PFAS-Free Food Packaging Market Size, Overview, and Growth Outlook (2021–2034)

PFAS-Free Food Packaging Market Forecast to Reach $79.4 Billion by 2034 Amid Rising Regulatory and Consumer Pressure

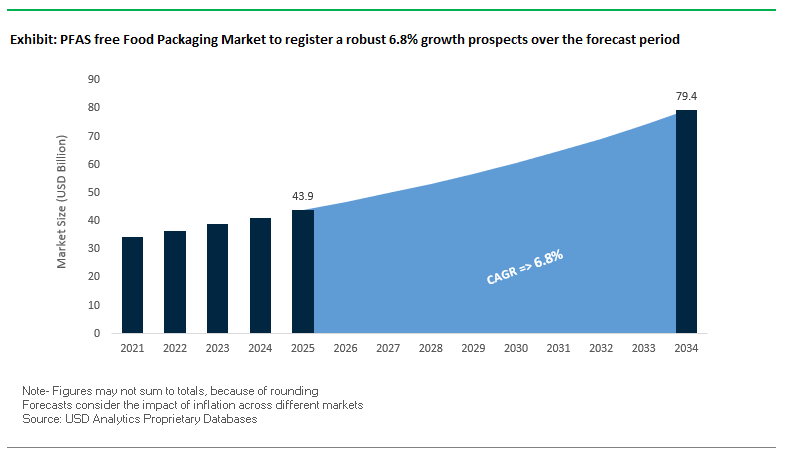

The Global PFAS-Free Food Packaging Market is projected to grow from $43.9 billion in 2025 to $79.4 billion by 2034, achieving a CAGR of 6.8%. PFAS-free packaging eliminates “forever chemicals” traditionally used for grease and water resistance in paper and molded fiber products, offering non-toxic, sustainable alternatives such as plant-based waxes, biodegradable biopolymers, and advanced cellulose-based barriers.

Key Insights for industry professionals and buyers:

- Regulatory Momentum: States like California, New York, and Washington in the U.S., along with EU initiatives, are banning PFAS in food packaging, accelerating the shift to safer alternatives.

- Consumer-Driven Demand: Increasing awareness of health risks associated with PFAS is driving preference for transparent, eco-friendly, and non-toxic packaging.

- Functional Sustainability: Innovative barrier coatings deliver grease and moisture resistance while maintaining compostability and recyclability.

- Technological Investment: Strategic R&D and partnerships are enhancing the scalability and performance of PFAS-free solutions.

- Market Differentiation: Brands leveraging PFAS-free packaging benefit from enhanced consumer trust and competitive positioning.

Market Analysis: PFAS-Free Food Packaging Industry Growth Accelerated by Strategic Collaborations, Regulatory Pressure, and Consumer Preferences

The PFAS-free food packaging market has seen notable developments in innovation, regulatory compliance, and strategic partnerships. In September 2025, Mondi and Saga Nutrition launched recyclable mono-material bags for dry pet food, emphasizing PFAS-free coatings and sustainable films. August 2025 saw ProAmpac release its Sustainability Impact Report highlighting net-zero commitments and circular packaging initiatives, while Zume partnered with Solenis to launch a comprehensive PFAS-free packaging line for food service applications. Regulatory milestones, such as the EU Packaging and Packaging Waste Regulation (PPWR) enforced in February 2025, established strict PFAS limits, further pushing adoption of safer alternatives.

Consumer insights are shaping product development. In June 2025, a U.S. university study highlighted the preference for “less-plastic” packaging, driving the market toward PFAS-free paper and fiber-based solutions. Industry initiatives like the Pet Sustainability Coalition in July 2025 support companies in transitioning to sustainable packaging practices. Investments in high-barrier, recyclable films also continued; Constantia Flexibles invested over €6 million in May 2025 in its MDO line in Germany to produce EcoLamHighPlus, and Berry Global collaborated with VOID Technologies in February 2025 to develop high-performance sustainable films for pet food packaging.

Innovation and sustainability are intertwined with market expansion. In December 2024, Storopack launched PAPERplus Classic CX paper cushioning, reflecting a broader trend toward eco-friendly alternatives. Earlier, in May 2024, Duni Group discontinued PFAS-containing products and joined the ChemSec anti-PFAS movement, demonstrating the growing commitment to chemical safety and consumer health.

Accelerating Trends and Breakthrough Opportunities in the PFAS-Free Food Packaging Market

Accelerated Legislative Bans on PFAS in Food Contact Materials Driving Market Transition

The global PFAS-free food packaging market is experiencing rapid growth, largely fueled by stringent legislative actions and consumer-driven demand for safer alternatives. In the United States, state-level bans are accelerating the pace of change, creating hard compliance deadlines for food packaging manufacturers. As of January 2024, states including Colorado, Connecticut, Maryland, and Minnesota officially banned intentionally added PFAS in food packaging. Several others, such as Illinois and Hawaii, are following with legislation scheduled for 2025. These developments have turned the removal of PFAS from packaging into a non-negotiable priority, forcing immediate innovation in coating and barrier technologies. On a federal level, the FDA announced in February 2024 the voluntary phase-out of grease-proofing agents containing PFAS, effectively closing off the main source of dietary exposure from authorized food contact applications. This set a clear precedent and strong signal across the industry. Meanwhile, large corporations are taking a proactive stance. Retailers and restaurant chains such as Whole Foods, Trader Joe’s, and Chipotle have committed to eliminating PFAS from their packaging portfolios, placing additional pressure on suppliers to accelerate the shift to compliant, PFAS-free alternatives. This convergence of legislative pressure and corporate leadership is driving a market-wide transformation at unprecedented speed.

Strategic Corporate Investment in PFAS-Free Alternative Coating and Material Production

Corporate and industry-level investments are reshaping the PFAS-free packaging landscape, with players moving from reactive compliance toward proactive innovation. Major chemical and packaging companies are scaling up R&D and production of PFAS-free coatings to ensure long-term sustainability and regulatory readiness. Kemira’s collaboration in the EU-funded ZeroF project exemplifies how industry leaders are pooling expertise to fast-track safer coating alternatives. On the commercial side, companies like delfort are introducing bio-based coatings enhanced with natural additives and advanced processes to replicate the oil- and water-resistant properties once offered by PFAS. Similarly, starch-based barrier technologies derived from renewable feedstocks, such as potato or corn, are gaining traction as commercially viable solutions. Another strategic development is the move toward vertical integration, with manufacturers like BYK phasing out PFAS-containing additives and shifting to in-house production of PFAS-free alternatives to ensure consistent supply security. These investments are not only filling the immediate performance gap but also establishing a long-term innovation pipeline, ensuring that PFAS-free packaging meets functional requirements across multiple food categories while enhancing circularity.

Development of High-Performance Grease and Oil Barriers for Fiber-Based Packaging

The most critical opportunity in the PFAS-free packaging market lies in creating high-performance barriers that can deliver oil and grease resistance without fluorinated chemicals. Fiber-based solutions, such as pizza boxes, bakery bags, and fast-food wrappers, have traditionally relied on PFAS coatings, leaving a performance gap that innovators are racing to close. Recent research breakthroughs highlight promising directions: for instance, Northwestern University developed graphene oxide-based coatings that offer exceptional water and oil resistance while strengthening paper substrates. At the same time, industry players like Cargill are commercializing biodegradable starch-based barrier coatings that combine functionality with end-of-life sustainability. These starch-based solutions have proven effective in resisting oil and grease, making them practical replacements for PFAS in short-contact packaging applications. As quick-service restaurants and bakery chains seek immediate compliance solutions, high-performance PFAS-free grease barriers represent one of the most commercially scalable and environmentally critical opportunities.

Innovation in Home-Compostable Packaging for Fast-Casual and Delivery Sectors

The intersection of PFAS bans and compostability targets creates a second major opportunity: the development of home-compostable food packaging that can handle hot, greasy foods. While many existing solutions are limited to industrial composting, consumer preference is shifting toward backyard compostable options that offer convenient end-of-life disposal. Packaging innovators are responding with molded fiber trays and containers lined with advanced bio-polymer coatings that resist oil and moisture while still being certified home compostable. These solutions are particularly attractive for the booming fast-casual dining and food delivery markets, where greasy, high-temperature foods present significant packaging challenges. By eliminating PFAS while meeting compostability standards, these new materials enable restaurants and delivery platforms to align with consumer expectations for sustainability, comply with upcoming state and municipal regulations, and reduce landfill contributions. This opportunity not only addresses an urgent regulatory challenge but also positions PFAS-free, compostable packaging as a premium differentiator in the competitive foodservice market.

Competitive LandscapeLeading PFAS-Free Food Packaging Companies Are Driving Innovation Through Sustainability, Chemical Expertise, and Strategic Partnerships

The PFAS-free food packaging industry is shaped by key players leveraging materials science, chemical innovation, and sustainable manufacturing to meet growing regulatory and consumer demand.

Solenis LLC: Partnering for High-Performance PFAS-Free Barrier Coatings

Solenis provides water-based barrier coatings and functional additives for paper and paperboard, delivering grease, oil, and water resistance without fluorochemicals. In August 2025, Solenis partnered with Zume to launch a PFAS-free packaging line for food service applications. Its strengths lie in specialty chemical expertise, strong R&D capabilities, and ability to support regulatory compliance. The company’s strategy focuses on developing innovative, non-toxic coatings to meet growing sustainability demands.

Kemira Oyj: Developing Sustainable Barrier Solutions Through Collaborative Innovation

Kemira offers PFAS-free barrier coatings and sizing agents for fiber-based packaging. The company participates in the EU-funded ZeroF project, aiming to find safe alternatives to PFAS. Its expertise in wet-end and surface chemistry enables efficient and cost-effective application during paper manufacturing. Kemira’s strategic focus is leading sustainable chemical solutions and anticipating regulatory trends to provide compliant, high-performance packaging.

ProAmpac: Expanding Flexible PFAS-Free Films With Circular Economy Initiatives

ProAmpac delivers PFAS-free flexible films and pouches, including the ProActive Recyclable series. Its Sustainability Impact Report demonstrates commitment to net-zero emissions and circular packaging initiatives. The company also acquired a flexible packaging manufacturer to expand capacity. Core strengths include innovation in materials science and high-barrier solutions, while its strategy emphasizes recyclable and compostable packaging for food and pet care markets.

Huhtamaki Oyj: Driving Sustainable Food Packaging Through Global Reach and Material Expertise

Huhtamaki provides PFAS-free paper, fiber-based containers, trays, and molded fiber products. Collaborations with SABIC and Mars Petcare focus on circular polypropylene and PFAS-free materials. Strengths include global manufacturing footprint and material versatility, supporting brands with comprehensive packaging solutions. The company’s strategy is aligned with 2030 sustainability goals for fully recyclable, reusable, or compostable packaging.

Constantia Flexibles Group GmbH: Investing in High-Barrier, Easily Recyclable PFAS-Free Films

Constantia Flexibles offers high-barrier films like EcoLamHighPlus, supporting freshness and extended shelf life. In May 2025, the company invested over €6 million in an MDO line in Germany to enhance production of sustainable, PFAS-free films. Strengths include innovation in flexible packaging materials and customized solutions, with a strategic focus on developing sustainable, high-performance films that meet evolving market and regulatory demands.

PFAS free Food Packaging Market Share Insights, 2025-2034

Plates, Cups & Bowls Dominate Market Share by Packaging Type in PFAS-Free Food Packaging

Plates, cups, and bowls represent 32% of the PFAS-free food packaging market, positioning themselves at the forefront of regulatory-driven adoption. This dominance is directly linked to the widespread bans in U.S. states such as Maine, Washington, and New York, which explicitly targeted single-use food service ware as a major source of PFAS contamination. With QSRs, catering services, and institutional buyers under pressure to replace legacy products quickly, this category has experienced accelerated uptake of compliant alternatives such as clay-coated and bio-polymer–lined fiberware. Containers and boxes follow closely at 28%, driven by fast-food clamshells, bakery trays, and grocery takeout packaging, where replicating PFAS’ grease resistance is both a technical and commercial challenge. Bags and wraps, while significant in volume, lag in adoption due to the complexity of reformulating barrier properties for oily or greasy foods like fries and popcorn. Meanwhile, lids, closures, and specialty liners are high-value but niche segments, where performance precision often dictates a higher cost premium. The dominance of plates, cups, and bowls highlights how legislation and high-volume foodservice demand have reshaped adoption curves in PFAS-free packaging.

Quick-Service Restaurants Drive Market Share by End-User in PFAS-Free Food Packaging

Quick-service restaurants (QSRs account for 35% of PFAS-free packaging demand), making them the single most influential end-user segment. Their dominance is a direct result of both scale and visibility, as QSR chains face intense consumer scrutiny and NGO pressure regarding the use of “forever chemicals.” Leading fast-food brands have proactively phased out PFAS-treated packaging to protect brand reputation and align with ESG reporting, setting a precedent for the broader foodservice industry. Retailers hold the second-largest share at 25%, leveraging their role as market gatekeepers by enforcing PFAS-free requirements across private labels and even third-party brands. Food and beverage manufacturers are aggressively transitioning away from PFAS coatings to safeguard consumer trust, with adoption particularly strong in high-risk categories such as popcorn bags, bakery wrappers, and frozen food trays. Catering services, institutions, and smaller operators remain slower adopters, constrained by regional legislation and cost sensitivity. Overall, QSRs’ leadership highlights how brand visibility, regulatory compliance, and consumer trust converge to position this segment as the catalyst for rapid PFAS-free packaging adoption across the industry.

United States PFAS-Free Food Packaging Market Led by Regulation and Quick-Service Chains

The United States PFAS-free food packaging market is rapidly expanding as multiple states—including New York and Washington—have enacted bans on intentionally added PFAS in fiber-based food packaging between 2022 and 2024. These state-level actions, combined with the FDA’s revocation of specific PFAS authorizations, are accelerating the phase-out of fluorinated chemicals in packaging. Major quick-service restaurant (QSR) chains, including McDonald’s and Restaurant Brands International, have pledged to globally eliminate PFAS from all packaging by 2025, driving supplier innovation.

Companies and research institutions are commercializing next-generation barrier technologies, such as graphene-oxide-based GO-Eco coatings, that deliver grease and moisture resistance without fluorinated additives. A significant push is also underway for plant-based, fiber-molded packaging alternatives that align with sustainability goals while ensuring performance in food-contact applications. Transparency is increasingly critical, with retailers demanding certified PFAS-free packaging and clear labeling to assure eco-conscious consumers. These combined regulatory, corporate, and consumer pressures are positioning the U.S. as a global leader in PFAS-free food packaging innovation.

Europe PFAS-Free Food Packaging Market Driven by PPWR and Circular Economy Goals

The Europe PFAS-free packaging market is undergoing transformative change under the EU Packaging and Packaging Waste Regulation (PPWR), which took effect in February 2025. From August 2026 onward, strict thresholds on individual PFAS, total PFAS, and total organic fluorine content will apply to food-contact packaging. This regulatory shift is forcing brands to adopt safer, PFAS-free barrier technologies and invest in recyclable and compostable materials.

Companies such as Tosaf are pioneering PFAS-free additives for flexible plastic packaging, replacing conventional fluoroelastomer-based aids. Meanwhile, the European Food Safety Authority (EFSA) is reviewing and validating alternative barrier materials to ensure compliance with food safety standards. Market momentum is firmly aligned with circular economy principles, as companies innovate around single-material packaging formats that are both recyclable and free of harmful substances. Europe’s stringent regulatory environment, combined with corporate sustainability commitments, is making the region a hub for PFAS-free packaging innovation.

China PFAS-Free Food Packaging Market Advancing Through Standards and Material Innovation

The China PFAS-free food packaging market is being shaped by the government’s GB 23350-2021 regulation, which restricts excessive packaging, pushing brands to optimize material usage. The new GB 4806.15-2024 standard for adhesives, effective February 2025, strengthens compliance for food-contact safety, creating opportunities for PFAS-free barrier materials.

China’s booming e-commerce grocery sector is amplifying demand for high-barrier PFAS-free packaging that ensures safety during transit. Local manufacturers are scaling up the production of sustainable films and coatings, while partnerships with academic institutions are commercializing cutting-edge solutions. A key example is the graphene-oxide coating developed with Chang Robotics and Northwestern University, now being piloted by multiple companies to replace PFAS in paper-based packaging. The combination of regulatory alignment, e-commerce growth, and scientific innovation is driving strong momentum in China’s PFAS-free packaging adoption.

Canada PFAS-Free Food Packaging Market Strengthened by Chemicals Management Plan

The Canada PFAS-free packaging market is supported by proactive government action through the Chemicals Management Plan (CMP), which evaluates and manages risks associated with PFAS. The federal government has already banned the manufacture, sale, and import of long-chain PFAS, including PFOA and PFOS, and is considering expanding disclosure requirements under Health Canada guidelines.

Major North American foodservice companies, such as Restaurant Brands International, are phasing out PFAS across Canada, accelerating demand for compliant alternatives. Canada’s single-use plastics ban has further boosted the adoption of fiber-based packaging solutions, which require PFAS-free coatings to perform effectively. Retailers and manufacturers are prioritizing consumer transparency through labeling, enabling buyers to identify PFAS-free products. With regulatory action and corporate commitments aligning, Canada is establishing itself as a significant regional market for PFAS-free food packaging.

Australia PFAS-Free Food Packaging Market Accelerated by APCO and Compostable Alternatives

The Australia PFAS-free food packaging market has moved quickly, with the Australian Packaging Covenant Organisation (APCO) setting an action plan to eliminate PFAS from fiber-based food packaging by the end of 2023. Domestic companies like Detpak have launched Vanguard® products, a No Added PFAS sugarcane-based packaging line that is compostable and compliant with national food-safety standards.

The PFAS National Environmental Management Plan (PFAS NEMP) provides a unified framework for managing PFAS contamination, while consumer and regulatory pressure is accelerating the adoption of compostable and biodegradable alternatives. These efforts also prevent PFAS contamination from becoming a barrier to recycling or organic waste processing. The Australian government is complementing industry innovation with site investigations and risk management strategies, ensuring that both environmental and health risks are minimized. Australia is thus positioned as a regional leader in PFAS-free, compostable food packaging.

Japan PFAS-Free Food Packaging Market Anchored in Positive List Compliance and E-Commerce Growth

The Japan PFAS-free food packaging market has entered a new regulatory era with the positive list system for synthetic food-contact materials, which came into effect in June 2025. The Ministry of Health, Labour and Welfare (MHLW) continues to revise its food packaging standards, influencing the shift toward non-fluorinated, high-performance barrier materials.

Japanese companies are investing heavily in PFAS-free coatings and films that balance strict safety compliance with functionality. Collaboration between government, academia, and industry ensures that innovations in sustainable packaging materials are both scientifically validated and commercially viable. The growth of e-commerce and home delivery services in Japan is expanding demand for robust PFAS-free packaging that maintains food freshness during distribution. With its reputation for precision manufacturing and stringent food safety standards, Japan is emerging as a key innovator in PFAS-free food packaging solutions.

PFAS free Food Packaging Market Report Scope

PFAS free Food Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$43.9 Billion

|

|

Market Size (2034)

|

$79.4 Billion

|

|

Market Growth Rate

|

6.8%

|

|

Segments

|

By Material (Paper & Paperboard, Plastics, Biopolymers & Composites, Metals, Glass, Others), By Packaging Type (Containers & Boxes, Bags & Wraps, Plates, Cups & Bowls, Lids & Closures, Liners & Barriers, Others), By Application (Baked Goods, Fast Food & Ready-to-Eat Meals, Fresh Produce, Confectionery, Meat, Poultry & Seafood, Dairy, Others), By End-User (Food & Beverage Manufacturers, QSRs, Retailers, Catering & Food Service, Institutional, Others)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Huhtamaki Oyj, Amcor plc, Mondi Group, Smurfit Kappa Group, International Paper, WestRock Company, Novolex, Graphic Packaging Holding Company, AptarGroup, Inc., ProAmpac, Pactiv Evergreen Inc., Ball Corporation, Detpak, Sealed Air Corporation, Greif, Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

PFAS free Food Packaging Market Segmentation

By Material

- Paper & Paperboard

- Plastics

- Biopolymers & Composites

- Metals

- Glass

- Others

By Packaging Type

- Containers & Boxes

- Bags & Wraps

- Plates

- Cups & Bowls

- Lids & Closures

- Liners & Barriers

- Others

By Application

- Baked Goods

- Fast Food & Ready-to-Eat Meals

- Fresh Produce

- Confectionery

- Meat

- Poultry & Seafood

- Dairy

- Others

By End-User

- Food & Beverage Manufacturers

- QSRs

- Retailers

- Catering & Food Service

- Institutional

- Others

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in PFAS free Food Packaging Market

- Huhtamaki Oyj

- Amcor plc

- Mondi Group

- Smurfit Kappa Group

- International Paper

- WestRock Company

- Novolex

- Graphic Packaging Holding Company

- AptarGroup, Inc.

- ProAmpac

- Pactiv Evergreen Inc.

- Ball Corporation

- Detpak

- Sealed Air Corporation

- Greif, Inc.

* List Not Exhaustive

Methodology

USDAnalytics employs a rigorous, multi-faceted research methodology to provide accurate and actionable insights into the PFAS-Free Food Packaging Market, combining both primary and secondary research sources. Primary research involves interviews with key stakeholders, including packaging manufacturers, chemical suppliers, foodservice companies, and regulatory authorities, capturing first-hand perspectives on market trends, innovations, and compliance challenges. Secondary research draws from verified trade journals, company reports, government publications, and industry databases to validate historical trends and emerging market dynamics. Market sizing, CAGR, and segmentation analysis are derived using a combination of top-down and bottom-up approaches, factoring in regulatory mandates, consumer preferences for chemical-free packaging, technological advancements in barrier coatings, and investments in biopolymers and cellulose-based alternatives. USDAnalytics also integrates insights from strategic partnerships, corporate sustainability initiatives, and regional adoption patterns to deliver a holistic view of growth opportunities, material innovations, and functional performance trends, ensuring industry professionals receive a comprehensive, forward-looking perspective for informed decision-making.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.