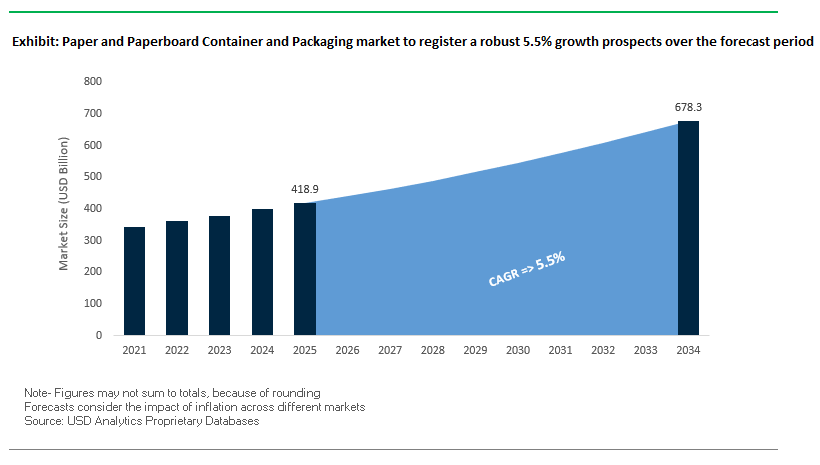

Market Overview: Paper & Paperboard Packaging Set to Reach $678.2 Bn by 2034 on E-commerce, Fiber Substitution, and Smart Labels

Market value (MV) 2025: $418.9 billion │ 2034: $678.2 billion │ CAGR (2025–2034): 5.5%

The global paper and paperboard container and packaging market is scaling on the back of e-commerce fulfillment, plastic-to-fiber conversion, and digitally enabled packaging. For buyers and operations leaders, the strategic questions are: How fast can fiber replace problem plastics without compromising performance? Which paperboard formats best balance protection, cost, and recyclability at scale? How do we embed traceability and consumer engagement without hurting line speeds? The answers increasingly favor corrugated, kraft, and high-performance paperboard engineered for lightweighting, curbside recyclability, and smart-code integration across omnichannel retail.

Key Insights for Industry Stakeholders

- E-commerce is the demand engine: Corrugated and paper mailers address last-mile stresses while meeting retailer recyclability mandates.

- Fiber-based alternatives accelerate plastic exit: Programs targeting removal of “problem plastics” shift SKUs into fiber trays, wraps, and MAP-compatible paperboard.

- Smart, scannable packaging scales: QR/NFC on paperboard unlocks traceability, authenticity, and dynamic content without changing form factors.

- Lightweighting cuts cost & carbon: Next-gen boards and structural design reduce basis weight, freight, and Scope 3 emissions while preserving stacking strength.

Market Analysis: M&A Scale and High-Barrier Papers Redraw the Competitive Map (2025–2024 timeline)

Market structure is consolidating around integrated fiber leaders while converters introduce high-barrier paper to unlock new food and household applications. In August 2025, Mondi launched Ad/Vantage Smooth Brown Semi Extensible and ramped FunctionalBarrier Paper Ultimate, signaling that paper is now credibly addressing use cases that once required multilayer plastics. Also in August 2025, Graphic Packaging secured child-resistant certification for CleanClose™ paperboard laundry pod packs and expanded food applications with PaperSeal® Pressed MAP trays, evidencing fiber’s advance into regulated, moisture- and oxygen-sensitive categories.

Industry scale increased sharply. In July 2025, Smurfit Kappa and WestRock finalized their merger, creating Smurfit WestRock a NYSE-listed fiber packaging giant with global converting coverage and mill integration. In parallel, International Paper completed the acquisition of DS Smith in July 2025 (following February 2025 deal closure steps), then divested five EU corrugated sites to PALM Group to meet remedy requirements consolidation that enhances IP’s EMEA footprint and synergy capture. Upstream and downstream partnerships continue to proliferate: June 2025 saw Mondi×Saga Nutrition launch paper-based pet food packs; and in August 2025 Orora reported FY25 results after fully exiting OPS, sharpening focus on beverage packaging and can-making investments. Net effect: bigger balance sheets, faster innovation sprints, and broader fiber portfolios aimed squarely at plastic replacement in food, beverage, household, and e-commerce.

Trends and Opportunities Reshaping the Paper and Paperboard Container and Packaging Market

Strategic Investment in Recycled Fiber Capacity and Water-Resistant Technologies

The paper and paperboard container and packaging market is undergoing a significant transformation as manufacturers scale up their investment in recycled fiber capacity and develop water- and grease-resistant coatings that maintain recyclability. This shift is a direct response to tightening regulations on plastic packaging and increasing brand commitments to sustainability. In May 2025, Mondi launched a $216 million recycled containerboard mill in Duino, Italy, with an annual production capacity of 420,000 metric tons using 100% recovered paper. Such large-scale projects demonstrate the industry’s commitment to closing the fiber loop and expanding access to sustainable materials.

Governmental initiatives are further accelerating this transition. In the United Kingdom, the Extended Producer Responsibility (EPR) scheme set to take effect in October 2025 will make producers directly responsible for packaging waste costs. This regulation increases fees on hard-to-recycle materials and incentivizes adoption of paperboard solutions, positioning them as the cost-effective and eco-friendly option for retailers and FMCG brands. At the same time, the innovation of biodegradable coatings is expanding the role of paperboard in foodservice and fresh produce applications. These coatings enhance barrier properties without compromising recyclability, unlocking new markets where plastic alternatives were once dominant.

Rapid Adoption of Digital Printing for Short-Run, Customized Packaging

The adoption of digital printing technology is rapidly transforming the paper and paperboard packaging market by enabling short-run, customized, and variable data printing (VDP). This technology is becoming central to personalization and seasonal campaigns, especially in the fast-moving consumer goods (FMCG) sector. Unlike analog printing, digital platforms allow brands to upload artwork directly to presses, reducing lead times and enabling product launches in days rather than weeks.

Global brands are already capitalizing on this capability. PepsiCo India, for example, integrated digital printing into its paperboard packaging to deliver unique, personalized designs and campaign messaging, enhancing consumer engagement. Beyond personalization, digital printing supports smaller, more frequent runs, reducing inventory waste and eliminating the costs of excess or outdated packaging. This trend is particularly valuable for brands pursuing limited editions, regional promotions, or sustainability campaigns, as it combines flexibility with efficiency. By lowering the cost barriers for short runs, digital printing is creating a more agile packaging supply chain while aligning with sustainability by reducing waste at every stage.

Development of Advanced Molded Fiber Solutions for Non-Traditional Applications

Molded fiber packaging is evolving beyond traditional uses like egg cartons and protective trays into premium primary packaging for high-value consumer goods, electronics, and cosmetics. The paper and paperboard container and packaging market is seeing major innovation in this segment, as manufacturers deploy new raw materials, thermoforming techniques, and finishing technologies to meet stricter performance and aesthetic standards.

Companies like Fiber Innovation are collaborating with Fortune 100 companies to supply molded fiber packaging for premium electronics and beauty products, replacing plastics and foams. Technological advancements in thermoformed thin-wall molded fiber allow smoother finishes and more precise shapes, making them suitable for consumer-facing applications like disposable cups, clamshells, and high-quality food containers. Material innovation is also playing a key role: bamboo and bagasse fibers are being used for enhanced tensile strength and flexibility, opening opportunities in demanding markets. This opportunity positions molded fiber as the next-generation replacement for rigid plastics across industries, aligning performance, sustainability, and premium branding.

Integration of Smart and Connected Packaging Features for Enhanced Traceability

Another major opportunity lies in embedding connected packaging features such as QR codes, NFC tags, and digital watermarks directly onto paperboard cartons. This enables packaging to serve not only as a protective shell but also as a digital engagement platform and supply chain enabler. For consumers, scanning a QR code can provide sustainability data, recycling instructions, or brand storytelling, enhancing loyalty and transparency. For brands, serialized identifiers and digital watermarks create a unique digital identity for every unit, enabling real-time supply chain tracking and anti-counterfeiting protection.

The interactive marketing potential of connected packaging is equally significant. Brands can use these features to launch gamified promotions, loyalty programs, or exclusive digital content, transforming a static box into a dynamic communication tool. As consumers increasingly demand transparency and authenticity, connected paperboard packaging positions itself as a bridge between sustainability, trust, and engagement, offering value far beyond containment.

Competitive Landscape: Integrated Fiber Champions and High-Speed Converters Lead on Circularity, Efficiency, and Design

The competitive field is anchored by integrated pulp–paper–converting systems and innovation-led converters. Differentiators include mill integration (cost/availability), barrier paper technology, automation and converting efficiency, and closed-loop recyclability programs with retailers and CPGs. Expect continued M&A, rapid line upgrades, and commercialization of MAP-capable paper trays and seal-through-contamination lidding to win plastic replacement briefs.

Smurfit WestRock Global circular-economy scale with e-commerce and display depth

The newly combined Smurfit WestRock (merger completed July 2025) unites extensive corrugated, consumer packaging, and specialty platforms 500+ converting sites and 62 paper mills across 40 countries. Strategy centers on responsibly sourced fiber, high OEE converting, and design-to-recycle solutions spanning e-commerce boxes, Bag-in-Box®, and retail POS displays. With unmatched footprint and design tools, the company can harmonize cost, lead time, and sustainability for multinational rollouts while capturing synergies across mills and box plants.

International Paper Fiber leader consolidating EMEA and North America positions

International Paper finalized its DS Smith acquisition (February–July 2025), forging a transatlantic leader with targeted $514M+ synergy ambitions and a differentiated EMEA presence. Core portfolio covers containerboard, corrugated packaging, and paperboard for food, beverage, and omnichannel retail. Strategy: optimize the asset base, invest in high-efficiency converting, and leverage end-to-end fiber integration to stabilize input costs and guarantee supply for large CPG networks pursuing plastic-to-fiber conversions.

Mondi High-barrier papers and integrated forest-to-converter model

Mondi scaled FunctionalBarrier Paper Ultimate in 2025 and introduced new industrial paper grades, pushing fiber into grease/oil/moisture-sensitive categories. Its integrated value chain from sustainable forestry to circular end-of-life supports speed-to-market and LCA gains. Strategic projects (e.g., biomass power in Slovakia) reinforce energy self-sufficiency and cost resilience. Ambition remains clear: 100% reusable, recyclable, or compostable product portfolio, enabling customers to hit ESG targets without sacrificing performance.

Graphic Packaging International Consumer brand partner for fiber-first retail experiences

Graphic Packaging advances fiber alternatives to rigid plastics with platforms like EnviroClip™ (clip-style multipacks), PaperLite trays, and PaperSeal® Pressed MAP introduced August 2025. Its CleanClose™ paperboard pod pack achieving child-resistant certification (August 2025) opens regulated home-care channels to fiber. The company’s “Better by 2030” goals drive recyclability and footprint reduction, while investments (e.g., Waco, TX recycled paperboard mill) add capacity, quality, and circular content for blue-chip FMCGs.

Orora Focused beverage packaging with disciplined capital deployment

Following the divestment of OPS (reported August 2025), Orora operates as a focused beverage packaging provider, spanning paperboard cartons and complementary fiber solutions. Strategy prioritizes can-making network investments, sustainability, and channel breadth across beer, soft drinks, and RTD categories. Orora’s disciplined capex and tight customer alignment position it to capture premiumizations and SKU proliferation in beverage while supporting retailer recyclability scorecards.

Paper and Paperboard Container and Packaging Market Share Insights

Corrugated Packaging Leads Market Share by Product Type in Paper & Paperboard Packaging

Corrugated packaging commands 55% of the global paper and paperboard packaging market in 2025, making it the undisputed backbone of modern trade and logistics. Its dominance is inseparable from the global e-commerce boom, where corrugated boxes serve as the default solution for shipping virtually every non-liquid product. Beyond shipping, their structural strength, stackability, and adaptability to high-quality printing make them essential for branding and retail-ready packaging. Folding cartons, accounting for 20%, play a critical role in premium consumer-facing applications such as cereals, frozen foods, cosmetics, and pharmaceuticals. Their high-quality printability ensures shelf differentiation, supporting their stable share. Paper bags and sacks are surging as plastic bans reshape retail and industrial packaging practices, positioning them as the sustainability champion. Meanwhile, liquid cartons remain a specialized but high-value niche, indispensable for milk, juice, and aseptic foods, though recyclability challenges temper their growth. Other formats, including paper tubes, trays, and specialty applications, maintain a stable share by serving niche industrial and consumer needs. Collectively, these product types illustrate how corrugated packaging dominates by volume, folding cartons sustain consumer retail relevance, and paper bags & sacks drive regulatory-led expansion.

Food & Beverage Dominates Market Share by End-Use in Paper & Paperboard Packaging

The food and beverage industry accounts for 45% of the global paper and paperboard packaging market in 2025, making it the largest end-use sector by a wide margin. The category’s dominance is driven by its extensive reliance on cartons, trays, liquid packaging, and paper bags across dry, frozen, fresh, and fast-food applications. Its non-discretionary, high-frequency consumption cements its role as the volume anchor of the industry. Industrial and automotive applications follow with 20%, fueled by demand for heavy-duty corrugated containers and multi-wall sacks for construction materials, chemicals, and agricultural inputs. The electrical and electronics sector continues to expand its share due to the e-commerce-driven shipment of consumer electronics, leveraging corrugated packaging as the default solution for secure transport. Healthcare and pharmaceuticals hold a high-value share where sterile, compliant, and tamper-evident paperboard packaging is critical for regulatory approval and consumer trust. Personal care and cosmetics remain a premium driver, using elaborately finished folding cartons to elevate brand identity and justify higher price points. This segmentation highlights how food and beverages dominate by volume, industrial sectors sustain bulk demand, and healthcare and cosmetics add premium value to the market.

United States: E-commerce Growth and Regulatory Mandates Shaping Sustainable Packaging Solutions

The U.S. paper and paperboard container and packaging market is being significantly influenced by the booming e-commerce sector, which has driven high demand for corrugated boxes and secure packaging solutions for online deliveries. This trend is complemented by PFAS-free mandates in thirteen states, requiring manufacturers to reformulate grease-resistant papers with clay or plant-based coatings. While these alternatives cost 20–30% more than fluorinated chemistries, they ensure regulatory compliance and consumer safety. Extended Producer Responsibility (EPR) regulations, such as California's SB-54, are further motivating companies to adopt recyclable and sustainable packaging materials. Investments in automation-ready secondary lines are helping companies like Mary Kay reduce labor by 85% while maintaining high output, improving efficiency and reducing costs. Additionally, public-sector support through the U.S. Department of Energy’s $52 million allocation for cellulose-based films is fostering next-generation, sustainable paper-based packaging substrates.

Germany: Circular Economy Leadership and Regulatory Compliance Driving Industry Innovation

Germany’s paper and paperboard packaging industry is strongly guided by a strict regulatory framework, including the German Packaging Act (VerpackG), which enforces environmental standards for recycling and waste reduction. The law is set to undergo major amendments in 2025, reinforcing sustainability obligations for businesses. Germany’s leadership in the circular economy promotes collaboration between manufacturers and end-users to develop packaging solutions with high recycled content and full recyclability. Furthermore, the EU Packaging and Packaging Waste Regulation (PPWR), effective February 2025, encourages the reduction of primary raw materials and the economic recycling of all packaging by 2030, creating a powerful incentive for innovation in sustainable paper and paperboard packaging solutions.

China: Capacity Expansion and Sustainability Initiatives Supporting Market Growth

China’s paper and paperboard container and packaging market is witnessing a surge in production capacity, with domestic finished paper capacity increasing by 10% in 2024, the fastest growth in five years. The government’s green transformation initiatives in the express delivery sector are promoting eco-friendly, reusable, and reduced packaging, which provides a sustainable alternative to plastics. A strong export market for Chinese packaging products also motivates manufacturers to meet high international quality standards. Innovations such as paper-based takeaway containers and express packaging are increasingly adopted to reduce plastic waste, supporting both environmental objectives and consumer preferences for sustainable alternatives.

India: National Packaging Initiatives and E-commerce Expansion Driving Industry Adoption

India’s paper and paperboard packaging sector is benefiting from the National Packaging Initiative, which promotes efficient logistics, returnable packaging, product safety, and sustainability. The rapid growth of e-commerce, especially in corrugated box demand for fresh produce, pharmaceuticals, and consumer goods, is a major driver for market expansion. Companies like WestRock are investing in high-quality corrugated containers to serve this growing market. Additionally, India’s Plastic Waste Management Amendment Rules are phasing out single-use plastics, further fueling demand for paper and paperboard alternatives and encouraging companies to adopt sustainable packaging solutions.

Brazil: Regulatory Push and Technological Innovations Expanding Sustainable Paperboard Adoption

In Brazil, stringent legislation restricting plastics, including bags, multilayer sachets, and expanded polystyrene, is promoting a shift toward fiber-based packaging solutions. Technological innovations in coatings are enabling paperboard to replace laminated plastics in food service and takeaway applications, including grease-proof and moisture-resistant variants for fast-food, bakery, and dairy sectors. The integration of digital printing, smart labeling, and anti-counterfeiting technologies such as QR codes and RFID tags is particularly critical for pharmaceutical, nutraceutical, and infant food packaging, ensuring traceability and authentication.

Japan: Government Initiatives and Functional Innovation Enhancing Sustainable Packaging Market

Japan’s paper and paperboard container and packaging market is strongly influenced by governmental initiatives aimed at reducing plastic waste and promoting eco-conscious packaging. Companies like Nippon Paper are expanding production of paper-based barrier materials that protect products from air and water, creating sustainable alternatives to plastics. The industry is also embracing functional innovations, producing robust, water-resistant paperboard capable of meeting demanding applications such as food packaging. Government support for recycling and resource circulation, including the Plastic Resource Circulation Act, ensures that paper-based packaging remains a recyclable and environmentally responsible solution in the Japanese market.

Paper and Paperboard Container and Packaging Market Report Scope

Paper and Paperboard Container and Packaging market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$418.9 Billion

|

|

Market Size (2034)

|

$678.2 Billion

|

|

Market Growth Rate

|

5.5%

|

|

Segments

|

By Product Type (Folding Cartons, Corrugated Packaging, Liquid Cartons, Paper Bags & Sacks, Other Product Types), By Material Grade (Virgin Fiber, Recycled Fiber, Hybrid/Mixed Fiber), By End-Use Industry (Food and Beverage, Healthcare & Pharmaceuticals, Personal Care & Cosmetics, Electrical & Electronics, Industrial & Automotive, Other End-use Industries)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

International Paper, WestRock, Smurfit Kappa Group plc, Mondi Group, DS Smith Plc, Packaging Corporation of America (PCA), Graphic Packaging Holding Company, Oji Holdings Corporation, Rengo Co., Ltd., Stora Enso Oyj, Nippon Paper Industries Co., Ltd., Amcor plc, Sonoco Products Company, Sealed Air Corporation, Greif, Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Paper and Paperboard Container and Packaging Market Segmentation

By Product Type

- Folding Cartons

- Corrugated Packaging

- Liquid Cartons

- Paper Bags & Sacks

- Other Product Types

By Material Grade

- Virgin Fiber

- Recycled Fiber

- Hybrid/Mixed Fiber

By End-Use Industry

- Food and Beverage

- Healthcare & Pharmaceuticals

- Personal Care & Cosmetics

- Electrical & Electronics

- Industrial & Automotive

- Other End-use Industries

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Paper and Paperboard Container and Packaging Market

- International Paper

- WestRock

- Smurfit Kappa Group plc

- Mondi Group

- DS Smith Plc

- Packaging Corporation of America (PCA)

- Graphic Packaging Holding Company

- Oji Holdings Corporation

- Rengo Co., Ltd.

- Stora Enso Oyj

- Nippon Paper Industries Co., Ltd.

- Amcor plc

- Sonoco Products Company

- Sealed Air Corporation

- Greif, Inc.

*List not Exhaustive

Research Coverage

This report by USDAnalytics investigates the global Paper and Paperboard Container and Packaging market, examining recent breakthroughs in fiber-based alternatives, smart packaging integration, and sustainable material innovations. The analysis reviews trends in e-commerce-driven demand, plastic-to-fiber substitution, and the adoption of high-performance paperboard grades across food, beverage, healthcare, and industrial segments. The report highlights competitive strategies, including M&A activity, advanced coating technologies, digital printing applications, and circular economy initiatives. This report is an essential resource for industry professionals, supply chain managers, and packaging decision-makers seeking actionable insights into market dynamics, regulatory impacts, and investment priorities. By integrating comprehensive historic data from 2021 to 2024 with forecast data from 2025 to 2034, the study provides robust projections, market share evaluations, and performance benchmarks across diverse regions and applications, making it a critical tool for identifying growth opportunities, strategic partnerships, and sustainability-aligned solutions. USDAnalytics offers in-depth profiles and strategic assessments of 15+ leading companies, enabling stakeholders to navigate competitive pressures while optimizing cost, performance, and environmental impact.

Scope Highlights:

- Segmentation: By Product Type (Folding Cartons, Corrugated Packaging, Liquid Cartons, Paper Bags & Sacks, Other Product Types), By Material Grade (Virgin Fiber, Recycled Fiber, Hybrid/Mixed Fiber), By End-Use Industry (Food and Beverage, Healthcare & Pharmaceuticals, Personal Care & Cosmetics, Electrical & Electronics, Industrial & Automotive, Other End-use Industries)

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Historic and Forecast Data: Historic data from 2021 to 2024; forecast data from 2025 to 2034.

- Company Coverage: Analysis and profiles of 15+ leading players including International Paper, Smurfit Kappa Group, Mondi Group, WestRock, Graphic Packaging, and more.

Methodology

The research methodology for this report combines a robust mix of primary and secondary research to ensure data accuracy, relevance, and strategic value. USDAnalytics conducted extensive interviews with industry stakeholders, including packaging converters, brand owners, and regulatory bodies, to validate market dynamics and adoption trends. Secondary sources included annual reports, regulatory filings, industry associations, trade publications, and company press releases, providing context for technological innovation, sustainability initiatives, and competitive positioning. Quantitative analysis was applied to historic shipment volumes, material consumption, revenue streams, and regional production capacities. Advanced forecasting models were then developed using CAGR projections, scenario analysis, and sensitivity checks to account for regulatory, environmental, and macroeconomic variables impacting the global paperboard packaging market. Market sizing, segmentation, and share analysis were performed using triangulation methods to cross-verify multiple data inputs, ensuring reliability for strategic decision-making.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.