2024) enhances aerosol and metal capabilities key in air care and specialty household categories. Sonoco’s Consumer Packaging segment surged in Q2 2025 (helped by M&A and volume), while procurement and fixed-cost programs delivered measurable productivity gains. The breadth enables multimaterial system solutions matched to performance and sustainability goals.

AptarGroup, Inc. Dispensing science and e-commerce ready closures

Aptar leads in dispensing pumps, sprays, and actuators for home and personal care. The 2 Disc Top Lite (Aug 2024) reduces weight using PP/PCR, and Aptar’s twist-to-lock and tamper-evident features protect integrity across omnichannel. With 25 regional manufacturing/R&D centers, Aptar localizes supply and co-develops geometry + rheology for tricky viscosities (gel cleaners, concentrates) to improve dose control and user experience.

Mondi plc Paper-to-flexible mono-material innovation at scale

Mondi offers kraft/functional papers and flexible films for home care refills and wipes. Its recyclable FlexiBag Reinforced widens mono-PE use cases (originating in pet food, extensible to consumer/home care). Under MAP2030, Mondi expands EcoWicketBag capacity for hygiene/home care and advances FunctionalBarrier Paper where paper can replace multilayer plastics. Mondi’s “sustainable by design” program aligns with retailer scorecards and brand CO₂ roadmaps.

Home care packaging Market Share Insights

Rigid Packaging Leads Market Share by Packaging Type

Rigid packaging dominates the home care packaging market, projected to capture 55% of total share in 2025. Its leadership is rooted in the widespread use of HDPE and PET bottles, jugs, and jars across high-volume categories such as laundry detergents and dishwashing liquids. Consumers consistently prefer rigid formats for their durability, stackability, and ease of dispensing through flip-tops, trigger sprays, or pump caps, which also enhance product convenience and shelf visibility. Flexible packaging is gaining momentum, particularly through lightweight pouches and refill packs that reduce plastic consumption by more than 70%, aligning with brand sustainability targets and eco-conscious consumer preferences. Meanwhile, aerosol packaging continues to hold a niche presence, largely in air fresheners and specialized cleaning solutions, where its fine mist delivery and one-touch application provide unmatched performance despite environmental concerns around propellants and recycling. Collectively, the packaging type landscape reflects a balance between durability, convenience, and sustainability-driven innovation.

Laundry Care Dominates Home Care Packaging Market Share by Product

By product category, laundry care remains the largest and most influential segment, projected to account for 40% of the home care packaging market in 2025. Its dominance stems from universal household penetration, frequent consumption cycles, and large packaging volumes, ranging from liter-sized bottles and powder boxes to innovative unit-dose pods. Packaging diversity in this segment is unmatched, blending rigid bottles for traditional liquid detergents, flexible pouches for ultra-concentrated refills, and carton formats for powders. Surface and toilet cleaners represent another major share, relying heavily on rigid bottles with trigger sprays for user convenience, though flexible refill pouches are increasingly popular as sustainability goals accelerate. Dishwashing products maintain a stable share, supported by daily consumer use and packaging formats designed for moisture protection and precise dosing. Air fresheners, while smaller in scale, are strongly tied to aerosol packaging, complemented by gels, reed diffusers, and electric devices that enhance household ambiance. Across all product segments, the shift toward sustainable packaging is a unifying theme, with brands adopting rPET and rHDPE in rigid formats, introducing refill packs to reduce plastic waste, and exploring water-soluble films for unit-dose cleaning products.

United States: Sustainability and E-Commerce Driving Packaging Innovation

The U.S. home care packaging market is experiencing rapid transformation, driven by sustainability and the booming e-commerce sector. Companies like P&G are pioneering eco-friendly solutions, including recyclable paper bottle prototypes, which reduce plastic usage and align with consumer demand for environmentally responsible packaging. Lightweighting is a major trend, with brands focusing on durable, lighter containers that reduce transportation costs and carbon emissions while improving consumer convenience. Concentrates and refill pouches are gaining popularity, with initiatives like Unilever’s “Love Home & Planet” brand emphasizing recyclable and refillable packaging solutions. Additionally, innovations in dispensing systems including ergonomic pumps and sprayers enhance usability and reduce product waste, improving the overall customer experience.

United Kingdom: Circular Economy Policies and Refillable Packaging Transform the Market

The UK home care packaging industry is strongly influenced by governmental sustainability initiatives. The Extended Producer Responsibility (EPR) policy incentivizes producers to design packaging for recyclability and reuse, creating demand for eco-friendly materials. The £60 million Smart Sustainable Plastic Packaging (SSPP) Challenge by UKRI fosters research in advanced recycling technologies and refillable packaging trials, supporting innovation across the sector. Reusable and refillable models are becoming mainstream, with in-store trials and new designs making it easier for consumers to adopt sustainable practices. Additionally, the UK’s Plastic Packaging Tax, which applies to packaging with less than 30% recycled content, has driven companies to invest in post-consumer recycled (PCR) materials, strengthening the circular economy.

China: Urbanization and E-Commerce Fuel Demand for Durable and Aesthetic Packaging

China’s home care packaging market is being shaped by rapid urbanization, evolving lifestyles, and the fast-growing e-commerce and social-commerce sectors. Consumers increasingly demand convenient, compact packaging suitable for smaller urban homes. Sustainable practices are prioritized due to governmental plastic bans and waste management regulations, prompting manufacturers to adopt recyclable and eco-friendly materials. Home care packaging designed for durability and visual appeal supports social media “unboxing” experiences, while advancements in automation and AI, including robotic handling and intelligent production lines, are enhancing manufacturing efficiency and operational stability.

India: Make in India and Sustainability Initiatives Driving Growth

India’s home care packaging market is expanding, supported by the Make in India initiative, which has attracted capital investment and foreign manufacturing facilities. The Plastic Waste Management (Amendment) Rules, 2022, banning single-use plastics, have spurred demand for eco-friendly alternatives. Rapid growth in e-commerce and modern retail channels is driving innovation in secure and visually appealing packaging that enhances the unboxing experience. Indian companies are increasingly focusing on high-quality, branded packaging to strengthen brand identity and differentiate themselves in a competitive market, fueling the demand for customized, premium solutions.

Brazil: Circular Economy and Bioplastics Innovation Shaping the Packaging Industry

The Brazilian home care packaging market is evolving with strong government initiatives aimed at promoting a circular economy. Upcoming decrees requiring companies to recycle significant portions of their products are expected to increase demand for recyclable packaging. The rapid growth of e-commerce has further amplified the need for secure, efficient packaging solutions. Innovations in bioplastics, such as green polyethylene produced from sugarcane ethanol, are creating competitive pressure across the packaging sector, encouraging companies to adopt sustainable alternatives and stay relevant in a rapidly changing market landscape.

Japan: Compact Packaging and High Standards Supporting Market Expansion

Japan’s home care packaging industry is heavily influenced by demographic trends, particularly the high percentage of single-person households, which drives demand for compact, small-format packaging. Manufacturers are responding with customizable machinery for individual packaging solutions that meet consumer needs. Strict regulatory standards ensure hygiene, product safety, and high quality, while the country’s extensive recycling infrastructure over 18 glass recycling plants converting glass into cullets and powders creates a favorable environment for paper-based and recyclable packaging. This combination of innovation, compliance, and sustainability continues to strengthen Japan’s position in the global home care packaging market.

Home Care Packaging Market Report Scope

Home care packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$111.2 Billion

|

|

Market Size (2034)

|

$168.1 Billion

|

|

Market Growth Rate

|

4.7%

|

|

Segments

|

By Material Type (Plastics, Paper & Paperboard, Metal, Glass, Composites), By Packaging Type (Flexible Packaging, Rigid Packaging, Aerosol Packaging), By Product (Laundry Care, Dishwashing, Surface & Toilet Cleaners, Air Fresheners, Other Home Care Products)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, Berry Global Group, Inc., Mondi Group, Silgan Holdings Inc., Pactiv Evergreen Inc., Huhtamaki Oyj, Sonoco Products Company, AptarGroup, Inc., Crown Holdings Inc., WestRock Company, DS Smith Plc, TC Transcontinental Inc., Uflex Limited, Alpla Group, Sealed Air Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Home care packaging Market Segmentation

By Material Type

- Plastics

- Paper & Paperboard

- Metal

- Glass

- Composites

By Packaging Type

- Flexible Packaging

- Rigid Packaging

- Aerosol Packaging

By Product

- Laundry Care

- Dishwashing

- Surface & Toilet Cleaners

- Air Fresheners

- Other Home Care Products

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Home care packaging Market

- Amcor plc

- Berry Global Group, Inc.

- Mondi Group

- Silgan Holdings Inc.

- Pactiv Evergreen Inc.

- Huhtamaki Oyj

- Sonoco Products Company

- AptarGroup, Inc.

- Crown Holdings Inc.

- WestRock Company

- DS Smith Plc

- TC Transcontinental Inc.

- Uflex Limited

- Alpla Group

- Sealed Air Corporation

*List not Exhaustive

Research Coverage

This report investigates the global home care packaging market, highlighting recent breakthroughs in refillable systems, mono-material pouches, smart labeling, and lightweighting initiatives. USDAnalytics’ analysis reviews emerging trends, regulatory drivers, and technological innovations reshaping packaging for laundry, dishwashing, surface, and air care products. The report highlights the integration of AI-driven quality control, sustainable resin adoption, and circular economy strategies, offering critical insights into evolving consumer preferences and operational efficiency. Additionally, this report is an essential resource for manufacturers, converters, packaging engineers, and investors seeking to understand competitive dynamics, supply chain resilience, and the adoption of high-performance, eco-friendly solutions. By tracking M&A activity, polymer innovation, dispensing system design, and connected packaging for traceability and consumer engagement, the study provides a holistic perspective on market growth, product differentiation, and sustainability imperatives from 2021 to 2034.

Scope Highlights:

- Segmentation: By Material Type (Plastics, Paper & Paperboard, Metal, Glass, Composites), By Packaging Type (Flexible Packaging, Rigid Packaging, Aerosol Packaging), By Product (Laundry Care, Dishwashing, Surface & Toilet Cleaners, Air Fresheners, Other Home Care Products)

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Historic Data: 2021–2024; Forecast Data: 2025–2034

- Companies Covered: Analysis and profiles of 15+ leading companies including Amcor plc, Berry Global Group, Mondi Group, Silgan Holdings Inc., AptarGroup Inc., Sonoco Products Company, Huhtamaki Oyj, Crown Holdings Inc., WestRock Company, Pactiv Evergreen Inc., DS Smith Plc, TC Transcontinental Inc., Uflex Limited, Alpla Group, and Sealed Air Corporation

Methodology

The study employs a multi-layered methodology combining both primary and secondary research to ensure accuracy and reliability. Primary research involved structured interviews with executives, product managers, and supply chain specialists from leading packaging manufacturers, converters, and FMCG brands, providing real-time insights into production trends, sustainability adoption, and smart packaging integration. Secondary research encompassed analysis of company reports, investor presentations, regulatory publications, trade journals, and industry databases. Quantitative models, including bottom-up and top-down approaches, were applied to derive market sizing, share, and growth projections from 2021 to 2034. USDAnalytics further validated data using triangulation techniques, integrating insights from regional trends, raw material costs, consumer adoption patterns, and technological innovation pipelines to produce a robust, forecast-ready market analysis suitable for strategy formulation and investment decision-making.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.