Market Overview: Sustainability and Thermal Innovation Drive Growth

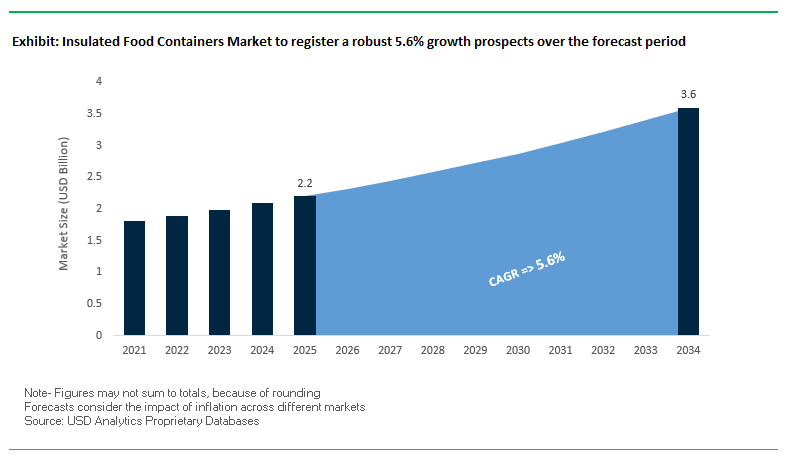

The Insulated Food Containers Market is valued at USD 2.2 billion in 2025 and projected to reach USD 3.6 billion by 2034, expanding at a CAGR of 5.6%. For industry professionals and buyers, the central question is how insulated solutions will evolve to meet demand from on-the-go consumption, food delivery, and sustainability mandates. The market is shaped by innovations in vacuum-insulated panels (VIPs), high-performance foams, and stainless-steel durability, along with strong momentum toward eco-friendly and reusable formats.

Key Insights for Industry Professionals:

- Growth vector: USD 2.2B (2025) → USD 3.6B (2034) at 5.6% CAGR, with growth anchored in meal-prep, catering, and delivery logistics.

- Consumer demand: Shift toward on-the-go food consumption and home-prepped meals at work/school.

- Sustainability push: Durable, reusable formats (stainless steel, glass, recycled plastics) replacing single-use plastics.

- Innovation: VIPs and high-performance foams enable thinner, lighter containers with superior retention.

- Applications: Food delivery, catering, e-commerce packaging, and specialized transit solutions for safe hot/cold storage.

Market Analysis: Recent Developments Highlighting Sustainability and Technology Shifts

The insulated food containers market has seen steady waves of innovation, partnerships, and market consolidation. In August 2025, YETI expanded its product portfolio with a new line of insulated lunch boxes designed to keep food fresh for up to 10 hours, aligning with consumer demand for healthy, portable meal solutions. That same month, DNP showcased recyclable, mono-material medical packaging at Medical Fair Thailand, highlighting cross-sector adoption of sustainable insulated packaging formats.

Strategic M&A continues to shape the industry. In July 2025, the Amcor–Berry Global all-stock merger created a global packaging leader with expanded capabilities across rigid and flexible materials, strengthening its position in insulated and specialty food solutions. Also in July 2025, new research highlighted surging demand for smart packaging technologies QR codes, NFC, and RFID integrated into insulated solutions for traceability and consumer engagement.

Earlier in March 2025, Toppan Group acquired Italy’s Irplast, a high-performance BOPP film company, to strengthen its sustainable packaging portfolio. Reports from November 2024 emphasized e-commerce demand for flexible and semi-rigid insulated formats, which balance cost efficiency with thermal control, while in September 2024, Shiseido replaced plastic bubble wrap with recyclable kraft honeycomb wrap for shipping, reinforcing the sustainability shift. The consistent thread across these developments is the dual push for performance and eco-responsibility, ensuring containers can meet both temperature retention and waste reduction goals.

Trends and Opportunities Defining the Future of the Insulated Food Containers Market

Corporate Sustainability Mandates Driving Material Innovation

Sustainability is becoming a non-negotiable feature in the insulated food containers market, as global consumer packaged goods (CPG) leaders and foodservice operators commit to ambitious environmental goals. Companies such as Nestlé and Unilever have made measurable progress toward reducing virgin plastic use, with Nestlé reporting a 14.9% reduction in virgin plastic use between 2018–2024 and aiming for a 33% cut by 2025. Similarly, Unilever has pledged to reduce virgin plastic by 30% by 2026 while investing in circular economy ventures such as Lucro Plastecycle to secure post-consumer recycled plastic supply.

These corporate commitments are directly pressuring packaging suppliers to accelerate innovation in bio-based polymers, biodegradable composites, and post-consumer recycled (PCR) content. According to sustainable packaging insights, the industry is seeing strong momentum toward materials that are not only recyclable but also reduce greenhouse gas emissions during manufacturing. Lightweight bio-based containers further enhance efficiency by cutting down on transport fuel consumption. This convergence of regulatory mandates, corporate investment, and consumer preference for “eco-conscious” products is making sustainable insulated food containers a high-value growth avenue in the global packaging ecosystem.

Integration of IoT for Cold Chain Integrity in Meal Delivery

The explosive growth of premium meal kits and specialized diet services such as HelloFresh and Factor is creating new performance requirements for insulated food packaging. Beyond passive insulation, companies are now integrating IoT-based temperature monitoring systems to ensure cold chain integrity from warehouse to doorstep. Providers like Seemoto and E-Control Systems offer real-time wireless monitoring solutions that align with HACCP food safety standards, ensuring compliance and protecting consumer trust.

IoT sensors allow logistics operators to receive real-time alerts on temperature fluctuations, humidity changes, or equipment malfunctions, enabling proactive intervention. For instance, Digi-Key Electronics highlights how predictive alerts reduce downtime and prevent costly spoilage events. This technology-driven transparency also reinforces brand trust, as continuous data ensures customers receive perishable items under safe storage conditions. The integration of IoT monitoring not only reduces waste and spoilage but also transforms insulated food containers into data-enabled assets that drive customer satisfaction and operational efficiency.

Expansion of Pharmaceutical-Grade Insulation for Home-Delivered Groceries

As online grocery delivery expands globally, there is a growing opportunity for pharmaceutical-grade insulation previously used for sensitive medical shipments to be adapted for food logistics. Advanced solutions like vacuum insulated panels (VIPs), which can hold stable temperatures for extended periods, are increasingly being marketed for frozen and chilled grocery deliveries.

Suppliers such as Supertech are already exploring cross-industry applications, promoting VIP technology for insulated bags and boxes that deliver the same reliability as pharmaceutical containers. This shift responds directly to consumer expectations for frozen and chilled groceries that maintain integrity across complex last-mile networks. With frozen products requiring stricter temperature consistency, the adoption of pharmaceutical-level insulation in food delivery provides a premium consumer experience while minimizing spoilage. For insulated food container manufacturers, this represents a lucrative path to move up the value chain by offering ultra-high-performance solutions beyond traditional packaging.

Development of Standardized, Reusable Container Pooling Systems

The global push toward reusable packaging, bolstered by both corporate initiatives and regulatory frameworks like the EU Packaging and Packaging Waste Regulation (PPWR), is accelerating the adoption of standardized, reusable insulated container systems. Logistics companies such as OLIVO Logistics are pioneering durable expanded polypropylene (EPP) containers that can be reused hundreds of times while maintaining thermal stability with eutectic plates.

Collaborative pooling models are reshaping the market. For instance, Circolution in Germany operates a container-sharing platform that cuts costs and waste across the supply chain, while IFCO’s SmartCycle enables widespread reuse of plastic containers in produce logistics. Startups like BOXO and Again are also innovating with infrastructure for sorting, cleaning, and redistributing reusable containers at scale.

Competitive Landscape: Leading Brands Redefine Performance and Sustainability

The competitive environment is shaped by global leaders leveraging materials science, product design, and strong brand positioning to meet growing demand for durable, reusable, and eco-aligned insulated food containers.

YETI Coolers, LLC: Premium durability with extended freshness

Overview. YETI has built its reputation on rugged, thermally superior outdoor and lifestyle products. In August 2025, it launched insulated lunch boxes capable of keeping food fresh for up to 10 hours, targeting school, work, and daily commuter use. Its offerings, including Rambler® drinkware and insulated food containers, emphasize stainless steel and advanced insulation. YETI’s strategy centers on innovation-driven brand expansion, maintaining a premium identity while appealing to diverse consumer groups.

Thermo Fisher Scientific Inc.: Scientific precision in insulated solutions

Overview. Thermo Fisher applies its life sciences expertise to insulated containers designed for temperature-sensitive samples and reagents. In July 2025, it announced a USD 2B US investment to expand manufacturing and strengthen resilience. Its insulated product line spans cryogenic vials, insulated shipping boxes, and specialized labware. Thermo Fisher’s focus is on compliance, sterility, and reliability, with a strategy built around innovation for healthcare, diagnostics, and industrial sectors.

Pelican Products, Inc.: Rugged insulated performance for logistics and recreation

Overview. Pelican is globally recognized for protective cases and thermal packaging. Its subsidiary Pelican BioThermal has expanded deep frozen ranges for COVID-19 vaccines and biologics, and is exploring recyclable VIPs. Core offerings include the Pelican Elite Cooler series and biopharma thermal solutions. Pelican’s focus is on durability and cold chain performance, with investments in innovation and partnerships to enhance sustainability and reliability.

Hydro Flask: Lifestyle branding meets durable insulation

Overview. Hydro Flask dominates the insulated drinkware and soft cooler niche, extending its line with Insulated Food Jars and Carry Out™ Lunch Boxes. These stainless-steel products provide long-lasting thermal retention and durability. Known for color and design innovation, Hydro Flask continues to attract a wide consumer base with customizable lids and accessories. Its strategy blends premium lifestyle branding with functional product innovation.

S’well: Stylish sustainability for food and drink containers

Overview. S’well is positioned as a premium, design-forward brand. Its offerings, such as S’well Eats™ 2-in-1 bowls, combine stainless steel outers with microwave-safe inner prep bowls. The company emphasizes sleek design, sustainable materials, and collaborations (e.g., Crayola co-branded lines). Its strategy is to merge functionality with fashion, maintaining a strong appeal among urban, eco-conscious, and style-driven consumers.

Insulated Food Containers Market Share Insights

Insulated Lunch Boxes Dominate Market Share by Product Type in Insulated Food Containers

Insulated lunch boxes hold the largest share of the insulated food containers market at 35% in 2025, reflecting their universal relevance across consumer demographics. Their dominance stems from the growing preference for home-prepared meals among school children, office professionals, and health-conscious consumers who seek to maintain food safety and temperature throughout the day. Unlike insulated bottles or bulk containers, lunch boxes are versatile for both hot and cold foods, ensuring strong daily-use demand. Insulated bottles follow closely, driven by hydration and wellness trends as consumers prioritize reusable, temperature-retaining containers for commuting and outdoor activities. Insulated bags and liners are emerging as a logistics-focused growth driver, propelled by the surge in meal kit delivery, grocery e-commerce, and last-mile distribution of perishables, where affordability and flexibility are key. Commercial categories such as jugs, carafes, and bulk insulated containers retain niche but strategic roles in catering, events, and industrial-scale food handling, but their overall contribution is smaller compared to the high-volume household and personal-use categories. This segmentation underscores how daily consumer use and meal-prep culture anchor demand, while delivery-driven applications are reshaping growth trajectories.

Food and Beverages Dominate Market Share by Application in Insulated Food Containers

The food and beverages sector accounts for 70% of the insulated food containers market in 2025, firmly establishing it as the foundation of industry demand. From individual consumers using lunch boxes and bottles to catering services relying on insulated carafes and bulk containers, the sector covers the full spectrum of applications. Its dominance is reinforced by the global emphasis on food safety, convenience, and waste reduction, where maintaining temperature is critical to preserving freshness and extending usability. The rapid growth of e-commerce and food delivery represents the strongest growth engine, as meal delivery platforms, grocery services, and subscription-based meal kits increasingly depend on cost-effective insulated liners and bags to maintain product integrity during last-mile logistics. Pharmaceuticals and healthcare form a smaller but high-value niche, requiring precise cold-chain performance for vaccines, biological samples, and temperature-sensitive drugs. Although limited in volume, this segment demonstrates how the insulated container market is bifurcated between high-volume food-related demand and high-value cold-chain healthcare applications.

United States Insulated Food Containers Market Bolstered by EPR Regulations and Smart Packaging Innovations

The U.S. insulated food containers market is heavily shaped by California’s SB-54 Extended Producer Responsibility (EPR) law, which mandates a 25% reduction in plastic usage by 2032 and establishes a $5 billion waste fund. This regulatory push is driving the adoption of reusable and sustainable materials such as stainless steel, glass, and high-performance polymers.

Technological advancements are transforming the sector, with innovations like reusable bulk insulated containers for dry ice and perishable goods, as introduced by Sonoco ThermoSafe in August 2025. Smart packaging with IoT sensors for real-time temperature monitoring is also gaining traction, ensuring food safety during transportation. Corporate investments focus on multi-compartment, leak-proof designs catering to the booming food delivery and on-the-go meal segments. Sustainability is prioritized, with antimicrobial technologies and eco-friendly materials integrated into new product designs, aligning with consumer demand and regulatory pressures.

Germany Insulated Food Containers Market Driven by Circular Economy and Alu-Free Packaging

Germany’s insulated food containers industry operates under the EU Packaging and Packaging Waste Regulation (PPWR), effective February 2025, mandating full recyclability or reusability by 2030. This has accelerated the adoption of sustainable insulated container solutions, especially reusable designs.

The market is witnessing innovative solutions such as aluminum-layer-free aseptic cartons, pioneered by Hochwald in partnership with SIG, which maintain insulation while reducing carbon footprint. Germany’s Packaging Act (VerpackG) incentivizes recyclable packaging through modulated fees, encouraging manufacturers to design containers that are easier to recycle. Corporate investment, including SIG’s SIG Terra portfolio of sustainable materials, reflects a strong focus on high-performance, eco-friendly insulated containers across liquid and perishable food applications.

China Insulated Food Containers Market Expands Through Dual Carbon Policies and Domestic Manufacturing

China’s insulated food containers market is driven by governmental initiatives such as the “dual carbon” goal and the March 2024 Action Plan for Large-Scale Equipment Updates, promoting sustainable materials and recycling. Regulatory reforms, including bans on disposable plastics in e-commerce and takeaway food, have accelerated the adoption of reusable insulated containers.

Technological advancements include the integration of AI, automation, and IoT-enabled real-time temperature monitoring, improving cold chain logistics efficiency. The push for domestic manufacturing to substitute imported products is a key trend, with local companies expanding capacity to meet the growing demand for high-quality, circular packaging solutions. These trends are particularly strong in food delivery and e-commerce sectors, ensuring temperature-sensitive goods are delivered safely and sustainably.

Japan Insulated Food Containers Market Leveraging Precision Manufacturing and Modular Designs

Japan’s insulated food container industry benefits from advanced precision manufacturing and next-generation production technologies. Innovations include self-cleaning materials, airtight systems, and bento-style modular containers that reduce food waste while catering to consumer preferences.

Regulatory guidance under the Plastic Resource Circulation Act (April 2022) promotes environmentally friendly packaging, limiting single-use plastics. Companies like Thermos, part of Nippon Sanso Holdings, focus on specialty vacuum-insulated containers with global reach. The market emphasizes high-performance and functional designs, blending traditional aesthetics with modern leak-proof and modular features to serve the home, office, and food delivery segments.

Brazil Insulated Food Containers Market Fueled by Sustainable Policies and Logistics Innovations

Brazil’s insulated food containers market is benefiting from sustainable waste management policies, including the National Solid Waste Policy, which encourages recycling and eco-friendly packaging. Government programs are expected to mandate increased recycling targets for manufacturers, driving demand for reusable containers.

Technological advancements focus on integrated shuttle systems that maintain temperature for frozen, chilled, and ambient foods during last-mile delivery. Key applications are in frozen food, fresh produce, and processed ready-to-eat meals. Corporate investments, such as Klabin’s BRL 188 million expansion of sustainable corrugated board production, support the growing need for insulated solutions in cold chain logistics and food delivery services.

United Kingdom Insulated Food Containers Market Strengthened by EPR Legislation and Sustainable Packaging Trends

The UK’s insulated food containers market is shaped by Extended Producer Responsibility (EPR) legislation, which shifts the cost of handling packaging waste to businesses. Higher fees for non-recyclable plastics and complex multi-material packaging encourage the adoption of reusable and sustainable insulated solutions.

Government initiatives, including bans on single-use expanded and extruded polystyrene containers, further drive the transition to eco-friendly packaging. Growth in food delivery and takeaway services creates demand for high-quality thermal insulation. Manufacturers are focusing on recyclable, reusable, and biodegradable materials to align with regulatory requirements and consumer preferences, ensuring both sustainability and compliance in the evolving market.

Insulated Food Containers Market Report Scope

Insulated Food Containers Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$2.2 Billion

|

|

Market Size (2034)

|

$3.6 Billion

|

|

Market Growth Rate

|

5.6%

|

|

Segments

|

By Material (Stainless Steel, Plastic, Glass, Paper & Paperboard, EPS, Others), By Product Type (Insulated Lunch Boxes, Insulated Jugs & Carafes, Insulated Bottles, Insulated Bags & Liners, Insulated Bulk Containers), By Application (Food & Beverages, Pharmaceuticals & Healthcare, E-commerce & Food Delivery), By End-Use (Retail, Commercial, Industrial)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Thermos L.L.C. (Nippon Sanso Holdings), Zojirushi America Corporation, Stanley (PMI Worldwide), Hydro Flask (Helen of Troy Limited), Contigo (Newell Brands), Cool Gear International, LLC, Aladdin (PMI Worldwide), Laken, Sonoco ThermoSafe (Sonoco Products Company), Cold Chain Technologies, Inc., Pelican Products, Inc., Amcor plc, Greiner Packaging International GmbH, RPC Group Plc, Cambro Foodservice Equipment and Supplies

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Insulated Food Containers Market Segmentation

By Material

- Stainless Steel

- Plastic

- Glass

- Paper & Paperboard

- EPS

- Others

By Product Type

- Insulated Lunch Boxes

- Insulated Jugs & Carafes

- Insulated Bottles

- Insulated Bags & Liners

- Insulated Bulk Containers

By Application

- Food & Beverages

- Pharmaceuticals & Healthcare

- E-commerce & Food Delivery

By End-Use

- Retail

- Commercial

- Industrial

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Insulated Food Containers Market

- Thermos L.L.C. (Nippon Sanso Holdings)

- Zojirushi America Corporation

- Stanley (PMI Worldwide)

- Hydro Flask (Helen of Troy Limited)

- Contigo (Newell Brands)

- Cool Gear International, LLC

- Aladdin (PMI Worldwide)

- Laken

- Sonoco ThermoSafe (Sonoco Products Company)

- Cold Chain Technologies, Inc.

- Pelican Products, Inc.

- Amcor plc

- Greiner Packaging International GmbH

- RPC Group Plc

- Cambro Foodservice Equipment and Supplies

* List Not Exhaustive

Methodology

USDAnalytics employed a comprehensive research methodology to evaluate the Insulated Food Containers Market, integrating primary interviews with packaging engineers, product developers, foodservice operators, and logistics specialists alongside secondary research from company reports, regulatory filings, industry publications, and verified databases. Market sizing, CAGR projections, and forecasts were developed using a combination of bottom-up and top-down approaches, cross-validated with historical adoption trends, materials consumption, and product deployment data. The analysis focuses on innovations in vacuum-insulated panels (VIPs), high-performance foams, stainless-steel and glass alternatives, and IoT-enabled cold chain monitoring. Sustainability trends, corporate mandates, and regulatory frameworks such as EPR, PPWR, and single-use plastic bans were factored into growth projections. Regional dynamics across North America, Europe, Asia-Pacific, and Latin America were incorporated, alongside competitive strategies of leading players like YETI, Thermo Fisher, Pelican, Hydro Flask, and S’well, highlighting innovations in reusable, eco-friendly, and high-performance insulated containers for food delivery, e-commerce, meal kits, and specialized cold-chain applications.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.