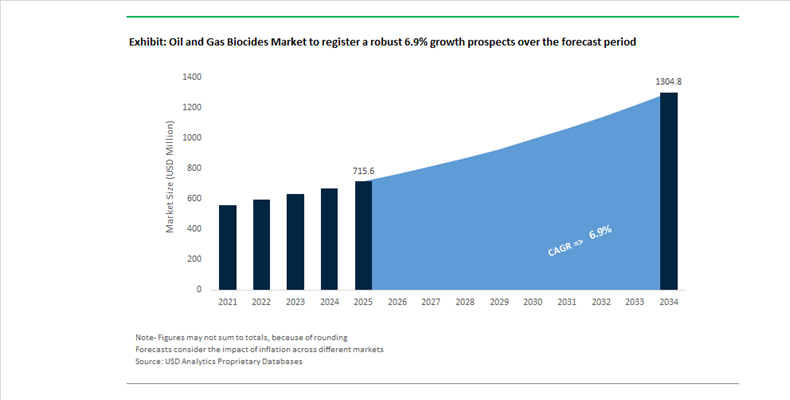

Oil and Gas Biocides Market Valued at $715.6 Million in 2025, Projected to Reach $1,304.6 Million by 2034 at 6.9% CAGR Driven by Water Reuse and Digital Chemical Management

The Oil and Gas Biocides Market is valued at $715.6 Million in 2025 and is forecast to reach $1,304.6 Million by 2034, expanding at a CAGR of 6.9%. Growth is anchored in the rising complexity of microbial control across upstream production, hydraulic fracturing, midstream pipelines, and refinery water systems. Increased recycling of produced water, souring risks from sulfate-reducing bacteria, and stricter corrosion management protocols are elevating demand for both oxidizing and non-oxidizing oilfield biocides. Operators in shale basins are prioritizing high-efficacy microbial control solutions to prevent biofilm formation, hydrogen sulfide generation, and microbiologically influenced corrosion (MIC), which collectively drive unplanned downtime and asset degradation.

In July 2025, SLB finalized its acquisition of ChampionX Corp, consolidating a major share of the oilfield chemical and specialty biocides portfolio under a single global production optimization platform. The integration strengthens SLB’s ability to deploy digital monitoring, reservoir analytics, and chemical dosing systems in tandem. To secure regulatory approval in the UK and Norway, targeted divestments and licensing arrangements were executed for specific chemical technologies. In Q4 2025, DuPont transitioned its reporting structure to “Healthcare & Water Technologies,” consolidating industrial microbial control assets and positioning oil and gas water treatment biocides as a strategic growth segment.

Technology innovation accelerated in 2024 and 2025. Solenis completed the global integration of Diversey operations during 2024 and 2025, expanding its antimicrobial and refinery water hygiene solutions portfolio. In early 2024, Solenis recognized Repsol’s Cartagena Industrial Complex for implementing advanced water treatment and optimized biocide strategies that reduced chemical consumption and enhanced water recycling efficiency. In parallel, Marathon Petroleum’s Los Angeles Refinery received the 2024 Solenis Sustainability Award for deploying advanced biofilm detection and ClearPoint™ monitoring systems, reducing downtime and lowering biocide overdosing.

Digitalization is reshaping dosing accuracy and corrosion prevention economics. In late 2025, companies such as Ecolab and Solenis rolled out AI-driven predictive dosing systems that analyze real-time microbial activity in pipelines and storage tanks. These platforms dynamically adjust biocide injection rates, minimizing excess chemical use while maintaining microbial thresholds. During 2024 and 2025, operators in the Permian and Eagle Ford basins increased adoption of oxidizing biocides including chlorine dioxide to treat high-organic-load recycled produced water streams.

Sustainability and regulatory navigation remain central to market dynamics. In November 2025, BASF and ExxonMobil signed a joint development agreement to scale methane pyrolysis technology, lowering the carbon intensity of precursor chemicals used in specialty formulations including high-performance oilfield biocides. In September 2024, Ramboll acquired SCC Scientific Consulting to strengthen regulatory advisory capabilities under frameworks such as the EU Biocidal Products Regulation. In mid-2025, academic research highlighted plant-based and essential-oil-derived antimicrobial systems designed to replace glutaraldehyde and THPS in environmentally sensitive offshore assets, targeting substantial reductions in anodic reaction inhibition while maintaining microbial suppression.

Oil and Gas Biocides Market Trends and Opportunities

Trend: Mandated Transition to Biodegradable Green Biocide Programs in Offshore and Marine Operations

The oil and gas biocides market is undergoing a structural transformation as environmental compliance shifts from voluntary stewardship to enforceable regulation. Offshore operators are now compelled to replace legacy biocides such as glutaraldehyde and THPS with biodegradable, low-toxicity alternatives that meet increasingly stringent discharge and biodegradation standards. The enforcement of the U.S. Vessel Incidental Discharge Act has materially tightened allowable limits for biocidal residues released through offshore support vessel ballast water and deck runoff. As a result, operators in the Gulf of Mexico have rapidly restructured their chemical programs, driving a measurable shift toward biocides that align with Environmentally Acceptable Lubricant classifications and Appendix A biodegradability benchmarks.

In parallel, the North Sea continues to set the global benchmark for chemical substitution through the OSPAR Harmonised Mandatory Control System. By late 2025, leading operators had accelerated the phase-out of nitrogen-based and poorly biodegradable biocides, driven by biodiversity protection goals and heightened scrutiny of offshore discharges. Oxidizing biocides such as peracetic acid are gaining share because they deliver effective microbial control while decomposing into benign byproducts, reducing long-term environmental persistence. Independent benchmarking by industry bodies confirms that modern green biocides now achieve microbial kill rates exceeding 90% against sulfate-reducing bacteria while cutting aquatic toxicity profiles by roughly 40% compared to formaldehyde-releasing agents. This convergence of regulatory pressure and proven field performance has repositioned biodegradable biocides from niche alternatives to default specifications for offshore oil and gas operations.

Trend: Rising Biocide Intensity from Mature Field Waterflooding and Chemical EOR

A second powerful demand driver is the resurgence of secondary and tertiary recovery programs as operators seek to maximize recovery from aging assets. Waterflooding and chemical enhanced oil recovery significantly increase the volume of injected water, creating ideal conditions for microbial growth, reservoir souring, and Microbial Induced Corrosion. As production portfolios mature, biocide consumption is increasingly viewed as a capital protection measure rather than a routine operating expense. Large-scale water injection projects sanctioned in the Gulf of Mexico illustrate this shift, where continuous-dose biocide programs are designed into field development plans years ahead of first water injection.

Deepwater and high-pressure, high-temperature reservoirs further amplify this requirement. Expansion of deepwater hubs and reinvestment in mature offshore assets have elevated demand for thermally stable biocides that remain effective at extreme depths and temperatures. Non-oxidizing chemistries such as DBNPA and advanced quaternary ammonium compounds are being specified to withstand harsh downhole conditions without rapid degradation. With industry estimates attributing approximately 2.5 billion dollars in annual global losses to MIC, operators in regions such as the Middle East and the Permian Basin are increasing biocide budgets to protect pipelines, injection systems, and production equipment. This trend structurally links biocide demand to long-life asset integrity strategies rather than short-term production cycles.

Opportunity: Real-Time Automated Biocide Dosing and Intelligent Monitoring Systems

Digitalization is creating a high-value opportunity to redefine how biocides are applied across upstream and midstream infrastructure. Operators are moving away from conservative slug dosing toward real-time, demand-based treatment enabled by IoT-enabled injection skids and advanced sensing technologies. The growing deployment of automated chemical injection systems integrated with ATP sensors allows operators to detect microbial activity instantaneously and trigger precise dosing responses. This shift directly addresses both environmental compliance and cost efficiency by minimizing chemical overuse.

Field trials conducted in 2025 demonstrate that AI-enabled dosing platforms can reduce biocide consumption by 15 to 20 percent while maintaining effective microbial control. By continuously analyzing data from downhole probes and produced water streams, operators are able to maintain minimum inhibitory concentrations rather than relying on periodic over-treatment. The next phase of this opportunity lies in predictive analytics. Machine learning models are being developed to forecast sulfate-reducing bacteria blooms based on variables such as temperature, flow rates, and nutrient availability. These predictive capabilities allow proactive intervention before biofilms form, reducing unplanned downtime and extending the operational life of corrosion-sensitive assets.

Opportunity: Multi-Functional Biocide and Corrosion Inhibitor Blends for Shale Operations

Unconventional shale plays present a distinct opportunity for integrated chemical solutions due to logistical constraints and high operational intensity. Operators in basins such as the Permian and Eagle Ford are increasingly favoring one-drum chemical strategies that combine microbial control and corrosion protection in a single formulation. Multi-functional biocide and corrosion inhibitor blends are being engineered specifically for high-salinity produced water environments common in hydraulic fracturing.

These synergistic formulations simplify supply chains, reduce onsite storage requirements, and lower handling risks while maintaining performance across multiple functions. Regulatory pressure to improve fracturing efficiency and reduce emissions has also driven the development of biocides that are fully compatible with friction reducers and other completion chemicals. At the same time, produced water recycling has become a strategic priority, with more than half of North American rigs now reusing water in subsequent fracturing stages. This has sharply increased demand for fast-acting oxidizing biocides capable of rapidly sterilizing recycled water to prevent downhole souring in newly fractured wells. Together, these dynamics position multi-functional biocide packages as a high-growth, value-added segment within the oil and gas biocides market.

Oil and Gas Biocides Market Share and Segmentation Insights

Non-Oxidizing Biocides Lead Oilfield Microbial Control with Broad-Spectrum Performance

Non-oxidizing biocides accounted for 68.40% of the Oil and Gas Biocides Market by type in 2025, driven by their superior compatibility with oilfield chemicals and long-lasting antimicrobial performance in harsh environments. Common chemistries such as glutaraldehyde, THPS, quaternary ammonium compounds, and DBNPA are widely used across drilling fluids, hydraulic fracturing, and produced water treatment systems. These biocides effectively control sulfate-reducing bacteria and biofilm formation, preventing corrosion and reservoir souring. Their stability under varying temperature and salinity conditions supports continuous application across upstream operations. In 2025, THPS is gaining preference due to its rapid biodegradability and environmental compliance, particularly in offshore and environmentally sensitive oilfield operations.

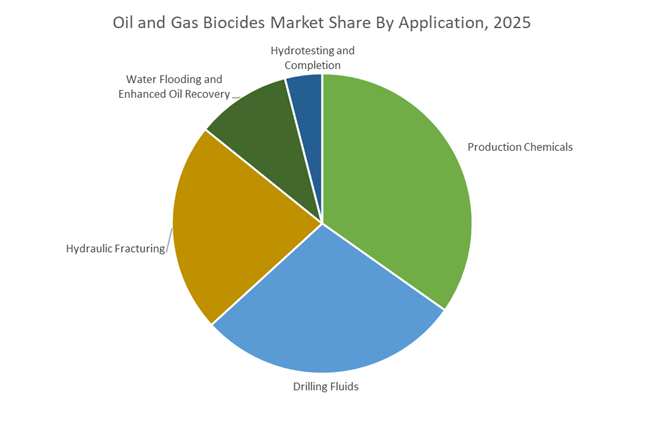

Production Chemicals Segment Drives Continuous Demand for Biocide Injection in Oilfield Operations

Production chemicals accounted for 34.8% of the Oil and Gas Biocides Market by application in 2025, reflecting the need for ongoing microbial control throughout the lifecycle of oil and gas wells. Biocides are continuously injected into production systems, flowlines, and produced water streams to prevent microbial-induced corrosion, biofouling, and hydrogen sulfide generation. This segment benefits from sustained demand as wells transition from drilling to long-term production phases. Effective microbial management ensures asset integrity and operational efficiency. In 2025, adoption of real-time microbial monitoring and automated dosing systems is increasing, enabling operators to optimize biocide usage based on actual bacterial activity while reducing operational costs and environmental impact.

Oil and Gas Biocides Market Competitive Landscape

The oil and gas biocides market in 2026 is driven by non-oxidizing chemistries, digital dosing systems, and compatibility with high-TDS produced water recycling. Competitive differentiation centers on microbial corrosion control (MIC), SRB-targeted formulations, and synergistic integration with corrosion and scale inhibitors for asset integrity optimization.

ChampionX leads integrated microbial control with data-driven biocide solutions for upstream asset integrity

ChampionX dominates the oilfield biocides segment through its “chemistry-plus-data” platform, combining molecular biology tools (MBTs) with real-time SRB monitoring for precision dosing. Its Clean n Cor® technology delivers dual functionality, enabling simultaneous cleaning, deposit control, and corrosion inhibition at the pipe surface. The company’s integration of H2S scavengers and biocides enhances operational efficiency and reduces downtime in high-pressure, high-temperature (HTHP) environments. Recognition through the Golden Peacock Sustainability Award highlights its shift toward low-toxicity, environmentally compliant biocides. ChampionX’s advanced diagnostics and integrated chemical management systems position it as a leader in digital oilfield microbial control.

BASF scales industrial biocide production with Verbund integration and cost-optimized specialty chemistries

BASF is leveraging its global Verbund infrastructure to deliver high-performance oilfield biocides, including glutaraldehyde and THPS, with strong cost competitiveness. The startup of its Zhanjiang Verbund site strengthens localized supply in Asia-Pacific, addressing growing demand from unconventional oil and gas operations. With €59.7 billion in 2025 sales and a targeted €2.3 billion cost reduction by 2026, BASF is optimizing margins while maintaining pricing flexibility. Its focus on CO2 emission reduction aligns biocide manufacturing with net-zero targets. BASF’s integrated production model ensures consistent quality and regulatory compliance under EPA and EU frameworks.

Solvay advances zero-residue peroxide-based biocides aligned with decarbonization and water treatment efficiency

Solvay is positioning hydrogen peroxide-based biocides as zero-residue alternatives for oilfield water treatment, addressing regulatory pressure under BPR and FIFRA. Its Peroxides segment continues to show growth, supported by increasing demand for environmentally compatible microbial control solutions. With €881 million EBITDA and a 20.7% margin in 2025, Solvay maintains strong financial stability while targeting €770–850 million in 2026. A 29% reduction in Scope 1 and 2 emissions enhances its appeal to ESG-focused operators. Ongoing energy transition projects in Europe ensure cost resilience in chemical production. Solvay’s focus on clean chemistry strengthens its position in sustainable oilfield biocides.

Clariant strengthens oil services portfolio with high-performance biocides and efficiency-driven specialty chemicals

Clariant is expanding its Oil Services segment within its Care Chemicals division, driven by demand for advanced microbial control and flow assurance solutions in mature oilfields. The company achieved CHF 50 million in cost savings in 2025 and is targeting CHF 80 million by 2026, improving EBITDA margins to 17.8%. Strategic collaboration with Vertimass highlights its commitment to bio-based innovation, extending into biocide development. Clariant’s strong ESG performance and low DART safety rate reinforce its reputation among global operators. Its focus on high-margin specialty chemicals supports sustained growth in oilfield applications.

LANXESS drives high-purity non-oxidizing biocides with global supply reliability and pricing discipline

LANXESS is reinforcing its leadership in oilfield biocides through its Consumer Protection segment, offering high-purity isothiazolinone-based chemistries (BIT, MIT) for microbial control. The company implemented price increases of 15%–50% in 2026 to offset rising energy and logistics costs, maintaining margin stability. With €6.4 billion in sales and operations across 32 countries, LANXESS ensures consistent global supply of specialty biocides. Its R&D focus on biodegradable and environmentally compliant formulations aligns with tightening regulatory standards. The company’s expertise in functional additives supports innovation in sustainable oilfield chemistry solutions.

United States Oil and Gas Biocides Market– Chlorine-Free Biocides and Smart Well Integrity Management

The United States oil and gas biocides market is undergoing a structural shift driven by regulatory approvals, shale-specific microbial risks, and produced water reuse economics. In September 2024, the U.S. Environmental Protection Agency approved a new portfolio of chlorine-free, high-performance biocides from LANXESS, explicitly addressing operator demand for lower environmental impact solutions in unconventional shale formations. This approval has accelerated substitution away from legacy oxidizing chemistries toward advanced formulations that balance microbial efficacy with regulatory acceptance. The trend is reinforced by the rapid adoption of peracetic acid biocides, which operators increasingly favor as biodegradable alternatives to glutaraldehyde in hydraulic fracturing and well stimulation programs, particularly where water reuse and discharge constraints are tightening.

Infrastructure and service-level innovation further define the U.S. market. In August 2025, Cathedral Holdings commissioned a dedicated technical laboratory in The Woodlands, Texas, designed to fast-track biocidal performance testing for Permian Basin conditions, including high total dissolved solids produced water. At the field level, service providers in the Midland region are deploying microencapsulated smart-release biocides that extend downhole protection cycles in mature wells, reducing intervention frequency and total chemical load. According to the Energy Information Administration, renewed focus on enhanced oil recovery projects is elevating demand for biocides that suppress sulfate-reducing bacteria responsible for reservoir souring. Parallel policy signals, including the EPA Safer Choice program and SDSI initiative, are reshaping procurement criteria toward biocides with higher biodegradability and improved environmental profiles.

Germany Oil and Gas Biocides Market– Sustainability-Led R&D and High-Temperature Offshore Solutions

Germany’s oil and gas biocides landscape is shaped by intensive corporate R&D investment and stringent European regulatory frameworks. BASF SE committed approximately €2 billion annually during 2024–2025 to research and development, with the majority of projects aligned to sustainability targets, including next-generation eco-friendly biocidal active substances. Product innovation remains central to Germany’s strategic positioning. In 2024, LANXESS launched BioGuard HTX, a high-temperature biocide stable up to 150°C, directly addressing the operational realities of ultra-deepwater, geothermal, and North Sea drilling environments where conventional actives rapidly degrade.

Regulatory compliance is simultaneously raising entry barriers. Updates to the European Biocidal Products Regulation, including the August 2025 implementation of Regulation (EU) 2025/1490, increased ECHA fees by nearly 20%, compelling manufacturers to rationalize portfolios and prioritize high-value, compliant formulations. Germany is also emerging as a green chemistry innovation hub for the biocides value chain. A joint development agreement between BASF and ExxonMobil on methane pyrolysis is creating low-emission hydrogen feedstocks for sustainable chemical intermediates. At the Ludwigshafen Verbund site, pilot deployment of recycled chemical building blocks is embedding circular economy principles into industrial biocide manufacturing.

China Oil and Gas Biocides Market– Digitalized Dosage Control and Sustainable Chemical Scale-Up

China represents one of the most dynamic oil and gas biocides markets, combining regulatory momentum with large-scale industrial capacity expansion. In early 2025, BASF commissioned its first commercial loopamid facility in Caojing, Shanghai, signaling a decisive shift toward sustainable chemical infrastructure that underpins domestic oilfield chemicals supply. Regulatory direction has been equally influential. In December 2024, the Ministry of Ecology and Environment authorized a new wave of environmentally friendly biocides for industrial and municipal water treatment, effectively extending green chemistry mandates into the energy sector.

Operationally, China is advancing faster than most regions in digital biocide management. Offshore developments in Bohai Bay and the South China Sea are increasingly deploying AI-driven and Industrial IoT platforms to monitor real-time biocide dosing, improving microbial control precision while reducing chemical overuse. Wastewater treatment remains a major growth vector, supported by stringent zero-liquid discharge mandates implemented across industrial zones during 2024–2025. Material science innovation is also gaining traction, with nano-biocide formulations and zinc oxide nanoparticles being tested to enhance oil recovery while lowering injection volumes. To secure supply resilience, China is expanding domestic ethoxylation and sulfonation capacity, reducing dependence on imported intermediates for non-oxidizing biocides used in exploration and production activities.

Brazil Oil and Gas Biocides Market– Offshore Corrosion Control and Bio-Based Alternatives

Brazil’s oil and gas biocides market is fundamentally offshore-oriented, anchored by deepwater and pre-salt developments. Petrobras continues to drive demand for specialized biocidal formulations capable of withstanding extreme pressure and temperature conditions. THPS-based systems and glutaraldehyde-quaternary blends are widely deployed to mitigate microbiologically induced corrosion in subsea infrastructure, where failure risks carry substantial operational and financial consequences. Regulatory alignment is tightening, with the national agency updating injection water quality standards to enforce stricter microbial thresholds across offshore assets.

Brazil is also emerging as a testing ground for sustainable alternatives. Research published in 2025 demonstrated the effectiveness of plant-based green biocides in inhibiting thiosulfate-reducing bacterial biofilms, opening pathways for partial substitution of conventional chemistries. Logistics investments are supporting this expansion, notably the scaling of chemical storage and blending terminals at the Port of Santos to service rising offshore drilling fluid demand. Enhanced oil recovery is another catalyst, as polymer flooding projects increasingly require robust biocide programs to prevent microbial degradation of polymers and maintain injection efficiency.

India Oil and Gas Biocides Market– Indigenous Manufacturing and Fast-Acting Oxidizing Biocides

India’s oil and gas biocides market is transitioning from import reliance toward domestic manufacturing and application-driven growth. In February 2025, Imperial Oilfield Chemicals introduced EcoFerm, a fermentation-derived biocide tailored for produced water treatment under high-salinity conditions, reflecting growing interest in bio-based actives. On the supply side, companies such as Melzer Chemicals Pvt. Ltd. are expanding high-purity DBNPA and glutaraldehyde production lines to meet rising demand from domestic oil marketing companies and export customers.

Policy support under the Make in India program is accelerating this shift by offering subsidies for indigenous oilfield chemical development, strengthening supply security. Field demand is expanding as India intensifies onshore exploration in the Rajasthan and Krishna-Godavari basins to enhance energy independence. Environmental regulation is a decisive factor. The Central Pollution Control Board has tightened effluent discharge norms for petroleum operations, favoring fast-acting, non-persistent oxidizing biocides that minimize residual toxicity while maintaining microbial control efficiency.

Strategic Country Comparison – Oil and Gas Biocides

Oil and Gas Biocides Market County Level Snapshot

|

Country

|

Primary Market Driver

|

Technology Focus

|

Regulatory Influence

|

|

United States

|

Shale optimization and water reuse

|

Chlorine-free and smart-release biocides

|

EPA approvals and Safer Choice criteria

|

|

Germany

|

Sustainability and offshore extremes

|

High-temperature and circular biocides

|

EU BPR and ECHA compliance

|

|

China

|

Scale and digital control

|

AI-managed dosing and nano-biocides

|

Green chemistry mandates

|

|

Brazil

|

Deepwater integrity

|

THPS and bio-based alternatives

|

Injection water standards

|

|

India

|

Domestic production and compliance

|

DBNPA, glutaraldehyde, bio-derived actives

|

CPCB effluent regulations

|

Oil and Gas Biocides Market Report Scope

Oil and Gas Biocides Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$715.6 Million

|

|

Market Size (2034)

|

$1304.6 Million

|

|

Market Growth Rate

|

6.9%

|

|

Segments

|

By Type (Oxidizing Biocides, Non-Oxidizing Biocides), By Application (Drilling Fluids, Hydraulic Fracturing, Production Chemicals, Water Flooding and Enhanced Oil Recovery, Hydrotesting and Completion), By Functionality (Decontaminating Biocides, Preservative Biocides, Dual-Action Biocides)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

LANXESS, BASF, ChampionX, Baker Hughes, Halliburton, Solvay, Innospec, Nouryon, Evonik Industries, Kemira, SUEZ, Imperial Oilfield Chemicals, Melzer Chemicals, Albemarle, Clariant

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Oil and Gas Biocides Market Segmentation

By Type

- Oxidizing Biocides

- Non-Oxidizing Biocides

By Application

- Drilling Fluids

- Hydraulic Fracturing

- Production Chemicals

- Water Flooding and Enhanced Oil Recovery

- Hydrotesting and Completion

By Functionality

- Decontaminating Biocides

- Preservative Biocides

- Dual-Action Biocides

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Oil and Gas Biocides Industry

- LANXESS

- BASF

- ChampionX

- Baker Hughes

- Halliburton

- Solvay

- Innospec

- Nouryon

- Evonik Industries

- Kemira

- SUEZ

- Imperial Oilfield Chemicals

- Melzer Chemicals

- Albemarle

- Clariant

*- List not Exhaustive