Polycarbonate Food Packaging Market Size, Overview, and Growth Outlook (2025–2034)

Polycarbonate Food Packaging Market Set to Nearly Double from $1.9 Billion in 2025 to $3.9 Billion by 2034 at an 8.2% CAGR Fueled by Heat-Resistant, BPA-Free, and Sustainable Innovations

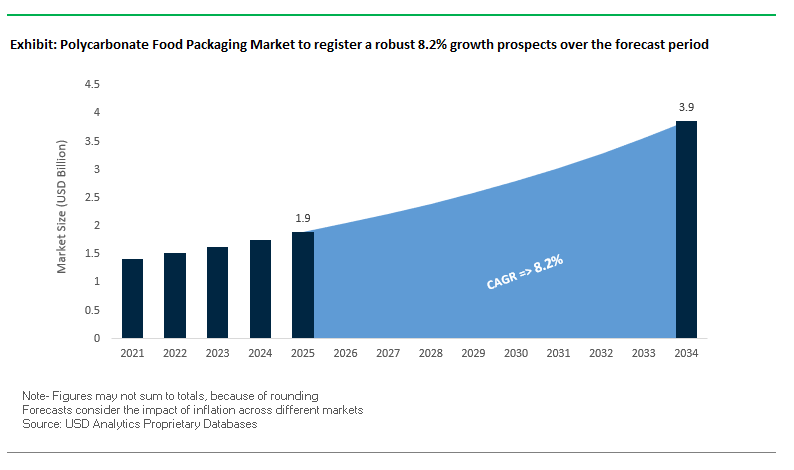

The global polycarbonate food packaging market is projected to grow from $1.9 billion in 2025 to $3.9 billion by 2034, at a CAGR of 8.2%, driven by rising demand for durable, heat-resistant, and transparent packaging solutions. This growth is supported by the increasing adoption of BPA-free polycarbonate formulations, consumer preference for sustainable and safe materials, and the need for high-performance packaging in reusable food containers, baby bottles, and specialized food storage solutions.

Key Insights for industry professionals and buyers:

- Exceptional Heat Resistance: Polycarbonate tolerates temperatures up to 135°C, suitable for sterilization and repeated high-temperature use.

- Crystal-Clear Transparency: Offers glass-like clarity for aesthetically appealing food presentation while meeting FDA and EU safety standards.

- Lightweight and Impact-Resistant: Reduces breakage during transportation and handling, minimizing product waste.

- BPA-Free Innovation: The shift toward BPA-free alternatives encourages research into monomers that maintain polycarbonate’s functional properties.

- Sustainability and Circularity: Increasing consumer and regulatory pressure drives adoption of recyclable and circular economy-compatible materials.

- Versatile Applications: Ideal for reusable food containers, water bottles, baby products, and specialty packaging in healthcare and foodservice sectors.

Market Analysis: Industry Advancements Emphasize Recycling, Bio-Based Innovations, and Strategic North American Expansion

The polycarbonate food packaging market has witnessed significant developments in sustainability, technological innovation, and capacity expansion. In August 2025, Trinseo launched a recycling project in China, investing USD 20 million with an annual production capacity of 5,000 tons of recycled polycarbonate. This initiative aligns with growing circular economy trends in the food packaging industry. That same month, research published in Nano Letters introduced a new inhibitor-modified ALD strategy for ultrathin films, promising future high-barrier polycarbonate containers with enhanced durability and functionality.

Strategic partnerships and capacity expansions are also shaping the competitive landscape. In June 2025, Covestro partnered with PolySource to expand distribution across the United States, strengthening its North American market position. Earlier in January 2025, Covestro announced a significant investment in its Ohio facility to expand production lines for customized polycarbonate compounds. Innovations beyond traditional packaging are emerging as well: in April 2025, Mitsubishi Chemical’s DURABIO™ bio-based engineering plastic was adopted for 3D-printed stools at Expo 2025, demonstrating versatility and the potential for future food-contact applications.

The market is further influenced by sustainability-driven product launches. February 2025 saw Tetra Pak introduce ISCC PLUS certified recycled polymers for food and beverages in India, embedding circularity into packaging practices. In March 2025, Mondi and Proquimia’s paper-based stand-up pouches highlighted a shift to monomaterial packaging, indirectly pressuring traditional polycarbonate containers to innovate sustainably.

Emerging Trends and Opportunities in the Polycarbonate Food Packaging Market

Strategic Phase-Out and Replacement in Key Applications

The polycarbonate food packaging market is undergoing a structural shift as regulatory bodies and global brands accelerate phase-outs of BPA-containing food contact materials. On June 12, 2024, the EU Expert Committee approved a ban on Bisphenol A (BPA) in food contact materials, which was formally adopted by the European Commission. This regulation directly impacts reusable plastic bottles, can coatings, and kitchenware, creating immediate pressure on manufacturers to seek alternative materials. Beyond regulation, brands are also leading proactive transitions. Starbucks, for instance, announced its global phase-out of PFAS in food packaging materials by the end of 2023, reinforcing consumer safety as a strategic brand differentiator. While this commitment did not specifically target polycarbonate, it sets a precedent that amplifies scrutiny of all potentially hazardous packaging materials. Collectively, these forces are driving demand for substitute polymers and signaling a long-term decline of polycarbonate in consumer-facing packaging applications.

Material Consolidation in High-Performance, Non-Migratory Applications

Even as polycarbonate faces restrictions in mainstream consumer packaging, it continues to hold ground in high-performance applications where its durability, heat resistance, and impact strength are critical. In professional catering, commercial kitchens, and food processing industries, polycarbonate remains indispensable for trays, containers, and machine parts that require repeated sterilization cycles without compromising structural integrity. Its shatter-resistance provides a unique safety advantage in environments where broken materials could contaminate food. Similarly, in medical and scientific applications where many products intersect with food-contact regulations polycarbonate is preferred due to its transparency, strength, and sterilizability. An American Chemical Society publication noted that despite the BPA phase-out in infant products, polycarbonate continues to dominate in laboratory and medical contexts. This dual positioning declining in consumer packaging but consolidated in industrial and scientific applications illustrates the material’s resilience where alternatives lack equivalent performance.

Development and Commercialization of Novel Non-BPA Polycarbonates

The phase-out of BPA has created a significant innovation gap, opening opportunities for the development of next-generation, non-bisphenol polycarbonates. Research published in ACS Sustainable Chemistry & Engineering in April 2024 demonstrated the successful synthesis of bio-based isohexide-derived copolycarbonates with comparable tensile strength and heat stability to traditional BPA-polycarbonate. These advances point toward a new era of high-performance, bio-based polymers designed to meet both safety and regulatory demands. However, challenges remain, particularly around “regrettable substitution.” A 2025 study in Environmental Science & Technology highlighted that common BPA substitutes, such as BPS and BPF, may not offer meaningful safety improvements. This underscores the opportunity for chemical companies that can commercialize truly safe, non-endocrine-disrupting polycarbonates. Manufacturers that succeed in this innovation race will not only address regulatory concerns but also gain a competitive edge by offering unique, compliant, and performance-driven materials.

Advanced Monolayer-Barrier Recycling to Create a Circular Economy for PC

Sustainability is emerging as a decisive opportunity for polycarbonate packaging, with advanced recycling poised to close the loop for this high-value material. Closed-loop partnerships are beginning to set the stage for polycarbonate recycling. In July 2025, POLYVANTIS partnered with a recycling specialist to launch a dedicated closed-loop program for PMMA, offering a model that the polycarbonate industry can replicate. Such collaborations enable manufacturers to secure post-consumer and post-industrial feedstock while meeting corporate ESG goals. Furthermore, chemical recycling technologies are proving to be game changers. A report by Closed Loop Partners emphasized that molecular recycling can depolymerize polycarbonate into its base monomers, enabling the production of virgin-quality recycled polycarbonate (rPC). This innovation overcomes the limitations of mechanical recycling, which often leads to downcycling, and opens the door to high-purity, food-grade applications. The integration of chemical recycling into polycarbonate supply chains positions the material for a more circular, environmentally responsible future.

Competitive Landscape: Leading Polycarbonate Food Packaging Companies Are Driving Innovation, Sustainability, and Global Capacity Expansion

The polycarbonate food packaging market is dominated by companies leveraging high-performance materials, recycling initiatives, and strategic partnerships to meet global demand. These market leaders are setting benchmarks in durability, heat resistance, transparency, and circular economy adoption.

Covestro AG: Expanding Production and Strengthening North American Leadership in Sustainable Polycarbonate Packaging

Covestro’s Makrolon® polycarbonate portfolio serves reusable containers, water bottles, and other food-contact applications. In January 2025, the company announced a major investment to expand its Ohio facility, enhancing capacity for customized polycarbonate compounds. Its June 2025 partnership with PolySource further strengthens North American distribution. Covestro’s focus on innovation, sustainability, and climate neutrality by 2035 positions it as a key driver of circular economy initiatives in the plastics industry.

SABIC: Driving Circular Economy and High-Performance Polycarbonate Solutions for Food Packaging

SABIC delivers a diverse portfolio of polycarbonate grades for food and beverage packaging, including high-performance caps and closures. Its TRUCIRCLE™ initiative emphasizes renewable solutions and carbon footprint reduction. SABIC is also advancing recycling processes for mixed plastic waste, supporting circular economy objectives. The company’s materials provide excellent transparency, regulatory compliance, and mechanical strength, making them a trusted choice for sustainable food packaging.

Lotte Chemical Corporation: Innovating High-Impact, Heat-Resistant Polycarbonate Through Chemical Recycling

Lotte Chemical manufactures polycarbonate for food containers, baby bottles, and household goods. In September 2022, it began producing products using pyrolysis oil-based naphtha, a first in the domestic market. Through its Green Promise 2030 initiative, the company aims to expand eco-friendly recycled material production to 1 million tons by 2030. Lotte Chemical emphasizes chemical recycling and ISCC Plus certifications, reinforcing its commitment to sustainability and high-quality performance.

Mitsubishi Engineering-Plastics Corp.: Pioneering Bio-Based Polycarbonate for High-Performance Food Packaging Applications

Mitsubishi Engineering-Plastics (MEP) produces Iupilon™ polycarbonate resins for applications requiring heat resistance, transparency, and impact strength. Its DURABIO™ bio-based polycarbonate offers high scratch resistance and sustainability advantages over conventional BPA-based resins. MEP focuses on innovative, high-performance materials to meet evolving food packaging demands while minimizing environmental impact.

Trinseo S.A.: Advancing Circular Economy Through Strategic Recycling Projects for Polycarbonate Food Packaging

Trinseo provides polycarbonate grades for food packaging and healthcare applications. In August 2025, it launched a recycling PC project in China with an annual capacity of 5,000 tons in Phase I, highlighting its commitment to a circular economy. The company focuses on innovative and sustainable material solutions, combining high-quality performance with advanced recycling technologies to meet growing global demand for sustainable polycarbonate food packaging.

Polycarbonate Food Packaging Market Share Insights, 2025-2034

Water Cooler Bottles Lead Market Share by Product Type in the Polycarbonate Food Packaging Industry

Water cooler bottles represent the largest product type with a 30% share, underlining polycarbonate’s irreplaceable position in large-format hydration solutions. These 5-gallon and 20-liter bottles dominate due to unmatched strength-to-weight performance, impact resistance, and clarity, which make them safer and more durable than glass while being lighter and reusable across multiple cycles. Bottles for sports and beverages remain a strong secondary segment, but their long-term growth depends on BPA-free polycarbonate acceptance amid consumer scrutiny. Baby bottles (18%) illustrate how the industry has successfully transitioned to BPA-free PC resins to sustain demand in safety-critical markets, while jars, containers, and food storage boxes face stronger competition from PET, PP, and Tritan. Tableware and kitchenware, once a core PC application, have eroded significantly, but still retain value in foodservice environments requiring break-resistant clarity. The segmentation highlights a clear duality: PC maintains dominance where performance and durability are non-negotiable, while facing competitive encroachment in consumer-facing niches where perceptions of safety and sustainability dictate market share.

Beverages Dominate Market Share by Application in the Polycarbonate Food Packaging Industry

The beverages segment commands 45% of application share, reflecting the sheer scale of water cooler bottles and reusable beverage containers, which remain PC’s strongest foothold. This application benefits from PC’s crystal clarity, light weight, and mechanical toughness, ensuring both visual appeal and functional resilience in repeated-use cycles. Baby food and formula packaging, at 22%, represents a high-value, highly regulated segment where trust in BPA-free certifications and compliance with FDA/EFSA standards drives brand adoption. Foodservice applications, including reusable pitchers, jugs, and commercial containers, sustain demand due to PC’s ability to withstand heavy use, frequent washing, and rough handling. Ready-to-eat meals and bakery & confectionery together contribute meaningful share by leveraging PC’s heat resistance and visual transparency in premium, microwaveable, and display-oriented formats. Fresh produce packaging remains a marginal niche, with PET and rPET dominating on recyclability, but PC retains selective adoption in premium reusable clamshells. Overall, the dominance of beverages reflects PC’s defensive fortress, while other applications reveal a battlefield of material substitution and regulatory acceptance.

European Union: BPA Ban and PPWR Redefining Polycarbonate Food Packaging

The European Union market for polycarbonate food packaging is undergoing a significant transformation following Commission Regulation (EU) 2024/3190, which became effective in January 2025. This regulation bans the use of bisphenol A (BPA), its salts, and other hazardous bisphenols in the manufacture of food-contact materials, directly impacting polycarbonate packaging producers. Limited exceptions apply only when no safe alternatives exist, placing heavy pressure on companies to accelerate R&D in safe alternatives.

In parallel, the Packaging and Packaging Waste Regulation (PPWR), which entered into force in February 2025, is reinforcing the shift toward recyclable and reusable systems. By 2030, packaging with less than 70% recyclability grade will no longer qualify as recyclable, forcing companies to adopt strict design-for-recycling strategies. A harmonized recycling label requirement by 2028 is expected to bring clarity to consumers while encouraging standardized labeling practices. Furthermore, regulations now require that packaging placed on the EU market must qualify as reusable under specific conditions, promoting the adoption of durable packaging designs. These combined measures make the EU one of the most regulated and sustainability-driven markets for polycarbonate packaging globally.

United States: FDA Restrictions, State-Level Bans, and EPR Expanding Market Compliance

In the United States, the Food and Drug Administration (FDA) continues to regulate BPA usage in food packaging. Polycarbonate resins are prohibited in infant feeding bottles and sippy cups, with safety remaining a key driver across the broader food-contact market. Regulatory measures are also evolving at the state level, such as New Mexico’s 2027 ban on PFAS in food packaging, which signals a trend toward broader chemical restrictions in packaging materials.

At the same time, California’s Extended Producer Responsibility law (SB-54) requires a 25% reduction in virgin plastic packaging and mandates producer participation in Producer Responsibility Organizations (PROs) by 2025. The U.S. Plastics Pact is also advancing a circular economy framework, encouraging higher recyclability and reusability of food packaging, including polycarbonate alternatives. Industry responses include investment in bio-based polymers and composite blends to replace traditional PC resins. The U.S. plastics sector is also advancing automation, adding over 1,600 robotic units in 2023, improving precision and lowering costs in packaging production. These dynamics are reshaping the U.S. into a compliance- and innovation-driven market for polycarbonate food packaging.

China: Packaging Regulations and Domestic Recycling Driving Market Evolution

China’s polycarbonate food packaging market is adapting to new packaging regulations effective June 2025, which aim to reduce e-commerce delivery waste and promote recycled and reusable systems. The National Development and Reform Commission (NDRC) and the Ministry of Ecology and Environment (MEE) are jointly enforcing stricter controls on plastic pollution, directly influencing material choices for polycarbonate packaging.

China’s positive list system for food-contact materials, alongside new adhesive standards effective February 2025, is shaping the development of safe and compliant packaging. A long-term driver is the 2018 ban on plastic waste imports, which has forced the country to develop domestic recycling infrastructure to supply raw materials for packaging producers. In practice, leading brands are demonstrating sustainability initiatives Coca-Cola introduced 500 ml bottles made entirely from rPET in Hong Kong, using materials sourced from mainland China. With regulators tightening oversight and industry leaders investing in recycling, China is steadily moving toward a circular economy in polycarbonate food packaging.

India: EPR Regulations and Local Recycling Innovations Supporting Sustainable Packaging

India’s polycarbonate food packaging market is governed by the Plastic Waste Management Rules (2016, amended in 2022), which emphasize Extended Producer Responsibility (EPR) for brand owners and manufacturers. This framework mandates collection and recycling of plastic waste, placing accountability on companies to ensure sustainable end-of-life management. The FSSAI is holding consultations on food-grade sustainable packaging, encouraging businesses to transition toward biodegradable and recyclable alternatives.

Domestic companies are investing in large-scale recycling projects to reduce dependency on polycarbonate resins. Varun Beverages, in collaboration with Indorama Ventures, is constructing a major PET recycling plant to meet rising demand for food-grade recycled PET, which could replace polycarbonate in some applications. Meanwhile, the Swachh Bharat Abhiyan (Clean India Mission) continues to push for improved waste collection and segregation, strengthening the ecosystem for recycling-based packaging. Together, these initiatives highlight India’s transition toward a circular economy for food packaging with innovation-driven alternatives to traditional polycarbonate.

Japan: Positive List Compliance and R&D in Substitutes for Polycarbonate

Japan’s polycarbonate food packaging market is regulated under the positive list system for synthetic materials, which came fully into effect on June 1, 2025. This system, administered by the Consumer Affairs Agency (CAA), sets out approved materials for food packaging applications, ensuring polycarbonate usage aligns with safety requirements. Any new materials require technical approval through this rigorous process, strengthening compliance obligations for packaging producers.

Innovation in Japan is focused on developing durable and recyclable plastics that can substitute conventional resins, including polycarbonate, in food-contact applications. Government initiatives aimed at waste reduction and recycling are reinforcing circular economy practices, ensuring packaging manufacturers prioritize sustainability in both design and materials. With strict material approval processes and strong R&D investment, Japan is positioning itself as a technologically advanced and regulation-driven market for food-grade packaging solutions.

United Kingdom: Plastic Packaging Tax and Circular Economy Initiatives Reshaping Market Dynamics

The United Kingdom is steering its polycarbonate food packaging market through fiscal and innovation-based initiatives. The Plastic Packaging Tax (PPT), introduced in April 2022, applies to all plastic packaging with less than 30% recycled content, creating strong financial incentives for companies to adopt recycled raw materials. The government’s target is to ensure that all packaging is recyclable by 2030, pushing companies toward single-material, easily recyclable packaging formats.

In parallel, the Smart Sustainable Plastic Packaging (SSPP) Challenge, with a £60 million public funding allocation, has already supported over 80 projects focused on plastic waste reduction and advanced recycling technologies. The UK is also preparing to implement a deposit return scheme for plastic bottles, which will impact collection infrastructure and the broader recycling ecosystem. Industry trends show growing investment in single-material recyclable packaging to replace complex composites. These efforts collectively position the UK as one of the leading European markets driving circular economy innovation in food packaging.

Polycarbonate Food Packaging Market Report Scope

Polycarbonate Food Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.9 Billion

|

|

Market Size (2034)

|

$3.9 Billion

|

|

Market Growth Rate

|

8.2%

|

|

Segments

|

By Product Type (Jars & Containers, Bottles, Food Storage Boxes, Tableware & Kitchenware, Baby Bottles, Water Cooler Bottles), By Application (Baby Food & Formula, Beverages, Food Services, Bakery & Confectionery, Ready-to-Eat Meals, Fresh Produce), By End-Use (Residential, Commercial), By Form (Rigid Packaging, Semi-Rigid Packaging)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

SABIC, Covestro AG, Teijin Limited, Mitsubishi Engineering-Plastics Corporation, Chi Mei Corporation, Trinseo, LG Chem, Lotte Chemical Corporation, Sumitomo Chemical Co., Ltd., T&T Plastic Containers, RTP Company, PolyOne Corporation (Avient), Amcor plc, Novolex Holdings, LLC, Greif, Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Polycarbonate Food Packaging Market Segmentation

By Product Type

- Jars & Containers

- Bottles

- Food Storage Boxes

- Tableware & Kitchenware

- Baby Bottles

- Water Cooler Bottles

By Application

- Baby Food & Formula

- Beverages

- Food Services

- Bakery & Confectionery

- Ready-to-Eat Meals

- Fresh Produce

By End-Use

By Form

- Rigid Packaging

- Semi-Rigid Packaging

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Polycarbonate Food Packaging Market

- SABIC

- Covestro AG

- Teijin Limited

- Mitsubishi Engineering-Plastics Corporation

- Chi Mei Corporation

- Trinseo

- LG Chem

- Lotte Chemical Corporation

- Sumitomo Chemical Co., Ltd.

- T&T Plastic Containers

- RTP Company

- PolyOne Corporation (Avient)

- Amcor plc

- Novolex Holdings, LLC

- Greif, Inc.

* List Not Exhaustive

Methodology

USDAnalytics employs a comprehensive and structured research methodology to deliver precise insights into the Polycarbonate Food Packaging Market. Our approach integrates primary research, including interviews with industry leaders, packaging manufacturers, sustainability experts, and regulatory authorities, with secondary research drawn from company reports, trade publications, government regulations, academic studies, and press releases. Quantitative modeling and forecasting are applied to evaluate market size, growth projections, and segmentation by product type (water cooler bottles, baby bottles, jars, containers, food storage boxes, tableware), application (beverages, baby food & formula, food services, bakery & confectionery, ready-to-eat meals, fresh produce), end-use (residential, commercial), and form (rigid, semi-rigid). USDAnalytics also examines technological advancements, including BPA-free innovations, bio-based polycarbonates, chemical recycling, and circular economy initiatives. Regional regulatory landscapes across North America, Europe, China, India, Japan, and the UK are incorporated to assess compliance-driven market shifts. Our methodology emphasizes sustainability, functional performance, and market adaptability, providing industry professionals with actionable intelligence for strategic planning, investment decisions, and operational optimization in the global polycarbonate food packaging sector.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.