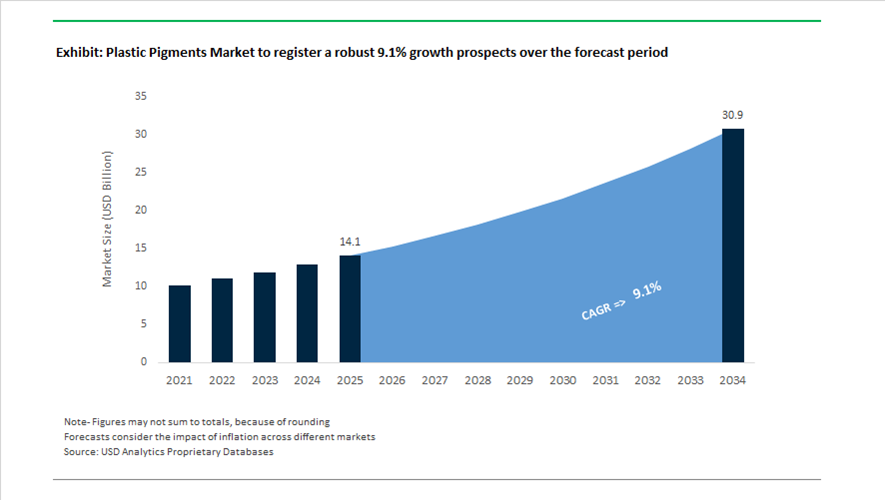

Plastic Pigments Market Size 2025–2034: $14.1 Billion to $30.9 Billion at 9.1% CAGR Fueled by EV Components, NIR-Compatible Colorants, and PFAS-Free Innovation

The global plastic pigments market is projected to expand from $14.1 billion in 2025 to $30.9 billion by 2034, registering a robust CAGR of 9.1%. Growth is being driven by rising demand for high-performance colorants in automotive plastics, EV battery housings, consumer packaging, construction materials, and engineered polymers. As plastics increasingly replace metals in lightweight vehicle structures and smart infrastructure, pigment technologies must deliver enhanced UV stability, thermal resistance, low warpage, NIR transparency, and regulatory compliance. The shift toward recyclable and sensor-compatible plastics is accelerating innovation in organic pigments, effect pigments, and specialty color systems.

Industry consolidation significantly reshaped the competitive environment in 2025. On March 3, 2025, Sudarshan Chemical Industries finalized acquisition of Germany-based Heubach Group, creating a global pigment powerhouse across 19 international sites. The transaction integrates Heubach’s technological legacy with Sudarshan’s manufacturing scale to strengthen supply in plastics, coatings, and inks. In early 2026, Sudarshan launched a Global Capability Center in partnership with Genpact to unify operations under an AI-enabled global model, reinforcing efficiency and digitalized production in plastic pigment manufacturing.

Automotive and EV applications are central growth catalysts. In October 2025, BASF Coatings introduced its 2025–2026 Automotive Color Trends collection, featuring interference pigments such as Tesseract Blue and liquid-metal effect shades optimized for sensor-integrated plastic body panels. In January 2026, Sun Chemical launched Spectrasense™ Black K 0089 FK, engineered for Near-Infrared (NIR) light management in LiDAR-enabled autonomous vehicles. Unlike conventional carbon black, this pigment allows laser transparency and sensor functionality while maintaining deep-black aesthetics—critical for modern automotive exterior plastics.

Sustainability-driven formulation is accelerating across the plastic pigments industry. In November 2024, Clariant completed transition to a fully PFAS-free additive portfolio, impacting polymer processing aids used in plastic extrusion and compounding. Its AddWorks® PPA line offers melt fracture control without fluorinated chemistries, aligning with global regulatory shifts. In 2025, Sun Chemical enhanced its Pigment Finder digital platform by integrating Product Carbon Footprint data, enabling plastic manufacturers to assess environmental impact in real time when selecting pigments for eco-label and sustainability compliance.

Innovation in specialty pigments continues to target premium segments. At CHINACOAT 2025, Sun Chemical unveiled Glacier™ Exterior Ceramic White S1303M, a synthetic mica pearl pigment delivering high-luster, weather-resistant finishes for automotive and industrial plastic components. In January 2026, the company expanded its Heliogen® phthalocyanine pigment range, offering ultra-high purity grades suitable for food packaging and children’s toys while minimizing warpage in HDPE injection molding. Additionally, DIC Corporation showcased BURNOCK® WD-569 high-adhesion resin systems for engineering plastics used in EV battery casings and sustainable infrastructure components.

Regional R&D investments are strengthening market responsiveness. In February 2026, Toyo Ink India inaugurated a research center in Bengaluru focused on high-performance colorants for India’s expanding plastics, automotive, and packaging industries.

Key Trends and High-Impact Opportunities in the Plastic Pigments Market

Regulatory-Driven Transition Toward Heavy-Metal-Free and High-Performance Pigment Systems

The plastic pigments market is undergoing a structural compliance-driven transformation as heavy-metal-based pigments move from being commercially discouraged to legally untenable across major manufacturing economies. Regulatory tightening under frameworks such as U.S. TSCA, EU REACH, and rapidly evolving Asian plastics governance has made the elimination of lead-, cadmium-, and chromium-based pigments a baseline requirement rather than a sustainability differentiator. For pigment suppliers, this has accelerated a decisive pivot toward Complex Inorganic Color Pigments (CICPs) and High-Performance Organic Pigments (HPOs) that can withstand the high processing temperatures of engineering plastics while meeting toxicological and migration thresholds.

A notable regulatory inflection point occurred in June 2025 when India’s Ministry of Environment, Forest and Climate Change notified the Plastic Waste Management (Second Amendment) Rules, 2025. The regulation mandates full traceability of plastic packaging through a centralized digital portal and enforces minimum recycled-content targets, including 30% recycled plastic for rigid packaging in 2025–26. This framework effectively disqualifies non-compliant pigments, as recycled resin streams amplify contamination risks. As a result, heavy-metal-free pigment chemistries have become a prerequisite for masterbatch suppliers servicing FMCG and packaging majors operating in India.

On the supply side, producers are reallocating capital toward compliant inorganic systems. Lanxess has expanded its Colortherm iron oxide pigment portfolio for biodegradable and compostable plastics, engineered to meet stringent heavy-metal thresholds required for industrial compostability certifications. These pigments allow processors to avoid costly secondary screening and safeguard downstream recyclability. Parallel to this, strategic portfolio realignment is visible among diversified chemical groups. In May 2025, BASF initiated steps to potentially divest its coatings business, a move widely interpreted as a capital redeployment toward higher-margin, R&D-intensive specialty materials, including organic HPPs with superior lightfastness, migration resistance, and thermal endurance for automotive and electronics polymers.

Emergence of Multi-Functional “Smart” Pigments for Digital Traceability and Performance Enhancement

Beyond coloration, pigments are increasingly being engineered as functional materials that embed traceability, protection, and performance directly into plastic substrates. This shift reflects mounting regulatory and brand-owner pressure to ensure permanent identification, anti-counterfeiting, and lifecycle traceability without adding labels, inks, or secondary processing steps.

Laser-markable pigments represent a key growth vector within this trend. In 2025, Merck Group expanded its Iriotec® 8000 series, enabling high-contrast laser marking on plastics through localized foaming or carbonization mechanisms. These pigments allow medical devices, pharmaceutical packaging, and food-contact plastics to be permanently marked at high line speeds and reduced laser energy inputs, improving throughput while eliminating consumables such as inks or solvents. The value proposition extends beyond compliance, as laser-markable pigments reduce operational complexity and support serialization mandates in regulated industries.

Simultaneously, pigment manufacturers are integrating nanoscale functionalities into traditional colorants. In October 2025, Fineland Chemical announced the use of nanotechnology to enhance thermal conductivity and UV-opacity in plastic pigments. These pigments function as dual-purpose additives, contributing both coloration and protective performance in applications such as 5G infrastructure housings and advanced consumer electronics. This convergence of pigment chemistry and materials science is redefining competitive differentiation, particularly in high-performance polymer segments where durability and signal integrity are critical.

Circular Economy Enablement Through NIR-Detectable and Recycling-Compatible Pigments

One of the most commercially significant opportunities in the plastic pigments market lies in solving the long-standing “carbon black problem.” Conventional carbon black absorbs near-infrared light, rendering black plastics invisible to optical sorting systems and effectively excluding them from high-value recycling streams. As recycled content mandates tighten globally, this technical limitation has become a bottleneck for circular packaging strategies.

In December 2025, UPM launched UPM Circular Renewable Black™, the world’s first bio-based, NIR-detectable, and carbon-negative black pigment. Produced from renewable lignin at UPM’s €1.3 billion Leuna biorefinery in Germany, the pigment enables black plastic packaging to be accurately identified and sorted using existing NIR infrastructure. This innovation directly addresses one of the most persistent barriers to closed-loop recycling for premium packaging and positions NIR-detectable pigments as a strategic procurement requirement for brand owners with circularity commitments.

Complementing this, Vibrantz Technologies has introduced NIR-reflective pigment systems tailored for polypropylene and PET. Validation trials at large-scale sorting facilities such as those operated by TOMRA have demonstrated recovery rates for dark plastics approaching those of transparent resins. This creates a scalable, cost-effective alternative to packaging redesign, opening a sizeable retrofit opportunity across existing product portfolios.

Specialized Pigment Formulations for Industrial Additive Manufacturing and Digital Production

Industrial additive manufacturing and digital printing are creating a structurally new demand profile for plastic pigments. Unlike conventional molding, professional 3D printing requires pigments that maintain chromatic stability at extreme processing temperatures, disperse uniformly at sub-micron levels, and remain chemically inert to prevent nozzle fouling and layer defects.

By late 2025, industry assessments indicated a marked shift toward high-purity pigment dispersions for inkjet-based and polymer extrusion additive manufacturing systems. As digital printing penetrates packaging and functional prototyping, pigment suppliers are prioritizing ultra-fine particle size control and long-term dispersion stability in liquid and filament formats. These attributes are now critical performance specifications rather than optional enhancements.

Sustainability is amplifying this opportunity. In July 2025, Nature Coatings expanded the commercialization of BioBlack, a 100% bio-based and carbon-negative alternative to petroleum-derived carbon black. While initially adopted in coatings, BioBlack is increasingly being specified for 3D printing filaments, where professional users and OEMs are mandating non-toxic, renewable inputs for rapid prototyping and short-run production. This positions bio-based pigments at the intersection of additive manufacturing growth and ESG-driven material selection.

Plastic Pigments Market Share and Segmentation Insights

Inorganic Pigments Lead Plastic Pigment Demand with Titanium Dioxide and Carbon Black Dominating Polymer Coloration

Inorganic pigments accounted for 48.60% of the Plastic Pigments Market by pigment type in 2025, reflecting their widespread use in thermoplastic compounding and polymer coloration. Materials such as titanium dioxide, iron oxides, carbon black, and chromium oxide provide excellent heat stability, UV resistance, and opacity required for plastic processing across packaging, automotive components, and consumer goods. Titanium dioxide remains the most important white pigment for plastics, while carbon black is widely used for UV protection and black coloration in polymer products. In 2025, titanium dioxide optimization in plastic masterbatch formulations is gaining importance as compounders reduce pigment loading through improved dispersion technologies and use opacifying extenders to maintain brightness and coverage while controlling formulation costs.

Packaging Sector Drives Plastic Pigment Consumption Across Rigid and Flexible Plastic Products

Packaging represented 48.60% of the Plastic Pigments Market by application in 2025, reflecting the extensive use of colorants in plastic bottles, containers, films, caps, and closures used in consumer packaging systems. Pigments are essential for brand differentiation, product visibility, and UV protection in packaging materials produced from polyethylene, polypropylene, and PET. The large global scale of plastic packaging production continues to sustain strong pigment demand. In 2025, the circular economy transition in plastic packaging is influencing pigment selection strategies, with manufacturers prioritizing pigment masterbatches compatible with recycling streams and colorants designed to maintain performance through multiple mechanical recycling cycles.

Plastic Pigments Market Competitive Landscape

The global plastic pigments market is undergoing consolidation and a shift toward high-performance, UV-stable, and recyclable-compatible pigments. Competitive dynamics are shaped by premium effect pigments, digital pigment management, and sustainable chemistries aligned with circular plastics and regulatory-driven material innovation.

DIC Leads High-Chroma Effect Pigments with Advanced Automotive and Electronics Applications

DIC Corporation, through Sun Chemical, maintains global leadership in plastic pigments with a strong focus on functional performance and aesthetics. The launch of Paliocrom® Brilliant Ruby L 3558 delivers high-intensity bluish-red aluminum effect pigments for automotive plastics with superior hiding power and brilliance. The Glacier Exterior Ceramic White S1303M pigment introduces synthetic mica-based pearl technology for high-purity white shades in consumer electronics and motorcycle plastics. Expansion into South Asia through PAINTINDIA 2026 strengthens regional presence in automotive and architectural plastics. Digital transformation initiatives enhance color consistency and supply chain transparency for masterbatch producers. Product strategy emphasizes high-chroma pigments, UV stability, and advanced effect materials.

Sudarshan-Heubach Builds Global Pigment Platform with Lead-Free Innovations and Expanded Manufacturing Footprint

Sudarshan Chemical Industries, following the acquisition of Heubach Group in March 2025, has created a global pigment platform across 19 sites and 33 stock points. Integration under the “ONE Sudarshan” strategy combines European technical expertise with large-scale Indian manufacturing. Establishment of a Frankfurt-based global headquarters supports unified operations across Europe and the Americas. The company is promoting lead-free pigment dispersions targeting automotive and construction plastic applications. A ₹1,000 crore Qualified Institutional Placement supports restructuring and optimization of acquired assets. Portfolio expansion includes organic, inorganic, and anti-corrosive pigments aligned with high-performance plastic applications.

BASF Strengthens High-Performance Plastic Pigments with Verbund Integration and Circular Economy Technologies

BASF SE is focusing on specialty pigments and dispersions for high-performance plastics under its “Winning Ways” strategy. The divestment of its decorative paints business enables concentration on industrial and automotive plastic pigments. Expansion at the Zhanjiang Verbund site enhances production of intermediates used in advanced pigment synthesis. The company reported €59.7 billion in sales in 2025, supported by €1.3 billion in free cash flow for reinvestment. Collaboration with Borealis and SINTEF on pyrolysis oil upgrading ensures compatibility of pigments with chemical recycling processes. Strategy centers on sustainable pigment technologies, circular plastics integration, and high-margin specialty applications.

Chemours Optimizes TiO₂ Portfolio with Digital Platforms and High-Value Plastic Applications

The Chemours Company is focusing on high-performance titanium dioxide pigments for plastics through its Ti-Pure™ portfolio. The sale of its Taiwan facility for $360 million supports debt reduction and strategic repositioning toward Western markets. A global TiO₂ price increase in December 2025 addresses rising raw material costs and supports continued R&D investment. The Titanium Technologies segment reported $2.43 billion in sales in 2025 with a 6% adjusted EBITDA margin. Ti-Pure™ Connect provides digital tools for formulation optimization and real-time pigment performance tracking. Strategy emphasizes pricing discipline, digitalization, and high-value plastic pigment applications.

Tronox Expands Titanium Pigment Supply with Vertical Integration and India Market Growth

Tronox Holdings plc leverages its vertically integrated mining-to-pigment model to ensure supply stability in the plastic pigments market. The closure of its Fuzhou plant in January 2026 reflects strategic retrenchment from low-margin operations. The company reported a 13% increase in TiO₂ volumes in Q4 2025, driven by strong demand in India’s plastics and coatings sectors. Inventory optimization generated $53 million in free cash flow, supporting a positive financial outlook for 2026. The company is exploring rare earth element recovery from mineral sands tailings to diversify revenue streams. Strategy focuses on cost control, vertical integration, and expansion in high-growth markets.

Clariant Advances Sustainable Plastic Pigments with Circular Economy and Low-Carbon Innovation

Clariant AG is strengthening its position in plastic pigments through sustainability-focused innovation and operational efficiency. The company reported a 17.8% EBITDA margin in 2025, supported by cost optimization and performance improvement initiatives. Development of pyrolysis oil upgrading technology ensures pigment compatibility with recycled plastics and supports circular economy goals. Approximately 18.8% of sales are derived from innovation products with lower carbon footprints and safer chemical profiles. The company is expanding applications in agricultural plastics, including smart mulch films with enhanced stability and environmental compatibility. Strategy emphasizes eco-friendly pigments, regulatory compliance, and circular material integration.

India Plastic Pigments Market: Global Consolidation, PCPIR Investments, and High-Performance Organic Pigment Expansion

India is rapidly transforming into a global hub for plastic pigments manufacturing, shifting from a supplier of intermediates to a high-value producer of high-performance organic pigments (HPPs). A defining milestone in the India plastic pigments market is the March 2025 acquisition of Heubach Group by Sudarshan Chemical Industries Ltd., positioning India as a top-tier global pigment supplier with a diversified portfolio across azo pigments, phthalocyanine pigments, and specialty colorants for plastics. This consolidation significantly enhances India’s footprint in automotive plastics, packaging materials, and engineering polymers, strengthening export competitiveness.

Government-backed infrastructure through Petroleum, Chemicals and Petrochemicals Investment Regions (PCPIRs) has attracted over ₹41,900 crore (~$5 billion) in investments, particularly in hubs like Dahej, accelerating the development of advanced masterbatch production and pigment dispersion technologies. Domestic capacity expansions at Sudarshan’s Roha and Mahad facilities are addressing rising demand from automotive lightweighting and high-clarity packaging applications. Additionally, Indian manufacturers are increasingly adopting nanopigment technology, delivering superior UV resistance, weatherability, and scratch durability, essential for South Asia’s harsh climatic conditions. With the introduction of stricter Bureau of Indian Standards (BIS) Quality Control Orders (QCOs) in 2025–2026, the market is witnessing a transition toward heavy-metal-free, environmentally compliant pigment formulations, reinforcing India’s leadership in sustainable plastic pigments.

Germany Plastic Pigments Market: Circular Economy Compliance, Smart Pigments, and Green Hydrogen Integration

Germany remains the technology leader in the global plastic pigments market, driven by circular economy mandates, advanced material innovation, and strict EU regulatory compliance. The expansion of perylene pigment production by Sun Chemical (DIC Corporation) in Ludwigshafen (2025), adding ~200 metric tons capacity, underscores Germany’s strength in high-performance pigments for engineering plastics and industrial applications. These pigments are critical for high-temperature polymers used in automotive, electronics, and construction sectors.

Sustainability innovation is central to Germany’s strategy, with companies like BASF and Heubach introducing water-free, biocide-free pigment preparations such as HEUCODUR® Green 630, a chrome-free spinel pigment with high thermal stability. Germany is also at the forefront of enforcing the EU Packaging and Packaging Waste Regulation (PPWR), which mandates strict heavy metal limits (≤100 mg/kg for Pb, Cd, Hg, Cr6+) in plastic packaging pigments by 2026, accelerating the adoption of non-toxic, recyclable pigment systems. At the Ludwigshafen Verbund site, BASF’s integration of green hydrogen via PEM electrolyzers is reducing the product carbon footprint (PCF) of pigment synthesis. Furthermore, German innovation in laser-markable pigments is enabling ink-free, high-speed traceability solutions in medical devices and electronics, reinforcing Germany’s leadership in smart and functional pigments for advanced polymers.

United States Plastic Pigments Market: Semiconductor Growth, PFAS-Free Transition, and FDA-Driven Compliance

The United States plastic pigments market is being reshaped by semiconductor manufacturing expansion, stringent regulatory oversight, and sustainability-driven product innovation. The rise of the “Silicon Desert” manufacturing corridor in Arizona and Texas is driving demand for high-performance pigments compatible with engineering polymers such as polyphenylene sulfide (PPS), which require thermal stability above 300°C. This is creating opportunities for advanced inorganic and organic pigments used in electronic enclosures and high-temperature applications.

Technological advancements include the launch of Ronaflux by Merck KGaA (2025), a metal-free metallic effect pigment that delivers high brilliance without conductivity or leaching risks, addressing critical requirements in food-contact and electronics applications. Regulatory pressure is intensifying, with the U.S. EPA mandating detailed reporting on PFAS-containing pigments starting December 2025, accelerating the transition toward PFAS-free, non-toxic pigment chemistries. Additionally, tariff adjustments implemented by Sun Chemical reflect ongoing global supply chain volatility and raw material cost pressures. ESG performance is also becoming a competitive differentiator, as evidenced by EcoVadis sustainability ratings, signaling a shift toward environmentally responsible pigment production and lifecycle transparency in the U.S. plastics industry.

China Plastic Pigments Market: Green Manufacturing, EV-Driven Demand, and High-Purity Pigment Localization

China’s plastic pigments market is transitioning toward a “value-first” manufacturing model, supported by Made in China 2025 policies and stringent environmental enforcement under the “Green Storm” initiative. Strategic collaborations between DIC Corporation and Sun Chemical, showcased at CHINACOAT 2025, highlight the localization of phthalocyanine and azo pigment production tailored for the rapidly expanding electric vehicle (EV) plastics market. This is driving demand for high-durability pigments with superior heat resistance and color stability.

Industrial upgrades in provinces such as Zhejiang and Jiangsu have introduced automated pigment dispersion lines, achieving up to 50% reduction in energy consumption and near-zero wastewater discharge, aligning with China’s low-carbon manufacturing goals. The Jiangbei New Material Technology Park’s Green Transformation initiative has led to a 20% improvement in color retention performance of high-performance pigments (HPPs) compared to 2022 levels. China is also leading in cool roof reflective pigments, which are being widely adopted in plastic construction materials for smart cities, supporting the country’s urban heat island mitigation and 2030 carbon peak targets. Record investments in semiconductor-grade pigments further indicate China’s ambition to achieve self-sufficiency in high-purity colorants for electronics and display technologies.

Japan Plastic Pigments Market: Bio-Based Pigments, Functional Intelligence, and Ultra-High Purity Standards

Japan continues to lead the high-end segment of the plastic pigments market, focusing on ultra-high purity pigments, bio-based colorants, and functional pigment technologies. A key innovation is DIC Corporation’s expansion into spirulina-based biopigments (2025) through its subsidiary Earthrise Nutritionals, targeting food-grade plastics and sustainable packaging applications as alternatives to synthetic azo dyes. This aligns with Japan’s broader push toward bio-based and environmentally friendly pigment solutions.

Japanese companies such as Canon and DIC are pioneering “functional intelligence” pigments, including thermochromic pigments that change color based on temperature, now widely used in cold-chain logistics and supply chain integrity labeling. Government support from METI is accelerating the development of low-dust granular pigment formulations, improving worker safety and precision dosing in automated plastic processing systems. Additionally, advanced R&D has demonstrated that incorporating boron nitride synergists in pigment masterbatches can enhance biopolymer crystallization efficiency by over 46%, improving mechanical performance and processing efficiency. With updates to Japan’s Positive List System for food-contact plastics (2025), the market is shifting toward high-purity organic pigments, reinforcing Japan’s leadership in premium, compliant, and technologically advanced plastic pigments.

Plastic Pigments Market Report Scope

Plastic Pigments Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$14.1 Billion

|

|

Market Size (2034)

|

$30.9 Billion

|

|

Market Growth Rate

|

9.1%

|

|

Segments

|

By Pigment Type (Organic Pigments, Inorganic Pigments, Specialty & Effect Pigments, Functional Pigments), By Physical Form (Powder Pigments, Pigment Masterbatches, Liquid Dispersions & Pastes, Flush Colors), By Resin Compatibility (Commodity Thermoplastics, Engineering Plastics, High-Performance Polymers), By Application (Packaging, Automotive, Building & Construction, Consumer Goods, Medical & Healthcare)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Sudarshan Chemical Industries Limited, BASF SE, DIC Corporation, Clariant AG, Lanxess AG, Cabot Corporation, Chemours Company, Shepherd Color Company, Tronox Holdings plc, Pidilite Industries Limited, Altana AG, Vibrantz Technologies, Sensient Technologies Corporation, Toyo Ink SC Holdings Co. Ltd., Venator Materials PLC

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Plastic Pigments Market Segmentation

By Pigment Type

Azo Pigments

Phthalocyanine Pigments

Quinacridone Pigments

Perylene Pigments

High-Performance Pigments

Titanium Dioxide

Iron Oxide

Carbon Black

Chromium Oxide

Ultramarine

- Specialty & Effect Pigments

- Functional Pigments

By Physical Form

- Powder Pigments

- Pigment Masterbatches

- Liquid Dispersions & Pastes

- Flush Colors

By Resin Compatibility

- Commodity Thermoplastics

- Engineering Plastics

- High-Performance Polymers

By Application

- Packaging

- Automotive

- Building & Construction

- Consumer Goods

- Medical & Healthcare

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Plastic Pigments Industry

- Sudarshan Chemical Industries Limited

- BASF SE

- DIC Corporation

- Clariant AG

- Lanxess AG

- Cabot Corporation

- Chemours Company

- Shepherd Color Company

- Tronox Holdings plc

- Pidilite Industries Limited

- Altana AG

- Vibrantz Technologies

- Sensient Technologies Corporation

- Toyo Ink SC Holdings Co. Ltd.

- Venator Materials PLC

*- List not Exhaustive