In-Mold Labelling (IML) Market Overview: Driving Premium Packaging and Circularity

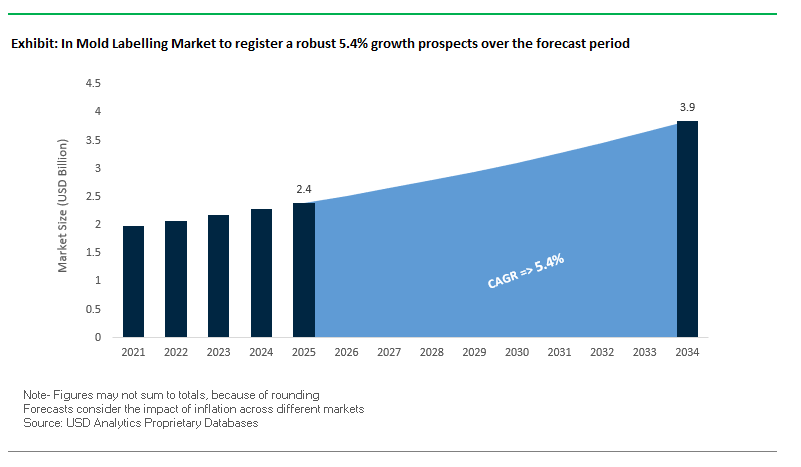

Market Size (MV): $2.4 Billion (2025) → $3.9 Billion (2034) | CAGR (2025–2034): 5.4%

The Global In-Mold Labelling Market is a specialized segment of the packaging industry where pre-printed labels are fused directly into plastic containers during molding. This process delivers seamless aesthetics, durability, and recyclability, making it a critical choice for industries requiring premium graphics, tamper resistance, and sustainability. Unlike post-molding labels, IML ensures abrasion, moisture, and chemical resistance while enabling mono-material designs that simplify recycling.

The sector is strongly influenced by consumer preference for premium packaging, brand demand for recyclability, and the adoption of smart features like RFID/NFC tags. IML’s growth is driven by its ability to deliver edge-to-edge printing, metallic effects, and soft-touch finishes that elevate brand presence in crowded food, personal care, and household goods markets. At the same time, regulatory and retailer pressure for recyclable and mono-material packaging strengthens IML’s role in the circular economy.

Key Insights for Industry Professionals:

- Premium packaging driver: Edge-to-edge graphics, metallic and tactile finishes boost brand differentiation in food & personal care.

- Circular economy enabler: Mono-material IML simplifies recycling and reduces waste.

- Durability edge: IML resists moisture, abrasion, and chemicals, key for food, automotive, and household goods.

- Smart packaging adoption: Embedding RFID/NFC tags enhances traceability, inventory management, and consumer engagement.

- Growth catalysts: Demand from high-value markets (pharmaceuticals, automotive) and rise of digital printing for IML enabling variable data and shorter runs.

Market Analysis: Sustainability, Smart Packaging, and Consolidation Shape IML

The Global In-Mold Labelling Market has been evolving with rapid advancements in sustainability, smart technology, and global mergers. In August 2025, the introduction of Titanium metallic IML film marked a new step toward premium aesthetics, particularly for consumer electronics and luxury goods. Earlier, in May 2025, Avery Dennison launched three RFID-enabled IMLs for reusable plastic packs, supporting item-level scanning and enabling circular economy business models.

Strategic consolidation reshaped the supply base in July 2025, when the Amcor–Berry Global all-stock merger closed, creating a dominant force across rigid and flexible packaging with extended IML capabilities. This followed March 2025 insights highlighting the acceleration of mono-material packaging adoption, aligning with global recycling mandates.

Smart packaging continued to drive innovation. A February 2025 report highlighted that demand for QR, NFC, and RFID features within IML formats is climbing, giving brands real-time tracking and consumers instant engagement tools. Digital transformation also expanded with the October 2024 surge in advanced digital printing for IML, supporting shorter runs and mass customization. At the same time, sustainability pressure intensified, with Unilever doubling its R&D spend in December 2024 to scale recyclable and compostable packaging, signaling brand-side commitment to next-gen labeling solutions.

The industry’s eco-innovation narrative extended beyond plastics: Sealed Air introduced a curbside-recyclable paper cushioning solution in August 2024, illustrating the competitive context in which IML suppliers operate. Likewise, reports in 2024 highlighted demand for bio-based adhesives and recyclable films, reinforcing the industry’s pivot toward low-impact materials.

Transformative Trends and Strategic Opportunities in In-Mold Labelling Market

Accelerated Adoption in Dairy and Food Service Packaging for Recyclability

The in-mold labelling (IML) market is experiencing rapid adoption in the dairy and food service sectors as brands strive for fully recyclable, mono-material packaging. Major players are embracing PP-on-PP IML solutions to ensure compatibility with existing recycling streams while maintaining structural integrity. Nestlé’s development of a 10% lighter IML-decorated polypropylene pot demonstrates the effectiveness of this approach, providing both durability in sub-zero conditions and compliance with circular economy initiatives.

This trend is further propelled by global regulatory frameworks, including the European Packaging and Packaging Waste Regulation (PPWR), which mandate the use of mono-material packaging to streamline recyclability. IML enables containers such as yogurt cups, ice cream tubs, and spreadable food containers to maintain label integrity throughout the cold chain, enhancing brand visibility and regulatory compliance. By aligning with sustainability objectives, IML is positioning itself as a critical enabler for eco-friendly packaging in food service.

Integration of Functional and Smart Features into the Label Substrate

IML is evolving beyond aesthetics into functional and smart packaging solutions. The technology now allows embedding active components directly into the label, such as antimicrobial agents (e.g., cinnamaldehyde in PLA films) to extend shelf life and inhibit microbial growth including E. coli and Listeria.

Moreover, brands are leveraging IML to incorporate high-resolution QR codes, conductive inks, and traceability features, enabling real-time product tracking, digital engagement campaigns, and supply chain transparency. These embedded functionalities are protected from abrasion, moisture, and chemical exposure due to the molding process, making IML a robust platform for smart packaging applications. This creates a high-value growth avenue for brands seeking to combine consumer engagement, product safety, and regulatory compliance.

Expansion into Thermoformed IML for Premium Food Trays

While injection IML is well-established, thermoformed IML (IML-T) offers significant growth potential for thin-gauge, high-speed production of premium food trays. This technology allows the creation of durable, full-wrap, high-resolution graphics for ready meals, fresh produce, and baked goods, effectively replacing glued-on labels and premiumizing the packaging format.

Innovative solutions, such as thermoformed IML cardboard hybrids, pioneered by companies like ILLIG, combine the durability of a plastic liner with the premium perception of cardboard. This approach not only enhances mechanical stability and sidewall rigidity but also allows material reduction, creating sustainable, lightweight packaging solutions for meat trays, deli items, and other high-value food products.

Development of Bio-Based and Compostable IML Films

The rise of bioplastic containers presents an emerging opportunity for bio-based and compostable IML films. Academic and industrial research is focused on creating films from cellulose, starch, and polysaccharides that maintain mechanical strength, heat resistance, and print quality while being certified for industrial composting.

Competitive Landscape: Leading Innovators in Global In-Mold Labelling

The In-Mold Labelling Industry is defined by a blend of film producers, label converters, and injection molding specialists who are scaling innovation, automation, and sustainable practices to meet global demand.

CCL Industries strengthens its global IML portfolio

CCL Industries leads the specialty labeling sector with global reach and advanced digital printing for IML. Its acquisition of Faubel & Co. Nachfolger GmbH (2023) strengthened pharmaceutical trial labeling, enhancing its healthcare presence. CCL’s IML portfolio spans food, personal care, and industrial packaging, offering high-definition graphics and RFID integration. Its strategy focuses on acquisitions and mono-material recyclability innovations to support circularity and high-value applications.

Multi-Color Corporation (MCC) expands with acquisitions in Europe and Türkiye

MCC is a global leader in premium label solutions, recognized for its aesthetic “no-label look” that enhances brand impact. In 2023, MCC acquired Stephanos Karydakis IML SA (Greece) and Korsini (Türkiye), boosting its European and EMEA footprint. MCC serves food, home care, and personal care markets with high-graphic IMLs, leveraging its creative design and supply chain scale. Its strategy centers on acquisitions and sustainable innovation to consolidate global leadership.

Jindal Films launches Enviro-IML films for circularity

Jindal Films dominates in BOPP film supply and showcased its Enviro-IML range (2024) thinner, lower-impact films supporting recyclability without performance trade-offs. Jindal’s films (opaque, clear, white voided) offer superior adhesion and printability. Its collaborations with global brands underline its role in circular packaging ecosystems, while its strategic focus remains on developing recyclable film solutions for mass adoption.

Taghleef Industries collaborates with SABIC on single-step IML

Taghleef Industries (Ti) operates a diverse BOPP portfolio and launched a single-step IML solution with SABIC (2023) to simplify part decoration. Its Derprosa™ films are used in food, yogurt cups, and rigid containers, delivering premium graphics with durability. The Dynamic Cycle initiative drives recyclable and reusable product development. Ti’s strategy emphasizes sustainability partnerships and customer-centric solutions aligned with global recycling targets.

EVCO Plastics integrates molding expertise with IML solutions

EVCO Plastics differentiates with its injection molding and IML integration expertise, offering end-to-end solutions from mold design to production. It supplies automotive, medical, and consumer durables with precision IML, leveraging automation and robotics for defect reduction and efficiency. EVCO’s strategy is to serve as a one-stop solution provider, combining engineering depth with decorative functionality for complex molded components.

In Mold Labelling Market Share Insights

Injection Molding Dominates Market Share by Molding Process in In-Mold Labelling

Injection molding accounts for 65% of the in-mold labelling (IML) market share in 2025, making it the undisputed leader across molding processes. Its dominance stems from its ability to deliver high-volume, thin-wall rigid plastic containers with seamless label integration, a core requirement in the food and beverage sector. Injection molding enables the placement of labels inside the mold before plastic is injected, producing containers with a permanent, no-label look that withstands moisture, abrasion, and handling stress. Dairy tubs, yogurt lids, and ready-meal containers are prime examples of its large-scale application. Thermoforming follows as a growth segment, particularly in lightweight, cost-sensitive food packaging formats such as margarine tubs and disposable cups, where branding is equally critical. Blow molding remains a niche, used mainly for bottles and hollow containers in high-value categories, but its slower cycle times and complexity have limited its broader uptake. The continued dominance of injection molding highlights its alignment with high-speed manufacturing, brand differentiation needs, and stringent food-contact requirements, making it the central force behind IML adoption.

Food and Beverages Sector Leads Market Share by Application in In-Mold Labelling

The food and beverages industry captures 70% of the in-mold labelling market in 2025, reflecting the technology’s near-perfect alignment with consumer packaging demands in this sector. IML is particularly valuable in dairy, beverages, and frozen food packaging, where labels must withstand refrigeration, condensation, and frequent handling without peeling or fading. Its durability and ability to deliver vivid graphics enhance branding and regulatory compliance simultaneously, cementing its role in high-volume food packaging. Household and personal care packaging is another important contributor, where IML ensures long-lasting labels on detergents, cleaning products, and cosmetics despite exposure to harsh chemicals. In healthcare, IML secures permanent labeling for pill containers and diagnostic equipment, where sterilization resistance and barcode readability are mandatory. Automotive and consumer electronics remain niche but high-value markets, leveraging IML for decorative and functional integration into parts and housings. Overall, food and beverages dominate volume demand, while healthcare and industrial segments sustain value-driven applications.

United States In-Mold Labeling Market Accelerates Through Mono-Material Solutions and Automation

The U.S. in-mold labeling (IML) market is being shaped by state-level Extended Producer Responsibility (EPR) regulations, which encourage brands to adopt mono-material packaging where both the label and container are made from the same resin, such as polypropylene. This regulatory push is driving recyclability-focused growth in IML applications across food and beverage, household goods, and personal care sectors. Technological advancements, including improved films and substrates for higher print quality, as well as robotics and automation, are enabling precise, high-speed label integration during molding.

Corporate investments are also propelling market expansion. Companies are strategically acquiring specialized technology firms and establishing new production facilities to meet the growing demand for sustainable, high-performance IML solutions. Key applications, including yogurt tubs, ice cream containers, and detergent bottles, leverage IML’s durability, moisture resistance, and superior aesthetics. The shift toward mono-material solutions simplifies recycling, reduces material waste, and aligns with the increasing sustainability goals of both consumers and brand owners.

Germany In-Mold Labeling Market Leads Through Regulatory Compliance and Sustainable Innovation

Germany’s IML market operates under a stringent regulatory framework, particularly the EU Packaging and Packaging Waste Regulation (PPWR) effective February 2025. This mandates fully recyclable or reusable packaging by 2030, driving adoption of in-mold labeling technologies that support circular economy objectives. The German Packaging Act (VerpackG) incentivizes recyclable packaging design through modulated fees, favoring IML over traditional labeling methods that complicate recycling.

Technological innovation is at the forefront, with companies developing ultra-thin, lightweight IML films that minimize material use while maintaining durability and print quality. The market is particularly strong in food, beverage, and medical applications, supported by Germany’s robust manufacturing base and strong sustainability focus. Strategic corporate collaborations, such as SÜDPACK’s partnership with SN Maschinenbau to develop innovative stand-up pouches, highlight the country’s emphasis on combining technological advancement with environmental responsibility.

China In-Mold Labeling Market Expands with Circular Economy Initiatives and Automation

China’s IML industry is strongly influenced by governmental initiatives, including the “dual carbon” goal and the March 2024 Action Plan for Large-Scale Equipment Updates and Consumer Goods Replacement, which promote recycling and sustainable materials adoption. Regulatory reforms, including the GB/T 31268 standard effective November 2024, limit excessive packaging, directly impacting e-commerce products that rely heavily on in-mold labeling.

Technological advancements, including AI, automation, and “5G plus industrial internet,” are enhancing production efficiency and flexibility. Corporate investments, exemplified by Dow’s collaboration with Mengniu to introduce a mono-material PE yogurt pouch in August 2023, focus on high recyclability and circular economy alignment. The market is also seeing a push for domestic manufacturing of IML technologies, reducing reliance on imported solutions and meeting rising demand for sustainable packaging in China.

Brazil In-Mold Labeling Market Grows Through Strategic Investments and Eco-Friendly Packaging

Brazil’s IML market is driven by government initiatives, including amendments to the National Solid Waste Policy that encourage domestic recycling programs. The packaging industry is undergoing a technological transformation, with innovations in flexible packaging and IML solutions that extend shelf life and maintain product quality, particularly in food, beverage, and personal care sectors.

Corporate expansion plays a key role, highlighted by MCC’s IML production plant in Louveira, set to open in early 2025. This strategic move demonstrates confidence in the Brazilian market while strengthening regional customer relationships. The demand for sustainable, high-quality IML solutions aligns with global trends toward eco-friendly materials and packaging innovations, supporting Brazil’s growing focus on circular economy principles.

Japan In-Mold Labeling Market Leverages Advanced Materials and Precision Manufacturing

Japan’s IML industry is supported by precision manufacturing expertise and the Plastic Resource Circulation Act, effective April 2022, which promotes environmentally responsible packaging. Companies are producing recycled BOPP films and specialty IML products for high-value applications, including electronics and delicate instruments. This positions Japan as a leader in sustainable and functional in-mold labeling.

Innovation in functionality, such as self-folding IML that reduces storage space and simplifies packaging, is gaining traction. Firms like ZACROS are pioneering specialized flexible packaging using IML, while major players focus on high-performance aesthetic solutions. Japan’s strong technological ecosystem ensures that IML applications meet both consumer demands and environmental regulations efficiently.

France In-Mold Labeling Market Advances Through Circular Economy Policies and Premium Packaging

France’s IML market is shaped by strict EU regulations and the Anti-Waste Law for a Circular Economy (AGEC), which emphasizes reducing plastic packaging and enhancing recyclability. Manufacturers are investing in advanced machinery and automation, enabling the production of complex shapes while maintaining high efficiency and premium graphics quality.

The market sees significant demand in cosmetics, food, and high-end consumer goods, where IML delivers a “no-label look” that enhances brand perception. Corporate expansions focus on lightweighting and developing IML solutions that reduce carbon footprint. Innovations in mono-material IML are simplifying recyclability, aligning with France’s circular economy objectives and supporting the growing preference for sustainable, high-performance packaging solutions.

In Mold Labelling Market Report Scope

In Mold Labelling Market

|

arameter

|

Details

|

|

Market Size (2025)

|

$2.4 Billion

|

|

Market Size (2034)

|

$3.9 Billion

|

|

Market Growth Rate

|

5.4%

|

|

Segments

|

By Material (PP, PE, PS, PET, Others), By Printing Technology (Flexography, Offset Printing, Gravure, Digital Printing), By Molding Process (Injection Molding, Blow Molding, Thermoforming), By Application (Food & Beverages, Household & Personal Care, Automotive, Consumer Electronics, Healthcare)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, CCL Industries Inc., Constantia Flexibles Group GmbH, Avery Dennison Corporation, Fuji Seal International, Inc., Huhtamaki Oyj, SÜDPACK Verpackungen GmbH & Co. KG, Mondi Group, MCC Label (Multi-Color Corporation), Taktik Print, Inland, WS Packaging Group, Inc., Korsini-Saf S.r.l., Smyth Companies, LLC, Innovia Films

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

In Mold Labelling Market Segmentation

By Material

By Printing Technology

- Flexography

- Offset Printing

- Gravure

- Digital Printing

By Molding Process

- Injection Molding

- Blow Molding

- Thermoforming

By Application

- Food & Beverages

- Household & Personal Care

- Automotive

- Consumer Electronics

- Healthcare

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in In Mold Labelling Market

- Amcor plc

- CCL Industries Inc.

- Constantia Flexibles Group GmbH

- Avery Dennison Corporation

- Fuji Seal International, Inc.

- Huhtamaki Oyj

- SÜDPACK Verpackungen GmbH & Co. KG

- Mondi Group

- MCC Label (Multi-Color Corporation)

- Taktik Print

- Inland

- WS Packaging Group, Inc.

- Korsini-Saf S.r.l.

- Smyth Companies, LLC

- Innovia Films

* List Not Exhaustive

Methodology

USDAnalytics has developed the In-Mold Labelling (IML) Market research through a comprehensive methodology combining primary and secondary research, ensuring actionable insights for industry professionals. Primary research involved in-depth interviews with packaging engineers, brand managers, supply chain executives, and sustainability experts across key regions including North America, Europe, and Asia-Pacific. Secondary research leveraged company annual reports, patent filings, regulatory documents, industry journals, and verified market publications. Market sizing, CAGR, and trend analyses were validated using data triangulation across macroeconomic indicators, raw material prices, technological innovations, and consumer preferences. Both top-down and bottom-up approaches were applied to forecast regional and global growth, while segment analysis covered molding processes, printing technologies, materials, and application sectors. Additionally, regulatory frameworks, circular economy initiatives, and smart packaging adoption were integrated into the assessment. This structured approach ensures USDAnalytics delivers precise, evidence-based insights for decision-makers seeking sustainable, high-performance, and premium IML solutions.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.