Market Overview: Thermal Performance Expansion and Circular Design Economics Elevate Polyester Hot Melt Adhesives

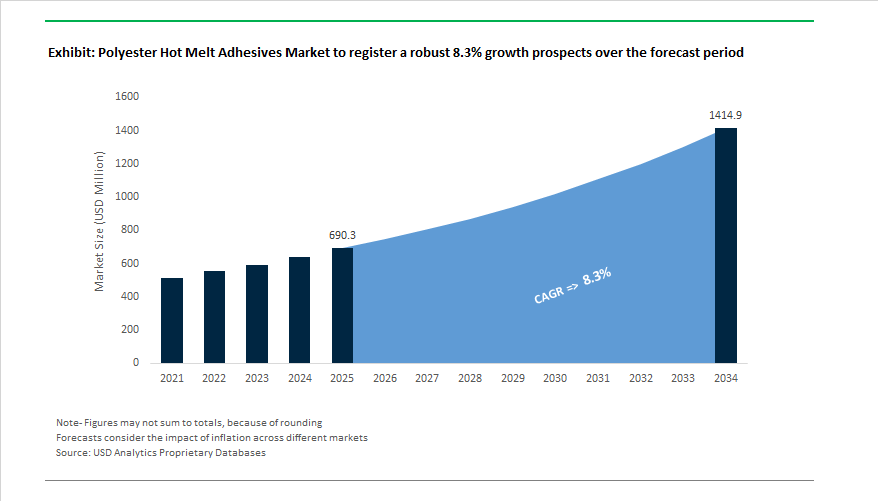

The Global Polyester Hot Melt Adhesives (PHMA) Market is projected to expand from USD 690.3 million in 2025 to USD 1414.8 million by 2034, advancing at a CAGR of 8.3%, as manufacturers increasingly require bonding systems that operate reliably at higher temperatures, under moisture stress, and within sustainability-constrained production models. Growth is being driven by substitution away from conventional EVA and polyolefin hot melts in applications where creep resistance, hydrolytic stability, and thermal endurance have become limiting factors for product performance and warranty risk.

A central growth lever is the rising adoption of reactive polyester hot melt adhesives (R-PHMAs), which extend the operating temperature window of traditional thermoplastic hot melts. These systems—capable of maintaining cohesive integrity at temperatures up to +180°C—are gaining importance in under-the-hood automotive components, EV battery assemblies, electronics housings, and industrial filtration, where exposure to sustained heat and cyclic loading is unavoidable. Manufacturers such as Henkel and H.B. Fuller are increasingly positioning reactive polyester systems as alternatives to polyamide hot melts and certain reactive polyurethanes, offering a balance of thermal performance and processing simplicity.

In parallel, non-reactive polyester HMAs continue to expand in textiles, footwear, furniture lamination, and packaging, supported by their high crystallinity (50–60%), which translates into superior creep resistance and tensile strength in bonded laminates. Their low moisture vapor transmission rates (as low as 0.2 g/m²·24h) are reinforcing adoption in moisture-sensitive packaging structures and electronic potting applications, where barrier performance directly affects shelf life and device reliability. Hydrolytic durability is a further differentiator: modern polyester formulations retaining over 90% shear strength after 1,000 hours of water immersion at 70°C are increasingly specified for washable textiles, outdoor components, and filtration media, where repeated exposure to heat and humidity is routine.

In October 2025, Henkel AG & Co. KGaA announced a €20 million investment in the modernization of its Bopfingen, Germany plant, expanding capacity for TECHNOMELT industrial adhesives, including high-heat polyester formulations. This move reflects Henkel’s long-term strategy to strengthen its European footprint in industrial adhesives for packaging, electronics, and automotive sectors. Just a month earlier, in September 2025, Henkel introduced a carbon-optimized upgrade to its TECHNOMELT SUPRA 130 Cool line, achieving a 20% cradle-to-gate carbon emission reduction, underscoring the growing focus on sustainability and energy efficiency in polyester-based systems.

The trend toward bio-based and recyclable hot melt adhesives continues to gain traction. In May 2025, H.B. Fuller Company announced a partnership with a global polymer supplier to ensure a stable feedstock of bio-based polyesters, supporting its next generation of sustainable hot melt products. Similarly, Bostik (Arkema Group), in March 2025, showcased a major R&D breakthrough in polyester web adhesives, introducing VOC-free formulations with low-temperature activation for automotive lamination and footwear manufacturing.

Regulatory momentum also accelerated during July 2025, when the European Union intensified its Packaging Waste Directive revisions, prioritizing recyclable mono-material packaging designs. This policy change is compelling manufacturers to develop PET-compatible polyester adhesives, accelerating market expansion.

On the corporate innovation front, H.B. Fuller’s acquisition of a UK-based adhesive manufacturer (September 2024) expanded its European reach in reactive hot melt technology. Meanwhile, 3M and Jowat SE announced product expansions (July–June 2024), introducing low-surface-energy plastic bonding and reactive PUR polyester hot melts to cater to the growing demand from electronics, furniture, and textile manufacturers in Asia-Pacific.

Notably, DOW Inc. reinforced its leadership in advanced adhesive polymers for EV battery assemblies (January 2025), leveraging polyester-derived resins to enhance thermal management and structural bonding—critical for next-generation electric mobility solutions.

Market Trend 1: Formulation for High-Temperature Resistance in Automotive and Electronics Assembly

The shift toward electric vehicles (EVs) and lead-free electronics manufacturing is significantly redefining adhesive formulation priorities. The growing prevalence of high-heat, high-stress assembly environments in these sectors has accelerated demand for thermally stable polyester hot melt adhesives (HMAs) capable of maintaining mechanical integrity under extreme temperature conditions.

In EV battery modules, adhesives must retain cohesive and adhesive strength at sustained operating temperatures around 80°C, particularly in bonding and encapsulating components like cell holders and electrical housings. Traditional EVA or polyolefin-based adhesives, which soften under such conditions, are increasingly being replaced by polyester HMAs that exhibit melting points up to 250°C and excellent resistance to creep and delamination. The high-temperature endurance ensures dimensional stability and bond reliability, especially in under-hood, thermal interface, and vibration-prone areas of electric vehicles.

In the electronics sector, the global shift to lead-free soldering, which requires solder reflow temperatures exceeding 240°C, has created a strong market for polyester-based HMAs as temporary or permanent bonding agents during assembly. These adhesives provide precise viscosity control, thermal endurance, and compatibility with surface mount devices (SMDs), offering manufacturers a superior alternative for securing components on flexible circuits and display modules. As electronics miniaturization continues, polyester HMAs’ combination of low shrinkage, high adhesion, and stable glass transition (Tg) positions them as indispensable in thermal-sensitive, miniaturized assemblies.

Market Trend 2: Development of Bio-Based and Chemically Recyclable Polyester HMAs

Global sustainability mandates and the circular economy transition are reshaping adhesive chemistry, propelling investment into bio-based and recyclable polyester HMAs derived from renewable feedstocks. A major breakthrough in the domain is the commercialization of bio-based monomers such as 2,5-Furandicarboxylic Acid (FDCA), synthesized from lignocellulosic biomass. FDCA enables the production of polyethylene furanoate (PEF) and related polyesters that achieve glass transition temperatures (Tg) up to 89°C and tensile strengths around 66.7 MPa, providing a mechanical performance comparable to traditional terephthalic-based polyester systems while being fully sustainable.

The bio-based innovation is complemented by industry-level investments in renewable polyester intermediates. For instance, a leading global supplier of bio-succinic acid—a key precursor for polyester polyols—has earned USDA 100% Certified Biobased Content recognition, reinforcing the traceability of renewable inputs in adhesive formulations. The global production of bio-based hot melt adhesives surpassed 600,000 metric tons in 2024, marking a 21% year-on-year increase, as industries such as packaging, footwear, and automotive accelerate the shift toward low-carbon, non-petrochemical raw materials.

Equally significant is the emergence of chemically recyclable polyester adhesives, designed for compatibility with mechanical and depolymerization-based recycling streams. By enabling adhesives that can be separated and reused without contaminating post-consumer resin (PCR), the innovation supports the broader polymer circularity objectives outlined under frameworks such as the EU Green Deal and U.S. EPA’s National Recycling Strategy.

Market Opportunity 1: Penetrating the Sustainable Footwear Manufacturing Value Chain

The global footwear industry’s rapid transition toward low-VOC, solvent-free adhesive technologies presents a significant growth frontier for polyester HMAs. With sustainability regulations tightening across major footwear manufacturing hubs—particularly in the EU and Asia—manufacturers are increasingly phasing out traditional solvent-based adhesives in favor of 100% solids, thermoplastic bonding solutions that reduce emissions and streamline assembly.

Polyester HMAs offer a compelling balance of flexibility, heat resistance, and adhesion strength suitable for multi-material footwear designs. Their ability to bond textiles, EVA midsoles, synthetic leathers, and rubbers makes them ideal for both athletic and casual footwear manufacturing. Compared to polyurethane (PU) and EVA-based hot melts, polyester HMAs deliver higher cohesive strength and superior elasticity retention, essential for long-term durability under flexural stress.

From a manufacturing perspective, these adhesives enhance production efficiency by enabling rapid green strength development, eliminating lengthy drying cycles, and ensuring consistent adhesion under automated or robotic application systems. The industry’s ongoing VOC compliance push further accelerates polyester HMA adoption, as these formulations inherently meet ISO 14001 environmental standards and align with the EU REACH directive on restricted chemicals. The positions polyester HMAs as the leading solution for manufacturers targeting both sustainability and performance-driven bonding systems in next-generation footwear production.

Market Opportunity 2: Servicing the Proliferation of Multi-Material and Composite Packaging

The evolution of high-barrier, multi-material packaging—particularly for food, pharmaceutical, and industrial applications—presents a second major growth opportunity for polyester hot melt adhesives. As flexible packaging structures integrate polymer films, aluminum foils, and paper substrates, adhesive formulations must withstand both retort processing conditions (up to 160°C) and aggressive environmental exposure while maintaining optical and mechanical integrity.

Polyester HMAs, known for their thermal stability, chemical resistance, and strong adhesion to polar substrates, are ideally suited for lamination, sealing, and barrier enhancement in such structures. In contrast to EVA-based adhesives, they maintain cohesive strength under extreme temperature and humidity, ensuring delamination-free performance during sterilization or hot-fill packaging processes.

Major packaging converters adopting retortable and recyclable packaging formats increasingly rely on these advanced formulations to meet both performance and compliance demands under global food safety standards such as FSSC 22000 and HACCP. Further, the development of non-intentionally added substance (NIAS)-compliant polyester HMAs has become essential for achieving global food contact certification, addressing regulatory scrutiny on migration and toxicological safety.

Competitive Landscape: Strategic Company Profiles in the Global Polyester Hot Melt Adhesives Industry

The Polyester Hot Melt Adhesives Market is defined by strong competition between multinational adhesive manufacturers and specialty chemical producers investing in advanced polymer chemistry, sustainability, and application-specific innovation. Companies like Henkel, H.B. Fuller, Bostik, 3M, Jowat SE, and DOW dominate the market through vertical integration, R&D-driven differentiation, and expanding global footprints.

Henkel continues to lead global adhesive innovation, investing over €400 million in R&D (2024) to expand its TECHNOMELT portfolio for packaging, consumer goods, and electronics applications. The company operates more than 150 production sites worldwide, ensuring unmatched supply chain reliability. Its sustainability focus is evident in the TECHNOMELT SUPRA PRO line, which minimizes migration risks for food packaging and meets EU green compliance standards. Furthermore, Henkel’s integration of metallocene polymer technology enhances product thermal stability, reduces charring, and improves line efficiency in high-volume manufacturing environments.

H.B. Fuller stands at the forefront of reactive hot melt (RHM) innovation, offering specialized polyester and polyether adhesives for technical textiles, automotive, and construction applications. The company’s bio-based formulations, replacing up to 30% fossil content, reflect its sustainability-driven innovation. Its strategic acquisition in Europe (2024) expanded its regional presence by 15%, while its VOC-free, solvent-free polyester adhesives meet stringent global air quality standards. By integrating bio-renewable feedstocks through supplier partnerships, H.B. Fuller reinforces its leadership in low-emission industrial adhesives.

Bostik, a subsidiary of Arkema, specializes in polyester web adhesives for lamination, technical textiles, and footwear components requiring wash and dry-clean resistance. Key products such as PE85 polyester web provide easy handling and precise application. Arkema’s €250 million investment (2024) in its Adhesive Solutions segment supported the expansion of low-temperature activation products for temperature-sensitive substrates. With a strong sustainability agenda and a focus on automotive upholstery and footwear, Bostik’s VOC-free formulations are setting benchmarks for performance and environmental compliance.

3M maintains its leadership through high-performance adhesive films and tapes designed for electronics assembly, transportation, and medical devices. Its polyester hot melt adhesives—available in thicknesses as low as 0.05 mm—offer exceptional strength and thermal stability. With annual R&D reinvestment of 6% of sales, 3M continuously advances polymer chemistry for metal-to-plastic bonding and microelectronics integration. Under its rigorous <10 ppm contamination control, 3M delivers adhesives with unmatched precision and consistency for critical electronic and industrial applications.

Jowat SE specializes in polyester-based PUR hot melts for woodworking, furniture, and textile applications. As a core supplier to Europe’s edgebanding and profile wrapping industry, Jowat’s moisture-resistant adhesives comply with E1 and F4 star emission standards. With 22 subsidiaries worldwide, the company combines localized service with deep technical expertise—over 80% of its sales force holds advanced technical qualifications. Jowat’s innovation focus on low-emission, durable polyester adhesives ensures strong alignment with sustainability-driven furniture and interior design trends.

DOW Inc. plays a crucial upstream role, supplying high-quality polyester base polymers for hot melt adhesive producers worldwide. Its specialty resins are integrated into up to 70% of modern vehicles, supporting both structural and non-structural bonding. The company’s 100+ manufacturing sites across 30 countries ensure stable resin supply chains, while joint development projects with Tier 1 automotive suppliers enable next-generation adhesive qualification for EV assembly and infrastructure applications. DOW’s material science expertise remains critical to advancing the durability and temperature resistance of polyester-based HMAs.

Country Analysis: Regional Technological Advancements and Market Expansion in the Global Polyester Hot Melt Adhesives (PHMA) Industry

China: Expanding Domestic Innovation and Industrial Application in Eco-Friendly Polyester Hot Melt Adhesives

China dominates the Asia-Pacific Polyester Hot Melt Adhesives (PHMA) market, underpinned by strong government initiatives promoting solvent-free and eco-friendly adhesive technologies. National industrial programs are accelerating the transition from traditional solvent-borne adhesives toward sustainable polyester-based hot melt systems, reinforcing China’s leadership in environmentally responsible manufacturing. Major domestic producers, supported by global chemical multinationals, are investing heavily in capacity expansions to meet growing demand across sectors such as automotive, textiles, and packaging.

The country’s textile and non-woven fabric industry remains a cornerstone application area, with automated lamination lines increasingly adopting specialized PHMAs that ensure soft feel, wash durability, and high adhesion strength. In the automotive sector, high-temperature-resistant PHMAs are integral to lightweighting initiatives, particularly for EV battery packs and interior trim laminations. Additionally, China’s booming e-commerce sector is creating immense demand for sustainable PHMAs in carton and case sealing, while electronics miniaturization is driving the adoption of PHMA powders and microbeads for precision bonding in miniature assemblies. Backed by local R&D, infrastructure development, and a robust policy framework, China is emerging as the global hub for advanced PHMA production and application diversification.

United States: Technological Leadership and Sustainable Formulation Innovation Driving PHMA Growth

The United States polyester hot melt adhesives market is characterized by cutting-edge R&D, strategic acquisitions, and an accelerating shift toward sustainable, bio-based adhesive chemistries. Major U.S.-based manufacturers are developing partially bio-based PHMA formulations that meet low-VOC emission standards, aligning with corporate sustainability targets and evolving EPA guidelines. The new-generation adhesives cater to non-woven hygiene, packaging, and industrial bonding applications, offering both performance reliability and environmental compliance.

In the automotive sector, U.S. innovation focuses on ultra-high-performance PHMAs that bond dissimilar materials such as metals, composites, and engineered plastics, crucial for EV lightweighting and battery assembly. Furthermore, federal infrastructure investments are indirectly fueling PHMA demand for construction materials and civil engineering projects requiring durable, flexible adhesive systems. The electronics and semiconductor industries are also emerging as growth frontiers, with R&D directed toward PHMAs exhibiting superior dielectric properties and thermal management. High-speed packaging automation, particularly in food and beverage manufacturing, is boosting demand for fast-curing, long open-time polyester hot melts. Strategic mergers and acquisitions are enhancing domestic production capacity, positioning the U.S. as a global leader in performance-driven and eco-conscious PHMA innovation.

Germany: Industry 4.0 and Regulatory-Driven Innovation Strengthening Europe’s PHMA Leadership

Germany stands at the forefront of Europe’s PHMA market, driven by automotive electrification, Industry 4.0 manufacturing, and stringent VOC reduction regulations. The country’s world-class automotive OEMs are major consumers of thermally stable polyester hot melts, which are essential for headliners, acoustic dampening, battery enclosures, and interior laminations. With the EU’s progressive environmental mandates, German manufacturers are rapidly transitioning from solvent-borne to 100% solid, low-emission PHMAs, positioning them as leaders in eco-regulated adhesive innovation.

The nation’s textile machinery industry also plays a pivotal role, fostering the development of reactive PHMAs that offer superior water resistance and high bonding strength for technical textiles and performance apparel. Academic and industrial collaborations—particularly involving BASF, Henkel, and Fraunhofer Institutes—are pushing the boundaries of PHMA chemistry, exploring self-healing, recyclable, and thermally conductive polymer systems. Moreover, Germany’s specialty packaging sector relies on PHMAs for tamper-evident seals and high-clarity labeling adhesives that meet luxury and pharmaceutical standards. The integration of smart automation systems and precision dispensing technologies solidifies Germany’s position as a European powerhouse in advanced PHMA engineering and sustainability-driven adhesive production.

Japan: Advanced Manufacturing and Miniaturization Driving High-Precision PHMA Development

Japan’s Polyester Hot Melt Adhesives market is distinguished by its emphasis on precision engineering, electronics miniaturization, and high-reliability manufacturing. Leading Japanese firms are pioneering ultra-low viscosity PHMAs in powder and microbead forms, designed for micro-bonding in compact electronic devices, offering exceptional thermal stability and cycling resistance. The materials are indispensable for consumer electronics, flexible circuits, and semiconductor assemblies, where performance consistency is paramount.

Innovation in multi-layer film lamination and high-barrier packaging further underscores Japan’s leadership in PHMA for industrial and consumer applications. R&D initiatives focus on biodegradable and recyclable polyester-based formulations, aligning with Japan’s circular economy goals and sustainability agenda. High-speed, precision-based manufacturing systems—often integrated with robotics—demand PHMAs that feature rapid setting times, excellent flow properties, and non-stringing performance. Beyond industrial use, medical-grade PHMAs are being developed for non-implantable devices, offering biocompatibility and sterilization resistance. Combining world-leading automation expertise and materials science, Japan continues to define the global benchmark for PHMA innovation in electronics, packaging, and sustainable materials.

India: Expanding Manufacturing Infrastructure and E-Commerce Driving Demand for Cost-Effective PHMAs

India’s Polyester Hot Melt Adhesives industry is rapidly evolving, fueled by manufacturing expansion, booming e-commerce logistics, and growing automotive production. Major adhesive manufacturers are expanding hot melt production facilities in industrial hubs such as Gujarat, focusing on cost-effective, high-volume PHMAs for packaging and hygiene non-wovens. The nation’s automotive manufacturing surge, driven by export growth and rising domestic demand, is propelling PHMA consumption in interior trim bonding, filter assembly, and cable harnessing.

India’s massive textile and apparel manufacturing base is increasingly adopting PHMAs for seamless garment lamination, flocking, and technical fabrics, ensuring superior wash durability and comfort. The rapid expansion of digital commerce further elevates demand for fast-setting, high-strength PHMAs in carton sealing, packaging, and tamper-evident applications. Supported by the “Make in India” initiative, domestic production of advanced polymer adhesives is receiving policy support to reduce import dependency. Moreover, national infrastructure development projects are driving uptake in construction and insulation applications, reinforcing India’s emergence as a strategic manufacturing and consumption hub for PHMAs in South Asia.

France: R&D Leadership and High-End Industrial Applications Elevating the PHMA Market

France represents a critical European innovation hub for advanced PHMA development, combining industrial R&D investment, aerospace expertise, and sustainable construction practices. Leading multinational chemical companies are investing heavily in French R&D centers to develop next-generation PHMAs that meet both performance and environmental criteria. The country’s aerospace industry leverages high-temperature-resistant, lightweight PHMAs for composite bonding and non-critical structural assemblies, ensuring strong, flexible adhesion in extreme conditions.

In the luxury packaging segment, France’s globally recognized consumer goods and cosmetics industries drive demand for specialty PHMAs offering high clarity, non-yellowing characteristics, and invisible bonding performance to maintain aesthetic integrity. The construction sector benefits from eco-certified PHMAs compliant with energy-efficient building standards, especially in insulation and panel bonding. French automakers are also adopting flexible PHMAs for Noise, Vibration, and Harshness (NVH) reduction, enhancing interior comfort. With its robust research ecosystem, sustainability-driven regulations, and presence of global adhesive manufacturers, France is cementing its role as a European center for premium, high-performance PHMA technology and innovation.

Polyester Hot Melt Adhesives Market Report Scope

Polyester Hot Melt Adhesives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$690.3 Million

|

|

Market Size (2034)

|

$1,414.8 Million

|

|

Market Growth Rate

|

8.3%

|

|

Segments

|

By Product Type (Aromatic, Aliphatic, Bio-based / Sustainable, Reactive), By Application (Packaging and Paper Converting, Textiles and Non-Wovens, Automotive and Transportation, Electrical and Electronics, Woodworking and Furniture, Bookbinding and Printing, Others), By Form (Pellets / Granules, Powder / Web, Sticks, Films / Sheets

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Henkel AG & Co. KGaA, H.B. Fuller Company, Arkema Group (Bostik), 3M Company, Dow Inc., Sika AG, Jowat SE, Evonik Industries AG, Avery Dennison Corporation, Toyobo Co., Ltd., Beardow Adams, Mitsubishi Chemical Corporation, Paramelt B.V., TEX YEAR INDUSTRIES INC., Huntsman International LLC

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Product Type / Chemistry

- Aromatic

- Aliphatic

- Bio-based / Sustainable

- Reactive

By Application / End-Use Industry

- Packaging and Paper Converting

- Textiles and Non-Wovens

- Automotive and Transportation

- Electrical and Electronics

- Woodworking and Furniture

- Bookbinding and Printing

- Others

By Form

- Pellets / Granules

- Powder / Web

- Sticks

- Films / Sheets

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Polyester Hot Melt Adhesives Market

- Henkel AG & Co. KGaA

- H.B. Fuller Company

- Arkema Group (Bostik)

- 3M Company

- Dow Inc.

- Sika AG

- Jowat SE

- Evonik Industries AG

- Avery Dennison Corporation

- Toyobo Co., Ltd.

- Beardow Adams

- Mitsubishi Chemical Corporation

- Paramelt B.V.

- TEX YEAR INDUSTRIES INC.

- Huntsman International LLC

*- List not Exhaustive

Research Coverage

This report investigates the Global Polyester Hot Melt Adhesives (PHMA) Market, delivering analysis reviews on demand inflections, performance benchmarks, and cost-to-serve economics while it highlights regulatory tailwinds (REACH, RoHS), mono-material packaging compatibility, and the shift to bio-based and reactive chemistries; it synthesizes technology breakthroughs—from high-crystallinity, high-Tg polyester backbones to VOC-free web films and +180 °C-capable reactive PHMAs—into practical sourcing, application engineering, and scale-up roadmaps. Built by USDAnalytics, the study quantifies throughput gains, green-strength windows, and hydrolytic durability across automotive, electronics, packaging, and textiles use cases, stress-tests scenarios against resin volatility and energy prices, and benchmarks leading suppliers on carbon intensity and innovation cadence—making this report an essential resource for procurement leaders, converters, and OEM engineers targeting reliable, sustainable bonding at industrial scale.

Scope Highlights

Segmentation:

- By Product Type / Chemistry: Aromatic; Aliphatic; Bio-based / Sustainable; Reactive.

- By Application / End-Use Industry: Packaging and Paper Converting; Textiles and Non-Wovens; Automotive and Transportation; Electrical and Electronics; Woodworking and Furniture; Bookbinding and Printing; Others.

- By Form: Pellets / Granules; Powder / Web; Sticks; Films / Sheets.

- By Region: North America (United States, Canada, Mexico); Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe); Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC); South & Central America (Brazil, Argentina, Rest of SCA); Middle East & Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa).

Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

Time Horizon: Historic data 2021–2024 and forecasts 2025–2034.

Companies: Analysis / profiles of 15+ companies.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.