Methyl Isobutyl Carbinol Market 2025–2034: Mineral Processing Automation, Infrastructure-Led Solvent Demand, and Industry Restructuring Driving $770.6 Million Outlook at 4.7% CAGR

The Methyl Isobutyl Carbinol (MIBC) Market is projected to expand from $509.7 Million in 2025 to $770.6 Million by 2034, registering a CAGR of 4.7%. Growth is supported by steady demand from mineral flotation processes, architectural coatings, cement additives, and specialty solvent applications in electronics and automotive manufacturing. MIBC remains a critical frother in the beneficiation of copper, gold, and silver ores, where it enhances bubble stability and mineral recovery efficiency. At the same time, infrastructure expansion in emerging economies and the continued need for oxygenated solvents in high-performance coatings are sustaining baseline demand, despite margin pressures across the global chemical processing sector.

In March 2024, India unveiled a $120 billion National Infrastructure Pipeline program, directly stimulating regional demand for MIBC used in paints, coatings, and construction additives. In 2024, Eastman Chemical integrated advanced real-time monitoring and automated controls into its MIBC production lines to enhance yield stability and predictive maintenance efficiency. In September 2024, Mitsui Chemicals announced its withdrawal from non-core resin businesses to concentrate on Basic & Green Materials, where MIBC functions as a solvent and intermediate for electronics and automotive-grade materials. Throughout 2024 and 2025, Solvay achieved €191 million in cumulative cost savings, reallocating capital toward higher-growth specialty areas while optimizing legacy performance chemical lines.

Structural realignment accelerated in 2025 and early 2026. In April 2025, Dow delayed its Path2Zero net-zero polyethylene project, reflecting cautious capital expenditure conditions across the chemical industry. In late 2025, Sasol progressed with mothballing select U.S. and European plants to reduce exposure to underperforming commodity segments. In December 2025, Mitsui Chemicals and Idemitsu Kosan finalized consolidation of their Chiba Ethylene Complexes, strengthening feedstock security for downstream solvent production, including MIBC. In January 2026, Celanese announced price increases across engineered materials and solvent portfolios due to rising energy and feedstock costs, signaling margin pressure across the oxygenated solvent value chain. The same month, Dow launched its “Transform to Outperform” restructuring program, emphasizing AI-driven process simplification following a significant 2025 net loss. Concurrently, mining operators in late 2025 and 2026 increasingly adopted AI-based precision dosing systems paired with MIBC frothers to optimize flotation efficiency and minimize reagent waste, reinforcing the chemical’s strategic role in digitally enhanced mineral processing operations.

Market Size Outlook, 2021-2035.png)

Methyl Isobutyl Carbinol (MIBC) Market Trends and Opportunities

Trend: Strategic Diversification into High-Purity MIBC for Lithium-Ion Battery Electrolytes

The rapid build-out of global lithium-ion battery gigafactories is structurally redefining demand for methyl isobutyl carbinol, elevating it from a conventional industrial solvent to a mission-critical, high-purity specialty chemical. In electrolyte manufacturing, MIBC is increasingly used during the synthesis and purification of lithium hexafluorophosphate, where even trace moisture or metallic contaminants can accelerate electrolyte decomposition, reduce cycle life, and compromise safety in high-voltage cells. By 2025, leading electrolyte suppliers such as Targray and Enchem have standardized battery-grade specifications requiring ≥99.9% purity with moisture levels below 20 ppm. This tightening specification environment is compelling MIBC producers to deploy multi-stage fractional distillation and molecular-sieve dehydration systems to eliminate impurities such as mesityl oxide.

The scale of demand is equally transformative. By mid-2025, more than 400 GWh of new battery production capacity had been commissioned globally, creating a sustained pull for ultra-pure organic solvents used in electrolyte salts. The U.S. Department of Energy has identified electrolyte salt manufacturing as a priority beneficiary of the $2.8 billion Bipartisan Infrastructure Law funding aimed at domestic battery supply chain localization. Quality assurance is also becoming more stringent. A 2024–2025 technology audit by Agilent confirmed that ICP-MS is now the industry standard for verifying parts-per-billion metallic impurity thresholds in MIBC destined for EV and satellite battery applications, reinforcing barriers to entry for lower-grade suppliers.

Trend: Mine-Site Backward Integration and Dedicated Off-take Stability

In parallel with battery-driven diversification, the mining sector is reshaping MIBC procurement through backward integration and long-term offtake agreements. As a critical froth flotation reagent for copper and base metals, MIBC availability directly influences recovery rates and operating costs. To hedge against price volatility and geopolitical supply risks, Tier-1 miners are moving away from spot purchases toward strategic joint ventures and captive supply models.

A defining development occurred in December 2025, when the Government of Canada approved the merger of Anglo American and Teck Resources, forming a critical-minerals powerhouse targeting 690–750 kilotonnes of annual copper output. This combined entity is prioritizing industrial synergies that secure reagent supply chains, including MIBC, for operations across Chile and Peru. Sustainability requirements are reinforcing this shift. Mining majors such as Rio Tinto and BHP now mandate Life Cycle Assessment disclosure for all chemical reagents under their 2025 Sustainable Mining Plans, aligning MIBC sourcing with scope-3 emission reduction targets of 30% by 2030.

Operational efficiency is another driver. Findings presented at the 2025 Copper Flotation Innovations Summit indicate that AI-enabled reagent dosing systems can cut MIBC consumption by 12–15% while sustaining 93–96% recovery in low-grade ores. These systems require consistent, high-quality MIBC to perform reliably under automated control, further favoring long-term supply agreements over transactional buying.

Opportunity: Commercialization of Bio-Based MIBC for Decarbonized Supply Chains

Carbon pricing mechanisms and border adjustment policies are creating a compelling opportunity for bio-based MIBC. The EU Carbon Border Adjustment Mechanism and rising regional carbon taxes are eroding the cost competitiveness of petroleum-derived solvents, opening a pathway for MIBC synthesized from bio-acetone and renewable hydrogen. Feedstock availability is improving rapidly. In December 2025, the Indian Biogas Association announced that India’s biogas sector is on track for $4 billion in investment by 2026, enabling localized production of bio-alcohols and bio-ketones that serve as precursors for green MIBC.

Global chemical producers are aligning with this transition. Companies such as Solvay and Shell have accelerated Net-Zero 2050 strategies, with Shell reporting in September 2025 a $5–7 billion structural cost reduction program focused on lower-carbon product portfolios, including bio-derived industrial solvents. Regulatory incentives are amplifying adoption. The U.S. Environmental Protection Agency Safer Choice program and the EU Green Deal are fast-tracking certification for bio-based MIBC, allowing coatings and mining formulators to label finished products as sustainable-origin, a criterion now prioritized by roughly 60% of industrial procurement tenders.

Opportunity: MIBC-Based Low-VOC Solvent Blends for High-Performance Coatings

Tightening VOC regulations are expanding MIBC’s role in advanced coatings formulations. As the U.S. Environmental Protection Agency and European Chemicals Agency restrict aromatic solvents such as toluene and xylene, MIBC is gaining traction as a high-solvency, slow-evaporating component in low-VOC industrial and marine coatings. By November 2025, North American regulations capped VOC content at 450 g/L for industrial coatings, with limits as low as 50 g/L in California, pushing formulators toward high-solids systems where MIBC improves flow and leveling without breaching vapor-pressure thresholds.

Leading manufacturers are already commercializing this shift. In October 2025, PPG Industries and Sherwin‑Williams launched next-generation low-VOC industrial coatings in which MIBC is used to prevent surface skinning and ensure uniform film formation. These properties are critical for infrastructure projects targeting 10-plus-year durability benchmarks under Middle East Vision 2030 and large-scale APAC developments. Concurrently, the EU’s 2025 proposal to restrict cobalt-based driers is accelerating adoption of manganese-based catalysts such as Borchi Dragon, which depend on high-solvency carriers like MIBC to maintain fast drying and color stability. This convergence is creating a bundled growth opportunity for specialty solvent producers positioned at the intersection of low-VOC compliance and next-generation coating performance.

Methyl Isobutyl Carbinol Market Share and Segmentation Insights

Industrial Grade MIBC Dominates the Methyl Isobutyl Carbinol Market Driven by Large-Scale Mineral Processing Demand

Industrial grade methyl isobutyl carbinol (MIBC) accounted for 58.60% of the Methyl Isobutyl Carbinol Market share in 2025, reflecting its critical role in large-volume industrial applications, particularly mineral flotation processes. Industrial grade MIBC is widely used as a frothing agent in froth flotation systems, a key technique employed in the concentration of sulfide ores including copper, zinc, lead, and molybdenum, as well as coal beneficiation processes. In flotation circuits, MIBC stabilizes froth formation, improves bubble persistence, and enhances mineral separation efficiency, enabling recovery of valuable metal concentrates from low-grade ores. Because flotation operations consume large quantities of frothers, the cost efficiency and consistent performance characteristics of industrial grade MIBC make it the preferred grade for mining operators. Global mining output therefore directly influences MIBC consumption levels. In 2025, rising demand for base metals and energy transition minerals has strengthened mineral processing activity, reinforcing industrial grade MIBC as the dominant product category used across large-scale ore beneficiation and metallurgical processing operations.

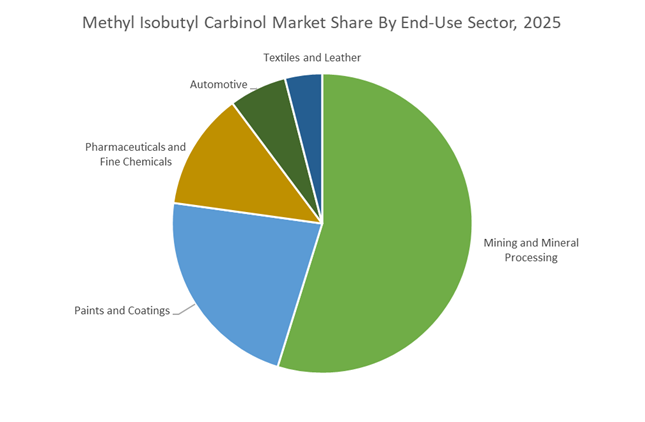

Mining and Mineral Processing Sector Leads Global MIBC Consumption

Mining and mineral processing accounted for 54.80% of the Methyl Isobutyl Carbinol Market share in 2025, establishing the sector as the primary consumer of flotation chemicals worldwide. Froth flotation remains the most widely used mineral concentration technique for base metal sulfide ores such as copper, zinc, and lead, as well as for coal cleaning operations, making MIBC an essential reagent within mineral beneficiation circuits. The effectiveness of MIBC as a flotation frother lies in its ability to produce stable yet easily breakable froth structures, improving mineral particle recovery and enhancing separation selectivity in flotation cells. In 2025, the mining sector has experienced renewed investment driven by rising demand for copper, nickel, and other energy transition metals required for electric vehicles, renewable energy systems, and power grid infrastructure. As copper demand increases across electrification technologies, mining operations are processing larger volumes of lower-grade ore, requiring more intensive flotation processes and higher consumption of flotation reagents such as MIBC to maintain efficient metal recovery.

Methyl Isobutyl Carbinol Market Competitive Landscape

The methyl isobutyl carbinol (MIBC) market in 2026 is driven by precision flotation chemistry, AI-enabled dosing systems, and high-flash-point solvent engineering. Demand is rising across mining, coatings, and lubricants, with innovation focused on salinity-tolerant frothers, VOC-compliant solvents, and high-performance evaporation kinetics.

Dow strengthens MIBC leadership through feedstock integration and high-performance solvent innovation

Dow Inc. is reinforcing its dominance in the MIBC market through its “Transform to Outperform” strategy, focusing on productivity, asset optimization, and sustainable feedstock integration. Its ISCC PLUS-certified operations at Freeport enhance its bio-circular solvent portfolio, aligning with global sustainability mandates. Dow’s strong ethylene supply agreement ensures long-term stability for C6 alcohol production, a key precursor for MIBC. The company is advancing R&D in electronic cleaning and photoresist applications through its Shanghai Cooling Science hub. Its MIBC remains a critical component in ZDDP synthesis, supporting high-performance automotive lubricants. Dow’s vertical integration and innovation pipeline position it as a leader in both mining frothers and specialty solvent applications.

Shell delivers high-purity MIBC for precision flotation in complex mining environments

Shell Chemicals is positioning itself as a leader in high-purity MIBC production, particularly for flotation processes in copper and molybdenum mining. Its technical-grade MIBC (≥98.5%) offers low water solubility and high boiling point, ensuring optimal performance in high-altitude and deep-sea mining conditions. Shell’s integration of pyrolysis oil into chemical production supports its circular chemicals strategy, reducing carbon intensity. Its strong logistics network in South America ensures reliable supply to major mining hubs. Expansion of intermodal capabilities in Asia-Pacific further strengthens its reach in emerging mineral processing markets. Shell’s focus on flotation efficiency and sustainable production reinforces its competitive positioning.

Celanese expands technical capabilities for mining-grade MIBC and industrial additive applications

Celanese Corporation is enhancing its position in the MIBC market through expanded R&D infrastructure and value-driven pricing strategies. The expansion of its Michigan Technology Center accelerates innovation in mining-grade frothers and industrial solvents. Its MIBC is widely used in lubricant additive production, particularly for flexible tubing systems in oil and gas extraction. Strategic price adjustments reflect its focus on high-performance chemical streams and cost optimization. Celanese is aligning its portfolio with “Responsible Growth,” emphasizing environmental compliance and operational efficiency. Its integration of specialty chemicals with engineered materials strengthens its presence across multiple industrial value chains.

Arkema diversifies MIBC applications across coatings, EV systems, and specialty chemicals

Arkema is leveraging its specialty materials expertise to position MIBC as a multifunctional solvent across coatings, lubricants, and electronics. Its MIBC plays a critical role in ZDDP synthesis for corrosion protection in EV thermal management systems. The company’s solvent properties, including optimized Hansen solubility parameters, make it ideal for nitrocellulose lacquers and high-gloss automotive coatings. Expansion of PVDF capacity in China supports its integration into battery and electronics supply chains. Arkema’s diversified market approach ensures stable demand across industrial, automotive, and consumer applications. Its focus on low-toxicity and high-performance solvents aligns with tightening VOC regulations.

Sasol advances low-carbon MIBC production through renewable energy integration and cost optimization

Sasol Limited is strengthening its position in the MIBC market through its International Chemicals Reset strategy, focusing on cost efficiency and sustainability. The company has secured over 1,200 MW of renewable energy capacity, enabling the production of lower-carbon “Green MIBC” with reduced Scope 2 emissions. Its high-purity oxygenated solvents are widely used in lubricants, corrosion inhibition, and biocidal applications in harsh industrial environments. Improved asset reliability at Secunda has driven higher production volumes and positive cash flow, supporting reinvestment in core operations. Sasol’s integrated production model and sustainability focus position it as a key supplier in the evolving MIBC landscape.

China: Green Beneficiation Policy and Digital Ore Optimization

China represents the most policy-driven growth engine for methyl isobutyl carbinol, anchored in non-ferrous metals modernization and resource efficiency. In September 2025, the Ministry of Industry and Information Technology jointly issued a non-ferrous industry work plan targeting 5% annual growth in sector value added through 2026. The directive elevates green and efficient beneficiation technologies, directly increasing demand for high-purity MIBC as a flotation frother in copper, aluminum, and polymetallic ore processing. Chemical suppliers are responding by upgrading purification and consistency controls to meet tighter froth selectivity and recovery benchmarks in large-scale concentrators.

Structural recycling mandates are compounding demand. China’s requirement to exceed 20 million metric tons of recycled metal output by 2026 is pushing mineral processors to recover value from complex electronic waste streams. This is accelerating development of specialized MIBC grades optimized for low-grade, mixed-feed ores. Parallel support for specialty industrial clusters under the 2025 machinery growth plan provides tax incentives and financing for SMEs producing high-performance flotation agents, reinforcing supply chain autonomy. By 2026, a national mineral resource data platform will deliver real-time ore analytics, enabling tailored MIBC formulations for difficult-to-process domestic deposits and tightening the feedback loop between mining data and reagent chemistry.

United States: Regulatory Certainty and Infrastructure-Led Solvent Demand

The United States MIBC market is characterized by regulatory clarity, critical minerals alignment, and steady downstream solvent consumption. In November 2025, the United States Environmental Protection Agency finalized an extension under the Toxic Substances Control Act for laboratories handling high-use industrial chemicals. The revised timeline allows non-federal facilities to implement Workplace Chemical Protection Programs for solvent-grade alcohols including MIBC, with initial monitoring deadlines extended to November 9, 2026. This provides compliance certainty while preserving continuity for high-volume users in mineral processing and industrial synthesis.

Strategic minerals policy is reinforcing demand fundamentals. The October 2025 U.S.–Australia rare earths agreement is expected to lift domestic refining capacity through 2026, supporting a stable market for flotation frothers in new extraction projects. The EPA’s designation of Methyl Isobutyl Carbinol 75% as a chemical of significant manufacturing commonality further underscores its role as a staple solvent across chemical synthesis, adhesives, and textile coatings. In parallel, steady U.S. housing activity projected into 2026 is sustaining MIBC use in architectural coatings and varnishes, where it functions as a latent solvent to improve flow and leveling.

South Africa: Low-Carbon Production and Mining Cost Discipline

South Africa’s role in the MIBC market is shaped by integrated production and export competitiveness. In September 2025, Sasol outlined a transformation at its Secunda Operations focused on enhancing gasifier performance. A destoning project scheduled for completion in the first half of 2026 will optimize feedstock quality for coal-to-liquids processing, improving yields and consistency of downstream alcohols including MIBC.

Energy transition initiatives are strengthening sustainability credentials. Sasol concluded power purchase agreements totaling 920 MW of renewable energy in 2025, lowering the carbon intensity of the Secunda complex by 2026. Concurrent mining cost optimization targets of R600 to R640 per ton through 2026 are critical for maintaining competitive export pricing of alcohol-based frothers supplied to global mining hubs. Together, operational efficiency and renewable integration position South African MIBC as a lower-carbon option for ESG-conscious mining operators.

Australia: Rare Earth Processing and Precision Flotation

Australia’s MIBC demand profile is increasingly linked to rare earth processing and technology-enabled mining. Following the 2025 strategic partnership with the United States, Australia is prioritizing regional refining projects that expand mid-stream processing capacity. These developments are driving localized demand for flotation chemicals, including MIBC, tailored to rare earth element extraction.

Technology adoption is refining reagent efficiency. Australian molybdenum operations are integrating AI and satellite monitoring into 2026 workflows, enabling predictive control of ore grade variability. This allows precise dosing of MIBC in flotation cells, reducing chemical waste while maintaining recovery rates. The combination of strategic mineral focus and digital mining is positioning Australia as a high-value, efficiency-driven market for specialized MIBC grades.

Chile and Peru: Copper Recovery and ESG-Aligned Reagent Selection

Chile and Peru remain structurally important to global MIBC consumption due to copper concentration. After water-related disruptions in 2025, copper output is projected to rebound by 4.7% in 2026, reaching 24.5 million tonnes. This recovery is expected to drive a sharp increase in MIBC consumption, given its role as the primary frother in copper sulfide flotation circuits.

Environmental policy is shaping product specifications. Governments in both countries are enforcing stricter environmental standards for 2026, compelling mining operators to transition toward biodegradable and higher-purity solvents. This is accelerating adoption of refined MIBC grades that offer improved environmental profiles compared with traditional branched-chain alcohols, aligning flotation performance with ESG compliance.

Country-Level Strategic Positioning in the Methyl Isobutyl Carbinol Market

Methyl Isobutyl Carbinol (MIBC) Market County Level Snapshot

|

Country / Region

|

Strategic Driver

|

Primary End Use

|

Policy or Industry Catalyst

|

Competitive Positioning

|

|

China

|

Green beneficiation and recycling

|

Non-ferrous flotation

|

MIIT work plan, recycling mandates

|

Scale with digital tailoring

|

|

United States

|

Regulatory certainty and infrastructure

|

Mining, coatings, solvents

|

TSCA extension, critical minerals deal

|

Stable high-volume demand

|

|

South Africa

|

Low-carbon integrated production

|

Mining frothers

|

Renewable PPAs, cost optimization

|

Sustainable export competitiveness

|

|

Australia

|

Rare earths and AI-enabled mining

|

Specialty flotation

|

U.S. partnership, digital mining

|

Precision reagent efficiency

|

|

Chile and Peru

|

Copper output recovery and ESG

|

Copper sulfide flotation

|

Environmental mandates

|

High-purity adoption

|

Methyl Isobutyl Carbinol (MIBC) Market Report Scope

Methyl Isobutyl Carbinol (MIBC) Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$509.7 Million

|

|

Market Size (2034)

|

$770.6 Million

|

|

Market Growth Rate

|

4.7%

|

|

Segments

|

By Grade (Technical Grade, Industrial Grade, Pharmaceutical Grade), By Application (Flotation Frothers, Solvents, Chemical Intermediates, Extraction Solvents), By End-Use Sector (Mining and Mineral Processing, Paints and Coatings, Pharmaceuticals and Fine Chemicals, Automotive, Textiles and Leather)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Shell Chemicals, Sasol, Arkema, Celanese, Dow, Eastman Chemical, Incitec Pivot, Mitsui Chemicals, KH Neochem, Zhejiang Kehong Chemical, Union Carbide, Solvay, Lonza, Mitsubishi Chemical, Clariant

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Methyl Isobutyl Carbinol Market Segmentation

By Grade

- Technical Grade

- Industrial Grade

- Pharmaceutical Grade

By Application

- Flotation Frothers

- Solvents

- Chemical Intermediates

- Extraction Solvents

By End-Use Sector

- Mining and Mineral Processing

- Paints and Coatings

- Pharmaceuticals and Fine Chemicals

- Automotive

- Textiles and Leather

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Methyl Isobutyl Carbinol Market

- Shell Chemicals

- Sasol

- Arkema

- Celanese

- Dow

- Eastman Chemical

- Incitec Pivot

- Mitsui Chemicals

- KH Neochem

- Zhejiang Kehong Chemical

- Union Carbide

- Solvay

- Lonza

- Mitsubishi Chemical

- Clariant

*- List not Exhaustive