Microcellular Plastics Market Overview: Size, CAGR, and Strategic Insights

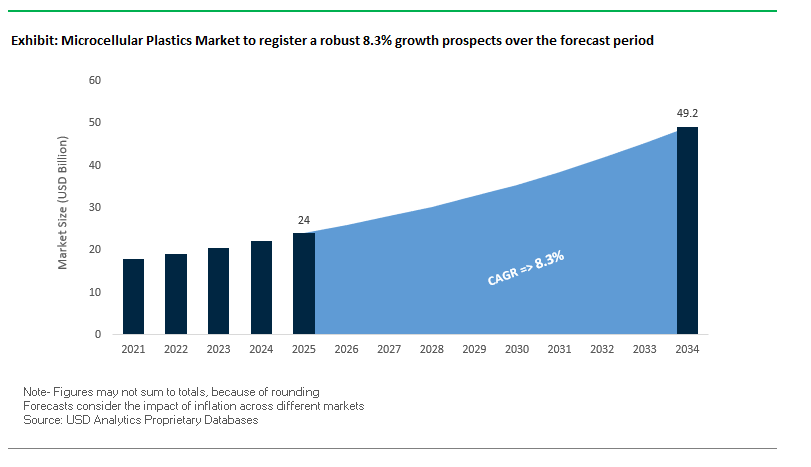

The global Microcellular Plastics Market is projected to grow from $24 billion in 2025 to $49.2 billion by 2034, at a CAGR of 8.3%. This growth is primarily driven by the increasing adoption of lightweight plastics in automotive and aerospace sectors, rising demand for enhanced material properties, and a global push toward sustainable manufacturing. Microcellular plastics offer foamed polymer structures that reduce part weight by up to 40%, while improving flatness, warpage, thermal insulation, and acoustic damping.

Key Insights for Industry Professionals:

- Lightweighting and carbon reduction: Microcellular plastics contribute to fuel efficiency and reduced emissions in automotive and aerospace applications.

- Enhanced material performance: Microscopic voids in the polymer matrix improve toughness, dimensional stability, and acoustic properties.

- Manufacturing efficiency: Microcellular injection molding reduces cycle times by up to 50%, lowering energy consumption and production costs.

- Eco-friendly processing: Use of nitrogen (N₂) and carbon dioxide (CO₂) as physical blowing agents avoids harmful VOC emissions.

- Cross-industry adoption: Applications span automotive interiors, consumer electronics, and sustainable packaging, reflecting versatility and innovation potential.

Microcellular Plastics Market Analysis: Recent Industry Developments

The microcellular plastics industry continues to evolve through advanced material innovations and sustainable manufacturing trends. In August 2025, a Nano Letters study introduced an inhibitor-modified atomic layer deposition (ALD) technique for ultrathin iridium and platinum films, demonstrating potential impacts on future microcellular plastic formulations for electronics. Additionally, August 2025 saw the development of liquid-metal printing for flexible ITO films, offering enhanced transparency and pliability for touchscreens compared to traditional methods.

By July 2025, metallized film converters invested in wider, faster coating lines to achieve economies of scale, while material innovators emphasized recycling-ready structures. The same month highlighted the substitution of aluminum foil with lightweight metallized films, reflecting a trend toward cost-effective, durable materials. In June 2025, copper-based metallic films gained traction, driven by high-power battery packs and 5G electronics, demonstrating the convergence of microcellular plastics with advanced electronics applications.

Strategic acquisitions and sustainable packaging developments have also shaped the market. In April 2025, Mondi Plc acquired Schumacher Packaging’s Western European assets, enhancing its high-performance sustainable packaging portfolio. Earlier, in March 2025, Mondi reported strong results from its flexible packaging segment, including micro-perforated and metallized films. In February 2025, Mondi and Proquimia introduced paper-based stand-up pouches for dishwashing tabs, exemplifying eco-friendly alternatives to conventional plastic packaging.

Strategic Trends and Growth Opportunities in the Microcellular Plastics Market

Adoption of Microcellular Foaming for Lightweighting in Electric Vehicle (EV) Components

The microcellular plastics market is being propelled by the automotive sector’s aggressive transition to electrification, where lightweighting has become a strategic necessity to counterbalance heavy EV battery packs. Microcellular foaming, particularly via the MuCell® process, is increasingly applied in dashboards, seat frames, door panels, and structural elements, reducing part weight by 10% to 30% without compromising mechanical integrity.

Lightweighting directly enhances EV efficiency: every 100 kg reduction in vehicle mass extends range and lowers energy consumption. The process also supports sustainability, as reduced material consumption cuts CO₂ emissions by 125–1,200 kg per ton of plastic produced, depending on the polymer. Beyond weight reduction, the MuCell® process delivers manufacturing advantages including 15–50% shorter cooling and packing times, lower energy usage per part, and elimination of sink marks or warpage. This combination of performance, productivity, and sustainability is establishing microcellular foaming as a core enabler of EV component design and next-generation mobility platforms.

Shift Towards Supercritical CO₂ as the Primary Physical Blowing Agent

Environmental regulations on volatile organic compounds (VOCs) and greenhouse gas emissions are accelerating the shift from chemical blowing agents to supercritical CO₂ (scCO₂) and nitrogen (N₂). This transition is reshaping the microcellular plastics market by offering a non-toxic, non-flammable, recyclable, and VOC-free solution that aligns with global sustainability mandates.

Studies in materials science highlight that scCO₂-based foaming achieves refined and uniform cell morphology, with average cell sizes reduced to

20.9 µm and >100% increases in cell density. This results in plastics with enhanced mechanical strength, dimensional stability, and impact resistance compared to conventional foams. Moreover, scCO₂ not only eliminates harmful additives but also improves workplace safety during production. As regulatory compliance converges with technical superiority, supercritical CO₂ is emerging as the industry standard for environmentally responsible microcellular plastics manufacturing.

Development of Microcellular Foams for High-Performance Thermal Insulation

Rising global demand for energy-efficient construction materials, appliances, and cold-chain packaging is unlocking opportunities for microcellular plastics with exceptionally low thermal conductivity values (<30 mW/m·K). The fine, uniform cellular structure of these foams minimizes convective heat transfer, making them superior insulators compared to traditional polymer foams.

Research on advanced foams highlights that polyetherimide (PEI) nanofoams can achieve thermal conductivities as low as 0.015 W/m·K, placing them among the most effective insulating polymers. This property is particularly valuable in refrigerators, freezers, fisheries logistics, and building insulation, where energy efficiency is a critical performance metric. By reducing heat transfer, microcellular plastics lower operational energy consumption while aligning with global energy conservation policies. Manufacturers investing in this segment are well-positioned to capture demand in both developed and emerging markets for sustainable thermal insulation solutions.

Application in Biomedical Scaffolds and Advanced Wound Care

The unique porous morphology of microcellular plastics—high porosity, interconnected pore networks, and tunable surface area-to-volume ratios—creates a promising frontier in biomedical applications. In tissue engineering, scaffolds fabricated using microcellular foaming combined with particle leaching techniques have shown excellent potential in supporting cell adhesion, growth, and tissue regeneration. For example, TPU scaffolds engineered with high pore density provide the structural environment required for bone and soft tissue repair.

The ability to precisely control pore geometry, size, and density enables manufacturers to design scaffolds with customized biomechanical properties, critical for applications in regenerative medicine. Furthermore, the same characteristics make microcellular foams highly suitable for advanced wound dressings, where they can effectively absorb exudate while maintaining a moist healing environment. These innovations address unmet needs in healthcare, especially as demand for chronic wound management and regenerative therapies rises globally.

Competitive Landscape: Leading Players in the Global Microcellular Plastics Market

The microcellular plastics industry is dominated by companies leveraging advanced polymer technologies, sustainable solutions, and lightweighting expertise. These industry leaders provide innovative, high-performance materials across automotive, aerospace, electronics, and packaging applications, establishing strong global market positions.

Trexel, Inc.: Pioneering MuCell® Technology for Lightweighting

Trexel is a leading provider of MuCell® microcellular foaming technology, using supercritical N₂ and CO₂ to produce foamed plastic parts. The company integrates its technology with Industry 4.0 automation, enhancing process stability and data-driven production. Trexel’s solutions are widely applied in automotive interiors such as dashboards and door panels, achieving 10–30% weight reduction and supporting carbon reduction goals.

BASF SE: Innovating NVH Solutions with Cellasto® Elastomers

BASF is a global chemical company known for its Cellasto® microcellular polyurethane (MCU) elastomers, which provide noise, vibration, and harshness (NVH) reduction in automotive applications. In February 2025, BASF India initiated a new Cellasto® production facility in Dahej, targeting the growing Indian automotive market. BASF emphasizes localized manufacturing, innovative NVH solutions, and sustainable practices to enhance vehicle performance and efficiency.

Evonik Industries AG: Advancing Sustainable High-Performance Polymers

Evonik is a specialty chemicals company offering tailored polymer additives and high-performance materials for the microcellular plastics industry. The company focuses on sustainable, energy-efficient solutions, leveraging R&D to optimize lightweighting, durability, and processability. Evonik collaborates closely with customers, providing technical support and product development services to enhance microcellular plastics manufacturing outcomes.

SABIC: Driving Circular Economy with Versatile Polymer Resins

SABIC is a global leader in chemical and polymer production, providing base resins for microcellular plastics, including PP, PE, and PC, along with specialty additives. The company focuses on circular economy initiatives, integrating recycled materials and high-performance products into its portfolio. SABIC continues to invest in innovative technologies and sustainable product development, reinforcing its leadership in lightweight, eco-friendly plastics.

LyondellBasell Industries: Delivering High-Quality Polymers for Microcellular Applications

LyondellBasell is a multinational specializing in plastics and petrochemicals, offering a broad range of polymer materials for microcellular foaming. The company’s strengths lie in its global manufacturing footprint and reliable, consistent products, critical for microcellular plastics production. LyondellBasell focuses on lightweight, durable, and recyclable solutions, investing in technology and product development to meet rising demand for sustainable high-performance materials.

Microcellular Plastics Market Share Insights

Polyurethane Leads Market Share by Material Type in the Microcellular Plastics Industry

Polyurethane (PU) accounts for 28% of the microcellular plastics market, making it the most widely adopted material due to its unmatched versatility in both flexible and rigid foam structures. Its dominance stems from its extensive use in automotive interiors, seating, dashboards, and insulation systems, where energy absorption, cushioning, and thermal performance are critical. In construction, PU-based microcellular foams are used in spray insulation and panels to meet global energy efficiency standards. Its adaptability to different densities and performance requirements allows it to serve diverse industries from consumer comfort products to high-performance industrial insulation, securing its leadership position. While polypropylene is gaining momentum as a sustainable, recyclable alternative, polyurethane maintains its market lead because of its performance range, durability, and established supply chain across automotive, building, and consumer sectors.

Automotive & Transportation Hold the Largest Market Share by Application in the Microcellular Plastics Industry

Automotive and transportation applications lead with 30% share of the microcellular plastics market, driven by the global push for lightweighting to reduce fuel consumption and emissions. Microcellular foams deliver weight reductions of up to 20–30% compared to solid plastics while maintaining structural integrity, making them ideal for door panels, seat cushions, dashboards, under-the-hood parts, and even structural reinforcements. The segment’s dominance is further supported by regulatory pressures such as the EU’s CO₂ emissions targets and the rising adoption of electric vehicles (EVs), which demand lighter components to extend driving range. Automakers’ emphasis on cost savings, recyclability, and safety compliance positions microcellular plastics as an integral material in next-generation mobility. This ensures the automotive and transportation sector remains the primary consumer of these advanced lightweight foams.

United States: Innovation in Microcellular Plastics for Lightweighting and Sustainability

The United States microcellular plastics market is advancing rapidly with a strong emphasis on technological innovation. Research at institutions such as the University of Washington and the Indian Institute of Technology, Delhi (through collaborative studies) is paving the way for high-performance microcellular and nanocellular foams with finer and more uniform cell structures. These advances significantly improve strength-to-weight ratios and impact resistance, making them ideal for industries demanding high-performance lightweight materials. A notable industry shift is also toward eco-friendly blowing agents like supercritical CO₂ and nitrogen, which align with sustainability goals while reducing reliance on chemical agents.

Corporate activity is strong, highlighted by Silgan Holdings’ acquisition of Gateway Plastics in October 2021, expanding its dispensing closures and microcellular plastics portfolio. Demand is particularly robust in the automotive and transportation industries, where lightweighting vehicle parts enhances fuel efficiency. Beyond this, the healthcare and electronics sectors are key growth drivers, requiring specialized foams for medical devices and precision electronic components. This convergence of sustainability, innovation, and strategic investment positions the U.S. as a leader in the global microcellular plastics market.

Germany: Regulatory Pressure and Advanced Foaming Technologies Fuel Growth

Germany’s microcellular plastics market is deeply influenced by the EU Circular Economy Action Plan, which mandates recyclability and the use of high-value materials. This regulation is pushing manufacturers to innovate with eco-friendly foams that align with circular economy principles. German companies have become global leaders in foaming and material-shaping technologies, combining technical expertise with sustainability-focused design. A prime example is Borealis’ €100 million investment in a new Burghausen production line, tripling capacity for recyclable foam-based polypropylene targeted at automotive, consumer goods, and construction markets.

Germany’s leadership in research and development further strengthens its global influence. With 75 research institutes collaborating with industry, the country operates as a hub for innovation across the plastics value chain. Key applications include the automotive industry, where microcellular plastics are applied in parts like jounce bumpers and coil spring isolators, improving performance and fuel economy. The building and construction sector is another major demand driver, using these foams for insulation and energy-efficient designs. By combining regulatory rigor, research leadership, and corporate investment, Germany sets the benchmark for advanced microcellular plastics development in Europe.

China: Government Support and Automation Power Market Expansion

China’s microcellular plastics market is growing rapidly, driven by governmental initiatives that support high-end manufacturing and sustainable materials adoption. With the “dual-carbon” targets and policies such as the Opinions on Further Strengthening the Control of Plastic Pollution, China is promoting innovative lightweight materials that address both environmental and performance requirements. This regulatory push is creating favorable conditions for the adoption of microcellular plastics across automotive, consumer goods, and construction sectors.

On the production side, Chinese manufacturers are investing in automation and artificial intelligence (AI) to enhance efficiency and ensure consistent quality in large-scale operations. Demand is particularly strong in the automotive industry for lightweight vehicle components, in electronics for sound insulation and housings, and in construction for durable insulation materials. While specific company-level investments are less transparent, the combined effect of government backing, rapid industrialization, and sectoral growth clearly indicates substantial capital flow into the market. As China scales both domestic capacity and technological sophistication, it is emerging as one of the most influential players in the Asia-Pacific microcellular plastics landscape.

Japan: Industry-Government-Academia Partnerships Drive Recycled Plastics Innovation

Japan’s microcellular plastics market is distinguished by collaborative initiatives between government, academia, and industry to promote sustainable materials, especially in the automotive sector. In late 2024, the Japanese government launched the Industry-Government-Academia Consortium for Developing a Market for Recycled Plastics in Automotive Applications, which aims to address challenges in sourcing, processing, and deploying recycled materials. This collaboration reinforces Japan’s global reputation for precision manufacturing and sustainable innovation.

Technological advancements are also evident through partnerships between automakers and material companies. For example, Honda and Sumitomo Chemical developed a polypropylene-based recycled plastic with high durability and superior appearance quality, now used in vehicle front grilles. Japanese manufacturers are heavily leveraging microcellular plastics for lightweighting strategies, reducing overall vehicle weight to meet fuel efficiency and environmental regulations. While automotive remains the dominant application, microcellular plastics are increasingly used across interior and exterior vehicle components, from dashboards to bumpers, reinforcing Japan’s focus on both performance and sustainability in material innovation.

Microcellular Plastics Market Report Scope

Microcellular Plastics Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$24 Billion

|

|

Market Size (2034)

|

$49.2 Billion

|

|

Market Growth Rate

|

8.3%

|

|

Segments

|

By Material Type (PE, PP, PU, PVC, PS, PC, Others), By Application (Automotive & Transportation, Building & Construction, Packaging, Electrical & Electronics, Healthcare, Others), By End-User (Automotive Manufacturers, Construction Companies, Electronics Manufacturers, Packaging Companies, Medical Device Companies, Consumer Goods Manufacturers)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, LyondellBasell Industries N.V., EVCO Plastics, ExxonMobil Corporation, Saudi Basic Industries Corporation (SABIC), Dow Inc., Covestro AG, Solvay S.A., RTP Company, Trexel, Inc., INEOS, Trinseo S.A., Formosa Plastics Corporation, TotalEnergies, INOAC CORPORATION

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Microcellular Plastics Market Segmentation

By Material Type

- PE

- PP

- PU

- PVC

- PS

- PC

- Others

By Application

- Automotive & Transportation

- Building & Construction

- Packaging

- Electrical & Electronics

- Healthcare

- Others

By End-User

- Automotive Manufacturers

- Construction Companies

- Electronics Manufacturers

- Packaging Companies

- Medical Device Companies

- Consumer Goods Manufacturers

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Microcellular Plastics Market

- BASF SE

- LyondellBasell Industries N.V.

- EVCO Plastics

- ExxonMobil Corporation

- Saudi Basic Industries Corporation (SABIC)

- Dow Inc.

- Covestro AG

- Solvay S.A.

- RTP Company

- Trexel, Inc.

- INEOS

- Trinseo S.A.

- Formosa Plastics Corporation

- TotalEnergies

- INOAC CORPORATION

* List Not Exhaustive

Methodology

USDAnalytics applies a rigorous, multi-layered research methodology to provide industry professionals with comprehensive insights into the global Microcellular Plastics Market. Our approach integrates primary research through interviews with polymer scientists, automotive and aerospace engineers, packaging specialists, and key manufacturing stakeholders, complemented by secondary research from corporate filings, industry reports, scientific publications, patent literature, and regulatory frameworks. We analyze critical market drivers, including lightweighting for EV components, supercritical CO₂-based foaming, thermal insulation applications, and biomedical scaffold innovations, while evaluating material-specific performance, production efficiency, and sustainability impacts. Advanced forecasting models are employed to assess regional market trends, including North America, Europe, and Asia-Pacific, alongside competitive dynamics involving leaders such as Trexel, BASF, SABIC, and LyondellBasell. Strategic initiatives, such as corporate acquisitions, R&D investments, and process automation, are assessed to understand technological adoption and market growth. This methodology ensures USDAnalytics delivers accurate, data-driven insights on emerging opportunities, market transformations, and technological innovations, equipping professionals to make informed strategic and investment decisions in the microcellular plastics industry.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.