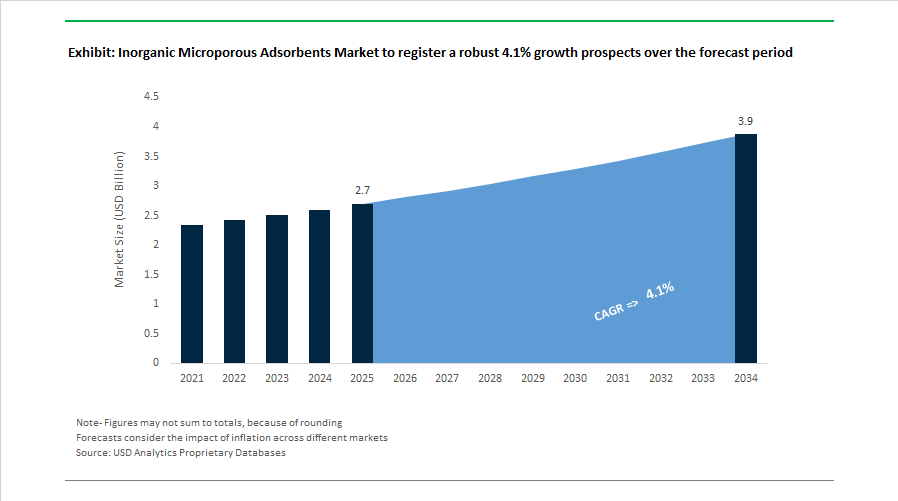

Inorganic Microporous Adsorbents Market to Reach $3.9 Billion by 2034 at 4.1% CAGR as Zeolite Innovation and Hydrogen Applications Accelerate

The Inorganic Microporous Adsorbents Market is projected to grow from $2.7 billion in 2025 to $3.9 billion by 2034, registering a CAGR of 4.1%. Market expansion is being driven by rising demand for zeolite molecular sieves in sustainable aviation fuel (SAF), hydrogen purification, carbon capture, pharmaceutical purification, and circular polymer recycling. Between 2024 and 2026, the sector experienced structural consolidation, advanced shaping breakthroughs, and increased patent activity in hierarchical zeolites, signaling a transition toward high-efficiency, application-specific microporous materials.

In March 2024, W. R. Grace & Co. completed a 21-month expansion of its South Haven, Michigan facility, adding capacity for high-purity silica-based adsorbents used in downstream API purification. During the second quarter of 2024, a sharp spike in alumina prices increased production costs for 3A, 4A, and 5A molecular sieves, prompting manufacturers to introduce surcharge mechanisms across natural gas dehydration applications. Throughout 2024, industry leaders including BASF and Zeolyst International reported a more than 40% increase in patent filings since 2021 for hierarchical zeolites that combine micro- and mesoporosity to improve diffusion efficiency in petrochemical cracking and heavy-metal removal.

Commercial deployment of advanced adsorbent systems accelerated in 2025. In early 2025, BASF began commercial production of loopamid® in Shanghai, utilizing proprietary inorganic adsorbent purification systems to enable textile-to-textile recycling for 100% recycled nylon 6. In May 2025, Clariant Adsorbents Brazil received ADM’s “Strive 35 – Sustainability Award” for its TONSIL™ adsorbents, recognized for improving feedstock quality in renewable fuels and edible oils while meeting strict environmental KPIs. In 2025, Arkema ramped up production of its Siliporite® molecular sieve portfolio optimized for fast-cycle Pressure Swing Adsorption in decentralized green hydrogen units. In late 2025, Honeywell confirmed that Inner Mongolia Jiutai Group selected its UOP eFining™ process for a methanol-to-jet fuel plant producing 100,000 tons per year of Sustainable Aviation Fuel, relying heavily on specialized zeolite purification systems.

Strategic integration and advanced shaping technologies defined late 2025 and early 2026. In September 2025, Technip Energies announced a $556 million agreement to acquire Ecovyst’s Advanced Materials & Catalysts business, including the Zeolyst International joint venture, with closure expected in Q1 2026. The move integrates proprietary zeolite technology into Technip’s carbon capture and sustainable fuel portfolio. In November 2025, BASF and ExxonMobil signed a joint development agreement to scale methane pyrolysis for turquoise hydrogen, utilizing high-temperature inorganic adsorbent beds for gas separation. In December 2025, BASF unveiled X3D® technology, enabling 3D-printed inorganic adsorbents with optimized open structures to reduce reactor pressure drop; a dedicated Ludwigshafen production facility is scheduled to begin operations in 2026. In October 2025, Clariant confirmed that its Adsorbents & Additives unit would be included in an CHF 80 million efficiency program involving site closures and production consolidation through 2027. In January 2026, Arkema finalized the divestment of its plastic additives business, reinforcing its capital allocation toward Specialty Materials, including high-growth molecular sieve applications for air separation and CO2 valorization.

Inorganic Microporous Adsorbents Market Trends and Opportunities Driving Advanced Separation Technologies

Carbon Capture Technologies Accelerating Demand for Engineered Zeolites and Metal–Organic Frameworks

The inorganic microporous adsorbents market is experiencing strong growth as carbon capture, utilization, and storage (CCUS) initiatives scale globally. Advanced materials such as engineered zeolites and metal–organic frameworks (MOFs) are increasingly deployed as high-performance adsorbents capable of selectively capturing carbon dioxide from industrial emissions and direct air capture systems. These microporous adsorption materials, characterized by extremely high internal surface areas and tunable pore structures, function as molecular-scale filters that enable efficient gas separation while reducing the energy required for regeneration.

The scientific and industrial momentum behind MOFs accelerated in December 2025 when the Nobel Prize in Chemistry recognized pioneering work in metal–organic frameworks, validating their role in large-scale carbon extraction technologies. In parallel, BASF has begun industrial-scale production of the CALF-20 MOF at its Seneca, South Carolina facility, supplying materials used by Svante Technologies for high-efficiency carbon capture from industrial flue gases. Public sector investment is also expanding rapidly. In January 2025, the U.S. Department of Energy allocated $101 million to establish five carbon capture test centers, evaluating advanced zeolite and MOF systems for deployment in power plants and cement facilities as part of the U.S. 2035 carbon-neutral electricity strategy. Academic research is also improving performance benchmarks. Recent 2025 studies on isoreticular zeolites such as the IPC-12 family demonstrate binding energies of 37.3–37.9 kJ/mol, achieving an optimal balance between adsorption capacity and low regeneration energy, which significantly reduces the operational power requirements of CCUS systems.

Nuclear Waste Treatment and Reactor Expansion Increasing Demand for Radiation-Resistant Adsorbents

The emerging global nuclear energy renaissance, particularly the development of small modular reactors (SMRs) and advanced nuclear fuel cycles, is creating sustained demand for inorganic microporous adsorbents capable of operating in extreme radiation environments. Materials such as zeolites, titanosilicates, and modified MOFs are widely used in nuclear waste treatment due to their strong ion-exchange properties and structural stability under high radiation and temperature conditions. These adsorbents play a critical role in capturing radioactive isotopes, stabilizing nuclear waste streams, and reducing the overall volume of radioactive material requiring long-term storage.

International nuclear programs are actively supporting research in this area. In May 2025, the OECD Nuclear Energy Agency launched the WISARD (Waste Integration for Small and Advanced Reactor Designs) project, focusing on the development of tailored inorganic adsorbents and ion-exchange materials for advanced reactor fuel cycles such as TRISO and molten salt reactors. Scientific studies published in 2025 in the Journal of Materials Chemistry A confirm that modified MOFs demonstrate strong selectivity and structural resilience when capturing radioactive metal cations in nuclear wastewater treatment systems. Infrastructure development is also increasing the demand for microporous adsorbents. According to the IAEA Nuclear Technology Review 2025, projects such as the National Disposal Facility in Bulgaria near Kozloduy Nuclear Power Plant and nuclear waste remediation programs in Lithuania’s Maišiagala site rely heavily on inorganic adsorption materials for the stabilization and containment of low- and intermediate-level radioactive waste during transportation and long-term repository storage.

Direct Lithium Extraction and Rare Earth Processing Creating New Opportunities for Selective Adsorbents

The global push to secure critical mineral supply chains, particularly lithium and rare earth elements, is opening new opportunities for the inorganic microporous adsorbents market. Advanced adsorption technologies are increasingly replacing traditional solvent extraction methods in direct lithium extraction (DLE) and rare earth element (REE) purification, enabling more selective and environmentally sustainable mineral processing. Zeolites, titanosilicates, and other microporous materials can selectively capture lithium ions or rare earth metals from brines and complex ores while minimizing chemical waste and energy consumption.

Policy initiatives and geopolitical strategies are accelerating adoption. Under India’s Union Budget 2026–27, the government announced Dedicated Rare Earth Corridors across four states, supported by a ₹7,280 crore REPM Manufacturing Scheme, targeting the processing of 482.6 million tonnes of identified rare earth resources. These projects create a major demand base for microporous adsorbents used in chemical separation and purification stages. Meanwhile, global industry analysis published in January 2026 highlighted that 2025 marked a turning point for rare earth supply diversification amid U.S.–China trade tensions. This has encouraged Western processing facilities to adopt titano-silicate adsorbents and advanced zeolite membranes, which significantly reduce the environmental footprint compared with solvent-intensive extraction methods. In lithium mining, international agreements signed by KABIL with Argentina’s CAMYEN in 2025 are exploring lithium brine deposits using selective inorganic adsorbents for DLE, enabling the return of processed brine back into aquifers and supporting emerging water-neutral mining ESG standards.

High-Purity Adsorbents Enabling Advanced Separation in Pharmaceutical and Biotech Manufacturing

The rapid expansion of pharmaceutical and biotechnology manufacturing is creating high-value opportunities for inorganic microporous adsorbents used in separation, purification, and drug delivery systems. Materials such as nanoporous silica gels, synthetic resins, and functionalized microporous adsorbents are widely used in chromatography and filtration processes to remove impurities during the production of active pharmaceutical ingredients (APIs), biologics, and advanced therapeutics. As pharmaceutical manufacturing scales globally, the demand for highly selective adsorbent materials capable of achieving sub-nanometer purification levels is increasing significantly.

Market expansion in pharmaceuticals is reinforcing this trend. According to the IQVIA Institute, global pharmaceutical spending is projected to reach $1.9 trillion by 2027, with approximately 25% adoption of eco-friendly adsorbents in pharmaceutical manufacturing by late 2025 as companies pursue greener purification technologies. Industry investment is also accelerating innovation. Major pharmaceutical and materials companies allocated approximately $180 million in 2025 for R&D focused on AI-optimized adsorbents, designed specifically for monoclonal antibody purification and mRNA therapeutics manufacturing, where traditional filtration methods often fall short. Beyond purification, microporous materials are also advancing drug delivery systems. A 2026 industry update reported that engineered nanoporous structures can improve the stability of temperature-sensitive biologics by around 24%, enabling controlled-release drug delivery platforms and creating a specialized, high-margin segment within the inorganic microporous adsorbents market.

Inorganic Microporous Adsorbents Market Share and Segmentation Insights

Zeolites Dominate Inorganic Microporous Adsorbents Through Precision Pore Engineering and Molecular Sieving Performance

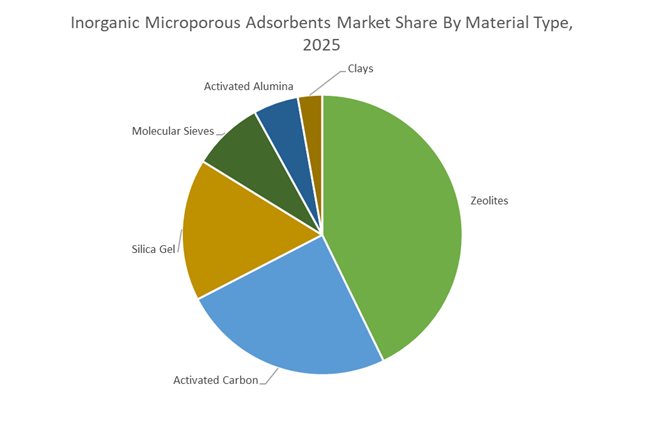

Zeolites represented 42.80% of the Inorganic Microporous Adsorbents Market share in 2025, making them the most widely deployed adsorbent materials in industrial separation and purification processes. Zeolites are crystalline aluminosilicate materials characterized by uniform microporous structures, high surface area, and tunable surface chemistry, enabling highly selective adsorption and molecular sieving performance. Their precisely defined pore structures allow separation of molecules based on size, polarity, and adsorption affinity, making zeolites indispensable in applications such as gas separation, petroleum refining, petrochemical processing, and air purification systems. Synthetic zeolites are particularly valuable because manufacturers can control pore diameter, acidity, and framework composition, enabling adsorbents tailored to specific industrial processes. In 2025, the market has seen rapid development of advanced hierarchical zeolites, which incorporate both micropores and mesopores to enhance mass transport and adsorption efficiency. These engineered materials improve performance in demanding applications including CO₂ capture, xylene isomer separation, and olefin–paraffin separation, supporting the growing demand for high-efficiency industrial separation technologies.

Petroleum Refining Sector Drives the Largest Demand for Inorganic Microporous Adsorbents

Petroleum refining accounted for 34.80% of the Inorganic Microporous Adsorbents Market share in 2025, positioning it as the largest end-use sector for microporous adsorption technologies. Modern refineries rely heavily on adsorbents to enable feedstock purification, hydrocarbon separation, and removal of contaminants such as sulfur, nitrogen compounds, and aromatics from process streams. Inorganic microporous adsorbents including zeolites, molecular sieves, activated alumina, and silica gel are used across numerous refining operations such as hydrotreating feed preparation, paraffin separation, hydrocarbon drying, and catalytic process purification. The massive scale of global refining infrastructure ensures sustained demand for high-performance adsorption materials capable of maintaining process efficiency and product purity. In 2025, the continued integration of refinery and petrochemical production complexes has significantly increased demand for specialized adsorbents designed for high-purity chemical separations. Advanced zeolite materials are increasingly deployed in para-xylene purification, propylene recovery, and aromatics separation processes, enabling production of polymer-grade petrochemical feedstocks required for plastics, fibers, and advanced materials manufacturing.

Competitive Landscape in Inorganic Microporous Adsorbents Market

Honeywell UOP Leads Synthetic Zeolite Innovation and Hydrogen PSA Optimization

Honeywell UOP remains the dominant pioneer in synthetic zeolites, supported by the largest installed base in global oil and gas separation units. Its MOLSIV, TRISIV, and OXYSIV product lines define benchmark performance in dehydration, air separation, and oxygen generation systems. In late 2025, UOP introduced MOLSIV MB, a high-efficiency powder for thermoplastics offering seven times higher moisture loading capacity compared to traditional calcium oxide desiccants. The company’s 2026 strategy emphasizes decarbonization infrastructure, particularly adsorbents optimized for hydrogen pressure swing adsorption and renewable natural gas purification. A recent breakthrough in tailor-made pore topology engineering has improved recovery rates in cryogenic air separation units beyond standard 13X grades. Full integration of alumina manufacturing assets now enables dual-bed dehydration solutions combining activated alumina and molecular sieves for large-scale natural gas and petrochemical drying operations.

BASF SE Integrates Environmental Adsorbents with Carbon Transparency

BASF SE positions its adsorbent portfolio within the Surface Technologies segment, focusing on environmental catalyst and industrial separation solutions. The company’s 2026 EBITDA guidance of €6.2 billion to €7.0 billion reflects contributions from its Environmental Catalyst and Metal Solutions division. Through its Winning Ways strategy, BASF prioritizes adsorbents that enable energy-lean regeneration cycles, lowering lifecycle operating costs in gas purification and petrochemical drying. The Durasorb and Sorbead brands anchor its portfolio, with Sorbead Orange CHAMELEON emerging as a heavy-metal-free indicating silica gel designed for sustainable humidity control. In 2026, BASF advances Scope 3 transparency by providing detailed carbon footprint data per batch of zeolite and alumina, strengthening procurement confidence for customers targeting emissions disclosure compliance.

Arkema S.A. Expands High-Purity Molecular Sieves for Olefin and Medical Applications

Arkema is advancing high-performance molecular sieve technology under the Siliporite brand, particularly the 3A OPX range engineered for olefin drying with minimized co-adsorption and reduced coking tendencies. These features extend bed life and enhance throughput efficiency in petrochemical crackers. In early 2026, Arkema scaled production of its PHYG product range to serve growing steam methane reforming and hydrogen purification demand. Since the pandemic period, Arkema has prioritized medical oxygen concentrator markets, with its molecular sieves now integrated into over 35% of new medical oxygen systems globally. Its 2026 strategic focus on advanced separation technologies includes titanosilicates and engineered minerals tailored for selective mercury and sulfur removal from liquid hydrocarbon streams, addressing stringent refinery and LNG specifications.

Clariant AG Enhances Margin Performance Through Digital Adsorbent Monitoring

Clariant has repositioned its Adsorbents and Additives unit toward higher-margin specialty solutions, achieving a 240 basis point EBITDA margin improvement to 17.8% year on year. The rollout of CLARITY digital service infrastructure enables over 800 users across 38 countries to monitor adsorbent performance and catalyst health in real time, improving plant uptime and predictive maintenance. In 2026, Clariant continues portfolio pruning by reducing exposure to low-margin commodity clay adsorbents and emphasizing Exolit and specialized bentonite technologies for edible oil purification. EU Commission approval of new sustainable additives reinforces alignment with tightening environmental frameworks. The company targets 18.8% innovation sales contribution from its R&D pipeline, underscoring its commitment to high-selectivity separation media and specialty purification systems.

W.R. Grace & Co. Advances Pharmaceutical and Food Safety Adsorbents

W.R. Grace & Co., owned by Standard Industries, remains the largest global producer of silica gel and a major supplier of zeolitic catalysts and adsorbents. Its SYLOBEAD and SYLOSIV brands support applications spanning hydrocarbon drying, insulating glass moisture control, and pharmaceutical purification. In 2026, Grace emphasizes high-purity silica solutions for lipid nanoparticle purification within advanced drug delivery systems. Late 2025 product launches addressed glycidyl ester removal in refined edible oils, aligning with tightening food safety standards in Europe and North America. The company is integrating machine learning into R&D workflows to shorten development cycles for custom adsorbents, accelerating commercialization of tailored pore structures and enhanced adsorption kinetics. Grace also maintains strong positioning in the insulating glass segment, where Phonosorb molecular sieves prevent fogging and condensation in architectural glazing systems.

Zeochem AG Strengthens Natural Gas Dehydration and Oxygen Separation Leadership

Zeochem AG, part of the CPH Group, is recognized for precision-engineered molecular sieves serving natural gas dehydration, oxygen concentration, and petrochemical drying markets. The company holds a significant share in sour gas dehydration applications requiring high thermal stability and resistance to acid gases. In early 2026, Zeochem completed modernization of its Louisville, Kentucky plant, increasing capacity for specialized 13X and 4A molecular sieves by 15%. Its ZEOX molecular sieve portfolio plays a critical role in portable oxygen concentrators, offering superior nitrogen-oxygen separation kinetics. Through a Regional Sovereignty strategy, Zeochem is expanding its Asian production base to reduce lead times and enhance supply reliability for Chinese and Indian petrochemical and LNG infrastructure projects.

United States Inorganic Microporous Adsorbents Market: Onshoring, Energy Transition, and Semiconductor Purity

The United States inorganic microporous adsorbents industry is entering a phase of supply chain localization and application deepening across energy, pharmaceuticals, and semiconductors. In January 2026, BASF confirmed that a new manufacturing line in Cincinnati, Ohio, will reach full start-up in Q1 2026. The facility is engineered to supply high-performance adsorbents and specialty surfactants, with an emphasis on bio-based and biodegradable solutions for North American industrial and personal care customers. This onshoring initiative directly addresses resilience requirements while shortening lead times for regulated end uses that require tight quality control and traceability.

Product innovation is advancing in parallel. Honeywell UOP expanded its MOLSIV adsorbent portfolio in late 2025, introducing low-reactivity variants optimized to minimize side reactions in ethylene and natural gas dehydration, achieving sub-0.1 ppm water specifications demanded by modern petrochemical complexes. In renewable fuels, W. R. Grace & Co. partnered with Chevron during 2025 to integrate advanced silica-based adsorbents into sustainable aviation fuel and renewable diesel pretreatment, targeting efficient removal of trace metals and phosphorus from fully renewable feedstocks. Pharmaceutical and nutraceutical demand is also strengthening, supported by Grace’s 2025 launch of the SYLOID mesoporous silica series to enhance drug micronization and moisture control. Driven by the CHIPS and Science Act, domestic producers are further pivoting toward ultra-high-purity zeolites for cleanroom air filtration and precision gas purification, supporting the 2026 expansion of sub-2nm semiconductor fabrication.

China Inorganic Microporous Adsorbents Market: Policy-Led Upgrading and Electronic-Grade Scale

China’s inorganic microporous adsorbents sector is being reshaped by industrial policy, electronics demand, and tighter environmental standards. Under the MIIT petrochemical growth blueprint for 2025–2026, the chemical sector is mandated to upgrade traditional products into high-end inorganic microporous materials, particularly for electronic-grade gas separation and purification. This policy direction is accelerating investment in zeolites, silica gels, and molecular sieves tailored for semiconductors, display manufacturing, and advanced coatings.

Capacity and compliance developments are converging. BASF is advancing operations at its Zhanjiang Verbund site as it enters a 2026 operational phase, focusing on high-purity adsorbents required for domestic brake fluids and high-performance inkjet intermediates. Regulatory pressure is also intensifying. From June 1, 2026, GB 30981.1-2025 will enforce stricter controls on hazardous substances in industrial coatings and inks, driving increased use of inorganic matting agents and moisture scavengers that meet low-VOC thresholds. Export controls introduced in April 2025 on specific rare-earth metals used in catalytic and security adsorbents have further realigned global supply chains, increasing strategic importance of China’s specialized chemical zones for formulation and substitution development.

European Union Inorganic Microporous Adsorbents Market: Harmonized Assessment and Mass-Balanced Decarbonization

Across Germany and France, the inorganic microporous adsorbents industry is advancing under harmonized regulatory oversight and accelerated decarbonization pathways. Regulation (EU) 2025/2457, adopted in November 2025, introduced the One Substance, One Assessment framework, streamlining scientific evaluation across European Chemicals Agency and European Food Safety Authority. This reform is improving predictability for safety assessments of inorganic adsorbents used in food contact, pharmaceuticals, and medical devices through 2026.

Sustainability leadership is translating into production practice. During 2025, Evonik Coating Additives and BASF implemented mass-balance approaches at German sites, enabling zeolites and silica gels with approximately 40% lower carbon footprints using ISCC PLUS certified feedstocks. At the specialty end, ALTANA, including its BYK business, reported Scope 1 and 2 CO2 neutrality at production sites in late 2025, setting a benchmark for low-carbon adsorbent and additive manufacturing across Europe.

Thailand and India Inorganic Microporous Adsorbents Market: APAC Scale and Incentivized Localization

Southeast Asia and India are emerging as complementary growth platforms for inorganic microporous adsorbents, driven by industrial cleaning, healthcare, and specialty chemical demand. In November 2025, BASF inaugurated a major capacity expansion in Bangpakong, Thailand, focused on bio-based surfactants and adsorbent-compatible formulations serving the APAC industrial cleaning market. This investment strengthens regional supply while aligning with sustainability requirements of multinational customers operating in Asia.

India’s trajectory is anchored in policy incentives. The expansion of the Production-Linked Incentive scheme for specialty chemicals through 2026 is accelerating domestic capacity for medical-grade and industrial-grade inorganic adsorbents. Companies such as Nalco India and Ginni Filaments are leveraging these incentives to localize production of high-purity adsorbents, supporting healthcare, water treatment, and industrial process applications while reducing import dependence.

Inorganic Microporous Adsorbents Industry: Country-Level Strategic Snapshot

Inorganic Microporous Adsorbents Market County Level Snapshot

|

Region

|

Primary Strategic Driver

|

Key Application Focus

|

Structural Direction

|

|

United States

|

Onshoring and energy transition

|

Gas dehydration, renewables, semiconductors

|

High-purity, localized supply with advanced performance

|

|

China

|

Policy-led upgrading and VOC control

|

Electronic-grade separation, coatings

|

Scale-driven modernization with compliance focus

|

|

European Union

|

Harmonized regulation and decarbonization

|

Food, medical, specialty materials

|

Mass-balanced, low-carbon adsorbents

|

|

Thailand & India

|

APAC demand growth and PLI incentives

|

Industrial cleaning, healthcare

|

Regional scale with localized manufacturing

|

Inorganic Microporous Adsorbents Market Report Scope

Inorganic Microporous Adsorbents Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$2.7 Billion

|

|

Market Size (2034)

|

$3.9 Billion

|

|

Market Growth Rate

|

4.1%

|

|

Segments

|

By Material Type (Zeolites, Activated Alumina, Silica Gel, Molecular Sieves, Activated Carbon, Clays), By Function (Dehydration and Desiccation, Separation and Purification, Catalysis and Catalyst Support, Ion Exchange, Contaminant Removal), By End-Use Sector (Petroleum Refining, Chemical Processing, Environmental and Water Treatment, Healthcare and Pharmaceuticals, Food and Beverage, Air Separation)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Honeywell International Inc., BASF SE, W. R. Grace & Co., Arkema S.A., Zeolyst International, Clariant AG, Evonik Industries AG, Tosoh Corporation, Zeochem AG, Mitsubishi Chemical Group, Albemarle Corporation, Axens SA, Yantai Hengye Chemical Industry Co., Ltd., National Aluminium Company Limited, Shijiazhuang Jianda High-Tech Chemical Co., Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Inorganic Microporous Adsorbents Market Segmentation

By Material Type

- Zeolites

- Activated Alumina

- Silica Gel

- Molecular Sieves

- Activated Carbon

- Clays

By Function

- Dehydration and Desiccation

- Separation and Purification

- Catalysis and Catalyst Support

- Ion Exchange

- Contaminant Removal

By End-Use Sector

- Petroleum Refining

- Chemical Processing

- Environmental and Water Treatment

- Healthcare and Pharmaceuticals

- Food and Beverage

- Air Separation

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Inorganic Microporous Adsorbents Industry

- Honeywell International Inc.

- BASF SE

- W. R. Grace & Co.

- Arkema S.A.

- Zeolyst International

- Clariant AG

- Evonik Industries AG

- Tosoh Corporation

- Zeochem AG

- Mitsubishi Chemical Group

- Albemarle Corporation

- Axens SA

- Yantai Hengye Chemical Industry Co., Ltd.

- National Aluminium Company Limited

- Shijiazhuang Jianda High-Tech Chemical Co., Ltd.

*- List not Exhaustive