Point-of-Purchase Packaging Market Size, Overview, and Growth Outlook (2025–2034)

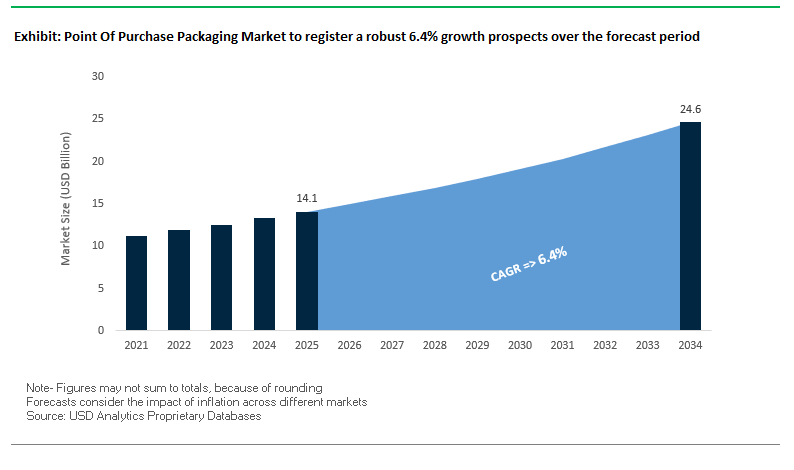

Point-of-Purchase Packaging Market Set to Expand from $14.1 Billion in 2025 to $24.6 Billion by 2034 at a 6.4% CAGR Driven by Impulse Buying and Sustainability Trends

The global point-of-purchase (POP) packaging market is projected to grow from $14.1 billion in 2025 to $24.6 billion by 2034, achieving a CAGR of 6.4%. Growth is primarily driven by rising consumer demand for visually engaging displays, the integration of digital technology, and the increasing adoption of sustainable materials. POP packaging remains a critical tool for retailers and brands to influence impulse purchases, optimize shelf visibility, and strengthen brand recognition.

Key Insights for industry professionals and buyers:

- Impulse Purchase Influence: Strategic POP displays significantly increase unplanned buying decisions at the point of sale.

- Digital Integration Enhances Engagement: Interactive screens, AR features, and QR codes are increasingly used to connect physical and online shopping experiences.

- Retail Ready Packaging (RRP) Streamlines Operations: RRP solutions facilitate rapid stocking, display efficiency, and product visibility on shelves.

- Sustainability Drives Consumer Preference: Recycled cardboard, biodegradable plastics, and plant-based alternatives are increasingly used in POP packaging to meet ESG goals.

- Cross-Channel Relevance: POP packaging supports both brick-and-mortar and e-commerce strategies, bridging the gap between online and offline consumer touchpoints.

Market Analysis: Industry Developments Highlight a Shift Toward Sustainable and Digitally Integrated POP Solutions

The POP packaging market is witnessing dynamic shifts in technology, sustainability, and corporate strategy. In August 2025, Mondi ramped up production of its FunctionalBarrier Paper Ultimate, an ultra-high barrier paper-based solution offering a sustainable alternative to conventional plastics. That same month, International Paper focused on its core sustainable packaging business by divesting its Global Cellulose Fibers segment, strengthening its POP packaging capabilities. Also in August 2025, Mondi expanded re/cycle MailerBAG capacity to support e-commerce, reflecting a growing trend toward flexible and sustainable display packaging.

Strategic mergers and new product innovations are shaping the competitive landscape. In July 2025, Smurfit Kappa and WestRock merged to form Smurfit WestRock, consolidating expertise in paper and POP displays. In June 2025, Graphic Packaging International launched PaperSeal® Pressed MAP Tray, reducing plastic use by 85% in food packaging applications relevant to POP displays. In April 2025, Nfinite Nanotechnology partnered with Amcor to develop nanocoatings that enhance oxygen barrier performance, promising next-generation functional POP packaging.

Earlier initiatives highlight long-term sustainability commitments. In February 2025, Mondi and Proquimia introduced paper-based stand-up pouches, signaling a shift to monomaterial packaging. In November 2024, DS Smith announced a £100 million R&D investment focused on circular and fully recyclable packaging products, a critical driver for sustainable POP innovations.

Emerging Trends and Opportunities in the Point of Purchase (POP) Packaging Market

Integration of Digital and Interactive Elements into Physical Packaging

One of the most transformative trends shaping the point of purchase packaging market is the adoption of digital and interactive technologies to deepen consumer engagement. Coca-Cola’s 2025 AR-driven campaign exemplifies how augmented reality (AR) is being deployed directly through POP displays to merge physical packaging with immersive experiences. By scanning a QR code, shoppers could activate a virtual soccer scene on their phones, extending brand storytelling beyond the shelf and reinforcing Coca-Cola’s connection with sports culture. Similarly, the integration of QR codes into POP packaging is enabling brands to deliver traceability and transparency. A food company case study demonstrated how shoppers, by scanning QR-enabled displays, accessed real-time product origin, ingredient, and sustainability details, resulting in a measurable 4.2% sales uplift in pilot markets. This illustrates how interactive POP packaging is evolving from a static promotional tool into a dynamic digital channel that drives both engagement and trust.

Mandated Shift Towards Retail-Ready and Shelf-Optimized Packaging

Retail-ready packaging (RRP) is becoming a mandate rather than an option as retailers prioritize efficiency and cost reduction in-store. A 2025 Royal Group report underscored how RRP helps retailers combat rising labor costs, with a snack brand case study showing replenishment times reduced by 25% after switching to retail-ready solutions. This time savings translates directly into operational cost reductions for retailers, making RRP a strong bargaining factor when selecting suppliers. The “Five Easies” framework—easy to identify, open, shop, replenish, and recycle—has become a retail standard, pushing brands to reengineer their POP packaging around convenience and recyclability. With labor representing up to 25% of retail costs according to Bennett Packaging, shelf-optimized packaging is increasingly a prerequisite for market access, positioning POP packaging as a core enabler of retail profitability and consumer convenience.

Adoption of Smart Labels for Dynamic Pricing and Personalization

Smart packaging technologies present a high-value growth opportunity for POP packaging, particularly in the area of electronic shelf labels (ESLs). Unlike traditional static displays, ESLs allow real-time, remote-controlled price adjustments, enabling flash sales and just-in-time promotions. Slimstock’s 2025 analysis revealed that ESLs can cut time spent on price updates by 60%, making them indispensable in a competitive, fast-moving retail environment where perishable product turnover is critical. Beyond operational efficiency, smart labels also enable shopper personalization. By integrating ESLs with a retailer’s CRM system, loyalty-specific offers and targeted discounts can be displayed directly at the shelf, creating a one-to-one marketing experience. This elevates POP packaging from a transactional channel into a personalized engagement platform, reinforcing brand loyalty and boosting conversion rates.

Development of Advanced Bio-based and Compostable Materials for Short-Lifecycle Displays

Sustainability is redefining POP packaging, particularly for temporary displays that often end up as single-use waste. Bio-based and compostable materials such as PLA and PBAT are emerging as viable alternatives for short-lifecycle POP displays. Companies like BASF and Novamont are actively developing materials that not only provide structural strength during use but also decompose in industrial composting facilities, returning nutrients to the soil. Academic studies, including reviews in Frontiers, highlight the potential of biopolymers to replace conventional plastics in temporary packaging applications, especially given their alignment with tightening single-use packaging regulations. Retailers and brands deploying compostable POP displays are reducing their waste footprint while signaling a commitment to sustainability, a message that resonates strongly with environmentally conscious consumers. By combining material innovation with functional design, the POP packaging industry is positioning itself at the intersection of sustainability, compliance, and brand differentiation.

Competitive Landscape: Global POP Packaging Leaders Are Driving Innovation, Sustainability, and Omni-Channel Retail Solutions

The POP packaging industry is dominated by companies focusing on sustainable materials, operational efficiency, digital integration, and strategic mergers. These leaders are defining market standards by delivering visually impactful, eco-friendly, and functionally advanced packaging solutions.

WestRock Company: Enhancing In-Store Consumer Engagement Through Innovative POP Displays

WestRock offers a comprehensive range of floor, end-cap, and counter POP displays, along with Shopper Ready Packaging designed to improve shelf visibility and reduce stockouts. Its solutions serve retail, e-commerce, processed foods, and personal care sectors. Following its July 2025 merger with Smurfit Kappa, WestRock has strengthened its global presence, delivering sustainable and data-driven packaging solutions to enhance consumer engagement at the point of sale.

Smurfit Kappa Group: Creating Sustainable POP Displays Through Global Integration and E-Commerce Expertise

Smurfit Kappa specializes in corrugated displays, shelves, and in-store promotional materials, emphasizing sustainability via its Better Planet Packaging initiative. The July 2025 merger with WestRock positions the company as a global powerhouse for POP packaging. Smurfit Kappa also leverages expertise in e-commerce packaging for online beverages and liquids, enabling brands to bridge physical and digital shopping experiences.

DS Smith Plc: Driving Circular Economy Solutions for Retail-Ready and Shelf-Ready POP Packaging

DS Smith delivers corrugated displays, retail-ready packaging, and omni-channel solutions designed to make brands stand out. Through its Now & Next Sustainability Strategy, DS Smith aims to replace one billion items of problem plastic with fiber alternatives by 2025. With a £100 million R&D investment, the company is developing fully recyclable POP solutions and tools like Circular Design Metrics to optimize sustainability performance.

Mondi Group: Introducing Barrier Paper Solutions and Circular-Driven POP Packaging Innovations

Mondi provides eye-catching corrugated solutions for fresh produce and consumer goods, emphasizing circular economy principles. In August 2025, the company launched FunctionalBarrier Paper Ultimate, a sustainable alternative to multilayer plastics for POP displays. Mondi also offers re/cycle MailerBAGs for e-commerce shipments, enhancing both cost efficiency and customer experience while reinforcing brand visibility at the point of purchase.

International Paper Company: Transforming Global POP Packaging Through Strategic Focus on Sustainability

International Paper provides a wide range of paper-based POP displays and corrugated packaging. In August 2025, the company divested its Global Cellulose Fibers business to focus on core sustainable packaging, strengthening its POP portfolio. The recent acquisition of DS Smith expands its product offerings and geographic reach, positioning International Paper as a global leader in environmentally conscious POP solutions.

Point Of Purchase Packaging Market Share Insights, 2025-2034

Floor Displays Lead Market Share by Product Type in the Point-of-Purchase Packaging Industry

Floor displays dominate the point-of-purchase (POP) packaging industry with a 28% share, owing to their unmatched visibility and bulk-handling capacity in high-traffic retail zones. These displays are the primary format for seasonal campaigns, new product launches, and promotional merchandising, driving sales uplift across categories from beverages to household goods. Counter displays follow at 24%, excelling at checkout points where impulse-driven, high-margin purchases like snacks, cosmetics, and accessories are triggered by last-minute consumer decisions. Pallet displays, with 18% share, provide the logistics-to-sales-floor efficiency advantage, especially for warehouse clubs and big-box retailers where labor savings and direct pallet-to-aisle deployment create significant value. Gravity feed displays secure 15% share by automating product rotation and reducing restocking costs, particularly in high-turnover segments such as snacks and beverages. Dump bins maintain relevance with 8%, particularly for value-driven, seasonal promotions, reinforcing a message of abundance and affordability. Sidekick displays at 4% and clip strips at 3% occupy smaller shares but play an outsized role in cross-merchandising and secondary placements, strategically boosting basket size through complementary purchases. Together, the POP packaging segmentation reflects a hierarchy where floor and pallet displays drive high-volume promotions, while counter, sidekick, and clip strips provide tactical, impulse-driven revenue in competitive retail environments.

United States: Omnichannel Packaging, Automation, and EPR Laws Reshaping POP Displays

The United States point-of-purchase packaging market is rapidly evolving due to the convergence of omnichannel retail and e-commerce logistics. Consumer packaged goods (CPG) companies are increasingly demanding omnichannel-ready packaging that integrates seamlessly between in-store displays and e-commerce shipping formats, reducing last-mile costs while maintaining brand visibility. This trend is supported by heavy investment in automation-ready secondary packaging lines, where robotics and AI-enabled vision systems enhance efficiency, quality, and speed for large-scale POP packaging production.

Regulatory frameworks are also shaping the U.S. market. The FDA’s stringent standards for food-contact materials drive innovation in hygienic POP packaging for food and beverage brands, while state-level bans in Delaware, Illinois, and New York are phasing out single-use plastics and polystyrene packaging in retail environments. On a broader scale, California’s Extended Producer Responsibility law (SB-54) mandates a 25% reduction in virgin plastic packaging and requires producer participation in Producer Responsibility Organizations by 2025. Major corporate investments are reinforcing these trends—Apple’s $100 billion “American Manufacturing Program” is expected to boost advanced chip packaging and high-tech retail displays produced domestically, creating new opportunities for U.S. POP packaging manufacturers.

European Union: PPWR Regulations and Circular Economy Standards Driving Packaging Redesign

The European Union’s POP packaging market is under strict pressure from the Packaging and Packaging Waste Regulation (PPWR), which came into effect in February 2025. This framework mandates recyclability and reusable standards across packaging categories, forcing manufacturers to redesign POP displays for circular economy compatibility. From August 2026, PFAS will be banned above specific thresholds in food packaging, further impacting material selection for retail packaging applications. By 2030, only POP packaging with a recyclability grade of 70% or higher will be classified as recyclable, accelerating innovation in single-material solutions.

In addition, the mandatory harmonized recycling label requirement by 2028 will reshape how packaging communicates disposal and recycling instructions to consumers, making labeling clarity a priority for retailers. However, regulatory debates are emerging—industry groups like the Alliance for Sustainable Packaging are calling for a “pause” on certain PPWR requirements, citing concerns that an exclusive focus on reusables may increase environmental impacts elsewhere. Despite these challenges, EU funding is supporting circular packaging innovation, ensuring the region remains at the forefront of POP packaging sustainability.

China: Waste Reduction Laws and Tech-Integrated POP Packaging Solutions

China’s point-of-purchase packaging market is being heavily influenced by new regulations effective June 2025, which target delivery waste and mandate the adoption of recycled materials and reusable systems in packaging, particularly in the fast-growing e-commerce sector. The State Administration for Market Regulation (SAMR) has introduced strict limits on excessive packaging for food and cosmetics, restricting void ratios, layers, and cost proportions to reduce material waste. These frameworks align with broader initiatives from the NDRC and MEE to reduce plastic pollution and phase out environmentally unfriendly plastics.

In terms of innovation, brands are merging cultural authenticity and digital engagement in POP packaging. A notable example is Asahi’s AR-enabled Chinese New Year red packets, which feature interactive sticker sheets to deliver customized consumer experiences. Regulatory oversight, such as the positive list for food-contact materials and new adhesive standards introduced in February 2025, is further guiding safe and sustainable packaging production. With a blend of strict waste reduction laws and consumer-centric innovations, China is pushing POP packaging toward a digitally enhanced, sustainable future.

India: EPR Frameworks and Fast-Food Demand Fueling POP Packaging Growth

India’s point-of-purchase packaging market is being redefined by regulatory enforcement and rising consumer demand. The Plastic Waste Management Rules (2016, amended in 2022) establish a robust Extended Producer Responsibility (EPR) framework, requiring brand owners and manufacturers to ensure end-of-life collection and recycling of plastic packaging. The Legal Metrology (Packaged Commodities) Rules, 2011 add further compliance obligations by mandating transparent and standardized labeling on the principal display panel, driving improvements in labeling clarity for POP packaging.

India is also fostering biodegradable and recyclable packaging adoption, with the FSSAI holding consultations to encourage food businesses to transition to sustainable alternatives. Local innovation is growing—startups like Dharaksha Ecosolutions are pioneering agricultural waste-based packaging, supporting India’s circular economy. At the same time, rising fast-food consumption and higher disposable incomes are driving demand for retail-ready POP packaging across both large organized retailers and smaller independent stores. These trends make India a dynamic market for sustainable yet cost-efficient POP packaging solutions.

United Kingdom: Plastic Packaging Tax and Innovation Programs Accelerating Circularity

The United Kingdom’s POP packaging market is strongly shaped by the Plastic Packaging Tax (PPT), which has been in force since April 2022, applying to packaging with less than 30% recycled plastic. This tax is creating financial incentives for producers to adopt recycled materials while aligning with the government’s broader 2030 goal of full packaging recyclability. The Smart Sustainable Plastic Packaging (SSPP) Challenge, a £60 million public funding program, has already supported more than 80 innovation projects focused on reducing plastic waste and advancing recycling technologies relevant to POP packaging.

New 2025 compliance regulations for small businesses have further increased the need for precise food labeling, requiring full ingredient lists, nutrition labeling, and use-by dates on all food-related POP packaging. Additionally, the UK is encouraging a shift toward reusable systems and emphasizing a “design for circularity” approach across industries. These measures are reinforcing the UK’s position as one of the most innovation-driven and sustainability-focused POP packaging markets in Europe.

Germany: Packaging Act Compliance and Corporate R&D Driving Sustainable POP Displays

Germany’s POP packaging market is guided by the Verpackungsgesetz (Packaging Act), which mandates that all businesses distributing packaged goods must be registered with the LUCID Packaging Register. Retailers are also required to contribute financially to packaging recycling through system operators, with larger producers facing stricter obligations. These frameworks are reinforcing accountability and compliance throughout the supply chain.

Consumer preferences are accelerating demand for sustainable e-commerce packaging, with biodegradable, recycled, and renewable materials gaining traction in POP displays. Corporate investments are shaping the market—Mondi’s €5 million R&D center in Germany is developing both plastic- and paper-based packaging innovations, covering coating, extrusion, and filling technologies. This facility reflects a strong corporate commitment to developing durable and recyclable POP packaging solutions, ensuring Germany remains a hub for packaging research and sustainability leadership in Europe.

Point Of Purchase Packaging Market Report Scope

Point Of Purchase Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$14.1 Billion

|

|

Market Size (2034)

|

$24.6 Billion

|

|

Market Growth Rate

|

6.4%

|

|

Segments

|

By Material (Paper & Paperboard, Plastic, Foam, Metal, Glass), By Product Type (Counter Displays, Floor Displays, Gravity Feed Displays, Pallet Displays, Sidekick Displays, Dump Bins, Clip Strips), By End-Use Industry (Food & Beverages, Cosmetics & Personal Care, Pharmaceuticals, Consumer Electronics, Home & Personal Care), By Application (Supermarkets & Hypermarkets, Convenience Stores, Specialty Stores, E-commerce)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Smurfit Kappa Group, WestRock Company, DS Smith Plc, Mondi Group, International Paper Co., Sonoco Products Company, Novolex Holdings, LLC, Graphic Packaging Holding Company, Huhtamaki Oyj, Amcor plc, Pactiv Evergreen Inc., TCPL Packaging Ltd., Sealed Air Corporation, Uflex Ltd., Greif, Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Point Of Purchase Packaging Market Segmentation

By Material

- Paper & Paperboard

- Plastic

- Foam

- Metal

- Glass

By Product Type

- Counter Displays

- Floor Displays

- Gravity Feed Displays

- Pallet Displays

- Sidekick Displays

- Dump Bins

- Clip Strips

By End-Use Industry

- Food & Beverages

- Cosmetics & Personal Care

- Pharmaceuticals

- Consumer Electronics

- Home & Personal Care

By Application

- Supermarkets & Hypermarkets

- Convenience Stores

- Specialty Stores

- E-commerce

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Point Of Purchase Packaging Market

- Smurfit Kappa Group

- WestRock Company

- DS Smith Plc

- Mondi Group

- International Paper Co.

- Sonoco Products Company

- Novolex Holdings, LLC

- Graphic Packaging Holding Company

- Huhtamaki Oyj

- Amcor plc

- Pactiv Evergreen Inc.

- TCPL Packaging Ltd.

- Sealed Air Corporation

- Uflex Ltd.

- Greif, Inc.

* List Not Exhaustive

Methodology

USDAnalytics employs a rigorous, multi-faceted research methodology to deliver actionable insights on the Point-of-Purchase (POP) Packaging Market. Our analysis combines primary research—including interviews with industry leaders, packaging designers, retail procurement professionals, and regulatory authorities—with secondary research sourced from company reports, press releases, academic publications, trade journals, and government databases. Using quantitative modeling and forecasting techniques, we evaluate market size, growth potential, and segmentation by material (paper & paperboard, plastic, foam, metal, glass), product type (floor displays, counter displays, pallet displays, gravity feed, sidekick, clip strips, dump bins), application (supermarkets, convenience stores, specialty stores, e-commerce), and end-use industries (food & beverage, cosmetics, pharmaceuticals, consumer electronics, home & personal care). USDAnalytics also assesses key market drivers, including digital integration, retail-ready packaging (RRP), sustainability trends, and regulatory impacts across major regions such as the U.S., EU, China, India, and the UK. Our methodology emphasizes technological innovation, ESG-aligned material development, and omnichannel engagement strategies, providing industry professionals with precise, future-oriented intelligence to guide strategic planning, investment, and operational decision-making in the global POP packaging landscape.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.