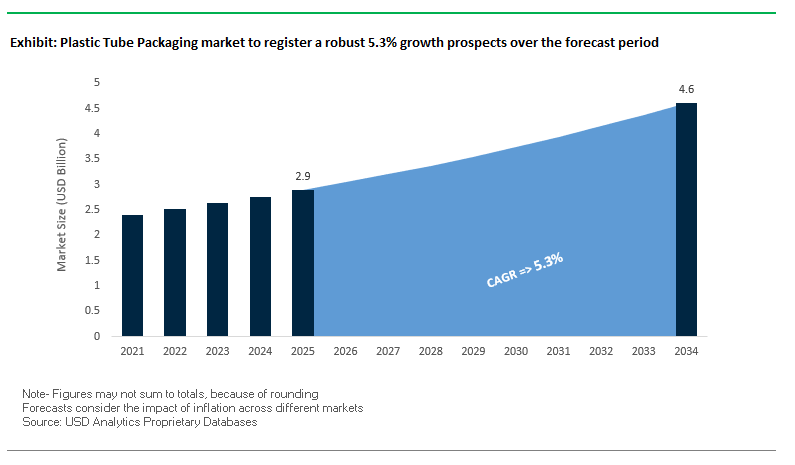

Market Overview: Plastic Tube Packaging Market Projected to Reach $4.6 Billion by 2034 at 5.3% CAGR

Market Value (MV) 2025: $2.9 billion │ 2034: $4.6 billion │ CAGR (2025–2034): 5.3%

The global plastic tube packaging industry is evolving as one of the most dynamic packaging segments, primarily driven by rising demand in oral care, personal care, pharmaceuticals, and cosmetics. With its convenience, portability, and strong branding potential, plastic tube packaging has become the preferred choice for global brands and consumers alike. For industry professionals and buyers, the key questions are: Which tube types are shaping market growth? How is sustainability influencing material innovation? And what role will partnerships and M&A activity play in scaling global production?

Key Insights for Buyers & Decision-Makers:

- Oral Care Leadership: Oral care continues to dominate, with major brands like Colgate, Unilever, and Vicco shifting to fully recyclable laminated tubes.

- Small-Volume Tube Surge: The ≤50 ml segment is the fastest growing, supporting cosmetic samples, pharma trial packs, and single-use applications.

- Laminated Tubes in Demand: Laminated tubes remain the largest category due to superior barrier protection and high-quality printing for branding.

- Sustainability at Core: Rising use of Post-Consumer Recycled (PCR) plastics, mono-material tubes, and innovations like HDPE-compatible Greenleaf tubes are driving eco-friendly adoption.

Market Analysis: Recent Developments in the Global Plastic Tube Packaging Industry

The global plastic tube packaging market has seen a flurry of M&A activity, sustainability initiatives, and product innovations that are reshaping competition. In May 2025, Amcor finalized its $8.43 billion acquisition of Berry Global, significantly consolidating market leadership and expanding its presence in both rigid and flexible packaging. Similarly, Albéa strengthened its regional footprint in August 2025 by acquiring Amfora Packaging in Latin America, a move aimed at increasing its service capabilities in high-growth emerging markets.

Sustainability-driven partnerships remain central. In January 2025, Albéa partnered with clean beauty brand Drunk Elephant to co-develop sustainable tube formats, while in May 2024, Hoffmann Neopac introduced Polyfoil EcoPro tubes containing up to 60% EU food-grade PCR material, reinforcing the push towards eco-conscious packaging. Leadership changes have also shaped industry direction, with Albéa appointing two new CEOs in April 2024 to accelerate operational efficiency and long-term growth.

Energy and environmental initiatives are equally crucial. In September 2024, Albéa signed a 15-year solar energy deal with TSE to power its facilities with renewable energy, while Berry Global merged its Health, Hygiene & Specialties division with Glatfelter (February 2024) to create a stronger specialty packaging company. This strategic restructuring highlights the growing focus on sustainability, resource optimization, and product portfolio expansion.

Trends and Opportunities Reshaping the Plastic Tube Packaging Market

Accelerated Material Transition to Post-Consumer Recycled (PCR) Resins

The plastic tube packaging market is undergoing a structural shift as manufacturers and brand owners rapidly scale the integration of post-consumer recycled (PCR) resins into tubes. What once began as limited pilot projects is now becoming an industry-wide standard, fueled by corporate sustainability pledges and regulatory mandates across key markets such as Europe and North America.

Beauty and personal care brands are taking the lead, with Shiseido pledging 100% sustainable packaging by 2025, including monomaterial and recycled solutions. Tube producers are matching this demand with offerings like Neopac’s Coex PCR Tube, which integrates up to 35% PCR, and Evergreen Resources’ product line, which offers PCR inclusion from 25% up to 100% depending on specifications. Regulatory frameworks like the EU Packaging and Packaging Waste Regulation (PPWR) are accelerating this adoption, mandating at least 30% PCR content by 2030, with stricter thresholds for certain categories by 2040. These changes are creating intense demand for high-quality recycled polyethylene (PE) and polypropylene (PP), prompting investments in recycling infrastructure and supply chain integration.

Adoption of Monomaterial and Polymer-Lite Tube Structures

Another defining trend in the plastic tube packaging industry is the move away from multi-layer laminates, which pose recyclability challenges, toward monomaterial and polymer-lite tubes. This evolution ensures compatibility with existing recycling streams, addressing consumer and regulatory scrutiny over packaging waste.

Shiseido’s ELIXIR brand is a case in point, with tubes redesigned from multi-material to all-PE monomaterial, boosting recyclability without compromising on aesthetics or performance. Innovations are also extending to pumps and closures, with Express Tubes launching a fully recyclable single-polymer pump to complement monomaterial tubes. Collaborative partnerships are amplifying this trend, exemplified by Origins and SABIC’s alliance, which delivered an advanced recycled tube solution that reinforces both sustainability commitments and functional performance. For industries such as cosmetics, personal care, and pharmaceuticals, this alignment of sustainability, compliance, and consumer preference is becoming a cornerstone of competitive advantage.

Development of High-Performance Bio-Based and Compostable Polymer Tubes

A significant opportunity exists in pioneering bio-based and compostable polymer tubes that combine sustainability with high-performance functionality. While polylactic acid (PLA) and other early bioplastics faced limitations in durability and barrier properties, recent advancements in biopolymer chemistry are addressing these gaps, opening the door for scalable adoption.

Greendot Biopak’s proprietary compostable resins demonstrate how new materials can be integrated into existing extrusion lines, minimizing conversion costs while delivering eco-certified performance. In the premium organic and natural product segments, bio-based feedstocks such as sugarcane polymers are gaining traction, especially when paired with certifications from ECOCERT and similar bodies. For pharmaceuticals and cosmetics, material performance is equally critical, and companies like SABIC are offering bio-based polymers that meet regulatory compliance, barrier requirements, and chemical resistance. As sustainability pressures converge with consumer expectations, bio-based and compostable tubes are poised to capture high-margin niches and mainstream applications alike.

Integration of Smart Features for Consumer Engagement and Anti-Counterfeiting

The digital transformation of packaging is creating new opportunities for plastic tube manufacturers to add value far beyond containment. By embedding Near-Field Communication (NFC) chips, QR codes, or augmented reality triggers, tubes are being redefined as interactive platforms that provide real-time brand engagement, transparency, and product protection.

Competitive Landscape: Key Companies in Plastic Tube Packaging

The plastic tube packaging market is highly competitive, with global leaders and regional specialists focusing on sustainability, high-barrier innovation, and brand partnerships. Competition revolves around laminated vs. extruded tubes, mono-material solutions, and increasing PCR content integration.

Albéa Group Global Leader in Plastic Tube Packaging with Sustainability at Core

Albéa Group is a leading supplier of plastic, laminate, and cardboard-based tubes, serving global beauty, personal care, and pharmaceutical brands. Known for its Greenleaf 2 tube technology, Albéa ensures compatibility with HDPE recycling streams. Recent moves include the acquisition of Amfora Packaging (August 2025) to strengthen its Latin American footprint and a 15-year solar energy deal with TSE (September 2024) to reduce carbon emissions. With 34 industrial sites across Europe, the Americas, and Asia, Albéa delivers integrated packaging solutions that balance branding, performance, and sustainability.

EPL Limited Laminated Tube Specialist Driving Oral Care Sustainability

EPL Limited (formerly Essel Propack) is a global pioneer in laminated tubes, particularly its Platina and Greenleaf series, which are APR-approved for recyclability. It is a leading supplier for oral care giants like Unilever and Colgate-Palmolive, converting their toothpaste portfolios to fully recyclable formats. In November 2024, EPL collaborated with Vicco Labs to transition to recyclable tube packaging. Its product profile spans high-barrier, transparent, and decorative tubes, making it a key player in both mass-market and premium applications.

Amcor plc Expanding Global Leadership Through Berry Global Acquisition

Amcor produces extruded plastic tubes and flexible packaging, with applications in food, pharma, and personal care. The May 2025 acquisition of Berry Global was a transformative move, boosting Amcor’s global footprint to 290+ locations with 77,000 employees. Amcor’s Liquiform technology exemplifies its innovation, using the packaged product itself to form and fill containers, cutting costs and material waste. The company is uniquely positioned to drive efficiency and sustainability in tube packaging through scale, R&D investment, and global customer partnerships.

Berry Global Group Integrated into Amcor After May 2025 Acquisition

Before its acquisition, Berry Global was a major force in consumer packaging and engineered materials, known for introducing PCR-integrated tubes such as the Verdant extruded tube (February 2024) with 25% PCR content and a new oval tube design (March 2024). Its sustainability goals of 100% recyclable, reusable, or compostable packaging made it a leader in circular economy initiatives. While now part of Amcor, Berry’s design legacy and product development pipeline continue to influence the combined company’s innovation strategy.

CCL Industries Inc. Specialty Packaging Powerhouse with Diverse Tube Offerings

CCL Industries, the world’s largest converter of pressure-sensitive and extruded film materials, offers extruded and laminated plastic tubes as part of its broad specialty packaging portfolio. With 213 production facilities across 42 countries, CCL serves consumer goods, healthcare, and chemical industries with tube formats designed for precision and brand impact. Its strength lies in materials science expertise, particularly polymer extrusion and adhesive technologies, enabling advanced packaging designs. The company’s strategic integration across labels, aerosols, and tubes makes it a versatile partner for global brands.

Plastic Tube Packaging Market Share Insights

Squeeze Tubes Hold the Largest Market Share by Product Type in Plastic Tube Packaging

Squeeze and collapsible tubes represent 58% of the global plastic tube packaging market in 2025, reflecting their dominance in cosmetics, pharmaceuticals, and food products that require hygienic, barrier-protective, and easy-to-dispense packaging. Their functional advantages precise dosage control, near-total product evacuation, and strong barrier protection against air and moisture make them indispensable in high-value applications such as dermatological creams, serums, and medical ointments. Twist tubes, while smaller, are the fastest-growing format, anchored in the oral care sector where toothpaste adoption is near-universal. Their expansion into food condiments and portable energy gels highlights their growing versatility. The “other tube types” category, encompassing laminated and co-extruded tubes, sustains a competitive edge in premium markets through lightweight designs, sustainable material integration, and high-quality graphics for brand differentiation. The segmentation reinforces how squeeze tubes dominate through functionality and trust, while twist and specialty tubes act as growth engines via innovation and category diversification.

Cosmetics and Oral Care Lead Market Share by Application in Plastic Tube Packaging

Cosmetics and personal care account for the largest share of the plastic tube packaging market in 2025 at 35%, underscoring the segment’s role as the most lucrative revenue driver. This dominance stems from the continuous pipeline of skincare and haircare innovations requiring protective, airless, and visually appealing packaging that elevates product value. Oral care, at 28%, is the undisputed volume leader, with toothpaste tubes consumed at a massive global scale and increasingly upgraded with flip-top closures, stand-up formats, and multi-chamber innovations. Pharmaceuticals and healthcare, holding 20%, represent the high-stakes segment, where stringent regulatory compliance and superior barrier properties are essential to ensure patient safety and efficacy of topical formulations. Food and beverages, while smaller at 9%, is rapidly growing as tubes gain traction for condiments, pastry products, and nutrition gels, provided material safety and shelf-life criteria are met. Industrial and commercial uses, with 5%, remain stable, prioritizing durability and chemical resistance over aesthetics for adhesives and lubricants. This segmentation highlights how cosmetics and oral care drive both value and volume, while pharmaceuticals and food applications expand the industry’s regulatory and innovation frontiers.

United States: Sustainable Materials and E-Commerce Innovation Reshape the Plastic Tube Packaging Market

The United States plastic tube packaging market is undergoing a rapid transformation, strongly influenced by evolving consumer preferences and sustainability demands. Brands are increasingly shifting to recyclable and bio-based materials to align with circular economy practices, responding to heightened awareness about eco-friendly packaging. At the same time, companies are investing in unique tube designs with features such as needlepoint tips, slanted nozzles, and ergonomic caps to stand out on retail shelves and enhance customer convenience.

E-commerce continues to be a powerful growth driver, with lightweight, durable, and stackable plastic tubes designed to withstand shipping pressures while reducing material usage. Technological advancements further reinforce U.S. market leadership, as automated production and digital printing enable mass customization, short-run flexibility, and faster response to consumer trends. Together, sustainability, e-commerce packaging innovation, and automation make the U.S. one of the most dynamic plastic tube packaging markets worldwide.

Germany: Circular Economy Leadership and Eco-Design Innovations Define the Market

Germany’s plastic tube packaging industry is shaped by some of the strictest regulations in Europe, including the German Packaging Act (VerpackG) and the EU’s Packaging and Packaging Waste Regulation (PPWR). These policies have created strong demand for recyclable, eco-friendly tube solutions with high post-consumer recycled (PCR) content. Manufacturers are aligning with Germany’s broader circular economy goals by developing packaging that supports material recovery and reuse at scale.

Technological advancements in recycling are setting new benchmarks for efficiency, with AI-enabled systems improving plastic sorting and mechanical recycling outcomes. Companies are also embracing innovative eco-design strategies, such as Packsys’ noSho cap-free, shoulderless tube, which significantly reduces material usage and waste. By combining regulatory rigor, high recycling rates, and eco-centric product design, Germany stands as a leader in sustainable plastic tube packaging across Europe.

China: Cosmetics Boom and Government Push for Green Transformation Propel Market Growth

China’s plastic tube packaging market is expanding rapidly, fueled by the country’s booming cosmetics and personal care industries. Tubes are increasingly preferred for lotions, creams, and skincare products due to their portability and convenience. The cost-effectiveness of Chinese manufacturing also strengthens its global competitiveness, making China a leading exporter of high-quality yet affordable plastic tubes that meet international standards.

On the technological front, manufacturers are adopting advanced production techniques such as multi-layer co-extrusion and barrier-enhanced materials to improve durability and product protection. At the same time, China’s government is pushing sustainability initiatives, including green packaging mandates for the express delivery sector. This regulatory shift is accelerating adoption of reusable, recyclable, and reduced-packaging tube solutions. With cosmetics expansion, cost-efficient production, and sustainability-driven regulations, China is set to remain one of the fastest-growing markets for plastic tube packaging.

India: Pharmaceutical Expansion and Sustainable Innovation Drive Tube Packaging Demand

India’s plastic tube packaging industry is witnessing significant growth, anchored by the rapid expansion of the pharmaceutical and cosmetics sectors. Plastic tubes are widely used for ointments, gels, and creams, making them an essential packaging format for healthcare and personal care applications. Governmental support through the Plastic Waste Management (Amendment) Rules has further spurred demand for eco-friendly packaging alternatives, accelerating the shift toward reusable and recyclable tube solutions.

Innovation is another defining feature of the Indian market. For instance, UFlex introduced “Kraftika,” a tube that replaces up to 70% of its structure with virgin kraft paper, offering an eco-friendly alternative to traditional plastic tubes. Rising consumer demand for portable, hygienic, and easy-to-use packaging in personal care, food, and pharmaceuticals further strengthens the sector. By combining regulatory backing, consumer-driven demand, and local product innovation, India is positioning itself as a strong growth hub for sustainable plastic tube packaging.

Brazil: Circular Economy Policies and Bio-Based Plastic Innovation Enhance Market Competitiveness

Brazil’s plastic tube packaging market is advancing under the government’s National Solid Waste Policy, which promotes recycling, waste reduction, and circular economy principles. These regulations are fueling demand for reusable, recyclable, and bio-based tube solutions across industries. The strong growth of personal care and hygiene products in Brazil, including toothpaste, lotions, and creams, is further driving demand for hygienic and convenient tube packaging.

Technological innovation is also reshaping the Brazilian market, with companies investing in bio-based plastics that reduce reliance on traditional polymers. Manufacturers are building closed-loop recycling systems to convert post-consumer waste into new packaging materials, ensuring compliance with environmental standards while improving brand sustainability. With booming consumer demand and a regulatory focus on circularity, Brazil is emerging as a competitive market for next-generation plastic tube packaging.

Japan: Bio-Based Materials and Functional Innovation Drive a High-Tech Packaging Ecosystem

Japan is at the forefront of sustainable transformation in the plastic tube packaging market, led by its shift toward bio-polypropylene (bio-PP) and other bio-based materials. Collaborations between LyondellBasell, Shiseido, Futamura Chemical, and Iwatani highlight the country’s strategy to meet its 2030 target of producing two million tons of bio-PP products annually while aligning with its 2050 net-zero commitments. Governmental climate goals and strict recycling policies provide further momentum for eco-friendly packaging.

Japan also stands out for its advanced recycling infrastructure, which ensures high collection and reuse rates for plastics. On the innovation front, manufacturers are developing tubes with enhanced functionality and aesthetics, offering robust, hygienic, and water-resistant designs suitable for premium cosmetic and healthcare applications. This fusion of bio-based material adoption, advanced recycling systems, and continuous functional innovation positions Japan as a global leader in sustainable and high-performance plastic tube packaging.

Plastic Tube Packaging Market Report Scope

Plastic Tube Packaging market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$2.9 Billion

|

|

Market Size (2034)

|

$4.6 Billion

|

|

Market Growth Rate

|

5.3%

|

|

Segments

|

By Material Type (Polyethylene, Polypropylene, Polyvinyl Chloride, Ethylene Vinyl Alcohol, Bio-based Plastics, Other Materials), By Product Type (Squeeze and Collapsible Tubes, Twist Tubes, Other Tube Types), By Capacity (Less than 50 ml, 50 ml to 100 ml, 101 ml to 150 ml, More than 150 ml), By Application (Oral Care, Cosmetics & Personal Care, Pharmaceuticals & Healthcare, Food & Beverages, Industrial & Commercial, Other Applications)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Albéa S.A., Amcor Plc, EPL Limited (formerly Essel Propack Ltd.), Hoffmann Neopac AG, Berry Global Inc., CCL Industries Inc., Sonoco Products Company, LINHARDT GmbH & Co. KG, Montebello Packaging, Unette Group, CTLPACK, UFlex Limited, Huaxin Plastic, Fusion Packaging, Vayhan Paper & Boards

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Plastic Tube Packaging Market Segmentation

By Material Type

- Polyethylene

- Polypropylene

- Polyvinyl Chloride

- Ethylene Vinyl Alcohol

- Bio-based Plastics

- Other Materials

By Product Type

- Squeeze and Collapsible Tubes

- Twist Tubes

- Other Tube Types

By Capacity

- Less than 50 ml

- 50 ml to 100 ml

- 101 ml to 150 ml

- More than 150 ml

By Application

- Oral Care

- Cosmetics & Personal Care

- Pharmaceuticals & Healthcare

- Food & Beverages

- Industrial & Commercial

- Other Applications

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Plastic Tube Packaging Market

- Albéa S.A.

- Amcor Plc

- EPL Limited (formerly Essel Propack Ltd.)

- Hoffmann Neopac AG

- Berry Global Inc.

- CCL Industries Inc.

- Sonoco Products Company

- LINHARDT GmbH & Co. KG

- Montebello Packaging

- Unette Group

- CTLPACK

- UFlex Limited

- Huaxin Plastic

- Fusion Packaging

- Vayhan Paper & Boards

*List not Exhaustive

Research Coverage

This report investigates the evolving dynamics, technological breakthroughs, and strategic growth pathways within the global plastic tube packaging market, offering a comprehensive and data-driven analysis suitable for decision-makers, supply chain managers, and packaging professionals. USDAnalytics meticulously reviews material innovations, sustainability integration, product diversification, and high-value applications across oral care, cosmetics, personal care, pharmaceuticals, and food industries. The report highlights key developments, including corporate mergers, regional expansions, and adoption of eco-friendly solutions such as post-consumer recycled (PCR) and bio-based polymers. It provides detailed insights into market structure, competitive positioning, and emerging opportunities for packaging suppliers, while analyzing regulatory frameworks, market penetration, and innovation trends. This report is an essential resource for investors, procurement teams, and R&D professionals seeking actionable intelligence to optimize product strategies, enhance sustainability practices, and capitalize on growth prospects in both mature and emerging markets. USDAnalytics’ analysis reviews supply-demand dynamics, production capacity trends, and forward-looking forecasts to 2034, ensuring stakeholders understand both current and anticipated market forces.

Scope Highlights:

- Segmentation: By Material Type (Polyethylene, Polypropylene, Polyvinyl Chloride, Ethylene Vinyl Alcohol, Bio-based Plastics, Other Materials), By Product Type (Squeeze and Collapsible Tubes, Twist Tubes, Other Tube Types), By Capacity (Less than 50 ml, 50 ml to 100 ml, 101 ml to 150 ml, More than 150 ml), By Application (Oral Care, Cosmetics & Personal Care, Pharmaceuticals & Healthcare, Food & Beverages, Industrial & Commercial, Other Applications).

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Historical and Forecast Data: 2021–2024 historical market data and forecasts from 2025–2034.

- Company Analysis: Profiles and strategic evaluations of 15+ leading global players, including Albéa S.A., Amcor Plc, EPL Limited, Hoffmann Neopac AG, Berry Global Inc., CCL Industries Inc., Sonoco Products Company, and UFlex Limited.

Methodology

The study employs a hybrid methodology combining both qualitative and quantitative approaches to ensure accurate and comprehensive insights. Primary research involved in-depth interviews with industry leaders, packaging engineers, and regulatory specialists to validate market trends, material preferences, and adoption of sustainable solutions. Secondary research encompassed corporate filings, regulatory documents, patents, industry publications, and company press releases to capture historical and recent developments. Market sizing and forecasts were derived using bottom-up and top-down approaches, incorporating production, consumption, and trade data across key regions and applications. Competitive benchmarking, SWOT analysis, and trend mapping provide a multi-dimensional understanding of strategic positioning, innovation trajectories, and market dynamics. USDAnalytics integrates macroeconomic indicators, regional regulatory frameworks, and sustainability drivers to generate actionable intelligence for stakeholders seeking data-backed insights in the global plastic tube packaging market.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.