Laboratory Consumables Primary Packaging Market Overview: Key Industry Statistics

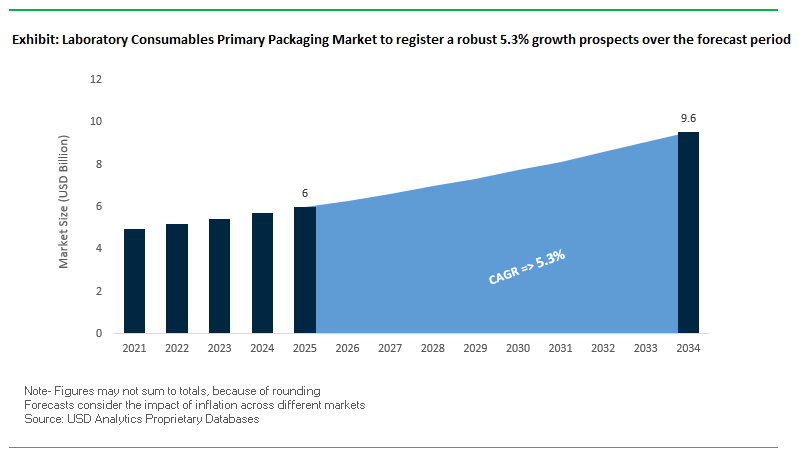

The Laboratory Consumables Primary Packaging Market is projected to grow from USD 6.0 billion in 2025 to USD 9.6 billion by 2034, registering a CAGR of 5.3%. This sector plays a mission-critical role in ensuring the sterility, safety, and integrity of lab consumables used across pharmaceuticals, diagnostics, biotechnology, and research. Packaging solutions such as vials, bottles, plates, and syringes not only safeguard product quality but also enable compliance with stringent global standards.

Key Insights for Industry Professionals

- Regulatory Compliance: Primary packaging must align with USP and Ph. Eur. standards, ensuring non-contamination and integrity of diagnostic and pharmaceutical consumables.

- Material Innovation: Shift toward Type I borosilicate glass and advanced polymers such as COC and HDPE, driven by chemical resistance and durability needs.

- Automation-Ready Formats: Growth of robotics and high-throughput labs fuels demand for geometrically precise vials and plates that integrate seamlessly with automated systems.

- Sustainability Imperatives: Rising use of PCR plastics and recyclable packaging solutions, aligning with ESG commitments and lab sustainability programs.

Market Analysis: Recent Developments in Laboratory Consumables Primary Packaging

The global laboratory consumables primary packaging industry is rapidly evolving, shaped by expansions, acquisitions, and sustainability commitments. In August 2025, SCHOTT AG announced an expansion in India for syringe and cartridge glass tubing, supporting surging demand for GLP-1 injectable drugs. The same month, Mauser Packaging Solutions joined the Association of Plastic Recyclers (APR), strengthening its alignment with global recyclability standards and advancing its role in the circular economy.

Consolidation continues to reshape the market landscape. International Paper completed the divestiture of five corrugated box plants in July 2025, part of regulatory requirements from its DS Smith acquisition. Earlier, in November 2024, Amcor acquired Berry Global, creating the largest global resin buyer and reinforcing scale advantages in packaging supply. Similarly, Smurfit Kappa and WestRock merged in October 2024, forming Smurfit WestRock, a paper-based packaging leader influencing lab supply chains.

Packaging innovation is also extending into the laboratory sector. In March 2025, Mauser Packaging Solutions expanded its stainless steel IBC line, enhancing durability for sensitive chemicals used in labs. Greif Inc., in September 2024, divested its containerboard business for USD 1.8 billion to strengthen its industrial packaging portfolio, including drums and jerry cans used in laboratory chemical storage.

Emerging Trends and Strategic Opportunities in the Laboratory Consumables Primary Packaging Market

Strategic Shift to Cyclo-Olefin Polymers (COP) and Copolymers (COC) for High-Value Applications

The laboratory consumables primary packaging market is experiencing a significant shift toward advanced polymer formulations, particularly Cyclo-Olefin Polymers (COP) and Copolymers (COC), driven by the need for extreme purity, chemical resistance, and clarity in biologics, cell and gene therapy, and advanced diagnostics applications. Traditional glass and standard plastics pose contamination risks; for instance, glass can release alkali ions, altering pH and compromising drug efficacy. COP/COC materials minimize extractables and leachables, ensuring product safety and purity. Beyond chemical stability, these polymers offer superior thermal performance, with West Pharmaceutical Services’ Daikyo Crystal Zenith® vials demonstrating exceptional break resistance at cryogenic temperatures. COP/COC also provide excellent optical clarity and low birefringence, essential for in-line inspections and diagnostic workflows, while their compatibility with sterilization methods, including NO2 processes, enhances safety for laboratory personnel handling sensitive samples. This trend underscores a strategic pivot toward advanced polymers that safeguard sample integrity and improve operational reliability.

Integration of Track-and-Trace and Anti-Counterfeiting Features Directly into Primary Packaging

Primary packaging is evolving into an intelligent, secure component of the laboratory supply chain, incorporating serialization, RFID, and tamper-evident features. Regulatory bodies worldwide, such as the European Medicines Agency (EMA) and India’s CDSCO, mandate serialization, requiring unique identifiers for pharmaceutical compliance. Companies like Körber Pharma integrate cryptoglyphs and serial codes directly into packaging lines to prevent counterfeiting. Additionally, cryogenic tubes with high-contrast 2D and 1D barcodes enable full lifecycle tracking, while RFID technology allows automated, hands-free inventory management, increasing visibility across labs and cold chains. Tamper-evident features, including specialized seals and smart labels that change upon opening, further enhance security. These innovations transform primary packaging from a passive container into an active, trackable, and secure solution, addressing both regulatory compliance and supply chain integrity concerns.

Development of Packaging for Cell and Gene Therapy (CAGT) Cold Chain Logistics

The explosive growth of cell and gene therapies has created an urgent need for primary packaging capable of withstanding cryogenic conditions ranging from −150°C to −196°C. Standard glass and plastics are prone to brittleness and fracture at these temperatures, posing risks to high-value, patient-specific therapies. Polymer-based solutions, including COP and COC vials from West Pharmaceutical Services and Schott Pharma, maintain container closure integrity for extended periods under ultra-low temperatures. Integration with cryogenic freezers and specialized transport systems, such as Cytiva’s VIA Freeze solutions, ensures compatibility with the cold chain infrastructure. Regulatory compliance and quality standards are paramount; packaging must be sterile, non-toxic, and resistant to degradation, while specialized components like cryogenic seals from Trelleborg Sealing Solutions support the extreme temperature requirements. This represents a high-value opportunity for innovation in durable, compliant, and purpose-built packaging for CAGT applications.

Standardization of Sustainable and Recyclable Plastic Resins for Lab Waste

Laboratories generate substantial plastic waste, creating a growing need for sustainable, recyclable primary packaging. The adoption of single-material, chemically resistant plastics, such as medical-grade polypropylene (PP), facilitates efficient recycling and aligns with institutional sustainability goals. Closed-loop initiatives and vendor take-back programs, exemplified by Thermo Fisher Scientific, allow laboratories to return used consumables for responsible disposal and recycling. Advanced resin formulations, such as Dow’s REVOLOOP™, offer mechanically recycled, high-quality plastics suitable for labware production. These innovations not only reduce environmental impact but also enable partnerships between resin producers and laboratory consumables manufacturers, creating a standardized, sustainable material ecosystem. The market potential for recyclable, chemically robust labware presents both environmental and economic benefits, supporting broader corporate ESG objectives while meeting regulatory expectations.

Competitive Landscape: Top Companies in Global Laboratory Consumables Primary Packaging

The competitive environment is shaped by companies with expertise in glass science, polymer technology, and life science services, all focusing on precision, compliance, and sustainability.

Thermo Fisher Scientific Inc.: Expanding automation-ready consumables

Thermo Fisher offers an extensive portfolio including reagent bottles, vials, and high-performance flasks. Its strength lies in automation-compatible packaging and digital traceability systems that meet the needs of high-throughput laboratories. By leveraging its global network and investing in R&D, Thermo Fisher positions itself as a single-source solution provider for regulated lab environments.

Corning Incorporated: Leading with specialty glass innovations

Corning’s life sciences division specializes in borosilicate vials, precision flasks, and high-purity bottles, known for outstanding chemical resistance and durability. The company is investing in bio-based plastic alternatives and efficiency improvements to meet sustainability goals. Corning’s “More Corning” strategy reinforces its focus on expanding presence in life sciences and advanced materials.

DWK Life Sciences: Precision in laboratory glassware and plasticware

DWK Life Sciences, with brands like DURAN®, WHEATON®, and KIMBLE®, provides a comprehensive line of glassware and consumable packaging. Its strength lies in certified, traceable products crucial for quality audits and regulatory compliance. DWK also offers custom fabrication and barcoding services, ensuring precision and traceability in laboratory workflows.

SCHOTT AG: Driving zero-defect pharmaceutical glass tubing

SCHOTT is a global pioneer in borosilicate glass tubing for vials, syringes, and cartridges, particularly critical for drug delivery systems. In August 2025, SCHOTT expanded in India to support biologics demand, reinforcing its leadership in GLP-1-related injectables. Its perfeXion quality system monitors over 100,000 data points per minute, ensuring near zero-defect manufacturing in pharma and lab packaging.

Avantor Inc.: Diversified solutions for life sciences packaging

Avantor delivers a broad portfolio spanning lab consumables, high-purity chemicals, and packaging solutions. Its focus on healthcare and biopharma positions it well for future growth. Avantor’s global network and innovation pipeline allow it to act as a single-source partner, particularly for regulated industries requiring high-quality packaging and consumables.

Merck KGaA: Innovating in eco-friendly lab packaging

Merck KGaA provides robust glass and plastic solutions for pharmaceutical, biotech, and diagnostics sectors. The company invests heavily in material science to enhance chemical compatibility and reduce environmental footprint. Its packaging is widely used for biologics, clinical reagents, and sensitive diagnostics, underscoring Merck’s role as a trusted global innovator in sustainable laboratory consumables packaging.

Laboratory Consumables Primary Packaging Market Share Insights

Plates Dominate Market Share by Product Type in the Laboratory Consumables Primary Packaging Industry

Plates, particularly multi-well microplates, account for 30% of the laboratory consumables primary packaging market in 2025, maintaining their leadership as the backbone of automation and high-throughput screening (HTS). Their ability to support parallel processing of hundreds to thousands of samples makes them indispensable in drug discovery, genomics, and diagnostics. This dominance reflects laboratories’ increasing reliance on miniaturization and efficiency to reduce costs while generating high-quality data. Tubes continue to play a critical role as universal consumables for mixing, centrifugation, and storage across research and clinical workflows. Vials, ampoules, and bottles collectively reinforce the market’s dependency on secure, sterile storage solutions, while bags and niche formats such as cryovials cater to advanced bioprocessing and emerging molecular techniques. The segmentation confirms that plates drive automation and throughput, while tubes and storage solutions provide universal and high-value support functions in laboratory operations.

Drug Discovery & Development Commands Market Share by Application in the Laboratory Consumables Primary Packaging Industry

Drug discovery and development is the largest application segment, capturing 30% of the laboratory consumables packaging market in 2025, due to its enormous demand for high-performance consumables that ensure reproducibility, sterility, and chemical compatibility. This segment is particularly value-intensive, as pre-clinical and translational research consumes massive volumes of microplates, assay tubes, reagent vials, and specialized storage formats. Diagnostics and sample collection also hold major shares, with hospitals, clinical labs, and point-of-care centers relying on standardized consumables like blood collection tubes, swabs, and urine cups. Microbiology and biochemical analysis drive steady demand from research institutes and industry labs, highlighting the foundational role of consumables in everyday scientific workflows. Meanwhile, emerging fields such as proteomics, synthetic biology, and environmental testing are pushing innovation in material science and specialized formats. This segmentation underscores how drug discovery secures the highest value share, while diagnostics and research applications sustain recurring, volume-driven demand across global laboratory ecosystems.

United States Laboratory Consumables Primary Packaging Market Driven by FDA Regulations and Advanced Sterile Packaging

The U.S. laboratory consumables primary packaging market is heavily influenced by regulatory compliance and innovations in sterile packaging technologies. The Food and Drug Administration (FDA), along with the Federal Trade Commission (FTC) through the Fair Packaging and Labeling Act (FPLA), enforces strict requirements for net contents, product identity, and manufacturer information, driving continuous product development. Growing demand in the pharmaceutical and medical sectors has fueled the adoption of advanced, aseptic and tamper-evident packaging systems, ensuring the integrity of sensitive laboratory and diagnostic products.

Innovations focus on sterile primary packaging, including advanced sealing technologies, to support point-of-care testing and diagnostics. The Environmental Protection Agency (EPA) is promoting climate-friendly materials under the $100 million “buy clean” initiative, creating opportunities for labeling and verification services. Rising demand for single-use pre-packaged laboratory consumables is further driving the market for high-performance, sterile packaging solutions.

European Union Laboratory Consumables Primary Packaging Market Expands Through Regulatory Compliance and Circular Economy Initiatives

The European Union laboratory consumables primary packaging market is experiencing significant growth due to stringent regulatory frameworks and sustainability trends. The Packaging and Packaging Waste Regulation (PPWR), effective February 2025, mandates standardized labeling and recycling protocols for all packaging by 2028, promoting eco-friendly and recyclable packaging solutions. Amendments under Regulation (EU) 2024/2865 enhance the classification, labeling, and packaging of chemicals, crucial for laboratory consumables.

The REACH regulation by the European Chemicals Agency (ECHA) imposes stricter limits on hazardous substances, increasing demand for compliant and safe primary packaging materials. Additionally, there is a growing trend toward incorporating recycled content in laboratory consumables, with advanced recycling technologies supporting the EU’s circular economy objectives and encouraging manufacturers to develop sustainable packaging solutions.

China Laboratory Consumables Primary Packaging Market Fueled by Smart Manufacturing and Anti-Counterfeiting Innovations

China’s laboratory consumables primary packaging market is rapidly evolving due to the government’s “14th Five-Year Plan”, which emphasizes digitalization and intelligent manufacturing. Automation and smart packaging technologies are becoming widespread, particularly in the life sciences and pharmaceutical sectors. Anti-counterfeiting and security features in packaging are critical for high-value laboratory products, ensuring authenticity and compliance.

Domestic manufacturers are expanding their capabilities to meet the growing demand for medical-grade, high-performance primary packaging, incorporating advanced barrier properties and security enhancements. These trends, combined with strong growth in the healthcare and research markets, are positioning China as a leading hub for technologically advanced laboratory consumables packaging.

India Laboratory Consumables Primary Packaging Market Accelerated by Domestic Manufacturing and Policy Support

India’s laboratory consumables primary packaging market is benefiting from government initiatives aimed at boosting domestic production and quality standards. The National Medical Device Policy 2023 emphasizes reducing imports while increasing local manufacturing of medical and laboratory consumables. Recent amendments to the Drugs Rules, 1945, mandate inclusion of excipient information on pharmaceutical packaging, creating opportunities for advanced labeling and primary packaging solutions.

India is also expanding its semiconductor and OSAT sectors under the India Semiconductor Mission (ISM), with programs like Chips to Startup (C2S) developing a skilled workforce. The Bureau of Indian Standards (BIS) has introduced mandatory certification for various plastic containers, further promoting high-quality and compliant packaging. Growing domestic demand across pharmaceuticals, diagnostics, and research labs is driving investments in sterile, high-performance laboratory packaging.

Japan Laboratory Consumables Primary Packaging Market Shaped by Chemical Safety Regulations and High-Performance Solutions

Japan’s laboratory consumables primary packaging market is influenced by chemical safety regulations and high-performance product development. Total migration testing for unregulated synthetic food packaging will be enforced from June 2026, impacting laboratory reagents and consumables. The Plastic Resource Circulation Promotion Law (2025) encourages reusable and compostable alternatives, stimulating demand for innovative packaging materials.

Companies like Catalent are expanding primary packaging capabilities to meet clinical supply needs, including high-speed blister packaging lines. The Japanese label industry, valued at $4.3 billion in 2024, demonstrates a shift toward functional and value-added labeling, with increased demand for durable, high-performance packaging in research and pharmaceutical sectors.

Brazil Laboratory Consumables Primary Packaging Market Driven by Regulatory Oversight and Sustainable Packaging Initiatives

Brazil’s laboratory consumables primary packaging market is being shaped by regulatory reforms and sustainability efforts. The National Health Surveillance Agency (Anvisa) introduced RDC n° 786/2023, establishing stringent rules for clinical laboratories and suppliers of laboratory consumables. New front-of-package labeling requirements, guided by the National Food and Nutrition Policy (PNAN) and Resolution No. 429/2020, are extending to laboratory products, ensuring compliance and safety.

Anvisa’s ongoing Regulatory Agenda for 2026–2027 and the country’s focus on risk assessment of chemical substances are driving manufacturers to implement self-declaration of conformity for laboratory consumables. Combined with trends in eco-friendly packaging, these initiatives are accelerating the adoption of sustainable, high-quality primary packaging solutions in Brazil’s growing laboratory and healthcare markets.

Laboratory Consumables Primary Packaging Market Report Scope

Laboratory Consumables Primary Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$6 Billion

|

|

Market Size (2034)

|

$9.6 Billion

|

|

Market Growth Rate

|

5.3%

|

|

Segments

|

By Product Type (Vials & Ampoules, Tubes, Bottles, Plates, Bags, Other Products), By Material (Plastics, Glass, Metals, Paper & Paperboard, Other Materials), By End-Use Industry (Pharmaceutical & Biotechnology, Healthcare, Research & Diagnostics, Chemical & Petrochemical, Academics & Government Research, Other End-Use Industries), By Application (Sample Collection, Drug Discovery & Development, Diagnostics, Microbiology, Biochemical Analysis, Other Applications)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Corning Incorporated, Thermo Fisher Scientific Inc., DWK Life Sciences, Greiner Bio-One International GmbH, Sarstedt AG & Co. KG, Gerresheimer AG, SCHOTT AG, Sartorius AG, Nippon Electric Glass Co., Ltd. (NEG), West Pharmaceutical Services, Inc., Becton, Dickinson and Company (BD), AptarGroup, Inc., Amcor plc, SGD Pharma, Catalent, Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Laboratory Consumables Primary Packaging Market Segmentation

By Product Type

- Vials & Ampoules

- Tubes

- Bottles

- Plates

- Bags

- Other Products

By Material

- Plastics

- Glass

- Metals

- Paper & Paperboard

- Other Materials

By End-Use Industry

- Pharmaceutical & Biotechnology

- Healthcare

- Research & Diagnostics

- Chemical & Petrochemical

- Academics & Government Research

- Other End-Use Industries

By Application

- Sample Collection

- Drug Discovery & Development

- Diagnostics

- Microbiology

- Biochemical Analysis

- Other Applications

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Laboratory Consumables Primary Packaging Market

- Corning Incorporated

- Thermo Fisher Scientific Inc.

- DWK Life Sciences

- Greiner Bio-One International GmbH

- Sarstedt AG & Co. KG

- Gerresheimer AG

- SCHOTT AG

- Sartorius AG

- Nippon Electric Glass Co., Ltd. (NEG)

- West Pharmaceutical Services, Inc.

- Becton, Dickinson and Company (BD)

- AptarGroup, Inc.

- Amcor plc

- SGD Pharma

- Catalent, Inc.

* List Not Exhaustive

Methodology

USDAnalytics employs a rigorous, integrated research methodology for the Laboratory Consumables Primary Packaging Market that combines targeted primary research (structured interviews with packaging engineers, QC leads, procurement heads, automation integrators, and regulatory affairs specialists across pharma, biotech, diagnostics and academic labs) with exhaustive secondary analysis of standards (USP, Ph. Eur.), patent filings, company disclosures, trade statistics, and technical whitepapers; market sizing and the 2025–2034 CAGR use a blended bottom-up approach (production capacity, unit volumes by product type vials, plates, tubes and automation adoption rates) validated by top-down demand modeling (drug discovery spend, diagnostic test volumes, and cold-chain logistics growth), while material- and technology-trend validation leverages lab performance benchmarks (extractables/leachables, cryo-fracture testing for COP/COC, and sterilization compatibility), competitive mapping (M&A, capacity expansions), and scenario analysis to quantify risks from regulatory shifts (serialization/UDI mandates, PPWR) and opportunities in CAGT cold-chain packaging and recyclable resin adoption delivering actionable guidance for R&D, procurement, operations and sustainability teams.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.