Market Overview: Growing Demand for Sustainable and High-Performance PET Lidding Films

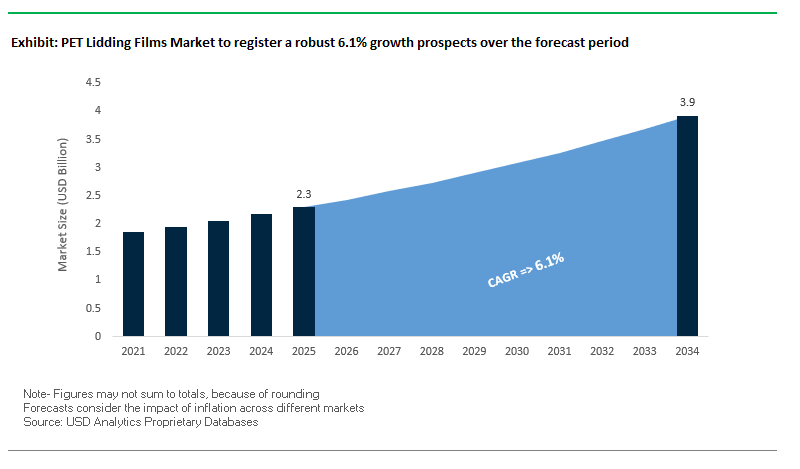

The Global PET Lidding Films Market is a specialized segment of the broader pet care packaging industry, projected to grow from $2.3 billion in 2025 to $3.9 billion by 2034, at a CAGR of 6.1%. Lidding films play a pivotal role in preserving product freshness, enhancing convenience, and supporting premium brand positioning. This segment is being driven by the dual trends of pet humanization and rising consumer awareness around sustainable packaging solutions.

Key Insights for industry professionals and buyers:

- Market Growth: Strong CAGR of 6.1% indicates increasing adoption of PET lidding films across wet pet food and treats.

- Sustainability Focus: Transition to recyclable, mono-material, and paper-based films in response to environmentally conscious pet owners.

- Convenience-Oriented Formats: Single-serve trays and easy-peel lidding films cater to busy lifestyles and premium snacks.

- Advanced Barrier Properties: Films engineered to protect against oxygen, moisture, and light, ensuring product freshness.

- E-Commerce Optimization: Films designed to withstand shipping stress while maintaining peel integrity and consumer appeal.

- Premium Consumer Experience: Packaging is evolving as a tool for brand differentiation, reflecting the emotional value consumers place on their pets.

Market Analysis: Strategic Partnerships, Sustainability Initiatives, and Technological Advancements Are Driving PET Lidding Film Innovation

The PET lidding films market has witnessed significant developments, reflecting the industry’s focus on sustainability, innovation, and market expansion. In September 2025, Mondi collaborated with Saga Nutrition to launch recyclable mono-material dry pet food bags, demonstrating a broader industry trend toward eco-friendly films, including lidding applications. August 2025 saw ProAmpac publish its Sustainability Impact Report and acquire a U.S.-based flexible packaging manufacturer to expand capabilities, signaling its growing focus on circular and high-performance films. In the same month, Mars Petcare introduced recyclable pouches for WHISKAS cat food in the UK and Germany, aligning with the trend of environmentally conscious packaging.

In July 2025, AptarGroup, Inc. announced partnerships to develop new pet care solutions, potentially including innovations in lidding films, while the Pet Sustainability Coalition launched a program to assist companies in transitioning to eco-friendly packaging. A June 2025 U.S. study highlighted consumer preference for “less-plastic” packaging, reinforcing the move toward mono-material and recyclable solutions. Earlier in May 2025, Constantia Flexibles invested over €6 million in a new MDO line in Germany to support production of high-barrier mono-polyethylene films like EcoLamHighPlus, crucial for lidding applications.

The market’s evolution is further reinforced by technological innovation. In April 2025, Storopack introduced PAPERplus Classic CX, a sustainable cushioning system, while February 2025 saw Berry Global and VOID Technologies collaborate on high-performance sustainable films designed for pet food packaging.

Breakthrough Trends and Emerging Opportunities in the PET Lidding Films Market

Shift to High-Barrier, Lightweight Mono-Material Films for Recyclability

The PET lidding films market is undergoing a transformative shift driven by the urgent need for recyclability and reduced carbon footprint. Global players are moving away from complex multi-material laminates toward high-barrier mono-material films that are compatible with established recycling streams for PE and PP. This change is being reinforced by both corporate sustainability commitments and regulatory obligations. For instance, in July 2025, Mars Petcare introduced a recyclable mono-material polypropylene pouch for its WHISKAS® brand in the UK and Germany, which not only aligns with recyclability targets but also achieved a 46% carbon footprint reduction compared to its predecessor. Regulatory frameworks such as the EU’s Packaging and Packaging Waste Regulation (PPWR), which came into force in February 2025, mandate that packaging must be recyclable by 2030 in an “economically viable way.” Non-compliance results in higher EPR fees, directly incentivizing brands to adopt sustainable structures. Alongside this, advancements in film engineering have ensured that performance is not compromised. Companies like KM Packaging have launched polypropylene-based mono-material lidding films that maintain superior oxygen and moisture barrier properties while catering to ambient, chilled, and frozen applications. This trend underscores a decisive market-wide pivot where recyclability, functionality, and compliance converge.

Adoption of Easy-Peel and Resealable Features for Premium Pet Products

The premiumization of pet food packaging is being fueled by rising consumer expectations for convenience, freshness, and functionality. Easy-peel and resealable lidding films are increasingly used for fresh and raw pet meals, supplements, and high-value products, mimicking trends long established in the human food industry. Packaging suppliers such as Amcor are offering resealable solutions that extend product life after opening, minimize waste, and enhance convenience for pet owners. This functionality is particularly valued by urban consumers and subscription-driven premium pet food buyers who demand practicality without compromising quality. The innovation lies in creating films that strike a delicate balance between maintaining strong, tamper-evident seals and enabling effortless resealing. Material scientists are pioneering specialty adhesives and sealants tailored for mono-material substrates, ensuring compatibility with recyclability requirements while maintaining user convenience. As resealability becomes a key differentiator, brands adopting these features are not only enhancing consumer satisfaction but also strengthening brand loyalty in a market where repeat purchase behavior is vital.

Development of Functional Active-Barrier Films with Antimicrobial Properties

The rise of raw and fresh pet food presents both an opportunity and a challenge in packaging innovation. These products, while appealing to health-conscious consumers, are more susceptible to microbial contamination and spoilage. Active-barrier lidding films with antimicrobial functionality offer a compelling solution. Research has demonstrated that embedding antimicrobial agents such as zinc ions, silver nanoparticles, or essential oils into polymer matrices can inhibit pathogens like E. coli and S. aureus, extending shelf life and enhancing safety. For fresh pet diets that skip high-heat processing, this technology could be a game-changer, adding a crucial safety buffer while maintaining the “natural” positioning. The pathway from research to commercialization involves integrating these agents directly into the polymer during extrusion, ensuring controlled release over the product lifecycle. Material science companies are actively working on scalable formulations that can withstand rigorous regulatory testing. The potential of antimicrobial films lies not only in extending shelf life but also in fostering consumer trust, making them a strategic innovation for brands competing in the fresh pet food segment.

Integration of Smart Labels for Supply Chain Visibility and Consumer Engagement

Smart packaging technologies are rapidly moving from concept to implementation in the pet care sector, with lidding films emerging as a practical application point. Incorporating QR codes, NFC tags, or RFID-enabled smart labels provides both transparency for consumers and efficiency for supply chains. Transparency is increasingly demanded by pet owners who want to trace the sourcing and quality of ingredients. For instance, Purina’s “Beyond” brand employs interactive QR codes that allow customers to verify sourcing, thereby strengthening brand credibility. Beyond consumer-facing transparency, smart labels also optimize supply chain efficiency by enabling automated inventory management and real-time product tracking, reducing stockouts and waste. Moreover, these interactive features open a direct communication channel between brands and consumers, creating opportunities for engagement through loyalty programs, personalized content, or cause-driven campaigns. Purina has successfully used on-pack QR codes for fundraising initiatives, exemplifying how brands can leverage packaging for deeper consumer connection. As digital engagement converges with sustainability and efficiency, smart-enabled lidding films represent a significant opportunity for differentiation in the competitive pet care packaging market.

Competitive Landscape: Leading PET Lidding Film Manufacturers Are Advancing Sustainability, High-Barrier Performance, and Consumer-Centric Designs

The global PET lidding films market is shaped by key players leveraging expertise in materials science, high-barrier solutions, and sustainable innovations. These companies are driving the transition toward recyclable, mono-material films that enhance product preservation and user convenience.

Amcor plc: Expanding Sustainable High-Barrier PET Lidding Solutions for Premium Pet Food

Amcor offers a wide range of high-barrier lidding films for tray and cup applications, including P-Plus flexible films adapted from produce to pet food. The company is expanding its sustainable portfolio through R&D in mono-material films that maintain freshness and are easily recyclable. With a global manufacturing network and expertise in material science, Amcor delivers customized, functionally superior packaging solutions. Its strategic focus is to make all packaging recyclable or reusable by 2025 while collaborating with pet food brands on eco-friendly innovations.

Constantia Flexibles Group GmbH: Innovating Lidding Films That Combine Hygiene, Sustainability, and Premium Performance

Constantia Flexibles provides flexible packaging solutions including ComforLid and EcoPeelCover, which integrate hygiene, reduced CO₂ emissions, and resource conservation. In August 2025, the company showcased its expanded portfolio at FACHPACK 2025 and invested €6 million in a new MDO line to support high-barrier mono-polyethylene films. Constantia’s core strength is material innovation and customized packaging, catering to high-end wet food and pet treats, with a strategic focus on sustainability and customer-centric solutions.

Huhtamaki Oyj: Delivering High-Performance Flexible Lidding Films with Circular Economy Focus

Huhtamaki produces high-barrier lidding films for wet pet food, ensuring product freshness and safety. Its collaboration with SABIC and Mars Petcare focuses on certified circular polypropylene, advancing the circular economy. Known for global manufacturing expertise and flexible film innovation, Huhtamaki’s strategy emphasizes sustainable packaging leadership and achieving 2030 goals for recyclable, reusable, or compostable solutions.

ProAmpac: Driving Material Innovation and Sustainability in PET Lidding Films

ProAmpac offers flexible packaging solutions including lidding films under its ProActive Recyclable series, suitable for store drop-off recycling. In August 2025, it acquired a U.S. flexible packaging manufacturer to expand production and commercialized high-performance recyclable films adaptable for pet food. ProAmpac’s strength lies in materials innovation and customized high-barrier solutions, focusing on sustainable packaging through its ProActive Sustainability platform.

UFlex Ltd.: Providing Advanced High-Barrier Films for Eco-Friendly PET Lidding Applications

UFlex is a leading flexible packaging manufacturer with products for lidding applications including high-barrier, metallized, and Alox-coated films. The recent launch of the patented BOPET F-UHB-M film aims to replace aluminum foil in packaging. Its vertically integrated business model enables rapid development of customized solutions. UFlex’s strategic focus is on sustainable, innovative flexible packaging, including recycling post-consumer waste and reducing environmental impact.

PET Lidding Films Market Share Insights, 2025-2034

Fresh Produce Leads Market Share by Application in the PET Lidding Films Industry

Fresh produce applications dominate the PET lidding films market with 28% share, underscoring the critical role of modified atmosphere packaging (MAP) in extending the shelf life of fruits, vegetables, and herbs. This segment benefits from strong global demand for pre-cut, washed, and ready-to-eat products that prioritize convenience and freshness. PET lidding films are engineered with precision micro-perforations to balance oxygen and carbon dioxide exchange, slowing respiration rates and significantly reducing spoilage across distribution channels. The rise of urban lifestyles and increased consumer preference for healthy, minimally processed foods further reinforce this leadership. Dairy products follow closely at 22%, driven by high-volume usage in yogurt cups, dessert pots, and cheese trays, where seal integrity and consumer-friendly peelability are essential. Meanwhile, ready-to-eat meals are the fastest-growing sub-segment, requiring high-performance lidding films that withstand microwave heating and offer steam-venting technologies. Meat, poultry, and seafood applications represent a high-value share, demanding ultra-high oxygen barrier films to prevent discoloration and microbial growth. Niche categories such as bakery, confectionery, pet food, and pharmaceuticals also contribute to steady demand, where PET lidding delivers aroma retention, premium visibility, and sterile protection in regulated applications. Collectively, the dominance of fresh produce reflects how sustainability, convenience, and food waste reduction converge to define this market’s growth trajectory.

Trays Dominate Market Share by Packaging Format in the PET Lidding Films Industry

Trays account for 52% of PET lidding film demand, solidifying their role as the most widely adopted format across fresh produce, ready-to-eat meals, and meat packaging. Their rigid structure ensures stability during transportation, excellent product visibility, and compatibility with MAP systems, making them the preferred choice for high-volume retailers and meal kit providers. The surge in convenience-driven food consumption, coupled with the popularity of portioned fresh produce and microwaveable meal trays, continues to expand tray demand. Cups and bowls represent the second-largest format, underpinned by their central role in the dairy industry where leak-proof seals, durability, and consumer convenience are paramount. Vials, while smaller in volume, command importance in specialized sectors such as pharmaceuticals, diagnostics, and premium spices, where lidding films with multilayer foil barriers provide the ultimate protection. Cans remain a legacy format, primarily for powdered nutrition, protein mixes, and niche non-food applications, where full-aperture lidding supports resealability and user convenience. Overall, trays remain the anchor of PET lidding demand, reflecting a balance between consumer visibility, operational efficiency, and extended shelf-life performance in both food and non-food applications.

United States PET Lidding Films Market Driven by Innovation and Recycling Initiatives

The United States PET lidding films market is rapidly advancing with strong adoption of high-performance solutions for refrigerated and frozen food packaging. Toray Plastics (America), Inc. leads the market with its LumiLid® series of peelable lidding films, designed to offer convenience, durability, and superior seal performance. A notable shift is occurring as manufacturers replace conventional aluminum foil with metalized PET (MET PET), which offers enhanced oxygen and moisture barriers at lower cost. The adoption of clear, high-barrier PET films with specialized coatings is gaining momentum, as consumers increasingly demand visibility into packaged foods.

The U.S. market is also witnessing strong innovation in dual-ovenable PET lidding films, which withstand both microwave and conventional oven heating up to 220°C, making them essential for the growing ready-to-eat meal sector. A further transition from rigid clamshells to lightweight PET lidding films for produce trays is reducing costs and plastic usage. Sustainability is another key driver, with the Association of Plastic Recyclers (APR) piloting municipal recycling projects to process household flexible packaging, including lidding films. This regulatory and consumer-driven push is accelerating the adoption of recyclable and compostable PET lidding films across food, beverage, and meal prep categories.

Germany PET Lidding Films Market Expands with Sustainable and High-Barrier Innovations

The Germany PET lidding films market is at the forefront of European innovation, with manufacturers transitioning from mono-material PET films to advanced multi-layer structures that combine superior functionality with recyclability. German companies are integrating Polyethylene Terephthalate (PET) for its oxygen barrier performance and clarity, making it the material of choice for sustainable food applications.

The country’s regulatory alignment with the EU Single-Use Plastics Directive is driving investments in biodegradable and compostable PET lidding films. High-barrier films for perishable goods are particularly in demand, with manufacturers catering to both extended shelf life requirements and eco-friendly mandates. Furthermore, German producers are innovating with lidding films for dairy, meat, and prepared meals, emphasizing convenience features such as peelability and resealability. This combination of strict regulatory compliance, advanced R&D, and consumer sustainability preferences makes Germany a leading hub for sustainable PET lidding films in Europe.

United Kingdom PET Lidding Films Market Strengthened by EPR and Flexible Plastic Regulations

The United Kingdom PET lidding films market is undergoing a transformation due to Extended Producer Responsibility (EPR) regulations that make producers accountable for packaging waste. Companies like KM Packaging have responded with sustainable product ranges such as K-Peel® and K-Reseal® films, designed for both recyclability and consumer convenience. At the same time, the UK government’s mandate for flexible plastics collection by March 2027 is creating a strong incentive for mono-material PET lidding films.

Industry leaders like Mars are also reshaping the market with recyclable mono-material pouches and lidding solutions for pet food, which balance shelf life with sustainability goals. The Flexible Plastic Fund’s 2025 report outlines scalable collection and recycling models, expected to significantly increase adoption rates. Consumer demand is strongly aligned with eco-friendly food packaging, accelerating the shift toward recyclable, resealable PET lidding films for dairy, ready meals, and perishable products.

China PET Lidding Films Market Boosted by Regulation and E-Commerce Growth

The China PET lidding films market is expanding rapidly, driven by government regulations like GB 23350-2021, which target excessive packaging and encourage thinner, lighter materials. Companies such as GreenPak are producing anti-fog, peelable, and high-barrier PET lidding films tailored for seafood, meat, and fresh produce. These technologies are essential in a market where online grocery platforms and food delivery services are rapidly growing.

China is also seeing increased investments in bio-PET and recyclable lidding films, reflecting consumer preferences for sustainable packaging solutions. With the growth of the urban workforce and convenience culture, demand is rising for ready-to-eat and pre-packaged meals, fueling adoption of high-barrier PET films. Domestic manufacturers are scaling up production capacity while enhancing performance features like clarity, barrier strength, and peelability to stay competitive.

India PET Lidding Films Market Expands with Domestic Investments and Regulatory Push

The India PET lidding films market is accelerating, fueled by both government regulations and corporate investments. Jindal Poly Films has invested over INR 700 crore to establish new PET and other film lines in Nashik, reinforcing India’s status as one of the world’s largest flexible film producers. Similarly, Uflex Limited is leveraging its Flexfresh™ Modified Atmosphere Packaging technology, which incorporates nano-perforation to extend freshness, a feature increasingly being applied to lidding films.

The ban on single-use plastics enforced on July 1, 2022, has pushed manufacturers to adopt recyclable and compostable PET film alternatives. Rising urban demand for fresh produce, bakery, and ready-to-eat meals further strengthens the market, particularly with the growth of e-commerce platforms requiring robust and visually appealing packaging. With Cosmo Films and other exporters expanding their specialty film portfolios, India is becoming a key global hub for PET lidding films production.

Japan PET Lidding Films Market Driven by Freshness Preservation and Recycling Goals

The Japan PET lidding films market is being shaped by demographic shifts and sustainability goals. With an aging population and health-conscious consumers, demand is rising for advanced food preservation packaging that extends shelf life and ensures safety. Local players such as Toppan Inc. and RM Tohcello Co. Ltd. are collaborating on innovations to enhance barrier and sealing properties of PET lidding films.

The country’s e-commerce and home delivery expansion is driving demand for protective and breathable packaging formats, particularly for meal kits and fresh foods. Moreover, the Japan Soft Drink Association’s goal of achieving 50% bottle-to-bottle recycling by 2030 encourages packaging companies to develop recyclable PET lidding films in line with broader circular economy goals. Japan’s expertise in precision manufacturing and material science positions it as a global leader in premium, functional, and sustainable PET lidding films.

PET Lidding Films Market Report Scope

PET Lidding Films Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$2.3 Billion

|

|

Market Size (2034)

|

$3.9 Billion

|

|

Market Growth Rate

|

6.1%

|

|

Segments

|

By Material (PET, PE, PP, PA, Others), By Functionality (High Barrier, Anti-fog, Peelable, Resealable, Breathable, Dual-Ovenable), By Application (Fresh Produce, Ready-to-Eat Meals, Dairy Products, Meat, Poultry & Seafood, Bakery & Confectionery, Pet Food, Others), By Packaging Format (Trays, Cups & Bowls, Cans, Vials)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, Mondi Group, Coveris, Huhtamaki Oyj, Sealed Air Corporation, ProAmpac, Uflex Limited, Toray Industries, Inc., Innovia Films, KM Packaging Services Ltd., Sonoco Products Company, Winpak Ltd., Bolloré Packaging Films, TCL Packaging Ltd, Jindal Poly Films

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

PET Lidding Films Market Segmentation

By Material

By Functionality

- High Barrier

- Anti-fog

- Peelable

- Resealable

- Breathable

- Dual-Ovenable

By Application

- Fresh Produce

- Ready-to-Eat Meals

- Dairy Products

- Meat

- Poultry & Seafood

- Bakery & Confectionery

- Pet Food

- Others

By Packaging Format

- Trays

- Cups & Bowls

- Cans

- Vials

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in PET Lidding Films Market

- Amcor plc

- Mondi Group

- Coveris

- Huhtamaki Oyj

- Sealed Air Corporation

- ProAmpac

- Uflex Limited

- Toray Industries, Inc.

- Innovia Films

- KM Packaging Services Ltd.

- Sonoco Products Company

- Winpak Ltd.

- Bolloré Packaging Films

- TCL Packaging Ltd

- Jindal Poly Films

* List Not Exhaustive

Methodology

The PET Lidding Films Market report by USDAnalytics is formulated through a rigorous methodology integrating both primary and secondary research to deliver precise, professional-grade insights for industry stakeholders. Secondary research involved comprehensive analysis of company filings, sustainability reports, regulatory documents, press releases, and industry journals to capture the latest advancements in PET lidding films, high-barrier technologies, and sustainable packaging trends. Primary research included interviews with leading packaging manufacturers, R&D experts, and supply chain specialists to validate trends in mono-material adoption, smart labeling, and consumer-preferred functionalities such as easy-peel and resealable films. USDAnalytics employs a robust triangulation approach, combining supply-side data, demand-side insights, and macroeconomic trends to produce reliable projections for market value, CAGR, and segment growth across key regions including the U.S., China, Germany, UK, India, and Japan. The methodology also incorporates regulatory compliance analysis, competitive landscape assessment, and e-commerce packaging optimization trends, ensuring that market participants have actionable insights for strategic planning, investment decisions, and product innovation in the PET lidding films space.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.