Ink Solvent Market to Reach $2,236.4 Million by 2034 at 4.9% CAGR as NC-Free, Low-VOC, and Semiconductor-Grade Solvents Redefine Supply Chains

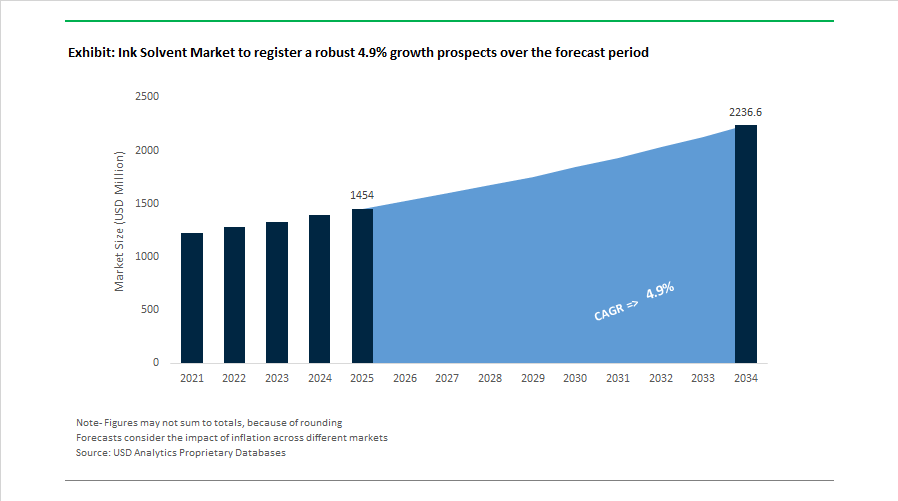

The Ink Solvent Market is projected to grow from $1,454 Million in 2025 to $2,236.4 Million by 2034, registering a CAGR of 4.9%. Growth is being driven by expanding flexible packaging demand, regulatory compliance requirements in Europe, rising semiconductor solvent consumption, and production realignment toward Asia. Between 2024 and 2026, manufacturers accelerated investments in nitrocellulose (NC)-free systems, low-VOC solvent chemistries, food-contact compliant formulations, and high-purity electronic-grade solvent platforms. The market is increasingly defined by sustainability certifications such as RecyClass and compliance with the German Ink Ordinance, while also adapting to supply volatility in traditional nitrocellulose and aromatic solvent streams.

In April 2024, Toyo Ink India, part of the Artience Group, announced a large-scale expansion at its Gujarat facility to increase solvent-based adhesives and functional materials capacity by 3.5 times, with full commercial operations targeted for April 2026. In November 2024, Flint Group opened a 9,000-square-meter manufacturing plant in Savli, Gujarat, complementing its Lamdapura solvent-based site and establishing a major localized production cluster for the South Asian market. In 2024, Nazdar expanded its digital printing portfolio with the 2131 Series solvent inkjet inks featuring low-odor formulations designed for enclosed industrial printing environments. During the same year, Fujifilm launched its VISION2030 plan, committing over ¥170 billion through fiscal 2026 toward electronics and semiconductor materials, including high-purity solvent-based photoresists and advanced cleaning chemistries required for next-generation chip fabrication.

Product innovation intensified through 2025. In January 2025, Sun Chemical introduced an expanded Nitrocellulose-alternative portfolio under the SunSpectro and SunStrato series. These NC-free solvent-based inks address both supply chain volatility and recycling-related thermal instability, aligning with RecyClass and CEFLEX flexible packaging guidelines. In May 2025, INX International completed the acquisition of Servicom New Zealand and Galaxy Inks Australia, strengthening localized solvent-based ink production and technical service for the Oceania wine and export packaging sectors. In August 2025, DIC Corporation inaugurated a new sustainable production facility in Indonesia dedicated to solvent-based materials for direct food-contact packaging, enhancing regional supply security across Southeast Asia. In November 2025 at CHINACOAT, Sun Chemical and DIC showcased low-VOC and mass-balance solvent systems designed to reduce carbon intensity without compromising drying speed or adhesion performance.

Regulatory compliance and recycling compatibility have become defining competitive parameters heading into 2026. In December 2025, Flint Group confirmed that its entire European ONECode solvent-based flexographic and rotogravure ink portfolio is fully compliant with the German Ink Ordinance, following the extension of the regulatory transition deadline to December 31, 2026. In February 2026, Siegwerk became the first company to receive RecyClass technology approval for its SICURA series, including UV-solvent hybrid systems verified as compatible with the colored PE flexible recycling stream in Europe. Concurrently, Toyo Ink India positioned its expanded Gujarat site as a primary export hub for the Middle East and Africa in 2026, reflecting a broader geographic shift of solvent-based ink production toward regions with scalable capacity and adaptable regulatory environments.

Ink Solvent Market Trends and Opportunities

Mandatory Phase-Out of High-VOC Solvents in Flexo and Gravure Packaging

The ink solvent market is undergoing a structural and non-reversible transformation as regulators across China, the European Union, and the United States enforce stricter limits on volatile organic compound emissions and food-contact safety. In September 2025, China’s National Health Commission finalized GB 4806.10-2025, expanding the list of permitted raw materials for food-contact inks and coatings from 105 to 346 substances while imposing tighter migration limits on primary aromatic amines. This regulatory expansion is not liberalization; it is a quality filter that removes high-risk aromatics and forces reformulation toward cleaner solvent chemistries.

China’s long-running “Blue Sky” policy has further accelerated this transition. Under national GB standards implemented between 2020 and 2025, inks and coatings exceeding a VOC threshold of 420 g/L are subject to a 4% consumption tax. This fiscal penalty has directly reshaped procurement behavior, pushing converters toward waterborne systems and high-solids solvent blends that minimize taxable emissions while preserving print quality and drying speed.

In Europe, the Packaging and Packaging Waste Regulation (EU) 2025/40, effective February 11, 2025, has added a circularity lens to solvent selection. All packaging placed on the EU market must be recyclable at scale by 2030, compelling ink formulators to simplify solvent packages so that residual solvents do not disrupt mechanical recycling of mono-material PE and PP films. This has reduced tolerance for complex aromatic blends and reinforced demand for low-boiling, low-residue alternatives.

The United States is reinforcing the same direction. In January 2025, the U.S. EPA finalized amendments to the National VOC Emission Standards for Aerosol Coatings, introducing updated reactivity limits that structurally favor “exempt” solvents such as acetone and PCBTF. Together, these regional policies are collapsing the addressable market for high-VOC solvents in flexo and gravure packaging and redirecting demand toward compliant, globally harmonized solvent systems.

Strategic Demand for High-Purity Solvents in Industrial Inkjet Printing

The rapid expansion of industrial inkjet printing on non-porous substrates has elevated solvent purity from a formulation detail to a strategic performance requirement. High-speed drop-on-demand inkjet systems used in pharmaceutical coding, food packaging, and electronics marking are highly sensitive to nozzle clogging, known in the industry as “decapping.” Preventing decapping has become a key determinant of uptime and yield in automated production lines.

By late 2025, demand for P-series glycol ethers such as propylene glycol methyl ether surged as ink manufacturers moved away from more toxic E-series alternatives. These solvents offer an optimal balance of evaporation rate, surface tension reduction, and operator safety, making them the preferred carriers for high-speed inkjet systems operating continuously in regulated environments.

Purity requirements are also rising sharply. In August 2024, Eastman expanded its Eastapure portfolio with a new electronic-grade isopropyl alcohol designed to meet semiconductor-grade purity thresholds. While originally developed for electronics cleaning, this ultra-pure IPA is increasingly being specified in industrial inkjet inks to protect printhead reliability in fully automated lines.

Formulation strategies have also evolved. High-boiling co-solvents are now deliberately incorporated to keep ink fluid at the nozzle tip for up to 60 minutes of idle time, representing a threefold improvement over legacy solvent systems. This directly reduces maintenance interventions, a key operational metric for decision makers managing high-throughput digital print fleets.

Bio-Based and Renewable Solvents for Decarbonized Packaging

Corporate decarbonization commitments are translating into concrete procurement mandates across the packaging value chain. Consumer packaged goods leaders are now explicitly specifying bio-derived solvents as part of Scope 3 emissions reduction strategies, creating a fast-growing opportunity for bio-ethanol, bio-acetone, and lactate ester solvents derived from fermentation routes.

In 2025, Flint Group formalized this shift through its PRISM sustainability strategy, targeting a 46% reduction in Scope 1, 2, and 3 emissions by 2030. A core execution lever is the replacement of fossil-derived solvents with vegetable-oil-based and petrol-free solvent technologies across packaging inks. This type of brand-driven mandate is reshaping supplier qualification criteria across the ink solvent market.

Innovation is accelerating. In October 2025, GFBiochemicals launched RE:CHEMISTRY NEW320, a plant-based solvent derived from second-generation biomass using levulinate-ketal chemistry. While initially positioned for cosmetics, the technology is being rapidly adapted for ink formulations as a drop-in replacement for petroleum-based acetates and silicones, offering comparable evaporation profiles with a materially lower carbon footprint.

Economic barriers are also falling. By 2025, bio-based ethanol and isopropanol had reached price parity with synthetic equivalents in several regional markets, supported by government incentives and a projected 8.8% CAGR for the broader bio-solvent sector through 2029. This combination of regulatory pressure, brand mandates, and improving cost competitiveness positions bio-based solvents as a structural growth engine rather than a niche premium segment.

Specialized Solvent Systems for Functional and Printed Electronics

The convergence of smart packaging, RFID, NFC, and flexible electronics is creating a high-margin niche for specialized ink solvents capable of supporting conductive and functional inks. These applications demand solvent carriers that maintain precise viscosity and surface tension while enabling uniform deposition of metal particles without agglomeration.

In 2025, inkjet printing accounted for nearly 29% of the manufacturing technologies used in printed electronics, driven by its ability to deliver mask-less, variable-data printing of conductive tracks. This has intensified demand for solvents that support stable dispersion and controlled evaporation during deposition.

Cost pressure is reshaping material choices. While silver nanoparticles still represent the largest share of conductive inks at 32.7%, manufacturers are increasingly shifting toward copper-based systems to reduce material costs. Copper’s susceptibility to oxidation has created a critical requirement for solvent systems that provide reducing environments or protective barriers during printing and curing.

Miniaturization trends further amplify this opportunity. As electronics become smaller and more portable, additive manufacturing and high-precision 3D printing of circuits require solvents that prevent nozzle clogging while ensuring consistent particle distribution. For decision makers, solvent performance in these applications directly links to yield stability, equipment uptime, and the economic viability of next-generation printed electronics production.

Ink Solvent Market Share and Segmentation Insights

Oxygenated Solvents Lead Ink Solvent Formulations Due to Superior Solvency and Regulatory Compatibility

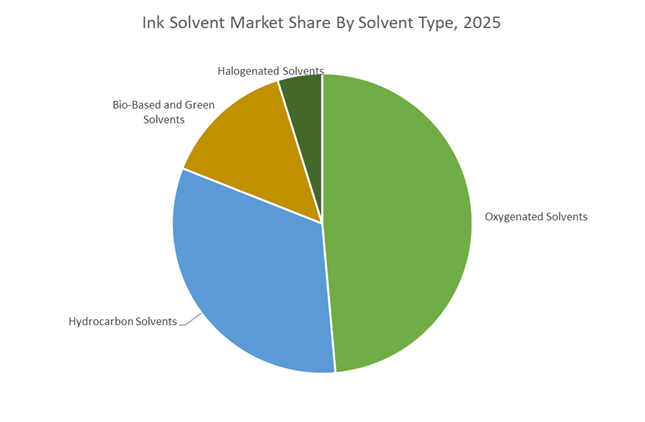

Oxygenated solvents accounted for 48.60% of the Ink Solvent Market share in 2025, establishing them as the most widely used solvent category in printing ink formulations. This solvent group includes alcohols, ketones, esters, and glycol ethers, which provide excellent solvency for common ink resins such as acrylics, polyamides, and polyurethane resins used in flexographic, gravure, and digital printing inks. Oxygenated solvents are preferred because they deliver balanced evaporation rates, strong resin compatibility, and efficient pigment wetting, all of which are critical for maintaining print clarity, color density, and drying performance in high-speed printing operations. Compared with hydrocarbon and halogenated solvents, oxygenated solvents typically offer lower toxicity profiles and improved environmental compliance, supporting their adoption across packaging, publication, and industrial printing segments. In 2025, solvent manufacturers are expanding portfolios of regulatory-compliant oxygenated solvents, including exempt solvent options such as acetone and specialized ester blends that enable ink formulators to meet global VOC regulations while maintaining the solvency and drying characteristics required for advanced printing technologies.

Packaging Sector Drives the Largest Consumption of Ink Solvents Across Global Printing Industries

Packaging represented 52.80% of the Ink Solvent Market share in 2025, making it the largest end-use sector for printing solvents. Packaging printing applications require large volumes of solvents to support ink dissolution, viscosity control, pigment dispersion, and drying performance across flexible films, pressure-sensitive labels, folding cartons, and corrugated packaging substrates. Solvents are critical components in both solvent-based inks and water-based ink systems, where they facilitate resin solubility, film coalescence, and rapid evaporation during high-speed printing processes such as flexography and gravure printing. The rapid expansion of flexible packaging, e-commerce logistics packaging, and consumer goods labeling continues to drive solvent demand globally. In 2025, regulatory oversight surrounding food-contact packaging inks has significantly influenced solvent selection, particularly in applications involving food, beverages, and pharmaceutical packaging. Ink formulators increasingly prioritize low-migration and high-purity solvent systems designed to minimize residual solvent contamination while maintaining print performance, enabling compliance with stringent global food safety and packaging regulations.

Competitive Landscape in Ink Solvent Market

BASF SE Expands Asian Solvent Capacity and Drives Green Transformation

BASF SE maintains leadership in oxygenated solvents and ink-related resins through its integrated Verbund infrastructure, enabling feedstock efficiency and energy optimization. In February 2026, the company reported 2025 EBITDA of €6.6 billion and projected a 2026 range between €6.2 billion and €7.0 billion under its Winning Ways strategy. The startup of major production plants at the Zhanjiang Verbund site in China during late 2025 and early 2026 establishes a strategic solvent and dispersion hub serving the rapidly expanding Asian packaging and industrial ink markets. BASF’s Green Transformation agenda prioritizes renewable electricity adoption and energy efficiency upgrades across solvent manufacturing facilities. The company expects annual cost savings of €2.3 billion by the end of 2026 while sustaining capital expenditure of €3.4 billion, reinforcing operational resilience in oxygenated ink solvent production.

Dow Inc. Accelerates Productivity and Oxygenated Solvent Optimization

Dow Inc. is executing its Transform to Outperform roadmap to deliver at least $2 billion in near-term operating EBITDA improvement through automation, AI integration, and structural simplification. With manufacturing operations across 29 countries and 2025 sales of approximately $40 billion, Dow maintains a strong position in oxygenated solvents and polyolefin dispersions used in metal packaging and high-performance industrial ink systems. The company has targeted a $500 million in-year EBITDA uplift for 2026 by resetting cost structures within its Performance Materials and Coatings segment. Modernized customer service platforms and streamlined processes are enhancing supply reliability for solvent-based and hybrid ink formulations. Dow’s focus on operational productivity supports margin stability in solvent markets exposed to feedstock volatility and cyclical demand in commercial printing.

Shell Chemicals Maintains Cost Leadership in Hydrocarbon Ink Solvents

Shell Chemicals leverages vertical integration across upstream oil and gas operations to sustain cost leadership in hydrocarbon and oxygenated ink solvents. Through its 2026 Energy Security Scenarios framework, Shell outlines strategies for chemical sector competitiveness amid AI-driven industrial shifts and energy transition pressures. In early 2026, the company targeted refinery utilization rates between 93 and 97% and chemical utilization between 75 and 79%, aiming to strengthen margins following a softer fourth quarter in 2025. Shell’s integrated supply chain provides global ink blenders with stable access to aromatic and aliphatic hydrocarbon solvents. Concurrently, the company is expanding lower-carbon chemical intermediates to align solvent production with its 2050 net-zero emissions commitment, supporting brand owners seeking lower lifecycle emissions in packaging inks.

ExxonMobil Product Solutions Advances High-Purity Hydrocarbon Fluids

ExxonMobil Product Solutions remains a major supplier of ultra-high-purity hydrocarbon fluids under the Exxsol and Isopar brands, widely used in specialty ink and coating formulations requiring controlled evaporation rates and low odor. Management has linked AI-driven process optimization and its Discovery 6 supercomputing platform to over $1 billion in incremental production value across refining and chemical assets. Investments across the U.S. Gulf Coast, Singapore, and China support long-term solvent output growth, while a 2030 target to double Permian Basin production to 2.5 million barrels of oil equivalent per day enhances feedstock security. ExxonMobil expects to achieve its 2030 greenhouse gas emissions intensity objectives ahead of schedule in 2026. The company plans to maintain share repurchases of $20 billion through 2026 and delivers a return on capital employed exceeding 17%, underscoring financial strength in solvent operations.

Celanese Corporation Strengthens Acetyl Chain Integration and Customer Co-Development

Celanese Corporation plays a central role in the acetyl chain, producing acetic acid and vinyl acetate monomer that underpin many ink solvent and resin systems. In February 2026, the company announced price increases of up to $100 per metric ton for acetic acid, VAM, and derivatives in the Western Hemisphere to offset rising feedstock and energy costs. The opening of its expanded Michigan Technology Center provides over 10,000 square feet of additional capacity for customer co-development, accelerating speed-to-market for engineered materials and solvent applications. Following the $500 million divestiture of its Micromax business, Celanese is prioritizing deleveraging and disciplined capital management. With 2024 net sales of $10.3 billion and a workforce exceeding 11,000 employees, the company maintains a strong industrial footprint across packaging, adhesives, and solvent-based formulations.

Clariant Enhances Margin Discipline and Digital Chemical Management

Clariant has strengthened profitability in the ink solvent and specialty chemicals landscape through portfolio optimization and operational efficiency programs. In February 2026, the company reported a 2025 EBITDA margin of 17.8% before exceptional items, an increase of 180 basis points year over year. For 2026, Clariant targets an EBITDA margin around 18% and a free cash flow conversion of approximately 40% despite macroeconomic headwinds. Its performance improvement program delivered CHF 50 million in savings during 2025, with the remaining CHF 80 million target largely expected in 2026. The rollout of CLARITY, a digital service platform with over 800 users across 38 countries, supports optimized catalyst and chemical management, enhancing transparency and supply chain efficiency in solvent-intensive industrial operations.

China Ink Solvent Market: Regulatory Acceleration and High-Purity Localization

China’s ink solvent industry is undergoing a rapid structural upgrade driven by mandatory national standards, food safety regulation, and petrochemical localization. From June 1, 2026, the State Administration for Market Regulation will enforce GB 30981.1-2025 and GB 30981.2-2025, sharply restricting hazardous substances and VOC content in architectural and industrial inks. This regulatory reset is forcing a market-wide transition toward low-VOC, water-borne, and high-solid solvent systems, particularly across packaging, publication printing, and decorative coatings. In parallel, GB 4806.14 food contact material regulation, fully active during 2025–2026, has eliminated toluene-based systems from food packaging inks, accelerating adoption of ethyl acetate and ethanol solvents among converters supplying FMCG and export-oriented packaging.

Industrial policy is reinforcing this shift. Under the Ministry of Industry and Information Technology petrochemical growth blueprint released in late 2025, China is targeting sustained value-added growth by upgrading traditional solvent products into electronic-grade and food-contact-compliant ink solvents. Capacity investments are aligned accordingly. BASF is advancing the next phase of its Zhanjiang Verbund site in 2026, scaling production of methyl glycols and glycol ethers critical for high-performance inkjet inks and downstream industrial fluids. Regional governments are adding financial incentives through VOC remediation programs in the Yangtze River Delta, subsidizing transitions from solvent-heavy inks to water-based and UV-curable alternatives. Meanwhile, export controls introduced in April 2025 on rare-earth elements used in specialty security inks have forced reformulation strategies, increasing reliance on domestically optimized solvent–stabilizer systems within China’s specialized chemical parks.

United States Ink Solvent Market: Federal Phase-Outs, Bio-Based Adoption, and Semiconductor Alignment

The United States ink solvent industry is being reshaped by federal chemical controls, sustainability mandates, and strategic reshoring of ultra-high-purity solvents. Under TSCA Section 6(g), the U.S. Environmental Protection Agency finalized February 17, 2026 as the effective date for Trichloroethylene exemption requirements, compelling industrial ink stripping and cleaning applications to transition away from TCE toward validated alternatives such as n-propyl bromide and advanced aqueous systems. This regulatory action is cascading into printing and ink manufacturing supply chains that historically relied on chlorinated solvents.

Investment and innovation are accelerating in response. Sun Chemical, part of the DIC Group, completed a $100 million investment in late 2025 to expand sustainable, solvent-reduced ink production for North American flexible packaging. Bio-based solvent adoption is also gaining traction as Vertec Biosolvents and Eastman expanded 2026 portfolios with corn- and soy-derived ethyl lactate and methyl soyate to meet green chemistry mandates in California and the Northeast. State-level PFAS bans in food packaging during 2025–2026 are further accelerating demand for PFAS-free solvent-based barrier systems that deliver oil and grease resistance without fluorinated chemistries. In parallel, CHIPS and Science Act initiatives are supporting the reshoring of ultra-high-purity solvents such as PGMEA, ensuring domestic supply for semiconductor-grade inks and photoresists through 2026.

Germany Ink Solvent Market: Mass-Balanced Decarbonization and REACH-Driven Substitution

Germany’s ink solvent market is defined by decarbonization leadership and early compliance with forthcoming EU chemical restrictions. In 2025, Evonik Coating Additives launched its first mass-balanced “eCO” solvent series using ISCC PLUS certified feedstocks, enabling ink formulators to reduce product carbon footprints without altering established production processes. This approach is gaining traction among European converters seeking Scope 3 emission reductions while maintaining consistent print performance.

Regulatory pressure is intensifying ahead of December 2026. Under Regulation (EU) 2025/1090, the REACH Annex XVII update will restrict solvents such as DMAC and NEP, permitting their use only if strict Derived No-Effect Levels for worker exposure are met. This is driving accelerated substitution toward safer oxygenated solvents across Germany’s printing and industrial ink ecosystem. Sustainability benchmarks are being reset at the producer level. ALTANA Group, including its BYK operations, confirmed achievement of Scope 1 and 2 CO2 neutrality at its Wesel production sites by the end of 2025, positioning Germany as a reference market for low-carbon solvent manufacturing in Europe.

India Ink Solvent Market: Carbon Market Readiness and Food-Safe Reformulation

India’s ink solvent industry is entering a compliance-led transformation phase shaped by carbon regulation, food safety standards, and capacity expansion for high-performance markets. The launch of the Indian Carbon Market and Carbon Credit Trading Scheme by mid-2026 will legally bind more than 740 industrial entities, including major petrochemical and ink solvent producers, to emission intensity targets. This policy is already influencing solvent selection, with manufacturers favoring lower-carbon alcohols and esters to improve lifecycle emissions profiles.

Capacity investments are aligning with this regulatory trajectory. Lubrizol is commissioning its 120-acre Aurangabad facility for operational testing in the first quarter of 2026, producing advanced solvents and additives for high-performance ink markets across APAC and the Middle East. On the demand side, enforcement of IS:15495 by the Bureau of Indian Standards has effectively banned toluene and phthalates in food packaging inks, triggering a sustained shift toward alcohol- and ester-based solvent systems. This regulatory harmonization is positioning India as a compliant manufacturing base for export-oriented packaging and publication inks.

Ink Solvent Industry: Country-Level Strategic Summary

Ink Solvent Market County Level Snapshot

|

Region

|

Primary Regulatory or Policy Driver

|

Core Solvent Transition

|

Structural Impact

|

|

China

|

GB 30981 standards and FCM rules

|

Toluene-free, water-based, high-solid systems

|

Policy-led upgrading and domestic purity scale

|

|

United States

|

TSCA TCE phase-out and PFAS bans

|

Bio-based esters, aqueous and ultra-pure solvents

|

Safer chemistry with reshored supply chains

|

|

Germany

|

REACH Annex XVII and decarbonization

|

Mass-balanced oxygenated solvents

|

Low-carbon, compliance-first solvent portfolios

|

|

India

|

Carbon Credit Trading Scheme and BIS 15495

|

Alcohol and ester-based food-safe solvents

|

Export-ready, regulation-aligned growth

|

Ink Solvent Market Report Scope

Ink Solvent Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1454 Million

|

|

Market Size (2034)

|

$2236.4 Million

|

|

Market Growth Rate

|

4.9%

|

|

Segments

|

By Solvent Type (Oxygenated Solvents, Hydrocarbon Solvents, Bio-Based and Green Solvents, Halogenated Solvents), By Technology (Water-Based Inks, Solvent-Based Inks, UV-Curable Inks, Oil-Based Inks), By Printing Process (Flexography, Gravure, Lithography, Digital Inkjet, Screen Printing), By End-Use Industry (Packaging, Publishing, Commercial Printing, Textiles, Industrial and Electronics Printing)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, Exxon Mobil Corporation, Shell plc, Dow Inc., Eastman Chemical Company, LyondellBasell Industries N.V., Chevron Phillips Chemical Company, Solvay S.A., Arkema S.A., Univar Solutions, Clariant AG, DIC Corporation, Evonik Industries AG, Sinopec, Celanese Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Ink Solvent Market Segmentation

By Solvent Type

- Oxygenated Solvents

- Hydrocarbon Solvents

- Bio-Based and Green Solvents

- Halogenated Solvents

By Technology

- Water-Based Inks

- Solvent-Based Inks

- UV-Curable Inks

- Oil-Based Inks

By Printing Process

- Flexography

- Gravure

- Lithography

- Digital Inkjet

- Screen Printing

By End-Use Industry

- Packaging

- Publishing

- Commercial Printing

- Textiles

- Industrial and Electronics Printing

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Ink Solvent Industry

- BASF SE

- Exxon Mobil Corporation

- Shell plc

- Dow Inc.

- Eastman Chemical Company

- LyondellBasell Industries N.V.

- Chevron Phillips Chemical Company

- Solvay S.A.

- Arkema S.A.

- Univar Solutions

- Clariant AG

- DIC Corporation

- Evonik Industries AG

- Sinopec

- Celanese Corporation

*- List not Exhaustive