Hot Drinks Packaging surges on single-serve, sustainability, and smart labels (2025–2034)

The Global Hot Drinks Packaging Market is scaling quickly as coffee and tea brands pivot to single-serve, on-the-go, and RTD formats while meeting low-carbon, recyclable, compostable, and bio-based requirements. Growth is underpinned by insulated paper cups, coffee pods/sachets, high-barrier pouches, and aseptic cartons that preserve aroma, heat, and food safety. At the same time, smart packaging (QR/NFC) raises engagement and traceability, and premium printing/structures lift shelf impact in convenience retail and e-commerce.

Key Insights for Industry Professionals:

- Format shift drives volume: Single-serve pods, sachets, and insulated cups lead urban, on-the-go demand; aseptic cartons expand RTD hot coffee/tea.

- Sustainability is table stakes: Rapid switch to recyclable/compostable fibers, bio-circular polymers, and mono-material paper solutions to meet EPR and retailer scorecards.

- Barrier & thermal performance matter: Oxygen/light barriers and cup insulation remain critical to aroma retention, heat-hold, and spill-resistance.

- Digitization accelerates: QR/NFC enables provenance, brewing guidance, and recycling instructions fueling loyalty and data capture.

- Premiumization lifts ASPs: Specialty coffee/tea players pay for tactile finishes, shaped cartons, and high-fidelity graphics to stand out in RTD and D2C.

Market Analysis anchored in dated developments and investable signals

Momentum in sustainable hot drink formats intensified through 2025. In February 2025, Amcor launched AmFiber Performance Paper stand-up pouches for instant coffee, citing a 73% carbon-footprint reduction versus standard pouches signaling retailer-friendly, fiber-first transitions at scale. June 2025 saw Elopak roll out cartons combining recycled PE and bio-circular polymers, reinforcing the shift to renewable, low-plastic inputs. Parallel to materials innovation, January 2025 introduced Wiliot’s IoT packaging for end-to-end visibility, supporting traceability, shelf-life management, and post-consumer recycling guidance via connected labels.

Strategic consolidation is reshaping supplier breadth and bargaining dynamics. The Amcor–Berry all-stock combination closed in July 2025, creating a heavyweight across flexibles, rigids, and closures with deep R&D scale for coffee/tea applications. In March 2025, DS Smith–Mondi merger talks advanced (proposed all-stock deal), pointing to a stronger fiber-based ecosystem for cups, sleeves, carriers, and paper-based pouches. Material platforms also broadened: Mondi (March 2025) showcased cross-category paper stand-up pouches that transfer readily into hot drinks refill programs. Supporting e-commerce and protective transit, Smurfit Kappa invested over $15M in UK honeycomb capacity in August 2025, improving curbside-recyclable void fill for D2C coffee/tea subscriptions.

Finally, smart packaging accelerated as a mainstream spec: July 2025 reports highlighted brand adoption of QR/NFC/RFID for origin storytelling, brewing tips, loyalty ties, and recycling instructions capabilities that reduce consumer confusion and bolster EPR compliance. With Unilever (December 2024) doubling packaging R&D and prioritizing recyclable/compostable “Future Flexibles,” the supply base is firmly aligned to circularity, barrier performance, and digital engagement the three pillars driving 2025–2034 growth.

Innovative Trends and High-Value Opportunities in Hot Drinks Packaging

Strategic Shift to Mono-Material and Polymer-Barrier Flexible Pouches

The hot drinks packaging market is undergoing a major transformation as leading beverage brands adopt mono-material polyolefin pouches (PP or PE) to meet ambitious recyclability and circular economy targets. Global brands are committing to make all consumer packaging reusable, recyclable, or compostable by 2030, creating a clear industry push toward sustainable mono-material solutions. Innovation in barrier technology is central to this trend, with multi-layer mono-material structures using transparent polymer coatings or advanced layers replacing traditional aluminum foil. These pouches provide the same high-barrier protection against oxygen and moisture, preserving coffee freshness while remaining compatible with existing recycling streams.

Packaging suppliers are responding with mono-material coffee bags featuring integrated recyclable zippers and one-way degassing valves, ensuring full compatibility with LDPE #4 or PP #5 recycling streams. These solutions represent a strategic growth avenue, allowing brands to balance product protection with environmental responsibility. The shift also necessitates close collaboration between film manufacturers and recyclers, ensuring smooth integration into the circular economy while maintaining high-quality packaging performance.

Integration of Smart Features for Authenticity and Brewing Connectivity

Smart packaging is increasingly redefining the consumer experience in hot drinks, offering both engagement and product integrity. Brands are embedding QR codes and NFC chips to provide consumers with product information, verify authenticity, and facilitate recycling instructions. This approach protects high-value brands from counterfeiting, especially in complex international supply chains.

For single-serve coffee systems, smart packaging enables a connected brewing experience. Through NFC or QR-enabled pods, coffee machines can automatically adjust brewing parameters water temperature, pressure, and flow rate based on the roast profile. This ensures consistent, high-quality coffee with minimal user intervention, creating a premium consumer experience and reinforcing brand loyalty. The integration of smart features positions hot drinks packaging as both functional and interactive, opening opportunities in digital engagement and data collection for market intelligence and personalization strategies.

Development of Compostable and Bio-Based Coffee Pods

The shift toward sustainable single-serve solutions creates a significant opportunity in compostable and bio-based coffee pods. Certification standards such as TÜV Austria “OK compost INDUSTRIAL” ensure that these pods break down in industrial composting facilities within 12 weeks, reinforcing consumer trust and end-of-life processing.

Innovations in bio-polymers and polysaccharide-based films are enabling pods to withstand high-temperature, high-pressure brewing while maintaining oxygen barrier properties and structural integrity. Corporate leaders like Keurig Dr Pepper have invested in fully compostable K-Cup® pods, validating the commercial potential and underscoring the R&D efforts driving sustainable packaging adoption. This opportunity aligns with circular economy objectives and addresses growing consumer demand for eco-friendly packaging in premium hot drinks.

Lightweighting and Alternative Materials for Instant Beverage Jars

Lightweighting presents another high-value opportunity, particularly for instant coffee and hot chocolate jars. Incorporating recycled glass (cullet) reduces energy usage by up to 74% and saves raw materials, significantly lowering the carbon footprint of packaging production. Transitioning to lightweight, recyclable PET alternatives further enhances sustainability, as seen in companies achieving a 60% weight reduction compared to traditional glass containers.

Using high levels of post-consumer recycled (PCR) content not only aligns with circular economy goals but also provides a competitive advantage in an increasingly environmentally conscious market. This dual focus on material innovation and recyclability enables hot drinks brands to reduce costs, minimize environmental impact, and meet consumer expectations for sustainable packaging solutions.

Competitive landscape: who leads in aseptic cartons, fiber formats & barrier flexibles

A concentrated group of global packaging leaders is scaling aseptic carton systems, paper-based barrier structures, and recycle-ready flexibles for coffees and teas. Their strategies converge on renewable materials, mono-material design, equipment speed/uptime, and smart-label enablement.

Tetra Pak expands high-speed aseptic for RTD hot beverages

Positioning: Global benchmark in aseptic carton technology that locks in quality and shelf life without refrigeration.

Portfolio: Tetra Brik® Aseptic and Tetra Rex® Plant-based cartons, plus paper-based barrier alternatives to aluminum to advance recyclability.

Innovation: E3/Speed Hyper line produces up to 40,000 packs/hour with electron-beam sterilization (≈99% chemical reduction; up to 45% less water), cutting OPEX and footprint.

Strategy: Scale renewable, low-carbon packaging and circular end-of-life systems while enabling brand differentiation and traceability for coffee/tea.

SIG Combibloc pushes alu-free structures and design differentiation

Positioning: Aseptic systems specialist with flexible filling and shelf-differentiated carton shapes for RTD coffee/tea.

Portfolio: Combibloc formats optimized for hot drinks; options include aluminum-free materials to reduce environmental impact.

Innovation: combishape structural designs enhance ergonomics and premium look/feel; line flexibility supports SKUs from functional teas to café-style lattes.

Strategy: Drive responsibly sourced materials, lifecycle impact reduction, and format agility for rapid NPD cycles.

Elopak advances bio-circular content and fiber-based closures

Positioning: Paper-based packaging champion expanding from chilled into aseptic with low-plastic dependency.

Developments: In June 2025, launched cartons with recycled PE + bio-circular polymers; in March 2025, invested in Blue Ocean Closures for fiber-based caps on gable-tops.

Portfolio: Pure-Pak® and D-PAK cartons; Natural Brown Board variants lower plastic and deliver a premium, “natural” aesthetic for specialty coffee.

Strategy: “Repackaging Tomorrow” roadmap to double down on renewable inputs, lower Scope 3, and replace PET where performance allows.

Smurfit Kappa scales fiber systems for D2C and retail multipacks

Positioning: Paper-based leader delivering TopClip (plastic-free can multipacks), Pouch-Up®, and Bag-in-Box® for hot drinks supply chains.

Developments: August 2025 UK investment (>$15M) in honeycomb sheets bolsters protective, curbside-recyclable e-commerce flows for coffee/tea.

Value prop: Integrated design-to-distribution capability (graphics, retail-ready, transit protection) to cut total system cost and emissions.

Strategy: Under Better Planet Packaging, replace plastics with recyclable fiber while maintaining barrier/strength via coatings and structural design.

Amcor accelerates paper-based and mono-material flexible coffee packs

Positioning: Scaled global player in flexibles/rigids (post-July 2025 combination with Berry) with deep hot drinks expertise.

Developments: February 2025 AmFiber Performance Paper coffee refill pouch delivering ~73% CO₂ reduction vs. standard pouches.

Portfolio: High-barrier pouches, lidding films, sachets for coffee/tea aroma and freshness; mono-material and paper solutions tuned for recyclability.

Strategy: Make all packaging recyclable or reusable, prioritize barrier + sustainability, and support brands with LCAs and line performance at scale.

Hot Drinks Packaging Market Share Insights

Pouches & Sachets Dominate Market Share by Packaging Type in Hot Drinks Packaging

Pouches and sachets account for 40% of the hot drinks packaging market in 2025, cementing their role as the most widely used format for coffee, tea, and hot chocolate powders. Their high share is driven by their ability to offer excellent oxygen and moisture barrier protection while ensuring affordability and portion control. This dominance reflects the immense global demand for ground coffee, whole beans, loose-leaf tea, and instant mixes, where freshness and convenience are non-negotiable. Cups and containers, with 25% share, are indispensable in the out-of-home and ready-to-drink (RTD) segment, where paper cups, instant coffee jars, and tea tins define consumption in cafés, offices, and events. Bottles and lids are gaining traction in the booming cold-brew and iced tea market, while cans are enjoying a niche revival as sustainable, recyclable packaging formats for RTD beverages. Collectively, this segmentation demonstrates how pouches dominate the at-home consumption market, while cups, bottles, and cans capture the rising out-of-home and premium RTD categories.

Coffee Industry Leads Market Share by Application in Hot Drinks Packaging

Coffee represents 60% of the hot drinks packaging market in 2025, firmly establishing it as the segment’s primary growth engine. Global coffee consumption spans all packaging types from pouches for beans and ground coffee, sachets for instant mixes, pods for single-serve systems, and the billions of disposable cups used in cafés worldwide making it the most influential application by both volume and value. Tea represents the second largest share, fueled by its diverse formats: loose-leaf in resealable pouches, premium teas in tins, single-serve bags in sachets, and ready-to-drink bottles or cans. Hot chocolate and malted beverages occupy a smaller but resilient share, particularly in colder markets, where sachets and pouches dominate as portion-controlled, family-friendly packaging solutions. The “Others” category, including functional powders such as matcha, chai latte mixes, and wellness drinks, is expanding as health-conscious consumers adopt specialty beverages, often requiring premium packaging formats that communicate quality. This segmentation illustrates how coffee anchors the majority of packaging demand, tea diversifies applications across formats, and niche wellness beverages drive premiumization trends.

United States Hot Drinks Packaging Market Accelerates Through Sustainability and Smart Innovations

The U.S. hot drinks packaging market is heavily shaped by California’s SB-54 Extended Producer Responsibility (EPR) law, which mandates a 25% reduction in plastic use by 2032 and establishes a $5 billion waste fund. This regulatory environment is driving growth in sustainable materials like recyclable paper and aluminum for coffee, tea, and ready-to-drink (RTD) beverages. Technological advancements, including barrier coatings for paper cups and integration of QR codes for traceability and recycling guidance, are enhancing both product protection and consumer transparency.

Corporate strategies are also influencing market growth. Amcor’s planned acquisition of Berry Global Group, expected in mid-2025, will consolidate capabilities and boost R&D investments in sustainable hot drinks packaging solutions. Key applications are concentrated in coffee and tea sectors, fueled by on-the-go consumption trends and e-commerce expansion. Sustainability remains central, with bio-based films and recyclable paperboard packaging increasingly adopted to meet environmental expectations and consumer demand for eco-friendly hot drinks packaging.

Germany Hot Drinks Packaging Market Thrives on Circular Economy Leadership and Regulatory Compliance

Germany’s hot drinks packaging industry operates under a stringent regulatory framework, notably the EU Packaging and Packaging Waste Regulation (PPWR), effective February 2025. This legislation mandates fully recyclable or reusable packaging by 2030 and defines rules on recycled content, directly impacting hot beverage packaging. The German Packaging Act (VerpackG) further incentivizes recyclable design through modulated fees, favoring paper and aluminum solutions.

Technological innovation is key, with manufacturers exploring new films and paper coatings, such as extrusion barriers, that combine liquid protection with recyclability. The market sees strong demand in coffee and tea sectors, particularly single-serve and ready-to-drink formats. Germany’s robust manufacturing base, coupled with an emphasis on sustainability, is encouraging adoption of high-performance, eco-friendly packaging.

China Hot Drinks Packaging Market Advances with Regulatory Reforms and Smart Manufacturing

China’s hot drinks packaging market is being transformed by governmental initiatives targeting the “dual carbon” goal, driving the adoption of sustainable materials and recycling practices. The March 2024 Action Plan for Large-Scale Equipment Updates and Consumer Goods Replacement encourages greener packaging solutions. Regulatory reforms, including GB/T 31268 effective November 2024, limit excessive packaging, defining standards for layers and void ratios, which directly affect e-commerce hot drinks packaging.

Technological advancements, including AI, automation, and integration of “5G plus industrial internet,” are optimizing production efficiency and flexibility. Corporate collaborations, such as Dow’s partnership with Mengniu to develop mono-material PE pouches, illustrate a focus on recyclable, functional packaging. Domestic manufacturing is expanding, allowing local producers to meet increasing demand for high-quality, circular hot drinks packaging solutions.

India Hot Drinks Packaging Market Gains from Circular Economy Policies and Automation

India’s hot drinks packaging market is being driven by the government’s circular economy initiatives and the draft Environment Protection (Extended Producer Responsibility for Packaging) Rules, 2024. These policies promote sustainable manufacturing, particularly for coffee and tea packaging. Technological adoption is increasing, with automated printing systems and nanofabrication techniques used to enhance barrier coatings and extend shelf life.

Corporate investments are accelerating, such as Tetra Pak’s introduction of certified recycled polymer packaging in February 2025. Key applications include urban consumption, e-commerce, and the expanding food processing sector. The demand for high-performance, sustainable packaging is being fueled by consumer preferences for eco-friendly hot drinks solutions, combined with rising awareness of recyclable and bio-based materials.

Japan Hot Drinks Packaging Market Focuses on Heat-Resistant, Functional Packaging

Japan’s hot drinks packaging market benefits from advanced precision manufacturing and the Plastic Resource Circulation Act of April 2022, which promotes environmentally responsible packaging and reduces single-use plastics. Companies like Toyo Seikan Co. Ltd. are producing heat- and pressure-resistant PET bottles, tailored for coffee, tea, and ready-to-drink beverages, highlighting the market’s focus on high-performance functionality.

Innovation is also driving lightweight, easy-to-handle packaging suitable for vending machines and single-serve consumption. Advanced filling technologies and heat-resistant PET solutions are enabling Japan to maintain a competitive edge while emphasizing sustainability. The focus on specialized, durable, and functional packaging ensures that consumer convenience aligns with environmental goals.

Brazil Hot Drinks Packaging Market Expands Through Sustainable Practices and Strategic Collaborations

Brazil’s hot drinks packaging industry is influenced by amendments to the National Solid Waste Policy, promoting domestic recycling initiatives. The market is experiencing a push toward premium and digital packaging solutions that extend shelf life and preserve product freshness, particularly for coffee, tea, and hot-fill beverages.

Corporate collaborations are strengthening the market, such as SIG Group’s partnership with DPA Brazil in March 2024 to introduce spouted pouch packaging for DPA’s Chamyto yogurt brand. Key applications extend to coffee, tea, and juice, with innovations in flexible and sustainable packaging gaining traction. Brazil’s emphasis on eco-friendly materials and process improvements ensures the market continues to expand in alignment with global sustainability trends.

Hot Drinks Packaging Market Report Scope

Hot Drinks Packaging Market

|

Parameter

|

Details

|

|

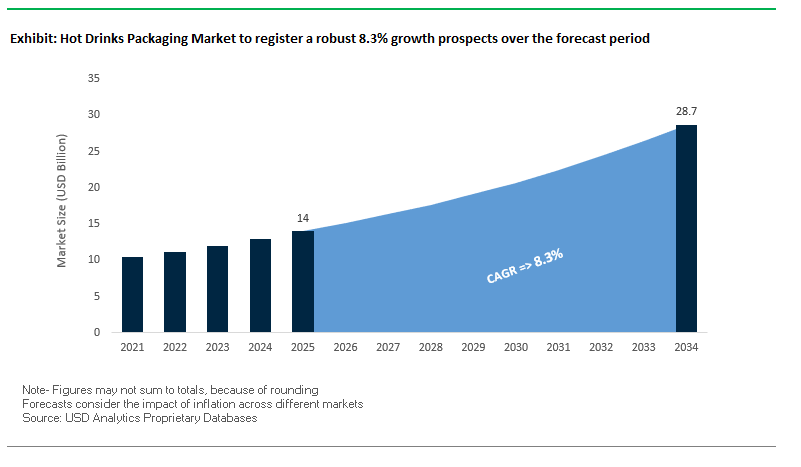

Market Size (2025)

|

$14 Billion

|

|

Market Size (2034)

|

$28.7 Billion

|

|

Market Growth Rate

|

8.3%

|

|

Segments

|

By Material (Paper & Paperboard, Plastic, Glass, Metal), By Packaging Type (Cups & Containers, Pouches & Sachets, Bottles, Cans, Lids & Closures), By Application (Coffee, Tea, Hot Chocolate & Malts, Others), By End-User (Retail, Foodservice, Institutional)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, Mondi Group, Huhtamaki Oyj, DS Smith Plc, Ball Corporation, Graphic Packaging International, LLC, Sonoco Products Company, Smurfit Kappa Group, WestRock Company, Ardagh Group S.A., Crown Holdings, Inc., Tetra Pak, SIG Combibloc Group AG, Novolex Holdings, LLC, Greif, Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Hot Drinks Packaging Market Segmentation

By Material

- Paper & Paperboard

- Plastic

- Glass

- Metal

By Packaging Type

- Cups & Containers

- Pouches & Sachets

- Bottles

- Cans

- Lids & Closures

By Application

- Coffee

- Tea

- Hot Chocolate & Malts

- Others

By End-User

- Retail

- Foodservice

- Institutional

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Hot Drinks Packaging Market

- Amcor plc

- Mondi Group

- Huhtamaki Oyj

- DS Smith Plc

- Ball Corporation

- Graphic Packaging International, LLC

- Sonoco Products Company

- Smurfit Kappa Group

- WestRock Company

- Ardagh Group S.A.

- Crown Holdings, Inc.

- Tetra Pak

- SIG Combibloc Group AG

- Novolex Holdings, LLC

- Greif, Inc.

* List Not Exhaustive

Methodology

The research methodology employed by USDAnalytics for the Hot Drinks Packaging Market integrates a rigorous combination of primary and secondary research to ensure accurate, actionable insights for industry professionals. Primary research involved structured interviews and consultations with packaging engineers, sustainability experts, brand managers, supply chain stakeholders, and regulatory authorities across major regions including North America, Europe, and Asia-Pacific. Secondary research included comprehensive analysis of corporate annual reports, patent filings, sustainability disclosures, regulatory databases, verified industry journals, and trade publications. Advanced data triangulation was applied to validate market sizing, growth rates, and adoption trends, incorporating macroeconomic indicators, raw material costs, technological innovations, and consumer preferences. Market forecasts were generated using both top-down and bottom-up approaches, while regional analysis was contextualized against EPR regulations, circular economy initiatives, and smart packaging trends. This multi-layered methodology ensures that USDAnalytics delivers fact-based, reliable insights aligned with evolving market dynamics, sustainability imperatives, and technological advancements in hot drinks packaging.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.