Jerry Cans Market Overview: Lightweighting, Shelf Life, and Safety Driving Growth

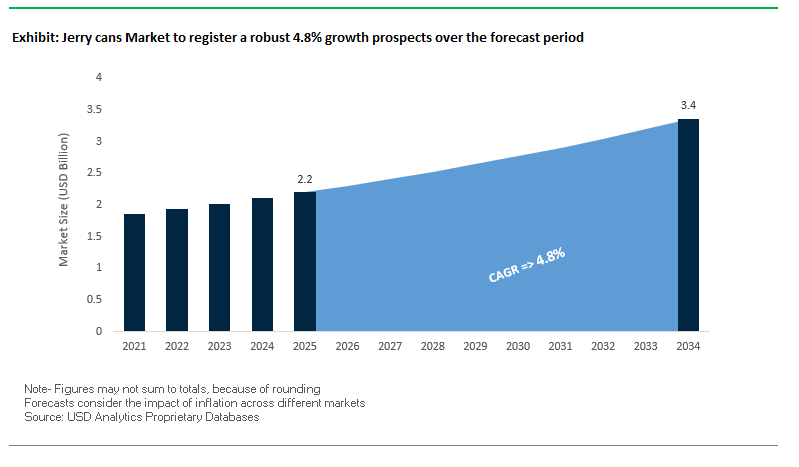

The Global Jerry Cans Market is expected to grow from $2.2 billion in 2025 to $3.4 billion by 2034, expanding at a CAGR of 4.8%. Jerry cans remain a critical component in the packaging industry, serving diverse sectors such as chemicals, agrochemicals, edible oils, fuels, and beverages. The market is shaped by the adoption of HDPE-based lightweight designs, innovations in collapsible cans, and the widespread use of barrier layers to extend shelf life.

Professionals in the industry are increasingly focused on cost optimization, safety compliance, and sustainability, given the strong demand for UN-rated jerry cans in transporting hazardous and sensitive products. The shift toward circular packaging solutions using post-consumer recycled (PCR) content also reflects the industry’s movement toward a low-carbon economy.

Key Insights for Industry Professionals:

- Lightweight HDPE Cans: Up to 50% lighter than steel, improving transport efficiency and lowering emissions.

- Extended Shelf Life Advantage: Barrier layers protect sensitive products like oils, chemicals, and agro-inputs.

- Collapsible Jerry Cans: Reduce post-use volume by up to 80%, streamlining storage and reverse logistics.

- Safety and Compliance: UN-rated cans ensure reliable transport of hazardous materials, a regulatory must.

Market Analysis: Recent Developments in the Jerry Cans Industry

The Jerry Cans Market has seen significant corporate moves, investments, and sustainability-driven innovations over the past two years. In August 2025, Smurfit WestRock, the newly formed leader in paper-based packaging, launched an all-paper pallet stretch wrap, presenting a recyclable alternative to conventional polyethylene films. Though not a direct competitor to jerry cans, it reflects the industry’s broader drive toward sustainability.

In February 2025, Smurfit Kappa invested €54 million in its Alicante, Spain bag-in-box plant, doubling capacity and enhancing energy efficiency. The expansion is designed to strengthen the company’s competitive edge in liquid packaging, indirectly intensifying competition with jerry can formats. Similarly, in January 2025, the merger between Smurfit Kappa and WestRock was finalized, creating a packaging giant with enhanced capabilities to disrupt multiple liquid packaging markets.

Innovation around recyclable materials is reshaping the industry. In November 2024, Smurfit Kappa introduced a recyclable polyethylene film to replace nylon in bag-in-box products, signaling a broader trend toward barrier films that could also benefit jerry can liners. In October 2024, Amcor launched a new recyclable connector for bag-in-box solutions, catering to customers like Walmart, demonstrating how sustainability pressures are reshaping the competitive landscape.

Strategic acquisitions and certifications also shaped the market. In February 2024, Sealed Air completed its acquisition of Liquibox, expanding into liquid dispensing packaging a direct competitor to jerry cans. Meanwhile, Fu Deng Plastic Co., Ltd (July 2024) achieved European food-grade container standards (BPA-free, No DEHP), paving its way into the highly regulated food and beverage segment. In July 2023, Avior finalized its acquisition of Brematech Inc., strengthening its industrial packaging portfolio.

Emerging Trends and Strategic Opportunities in the Jerry Cans Market

Strategic Shift Towards Advanced, Sustainable Materials

The industry is moving away from conventional HDPE-only structures and embracing advanced, sustainable materials that balance durability with circularity. Leading manufacturers such as Berry Global have introduced 20- and 25-liter jerry cans containing up to 35% post-industrial recycled HDPE (rHDPE) that carry UN approval for transporting hazardous goods. This milestone highlights that recycled content, when sourced and processed under controlled systems such as from IBCs and industrial drums, can achieve the same performance benchmarks as virgin plastic.

Government regulations and corporate pledges are also accelerating this transition. Nestlé, for instance, has committed to sourcing two million metric tons of food-grade recycled plastics by 2025, backed by a 1.5 billion Swiss Franc investment. Certification bodies like ISCC are reinforcing this shift by ensuring recycled supply chains are credible and compliant. The challenge lies in maintaining product integrity while integrating recycled content, but manufacturers are increasingly meeting this requirement through targeted R&D and closed-loop recycling systems, positioning sustainable jerry cans as the industry standard.

Integration of Smart Technology for Logistics and Safety

A major transformation in jerry cans is the incorporation of IoT-enabled features that elevate containers from passive storage to active supply chain assets. Using sensor technologies like Semtech’s LoRa, jerry cans can now provide real-time tracking of location, fill levels, and temperature, offering unprecedented visibility in logistics. This development reduces inefficiencies in industries dealing with hazardous materials or critical fluids.

For industrial and commercial applications, smart jerry cans enable automated inventory management by triggering alerts when fluid levels drop, thereby reducing manual labor and preventing supply chain disruptions. Safety is another benefit, with sensors detecting tampering or unauthorized movement, ensuring compliance in high-risk sectors like chemicals or pharmaceuticals. As smart logistics become mainstream, the adoption of connected jerry cans is set to become a differentiator in industrial packaging solutions.

Capitalizing on Global Water Scarcity and Emergency Preparedness Initiatives

With global water demand projected to outstrip supply by 40% by 2030, durable and portable water storage solutions are becoming critical. Jerry cans are emerging as essential tools in both humanitarian relief and long-term water management strategies. Governments, NGOs, and international agencies such as the UN are investing heavily in portable containers to support emergency preparedness, disaster relief, and sanitation programs.

NGOs working on drought mitigation and rainwater harvesting, such as those highlighted by Social For Action, further underscore this demand. After natural disasters like floods, hurricanes, or droughts, the immediate priority is safe drinking water, and jerry cans remain the most reliable solution. This has created a steady demand in both developed and developing regions, presenting manufacturers with a growing humanitarian-focused market that is expected to accelerate as climate impacts intensify.

Development of Specialty Cans for the Electric Vehicle Coolants Market

The electrification of mobility is generating a lucrative new demand for specialty jerry cans designed to handle EV battery coolants. Products like LIQUI MOLY’s Battery Coolant EV 200, which requires ultra-pure and non-reactive packaging, highlight the need for containers with advanced specifications. These jerry cans must ensure zero contamination, corrosion resistance, and long-term integrity to protect high-value fluids essential for EV battery performance.

The aftermarket adds another growth layer: as the EV fleet expands globally, battery coolant replacement is emerging as a recurring service requirement. Analysts note that service networks will rely on dedicated coolant storage and handling systems, making specialized jerry cans indispensable. For manufacturers able to meet these strict standards, the EV sector represents a fast-growing, high-margin niche that will continue to scale as governments push EV adoption worldwide.

Competitive Landscape: Key Players in the Global Jerry Cans Market

The competitive landscape of the Jerry Cans Market is marked by global packaging majors and specialized industrial packaging leaders that continue to innovate around sustainability, compliance, and operational efficiency.

Smurfit West Rock: Leveraging paper-based alternatives to liquid packaging

Formed by the merger of Smurfit Kappa and WestRock, Smurfit WestRock has positioned itself as a leader in paper-based packaging. While not a traditional jerry can manufacturer, its bag-in-box systems compete directly with jerry cans in food and beverage logistics. The company’s Lx polyethylene film, a recyclable nylon alternative, highlights its sustainable innovation strategy. Its vertically integrated model, from forestry to packaging, provides a strong competitive advantage.

Mauser Packaging Solutions: Pioneering PCR-based jerry cans

Mauser is a global industrial packaging leader producing steel and plastic jerry cans, drums, and IBCs. Its PureMauser® jerry cans, made from 100% recycled HDPE, are central to its sustainability agenda. With more than 120 production sites in over 20 countries, Mauser provides localized support on a global scale. Its strong focus on circular economy practices and customer-specific designs reinforces its market leadership in regulated industries.

Greif, Inc: Innovating with bio-based resin jerry cans

Greif manufactures steel and plastic jerry cans for industries like chemicals, oil & gas, and food. Its Brazilian division recently developed 10-liter multilayer jerry cans made from sugarcane-derived polyethylene resin, demonstrating innovation in bio-based materials. The company’s strategy emphasizes lightweighting, recycled inputs, and product diversification, positioning it as a frontrunner in sustainable industrial packaging.

RPC Group (Berry Global): Strengthening plastic packaging capabilities

RPC Group, now part of Berry Global, remains influential in the jerry cans segment. Berry Global leverages advanced processing technologies such as blow molding and injection molding to deliver cost-effective and high-performance jerry cans. The company is also working toward its 2025 target of 100% recyclable or reusable packaging, aligning with global sustainability standards. Its acquisition strategy continues to expand its reach in consumer and industrial packaging markets.

Sealed Air Corporation: Expanding liquid packaging alternatives

Sealed Air has diversified into liquid packaging following its 2024 acquisition of Liquibox, a major bag-in-box provider. Its expanded portfolio includes pouches, bag-in-box containers, and dispensing taps, offering strong competition to jerry cans in liquid transport. Sealed Air’s technology-driven solutions focus on supply chain efficiency and waste reduction, making it a strong player in liquid packaging segments competing for jerry can demand.

Jerry cans Market Share Insights

10–25L Jerry Cans Dominate Market Share by Capacity in Jerry Cans Industry

Jerry cans with a 10–25 liter capacity account for 45% of the market, cementing this range as the global workhorse. The 20L jerry can is a near-universal standard for transporting fuels, lubricants, and potable water, striking the balance between portability and volume efficiency. Its share is reinforced by regulatory compliance, with UN/DOT-certified designs widely mandated for hazardous material handling. In agriculture, construction, and disaster relief, the 20L jerry can is indispensable, while in petrochemical supply chains it represents the most frequently produced size. This segment benefits from durability innovations in high-density polyethylene (HDPE) with UV stabilization, extending lifecycle and lowering replacement costs, thereby entrenching its dominance in both developed and emerging economies.

Oil & Petroleum Industry Leads Market Share by End-Use in Jerry Cans Industry

Oil and petroleum applications account for 30% of the jerry cans industry, underscoring its historical and ongoing role as the segment’s anchor. Designed originally for military fuel transport, jerry cans remain irreplaceable for portable fuel storage across industrial, agricultural, and consumer sectors. The segment’s share is supported by robust demand in emerging economies where decentralized fuel distribution and off-grid energy reliance are common. The durability and spill-prevention features of HDPE and metal jerry cans ensure compliance with global fuel transport safety standards, making them indispensable for handling diesel, gasoline, and kerosene. Even with the rise of electrification in transportation, the sheer scale of global fuel demand ensures oil and petroleum remain the largest and most stable end-use segment.

United States: Specialized and Innovative Jerry Cans Driving Market Growth

The U.S. jerry cans market is characterized by a strong emphasis on high-durability, leak-proof containers for industrial, commercial, and recreational applications. Leading players such as Wavian USA and Scepter Military Containers are innovating with features like self-venting lids, pressure relief valves, and integrated measuring systems to improve convenience and safety. The Environmental Protection Agency (EPA) has implemented stricter controls on volatile organic compounds (VOCs) and material safety, prompting manufacturers to develop eco-friendly and compliant jerry can solutions.

Consumer trends are also shaping the market, with off-road recreation, camping, and emergency preparedness driving demand for reliable fuel and water storage containers. Additionally, the ongoing adoption of electric vehicles (EVs) is influencing market dynamics. While traditional gasoline storage may decline, jerry cans are finding new applications in lubricants, biofuels, and other automotive fluids, presenting opportunities for diversified product offerings.

European Union: Circular Economy and Advanced Recycling Technologies Boost Jerry Can Innovation

The EU jerry cans market is being propelled by the Packaging and Packaging Waste Regulation (PPWR), effective from February 2025, which mandates waste reduction and sustainable material usage. Initiatives such as Horizon Europe are providing funding for R&D in bio-based and compostable materials, supporting the development of next-generation jerry cans. Investments by companies like Sirplaste Portugal and SCG Chemicals in advanced recycling technologies are enhancing the production of high-density polyethylene (HDPE) pellets, a critical material for jerry cans.

Regulatory compliance is also key, with the European Chemicals Agency (ECHA) REACH regulations imposing strict limits on hazardous substances, boosting demand for safe, sustainable, and high-performance jerry cans. Manufacturers are increasingly integrating recycled content in new jerry cans to meet the growing emphasis on a circular economy, ensuring both environmental compliance and cost efficiency.

China: Government Initiatives and Lightweight, High-Performance Jerry Cans Propel Market Expansion

China’s jerry cans market is heavily influenced by the 14th Five-Year Plan, which emphasizes plastic pollution control and the development of the remanufacturing industry. Domestic manufacturers are expanding rapidly to meet the demand for lightweight, high-performance jerry cans with enhanced barrier properties, especially for the industrial and agrochemical sectors.

Government incentives, including tax breaks for green technology adoption, are encouraging the use of sustainable materials and eco-friendly manufacturing processes. The combination of industrial growth, agricultural expansion, and domestic consumer demand is fueling China’s position as a key market for high-quality, innovative jerry cans.

India: Regulatory Support and Sustainable Fuel Initiatives Driving Jerry Can Adoption

The Indian jerry cans market is benefiting from government programs such as Production Linked Incentive (PLI) and Design Linked Incentive (DLI) schemes, aimed at building a robust domestic manufacturing ecosystem for both consumption and export. Policies banning certain single-use plastic items are creating a strong demand for reusable jerry cans for various applications, including fuel, water, and agrochemical storage.

The SATAT initiative, promoting Compressed Bio-Gas (CBG) for sustainable transport, is a major driver, increasing the need for specialized jerry cans for fuel storage and distribution. Additionally, the Bureau of Indian Standards (BIS) has implemented mandatory quality and safety standards for plastic containers, ensuring that high-performance, compliant jerry cans dominate the market.

Brazil: Lightweight HDPE Jerry Cans and Sustainable Waste Policies Shaping Market Demand

In Brazil, the jerry cans market is evolving under the influence of sustainability and efficiency initiatives. Greif launched a 20% lighter, high-performance jerry can in June 2022, improving transport efficiency and reducing environmental impact. The National Solid Waste Policy (PNRS) emphasizes responsible waste disposal, reuse, and recycling, driving adoption of high-density polyethylene (HDPE) jerry cans across industrial, agrochemical, and lubricant applications.

The market is also supported by the increasing use of jerry cans for bulk storage and transportation, offering cost-effective solutions for a variety of sectors. Technological innovations and environmental compliance continue to be key factors shaping Brazil’s growing market for durable, reusable jerry cans.

Japan: Regulatory Push and Recycling Innovations Boost Eco-Friendly Jerry Cans

Japan’s jerry cans market is heavily influenced by the government’s Plastic Resource Circulation Strategy, which aims to make all plastic goods reusable or recyclable by 2025. The Plastic Resource Circulation Promotion Law, effective in 2025, mandates the reduction or redesign of 12 single-use plastic products, prompting the shift toward reusable and eco-friendly jerry cans.

Collaborative initiatives between the private and public sectors, such as the partnership of Toppan and Mitsubishi Chemical Group, are focused on developing new material recycling processes for packaging, with implementation targeted by 2027. These innovations highlight Japan’s commitment to sustainable, high-performance jerry cans, positioning the country as a leader in eco-conscious container solutions.

Jerry cans Market Report Scope

Jerry cans Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$2.2 Billion

|

|

Market Size (2034)

|

$3.4 Billion

|

|

Market Growth Rate

|

4.8%

|

|

Segments

|

By Material (Plastic, Metal, Other Materials), By Capacity (Below 10 Liters, 10–25 Liters, Above 25 Liters), By End-Use Industry (Oil & Petroleum, Chemicals, Food & Beverages, Agrochemicals, Pharmaceuticals, Other End-Use Industries), By Shape (Square, Round, Rectangle)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Greif Inc., Mauser Packaging Solutions, Myers Industries Inc., SCHÜTZ GmbH & Co. KGaA, Time Technoplast Ltd., Barrier Plastics Inc., Wilkinson Containers Ltd., DS Smith Plc, AST Kunststoffverarbeitung GmbH, Scepter Canada Inc., California Plastics Products, Ipackchem Group SAS, Promens h, Can-One Berhad, SOTRALENTZ Packaging S.A.S

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Jerry cans Market Segmentation

By Material

- Plastic

- Metal

- Other Materials

By Capacity

- Below 10 Liters

- 10–25 Liters

- Above 25 Liters

By End-Use Industry

- Oil & Petroleum

- Chemicals

- Food & Beverages

- Agrochemicals

- Pharmaceuticals

- Other End-Use Industries

By Shape

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Jerry cans Market

- Greif Inc.

- Mauser Packaging Solutions

- Myers Industries Inc.

- SCHÜTZ GmbH & Co. KGaA

- Time Technoplast Ltd.

- Barrier Plastics Inc.

- Wilkinson Containers Ltd.

- DS Smith Plc

- AST Kunststoffverarbeitung GmbH

- Scepter Canada Inc.

- California Plastics Products

- Ipackchem Group SAS

- Promens h

- Can-One Berhad

- SOTRALENTZ Packaging S.A.S

* List Not Exhaustive

Methodology

USDAnalytics employed a rigorous, multi-layered approach to assess the global Jerry Cans Market, combining primary interviews with industry leaders, manufacturers, and distributors with secondary research from regulatory frameworks, trade publications, corporate sustainability reports, and recent market developments. Our methodology focused on analyzing material innovations such as HDPE, bio-based resins, and recyclable plastics, as well as trends in collapsible and UN-rated jerry cans for hazardous and sensitive products. Market sizing and forecasts were developed by examining historical growth patterns, end-use industry demand, and regional adoption across North America, Europe, Asia-Pacific, and emerging markets. Competitive intelligence was derived from detailed evaluations of key players like Mauser Packaging Solutions, Greif Inc., Berry Global, and Sealed Air Corporation, emphasizing their product innovations, sustainability initiatives, and technology integration, including IoT-enabled smart jerry cans. Segmentation analysis covered material type, capacity, shape, and end-use industry, while specific attention was paid to regulatory compliance, circular economy initiatives, and emerging applications in EV battery coolants, emergency water storage, and chemical transport, ensuring a comprehensive, data-driven understanding of market dynamics and growth opportunities for industry professionals.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.