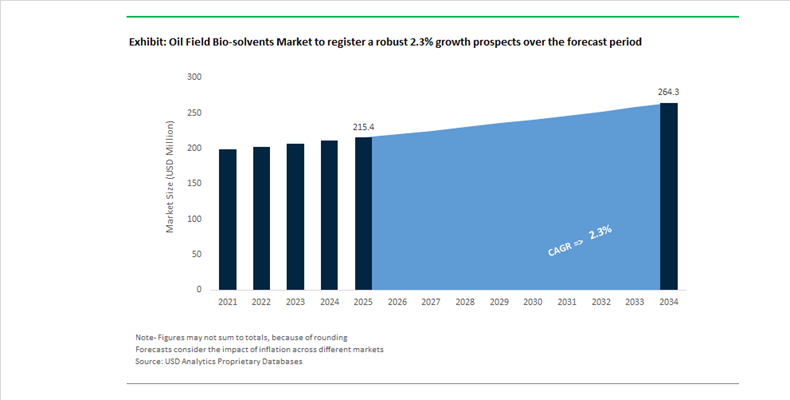

Oil Field Bio-Solvents Market Valued at $215.4 Million in 2025, Forecast to Reach $264.3 Million by 2034 at 2.3% CAGR Amid Decarbonized Production Chemistry

The Oil Field Bio-Solvents Market is valued at $215.4 Million in 2025 and projected to reach $264.3 Million by 2034, expanding at a CAGR of 2.3%. Growth is supported by tightening offshore discharge regulations, rising ESG-linked procurement standards, and the replacement of petroleum-derived aromatics with biodegradable, low-toxicity solvent systems. Oilfield bio-solvents are increasingly deployed for paraffin removal, asphaltene dispersion, tank cleaning, degreasing, and hydrate inhibition across upstream and midstream operations. Operators in environmentally sensitive basins such as the North Sea and Gulf of Mexico are prioritizing high-flash-point, readily biodegradable solvent chemistries to reduce environmental liabilities and worker exposure risks.

In March 2024, ExxonMobil Chemical and BASF Corporation formed a strategic collaboration to commercialize next-generation solvent solutions aligned with global ESG mandates. The partnership focuses on catalytic process improvements that enable drop-in high-performance solvents with improved lifecycle efficiency for oilfield extraction and industrial cleaning. In June 2024, Technip Energies and Shell Catalysts & Technologies advanced Bio-2-Glycols technology, enabling the production of bio-based monoethylene glycol from glucose feedstocks. Bio-MEG serves as a renewable hydrate inhibitor in subsea pipelines, reducing reliance on fossil-based glycols. In October 2024, LyondellBasell completed its acquisition of APK AG, securing solvent-based recycling technology that enhances access to high-purity recovered solvents suitable for specialty oilfield cleaning applications.

Market consolidation accelerated in July 2025 when SLB finalized its $7.8 billion acquisition of ChampionX. ChampionX’s portfolio of specialty bio-solvents for paraffin removal and asphaltene control is now integrated into SLB’s digital production ecosystem, enabling automated dosing, remote monitoring, and optimized chemical utilization. In September 2025, the SOLRESS consortium, coordinated by AIMPLAS, launched a €9.1 million initiative to produce industrial solvents such as 2-MeTHF and ethyl lactate from organic waste streams including coffee grounds and lignocellulosic biomass. In October 2025, GFBiochemicals introduced RE:CHEMISTRY NEW320, a levulinate-ketal solvent derived from agricultural waste, targeting oilfield degreasing and stimulation applications with reduced carbon intensity. During 2025, the Biofuture Platform issued a declaration at COP30 promoting sustainable carbon transitions, accelerating industry-wide solvent R&D shifts toward bio-based and recycled feedstocks.

Commercial scaling of renewable solvent portfolios intensified through 2025 and early 2026. The Nxtlevvel joint venture expanded production of levulinic-acid-derived solvents, positioning biodegradable levulinates as high-solvency replacements for petroleum aromatics in equipment maintenance. In 2024, Perstorp expanded its Pevalen™ Pro renewable portfolio, supporting polyol-ester-based bio-solvents for drilling fluids in regulated offshore environments. In 2025, Vertec BioSolvents advanced its VertecBio Gold series using ethyl lactate and soyate blends for heavy crude dissolution and paraffin removal. In early 2026, Innospec reported rising adoption of high-flash-point bio-based solvents across oilfield transport and storage, highlighting the safety advantages over volatile hydrocarbon systems.

Oil Field Biosolvents Market Trends and Opportunities

Trend: Mandated Adoption of Biosolvents in Offshore Decommissioning and Pipeline Pigging

Regulatory scrutiny around offshore decommissioning and late-life asset cleaning has intensified sharply, transforming biosolvents from optional substitutes into compliance-critical chemicals within oilfield operations. Regulators across mature offshore basins are tightening controls on solvent toxicity, discharge persistence, and air emissions during the “cleaning for disposal” phase of platforms, subsea pipelines, and storage systems. As a result, oilfield biosolvents are increasingly specified as default chemistries for pipeline pigging, tank flushing, and subsea equipment cleaning.

In the North Sea, updated requirements under the OSPAR Commission Harmonised Mandatory Control System implemented in 2025 have accelerated the shift toward PLONOR-listed biosolvents. These standards prioritize OECD 301-ready biodegradability, enabling treated wash water to be discharged overboard without long-term marine toxicity risks. Citrus terpene solvents and fatty acid methyl esters are now widely deployed for pipeline flushing because they dissolve waxy hydrocarbons and sludge while meeting strict biodegradation thresholds. Environmental impact assessments conducted in 2024 confirmed that replacing aromatic solvents such as toluene with bio-derived esters reduces aquatic toxicity by approximately 50%, directly supporting the North-East Atlantic Environment Strategy 2030.

In the Gulf of Mexico, regulatory enforcement under the Bureau of Safety and Environmental Enforcement Idle Iron policy is driving similar adoption. Operators decommissioning non-producing assets are increasingly constrained by air-quality limits and hazardous air pollutant exposure thresholds. Biosolvents with low volatility and high flash points are now preferred for tank and pipeline cleaning, as they mitigate VOC emissions and reduce worker exposure risks during confined-space operations. Collectively, these regulatory and operational pressures are embedding biosolvents into standard offshore decommissioning workflows, creating sustained, non-cyclical demand growth.

Trend: High-Performance Biosolvents Enable Green Well Stimulation in EOR

Beyond compliance-driven adoption, biosolvents are gaining traction as performance-critical tools in enhanced oil recovery programs, particularly in polymer flooding and mature reservoir management. In these applications, traditional acidizing techniques often fail to address organic fouling, polymer filter cakes, and asphaltene deposition that restrict injectivity. Biosolvents offer a non-corrosive, reservoir-compatible alternative capable of restoring flow without damaging downhole metallurgy or reservoir permeability.

Field deployments in 2024 and 2025 demonstrate that bio-based alcohols and ester solvents are increasingly used as soak treatments to dissolve polymer residues in injection wells. Unlike mineral acids, these biosolvents do not trigger iron sulfide precipitation, a common cause of irreversible formation damage. In the Permian Basin, methyl soyate-based formulations are emerging as preferred asphaltene dissolvers. These plant-derived solvents deliver solvency power comparable to xylene while offering significantly higher flash points, materially reducing fire and explosion risk during high-pressure injection operations.

Technical innovation is further amplifying their effectiveness. Research published in late 2024 confirms that incorporating biosolvents into nano- and microemulsion systems can reduce interfacial tension to near-zero levels. This enables deeper penetration into pore networks and mobilization of trapped hydrocarbons beyond the reach of conventional waterflooding. As operators increasingly align EOR programs with sustainability metrics, biosolvents are transitioning from niche green alternatives to core stimulation chemistries.

Opportunity: Low-VOC, High-Flash Point Biosolvents for Onshore Tank Remediation

Onshore oilfield operations in tightly regulated jurisdictions are creating a high-growth opportunity for biosolvents in remediation and maintenance services. States with chronic air-quality non-attainment issues are enforcing strict VOC limits, effectively disqualifying conventional petroleum solvents from tank cleaning, pit remediation, and soil washing activities.

In regions such as California and Colorado, oilfield service providers now treat low-VOC biosolvents as a license-to-operate requirement rather than a sustainability upgrade. Bio-derived esters and surfactant-solvent blends enable crude storage tanks to be cleaned without triggering air permit violations. Worker safety data published in 2025 indicates that replacing aromatic solvents with biosolvents can reduce exposure to hazardous air pollutants such as benzene by up to 80%. Higher flash points also allow safer high-temperature cleaning processes, expanding operational flexibility.

Biosolvents are also gaining traction in soil remediation. Pilot projects in shale basins demonstrate that bio-based washing agents can recover significantly more hydrocarbons from contaminated drill cuttings compared to mechanical separation alone. This improves onsite disposal outcomes, reduces transportation volumes, and lowers total remediation costs. As environmental enforcement intensifies, demand for high-performance, compliant biosolvents in onshore maintenance is expected to scale structurally.

Opportunity: Multifunctional Biosolvent-Based Flowback Aids for Hydraulic Fracturing

Hydraulic fracturing operations are increasingly integrating biosolvents into flowback and completion fluids to enhance early production performance while minimizing environmental risk. These multifunctional additives act as non-emulsifiers, surface-tension reducers, and cleanup agents within the fracture network, supporting faster recovery of injected fluids and improved hydrocarbon flow.

Field results from liquid-rich shale plays show that renewable biosolvent-based flowback aids can increase initial 30-day production rates by 5 to 8% by preventing stable emulsions in the proppant pack. By maintaining phase separation between oil and water, these additives reduce blockage and improve fracture conductivity. Importantly, bio-based microemulsions deliver this performance without altering rock wettability unpredictably, avoiding water trapping issues that undermine well productivity in tight formations.

Regulatory scrutiny is reinforcing this opportunity. Updated Clean Water Act oversight by the U.S. Environmental Protection Agency in 2025 has elevated transparency requirements for fracturing fluid additives. Biosolvents carrying GRAS or EPA Design for the Environment credentials are increasingly prioritized by major operators seeking to de-risk groundwater contamination and reputational exposure. As shale development matures, biosolvent-enabled flowback systems represent a convergence of performance optimization, regulatory compliance, and ESG alignment within the oil field biosolvents market.

Oil Field Bio Solvents Market Share and Segmentation Insights

Terpene-Based Bio Solvents Capture Leading Share Through High Solvency for Hydrocarbon Deposits

Terpenes accounted for 38.60% of the Oil Field Bio Solvents Market by solvent type in 2025, establishing them as the dominant renewable solvent category used in oilfield operations. Terpene solvents, particularly D-limonene derived from citrus processing, provide strong solvency for paraffin, asphaltene, and hydrocarbon sludge deposits that frequently impair flow assurance and equipment performance. Their renewable origin, low toxicity profile, and biodegradability make them increasingly attractive alternatives to conventional petroleum-based solvents in drilling, cleaning, and stimulation processes. A major 2025 development is the rise of circular economy sourcing, where terpene solvents are produced from upcycled citrus waste and biomass byproducts, improving feedstock sustainability while lowering raw material costs across the bio-based oilfield chemical supply chain.

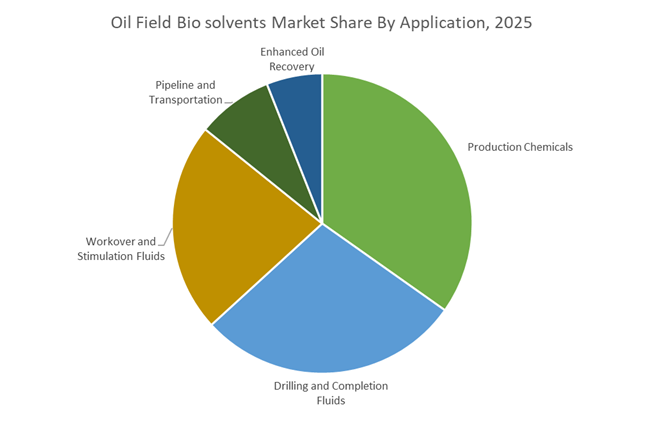

Production Chemicals Segment Leads Bio Solvent Consumption in Continuous Flow Assurance Programs

Production chemicals represented 34.8% of the Oil Field Bio Solvents Market by application in 2025, making it the largest demand segment across oilfield operations. Continuous management of produced fluids, paraffin deposition, and equipment fouling requires frequent solvent usage to maintain operational efficiency in production systems. Bio-based solvents such as terpenes and bio-esters are increasingly replacing traditional hydrocarbon solvents in paraffin control, scale removal, and equipment cleaning due to improved environmental and worker safety performance. A key 2025 trend is the adoption of continuous solvent injection programs, where cost-competitive bio solvents are dosed directly into production streams to maintain flow assurance, reduce workover frequency, and support sustainable oilfield chemical management strategies.

Oil Field Bio-Solvents Market Competitive Landscape

The oil field bio-solvents market in 2026 is driven by biodegradable FAME and terpene-based chemistries, dual-function flow assurance performance, and regulatory pressure under EPA and REACH. Competitive advantage lies in feedstock integration, low-VOC formulations, and AI-driven dosing to optimize asphaltene removal and crude flow efficiency.

SLB–ChampionX integrates AI-driven dosing with bio-solvent chemistry for production optimization

SLB, following the integration of ChampionX, leads the oilfield bio-solvents market with a combined digital-chemical platform targeting production and recovery optimization. The acquisition contributed $1.46 billion in 2025 revenue, strengthening global distribution of bio-based oilfield chemicals. AI-driven dosing systems reduce chemical consumption by up to 15%, improving cost efficiency in offshore operations. Integration of asset integrity solutions with reservoir analytics enables real-time monitoring of bio-solvent performance in HTHP environments. The company is expanding aggressively across the Middle East and Latin America, leveraging its scale and digital ecosystem. This synergy positions SLB–ChampionX as a dominant player in precision-applied bio-solvent technologies.

Solvay scales bio-based solvent portfolio with cost discipline and localized feedstock sourcing strategy

Solvay is advancing its bio-solvent portfolio through large-scale commercialization of renewable solvent chemistries aligned with circular economy principles. With a 20.7% EBITDA margin and €306 million net profit in 2025, the company maintains financial strength to support €300 million CAPEX focused on sustainable chemistry. Structural cost savings of €211 million, targeting €300 million by 2026, enhance competitiveness against fossil-based solvents. Solvay’s strategy to source 70% of raw materials locally by 2027 reduces supply chain risk and carbon footprint. Its focus on high-flashpoint, biodegradable solvents positions it strongly in Europe and Asia. This integration of sustainability and cost efficiency strengthens its market position.

BASF leverages Verbund integration and green R&D to expand low-VOC bio-solvent production

BASF is strengthening its position in bio-solvents through its “Winning Ways” strategy, focusing on low-VOC, high-performance formulations for oilfield applications. The startup of its Zhanjiang Verbund site enhances localized supply for Asia-Pacific, supporting growing demand for environmentally compliant solvents. With a projected €6.2–€7.0 billion EBITDA in 2026, BASF continues to invest in green chemistry innovation supported by €1.7 billion in cost savings. Its R&D is focused on reducing carbon intensity while maintaining solvent efficiency in asphaltene removal and flow assurance. BASF’s decarbonization targets further align its portfolio with global sustainability mandates. Its scale and integration provide a competitive edge in industrial bio-solvents.

Clariant expands EcoTain® bio-solvent portfolio with regional production and sustainability-led growth strategy

Clariant is positioning its Care Chemicals segment as a leader in sustainable oilfield bio-solvents under its EcoTain® label. Leadership restructuring in 2026 signals a stronger push into North American shale markets and global oil services expansion. The company is increasing local production in China to over 50%, supported by investments in its Shanghai innovation hub. With a targeted EBITDA margin of 19–21% and 4–6% sales growth, Clariant is focusing on high-margin specialty chemicals. Its sustainability-driven innovation emphasizes biodegradable, high-performance solvent systems. This localized and eco-focused approach enhances its competitiveness in evolving regulatory environments.

Croda delivers 100% bio-based solvent solutions through biotechnology and co-creation innovation model

Croda is leveraging its biotechnology expertise to deliver fully renewable, USDA BioPreferred® certified bio-solvents for oilfield applications. Its ECO range utilizes bio-based ethylene oxide and enzyme-driven processes, reducing energy consumption and Scope 2 and 3 emissions. With 2025 sales of £1,699.4 million and a targeted 3–6% CAGR, Croda is focusing on high-value specialty solutions. A 12% increase in R&D pipeline value highlights strong customer co-creation in designing tailored solvent systems. Its marine biotechnology capabilities enable advanced, low-toxicity formulations. Croda’s innovation-led strategy positions it as a premium provider of sustainable oilfield solvents.

United States – TSCA Enablement and Scale-Up of Bio-Derived Performance Solvents

The United States oil field bio-solvents market is transitioning from pilot adoption to scaled commercialization, supported by regulatory clarity and capacity expansion. In mid-2025, the U.S. Environmental Protection Agency updated the Toxic Substances Control Act inventory to formally include new bio-based esters approved for offshore applications. This regulatory milestone has materially shortened commercialization timelines for green drilling fluid additives and equipment cleaning solvents, allowing operators to substitute conventional petroleum-derived solvents without extended review cycles. Procurement decisions are increasingly shaped by the Safer Detergents Stewardship Initiative, with 2025 targets accelerating the replacement of nonylphenol ethoxylates in industrial degreasing and oilfield equipment maintenance using bio-solvent alternatives.

On the supply side, investment activity is reinforcing domestic manufacturing resilience. Innospec expanded bio-solvent production capacity at its Pleasanton, Texas facility in March 2025, with new proprietary units scheduled to come online by early 2026. Stepan Company further strengthened the ecosystem by commissioning a large alkoxylation plant in Pasadena, Texas, capable of producing 75,000 metric tons annually of surfactants and bio-based solvents. At the formulation level, Afton Chemical launched the HiTEC® 65522 series in August 2025, leveraging bio-derived solvent systems to protect advanced gasoline direct injection components from stochastic pre-ignition. Field adoption is most visible in the Permian Basin, where peracetic acid and soy-based esters are increasingly replacing traditional glutaraldehyde chemistries in hydraulic fracturing operations.

Brazil – Ethanol Feedstocks and Offshore Bio-Solvent Leadership

Brazil occupies a structurally advantaged position in the global oil field bio-solvents industry due to its deep integration of bio-ethanol into the chemical value chain. Following the 2025 mandate raising anhydrous ethanol blending to E30, sugarcane-derived ethanol has become a primary feedstock for high-solvency bio-solvents used in oilfield applications. This structural advantage underpins Brazil’s emergence as a global reference market for ethanol-based solvent systems such as Solsys® Bio Etac. Industry recognition reinforces this trajectory, with Clariant Oil Services receiving the Petrobras Best Suppliers Award in late 2025 for its delivery of specialty and bio-based solutions tailored to offshore conditions.

Product innovation and regulatory alignment are reinforcing adoption. Solvay expanded its Augeo® bio-solvent portfolio in late 2024, positioning it as a high-performance alternative to glycol-based solvents in completion and production fluids. Concurrently, updates by the National Agency of Petroleum in 2025 tightened fuel density and toxicity benchmarks, indirectly favoring low-toxicity bio-solvents across the upstream and midstream value chain. Petrobras is also piloting microbial-derived biosurfactants and bio-solvents in Pre-salt reservoirs to enhance oil recovery while reducing the environmental footprint of injection fluids, signaling longer-term integration of biologically sourced chemistries into offshore EOR programs.

Germany – Circular Feedstocks and North Sea Compliance-Driven Demand

Germany’s oil field bio-solvents market is shaped by its role as a global R&D nucleus for sustainable chemical intermediates and by strict European environmental frameworks. BASF SE is consolidating selected Asian production assets while preserving Ludwigshafen as its primary innovation hub, with 2025–2026 investments directed toward bio-based PolyTHF® grades and amine-based solvents suitable for oilfield use. A parallel joint development agreement between BASF and ExxonMobil, signed in November 2025, focuses on methane pyrolysis to generate low-emission hydrogen, supporting the synthesis of next-generation sustainable solvents.

Regulatory and circular economy developments are accelerating portfolio shifts. Implementation of Regulation (EU) 2025/1490 revised the European Biocidal Products Regulation fee structure, increasing compliance costs and incentivizing German manufacturers to favor non-toxic, bio-solvent-based preservation systems. BASF’s 2025 launch of ISCC EU-certified biomass-balanced methanol provides a traceable renewable feedstock for oilfield methyl ester production. Operationally, demand is rising in the North Sea, where low-foam bio-solvent formulations are increasingly specified for subsea equipment cleaning to meet the zero-discharge requirements enforced by the OSPAR Commission.

India – Policy-Driven Localization and Bio-Refinery Integration

India’s oil field bio-solvents market is evolving rapidly under supportive legislative reforms and domestic capacity building. The Oilfield Regulation and Development Amendment Act of 2025 modernized the upstream framework and introduced incentives for green chemical adoption in exploration and production activities. This legislative shift is complemented by consolidation in the domestic chemical sector. Godrej Industries expanded its bio-based solvent portfolio through the acquisition of Savannah Surfactants’ business in 2025, enhancing supply availability for Indian E&P operators.

Bio-refinery development is providing an additional structural tailwind. Under the SATAT initiative, more than 130 compressed bio-gas plants were operational by November 2025, generating by-product streams that are increasingly valorized into localized bio-solvent production. Policy initiatives such as the Hydrocarbon Exploration and Licensing Policy and Mission Anveshan have attracted multibillion-dollar investment commitments with explicit emphasis on sustainable drilling chemistries. Downstream, Indian public sector oil marketing companies are building an extensive network of energy stations to distribute bio-blended fuels and additives, indirectly strengthening logistics and market access for oil field bio-solvents.

Saudi Arabia – Vision 2030 and Bio-Solvents for Unconventional Reservoirs

Saudi Arabia’s oil field bio-solvents market is being shaped by localization strategies and decarbonization objectives embedded within Vision 2030. Halliburton continues to expand manufacturing at its Chemical Reaction Plant in PlasChem Park, Jubail, enabling localized production of oil and gas chemicals, including bio-based performance solvents tailored for regional reservoirs. In December 2025, Aramco awarded a long-term contract to SLB to support unconventional gas development, explicitly mandating the deployment of low-emission chemical technologies.

Biotechnology is emerging as a differentiator. Significant investment is flowing into EOR techniques that leverage extremophile microorganisms capable of producing bio-solvents in situ under high-temperature and high-salinity conditions. Concurrently, new national standards governing industrial water and process treatment are driving the phased replacement of aromatic solvents with aliphatic bio-alternatives, particularly in desalination-integrated oilfields. These developments position Saudi Arabia as a strategic growth market for advanced bio-solvents aligned with both operational performance and emissions reduction goals.

Strategic Country Comparison – Oil Field Bio-Solvents

Oil Field Bio-solvents Market County Level Snapshot

|

Country

|

Core Market Driver

|

Dominant Feedstock or Technology

|

Strategic Direction

|

|

United States

|

TSCA updates and SDSI procurement

|

Bio-esters, PAA, soy-based solvents

|

Scale-up and regulatory-led substitution

|

|

Brazil

|

E30 ethanol mandate and offshore demand

|

Sugarcane ethanol bio-solvents

|

Offshore leadership and EOR integration

|

|

Germany

|

EU regulation and circular chemistry

|

Biomass-balanced methanol, low-foam solvents

|

Compliance-driven innovation

|

|

India

|

Upstream reform and bio-refinery growth

|

Fermentation by-products, localized bio-solvents

|

Domestic manufacturing and policy alignment

|

|

Saudi Arabia

|

Vision 2030 and unconventional gas

|

In-situ bio-solvent production

|

Localization and low-emission EOR

|

Oil Field Bio-solvents Market Report Scope

Oil Field Bio-solvents Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$215.4 Million

|

|

Market Size (2034)

|

$264.3 Million

|

|

Market Growth Rate

|

2.3%

|

|

Segments

|

By Solvent Type (Bio-Based Esters, Bio-Based Alcohols, Bio-Based Glycols, Terpenes, Biosurfactant-Based Solvents), By Application (Drilling and Completion Fluids, Production Chemicals, Enhanced Oil Recovery, Workover and Stimulation Fluids, Pipeline and Transportation), By Source (Plant-Based, Microbial-Based, Animal-Based), By End User (Upstream Operators, Midstream Operators, Oilfield Service Providers)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF, Solvay, Clariant, SLB, Halliburton, Baker Hughes, ChampionX, Innospec, Stepan, Evonik Industries, Ecolab, Dow, Nouryon, India Glycols, Huntsman

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Oil Field Bio Solvents Market Segmentation

By Solvent Type

- Bio-Based Esters

- Bio-Based Alcohols

- Bio-Based Glycols

- Terpenes

- Biosurfactant-Based Solvents

By Application

- Drilling and Completion Fluids

- Production Chemicals

- Enhanced Oil Recovery

- Workover and Stimulation Fluids

- Pipeline and Transportation

By Source

- Plant-Based

- Microbial-Based

- Animal-Based

By End User

- Upstream Operators

- Midstream Operators

- Oilfield Service Providers

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Oil Field Bio Solvents Industry

- BASF

- Solvay

- Clariant

- SLB

- Halliburton

- Baker Hughes

- ChampionX

- Innospec

- Stepan

- Evonik Industries

- Ecolab

- Dow

- Nouryon

- India Glycols

- Huntsman

*- List not Exhaustive