Poultry Packaging Market Size, Overview, and Growth Outlook (2025–2034)

Poultry Packaging Market to Reach $5.3 Billion by 2034 Driven by Hygiene, Shelf-Life, and Case-Ready Innovations

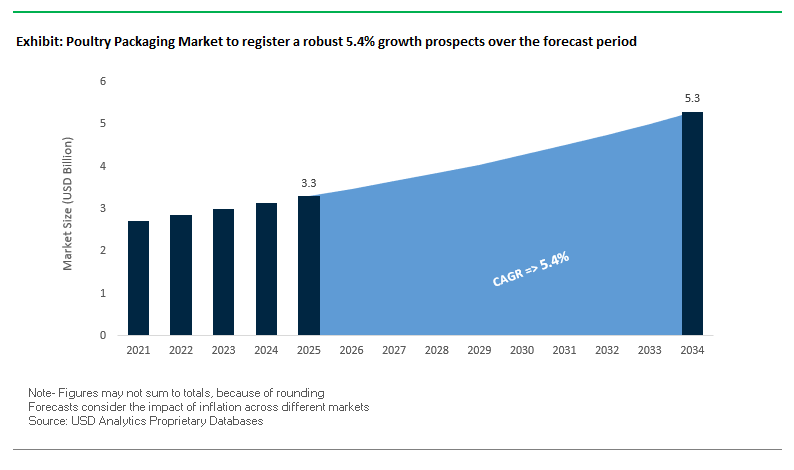

The global poultry packaging market is projected to grow from $3.3 billion in 2025 to $5.3 billion by 2034, at a CAGR of 5.4%, reflecting strong demand for solutions that ensure food safety, extend shelf life, and improve convenience. Packaging plays a critical role in protecting poultry from contamination, maintaining freshness, and meeting evolving consumer preferences. The increasing adoption of vacuum and modified atmosphere packaging (MAP), along with case-ready solutions, is reshaping the poultry supply chain.

Key Insights for industry professionals and buyers:

- Hygiene and Food Safety as a Priority: Over 85% of consumers rank hygiene and safety as top factors when purchasing fresh poultry, emphasizing the importance of high-barrier packaging solutions.

- Case-Ready Packaging on the Rise: Centralized preparation reduces labor, limits in-store handling, and minimizes contamination risks.

- Plastic Dominance with Sustainable Alternatives Emerging: Rigid trays and flexible films remain preferred due to durability, barrier properties, and cost-effectiveness, while eco-friendly materials gain traction.

- Consumer Demand for Transparency: Clear packaging allows shoppers to inspect products visually, driving innovation in transparent films and trays without compromising safety.

- Extended Shelf Life and Reduced Waste: High-barrier films and vacuum packaging support longer freshness, reducing spoilage and enhancing retailer profitability.

- Versatility Across Fresh and Frozen Poultry: Packaging solutions must meet the functional needs of both fresh and frozen product lines, supporting a wide variety of retail formats.

Market Analysis: Recent Industry Innovations Highlight Sustainability, High-Barrier Technologies, and Strategic Mergers

The poultry packaging industry is seeing rapid innovations driven by sustainability, high-barrier materials, and technological advances. In August 2025, a study in Nano Letters introduced an inhibitor-modified atomic layer deposition (ALD) strategy for ultrathin films, signaling a potential breakthrough in nanocoatings for high-barrier poultry packaging. That same month, Mondi ramped up production of its FunctionalBarrier Paper Ultimate, providing an ultra-high barrier paper alternative to traditional plastics, posing a competitive challenge to conventional poultry packaging solutions.

Strategic mergers and partnerships are also reshaping the competitive landscape. In July 2025, Smurfit Kappa and WestRock merged to form Smurfit WestRock, creating a stronger global presence in the food packaging sector. That month, Laitram Machinery joined The Poultry Federation as an allied member, reflecting a commitment to advancing operational efficiency and industry standards in Arkansas, Missouri, and Oklahoma. Additionally, sustainability trends are reinforced by Mondi and Saga Nutrition’s June 2025 launch of a sustainable paper-based pet food bag, illustrating transferable innovations for poultry packaging.

Investments in capacity expansion and circularity are shaping market growth. In November 2024, ORBIS Corporation expanded its Ohio plant by 30%, increasing tote and pallet production for poultry transport. February 2025 saw Tetra Pak introduce ISCC PLUS certified recycled polymers in India, supporting circular economy initiatives. April 2025 marked Nfinite Nanotechnology’s collaboration with Amcor to validate nanocoating technology for improved oxygen barrier performance.

Emerging Trends and Opportunities in the Poultry Packaging Market

Accelerated Adoption of High-Barrier, Leak-Resistant Modified Atmosphere Packaging (MAP)

Modified Atmosphere Packaging (MAP) is rapidly transforming poultry packaging as processors focus on extending shelf life, reducing waste, and ensuring food safety. Academic research on chicken thigh meat demonstrated that MAP can extend shelf life by up to nine days compared to conventional packaging, a critical advantage in global supply chains where logistics delays can lead to spoilage. By retarding lipid oxidation and suppressing microbial growth, MAP directly addresses two of the most significant challenges in poultry preservation: freshness and food waste reduction. Research published in Poultry Science further validated these findings, showing that high-oxygen MAP (HiOx-MAP) significantly inhibits spoilage organisms in ground chicken patties while maintaining the bright red color preferred by consumers. This dual benefit—enhanced food safety and greater consumer appeal—is fueling adoption across retail and wholesale channels. Moreover, the leak-resistant designs being integrated into MAP systems reduce contamination risks during transportation and handling, reinforcing MAP’s position as a premium, safety-driven packaging solution in the poultry sector.

Strategic Shift to Incorporate Post-Consumer Recycled (PCR) Content

Sustainability commitments are driving poultry packaging suppliers to integrate post-consumer recycled (PCR) materials without compromising performance. A notable collaboration between DSM, SABIC, and Viscofan demonstrated how advanced recycling of mixed post-consumer plastics can be used to create high-barrier casings for meat products, a critical step toward circular packaging systems. This initiative showcased how PCR can be reintroduced into demanding food-contact applications that traditionally relied on virgin resins. Similarly, Tekni-Plex introduced an egg carton incorporating 25% PCR foam polystyrene, signaling an industry-wide push to embed sustainability directly into mainstream products. The shift is not only regulatory-driven but also consumer-led, as brands increasingly differentiate themselves through environmental stewardship. With Extended Producer Responsibility (EPR) policies expanding globally and corporate ESG reporting under tighter scrutiny, the use of PCR in poultry packaging is becoming a non-negotiable strategy for brand competitiveness and compliance with upcoming regulations.

Development of High-Performance Bio-Based and Compostable Films

The poultry packaging market presents a high-growth opportunity for bio-based and compostable films that meet both safety and sustainability requirements. Chitosan-based films, derived from crustacean shells, are emerging as a promising material thanks to their strong antimicrobial activity, which helps inhibit harmful bacteria on raw meat surfaces. This property makes them particularly relevant in poultry packaging, where microbial contamination is a primary concern. In parallel, academic studies on polylactide (PLA)-based films enhanced with bimetallic nanoparticles or essential oils have shown significant improvements in antimicrobial performance and barrier properties. These engineered films are demonstrating the potential to match or surpass conventional plastics in protecting highly perishable poultry products. For processors and retailers, this represents a twofold opportunity: reducing environmental impact by moving away from fossil-based plastics while simultaneously improving food safety. The commercialization of such bio-based films could redefine the poultry packaging value chain by combining consumer health benefits with measurable ESG gains.

Integration of Smart Packaging for Enhanced Traceability and Food Safety

Smart packaging technologies are emerging as a transformative opportunity in poultry packaging, especially given the product’s short shelf life and strict cold chain requirements. Intelligent packaging systems that embed gas sensors can detect odor-causing compounds, providing real-time spoilage alerts that significantly reduce the risk of unsafe food reaching consumers. This early-warning system supports processors and retailers in ensuring compliance with stringent food safety regulations while protecting brand reputation. In addition, Time-Temperature Indicators (TTIs) are becoming increasingly relevant for poultry supply chains, offering irreversible visual cues if cold chain integrity is compromised. These indicators provide stakeholders across the chain—processors, distributors, retailers, and consumers—with a verifiable record of temperature exposure. By integrating TTIs or QR-code enabled digital platforms, brands can deliver transparency, enhance consumer trust, and reduce food waste. As regulatory bodies worldwide demand higher levels of traceability and food safety, the integration of smart packaging positions poultry companies at the forefront of compliance, innovation, and consumer engagement.

Competitive Landscape: Leading Poultry Packaging Companies Are Shaping Market Standards Through Innovation, Sustainability, and High-Barrier Solutions

The global poultry packaging market is dominated by companies offering advanced food safety solutions, extended shelf life technologies, and sustainable packaging options. These leaders leverage their innovation capabilities to enhance product visibility, operational efficiency, and compliance with evolving regulations.

Sealed Air Corporation (SEE): Innovating Food Safety and Shelf-Life Extension Through Advanced MAP and Vacuum Packaging

Sealed Air’s CRYOVAC® brand leads the poultry packaging market with vacuum and MAP solutions, including trays, shrink bags, and films. Its products focus on oxygen and moisture barrier performance, reducing food waste and extending freshness. The company is actively advancing recyclable CRYOVAC® Recycle-Ready Presentation Bags, addressing growing consumer demand for sustainability. Sealed Air’s automated systems integrate seamlessly with its machinery and materials, reducing manual adjustments and enhancing production efficiency.

Amcor plc: Advancing Sustainable and Case-Ready Packaging Through Innovative Films and Nanocoating Technology

Amcor offers flexible and rigid packaging solutions for fresh and frozen poultry, including vacuum and barrier films for case-ready applications. Its ICE® Coextruded Films optimize TFFS (Thermoform Fill Seal) processes, ensuring freshness and high-quality printing for shelf impact. In April 2025, Amcor partnered with a Canadian startup to test nanocoating technologies for recyclable and compostable packaging, reinforcing its strategy toward circular and sustainable solutions.

Mondi Group: Leading Paper-Based and Sustainable Alternatives to Plastic Poultry Packaging

Mondi provides films, pouches, and bags, emphasizing sustainable, paper-based solutions. In August 2025, it ramped up production of FunctionalBarrier Paper Ultimate, offering a viable high-barrier alternative to multi-layer plastics. Mondi’s vertical integration from sustainable forestry to packaging production enables comprehensive circular solutions for poultry packaging, aligning with corporate sustainability commitments under its MAP2030 initiative.

Pactiv Evergreen Inc.: Expanding Market Reach Through Acquisition and Sustainable Food Packaging Solutions

Pactiv Evergreen manufactures trays for poultry and clear rigid-display containers. Its April 2025 acquisition by Novolex Holdings creates a larger platform for food and specialty packaging. The company’s EarthChoice hinged-lid containers use 25% post-consumer recycled content and feature tamper-evident designs, reflecting a focus on sustainable, convenient, and consumer-friendly packaging solutions.

Tyson Foods, Inc.: Influencing Poultry Packaging Standards Through Strategic Supplier Engagement

While Tyson Foods does not manufacture packaging, its packaging requirements drive industry standards. Tyson uses MAP and vacuum-sealed solutions for case-ready products and collaborates with suppliers to eliminate harmful chemicals such as BPA and phthalates. Its proactive initiatives enhance food safety, reduce waste, and ensure regulatory compliance, demonstrating the impact of end-user requirements on packaging innovation.

Poultry Packaging Market Share Insights, 2025-2034

Trays Lead Market Share by Product Type in the Poultry Packaging Industry

Trays account for 35% of the poultry packaging industry, establishing themselves as the primary retail packaging format for fresh poultry. Their rigidity, ease of handling, and compatibility with breathable overwrap films make them indispensable for fresh meat presentation in supermarkets. Bags and pouches follow with 28%, serving as the growth engine for vacuum-sealed and modified atmosphere packaging (MAP) formats that extend shelf life for both fresh and frozen poultry. Films and wraps, holding 20%, play a critical enabling role since they are almost universally used alongside trays or for bundling. Boxes and cartons retain importance for secondary protection and branding, particularly in frozen breaded and processed poultry categories. Poultry containers, although niche, remain critical for B2B bulk handling and foodservice operations. This segmentation underscores how trays dominate fresh meat retail visibility, while bags and pouches capture the shift toward convenience, longer shelf life, and global cold-chain distribution.

Fresh Meat Dominates Market Share by Application in the Poultry Packaging Industry

Fresh meat packaging accounts for 45% of application share, underscoring its centrality to the poultry packaging industry. The continued shift to case-ready packaging solutions—where poultry is packaged at processing plants under controlled conditions rather than in-store—is driving innovation in high-barrier films, absorbent pads, and MAP systems that maximize shelf life and food safety. Frozen meat follows with 30%, forming a stable backbone of demand for vacuum-sealed and freezer-compatible packaging that prevents dehydration and freezer burn. Processed meat packaging (20%) is a high-value, innovation-led segment that thrives on consumer demand for convenience, leveraging resealable pouches, microwave-safe packs, and skin packaging to preserve quality and enhance shelf appeal. Egg packaging, while only 5%, remains a highly specialized and regulated category, with increasing adoption of recycled pulp and PET to meet sustainability requirements. The dominance of fresh meat packaging demonstrates how shelf life optimization, consumer safety, and retail-ready presentation are the defining competitive factors in this market.

United States: FSIS Oversight, Automation, and Cold Chain Packaging Innovation

The United States poultry packaging market is strongly shaped by regulatory oversight from the USDA’s Food Safety and Inspection Service (FSIS) and the Food and Drug Administration (FDA). While the FDA approves food packaging materials, FSIS ensures compliance within poultry plants under the Poultry Products Inspection Act of 1957. FSIS also mandates that all poultry product labels display truthful and non-misleading information, including product type, inspection status, net weight, and safe-handling instructions, which directly impacts packaging design and labeling requirements.

Innovation is accelerating in shelf-life extension technologies, with widespread adoption of Modified Atmosphere Packaging (MAP) and vacuum sealing to reduce food waste and maintain freshness. Sustainability is another core driver, as producers shift to trays made with post-industrial recycled content to meet consumer expectations and brand sustainability targets. The rise of e-commerce grocery delivery is boosting demand for robust packaging that preserves cold chain integrity in last-mile logistics. Meanwhile, automation is transforming processing lines—robotic arms are now used to weigh, wrap, and seal poultry products with higher precision and efficiency, reducing labor costs and enhancing quality control.

European Union: PPWR Regulations and Active Packaging Driving Circular Economy

The European Union poultry packaging market is at the forefront of sustainability due to the Packaging and Packaging Waste Regulation (PPWR), which took effect in February 2025. This regulation enforces recyclability and reusability standards, compelling poultry processors to redesign packaging for circularity. From 2028, all poultry packages must include a harmonized recycling label, which is creating demand for clear and standardized communication.

Producers are investing in active packaging technologies that extend shelf life and improve food safety, while packaging leaders like Mondi and Amcor are developing sustainable paper-based and high-barrier plastic films tailored for poultry. In line with Europe’s transition away from single-use packaging, IFCO’s acquisition of a meat and dairy reusable packaging pooling firm demonstrates the shift toward reusable container systems. These innovations ensure compliance with strict EU sustainability rules while supporting the poultry sector’s focus on safety and freshness.

China: E-Commerce Growth, Import Controls, and Food Safety Packaging Standards

China’s poultry packaging market is heavily influenced by government regulations aimed at both waste reduction and food safety. The June 2025 packaging regulation prioritizes recycled materials and reusable systems, particularly in the fast-growing e-commerce sector, where cold chain packaging is essential. Additionally, the General Administration of Customs of China (GACC) introduced a new requirement in April 2025 that all imported poultry products include a Product Expiration Date on customs declarations, ensuring stricter monitoring of food quality.

The NDRC and MEE continue to enforce plastic pollution controls, while the positive list system for food-contact materials and adhesive standards guide the development of compliant poultry packaging. China also enforces strict import bans on poultry products from avian influenza-affected countries, making food safety and disease control top priorities. These measures, coupled with growing domestic e-commerce demand, are driving investment in innovative and compliant poultry packaging solutions that balance safety, sustainability, and logistics efficiency.

India: EPR Framework, Government Incentives, and Cold Storage Investments

India’s poultry packaging market is expanding under the Plastic Waste Management Rules (2016, amended in 2022), which enforce Extended Producer Responsibility (EPR) for waste collection and recycling. Complementing this, the Ministry of Food Processing Industries is providing incentives through the Production Linked Incentive Scheme for Food Processing Industry (PLISFPI) to boost innovation and investments in poultry packaging and processing technologies.

The Department of Animal Husbandry & Dairying (DAHD) is actively collaborating with poultry producers to mitigate avian influenza risks through mandatory farm registration, enhanced surveillance, and strict biosecurity. At the same time, the FSSAI is engaging with businesses on sustainable packaging, fostering a transition to biodegradable and recyclable materials. The 2025 national budget includes subsidies on poultry feed, tax relief for SMEs, and investments in cold storage infrastructure, all of which strengthen the ecosystem for modern poultry packaging. Together, these policies are positioning India as a growth market for sustainable and efficient poultry packaging solutions.

Brazil: Global Export Leadership and Packaging for Shelf-Life Extension

Brazil is the world’s largest chicken exporter, making its poultry packaging industry highly sensitive to international trade agreements and disease outbreaks. To maintain competitiveness, producers are heavily investing in biosecurity and production efficiency, ensuring uninterrupted access to global markets. Packaging innovation plays a crucial role, with greater adoption of MAP and vacuum-sealed trays to extend shelf life and preserve quality during long-distance exports.

The National Solid Waste Policy is reinforcing waste reduction targets, encouraging poultry exporters to integrate sustainable packaging materials in compliance with global standards. However, recent avian influenza outbreaks have triggered import restrictions from countries such as Japan, Mauritius, and Saint Kitts and Nevis, underlining the importance of robust disease controls and packaging that assures international buyers of product safety. Brazil’s dual focus on export competitiveness and sustainability compliance makes it a pivotal player in the global poultry packaging market.

United Kingdom: Plastic Packaging Tax and Evolving Food Safety Regulations

The United Kingdom poultry packaging market is influenced by the Plastic Packaging Tax (PPT), introduced in April 2022, which imposes costs on packaging with less than 30% recycled content. This has accelerated industry adoption of recyclable and recycled-content packaging for poultry applications. The government’s long-term goal is to ensure that all packaging is recyclable by 2030, further pushing companies toward circular packaging solutions.

Regulatory oversight is also intensifying. The Department for Environment, Food & Rural Affairs (Defra) and the Scottish Government amended poultry meat marketing rules in 2025, removing the 12-week grace period for free-range status during mandatory avian influenza housing measures. This prevents market distortion and ensures fair competition among producers. At the same time, companies like Mondi are investing in paper-based recyclable poultry packaging, while the FSA’s evolving food safety standards are ensuring transparency and consumer protection. Together, these measures are creating a sustainability-focused and compliance-driven poultry packaging market in the UK.

Poultry Packaging Market Report Scope

Poultry Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$3.3 Billion

|

|

Market Size (2034)

|

$5.3 Billion

|

|

Market Growth Rate

|

5.4%

|

|

Segments

|

By Material (Plastic, Paper & Paperboard, Molded Fiber, Others), By Product Type (Trays, Bags & Pouches, Films & Wraps, Boxes & Cartons, Poultry Containers), By Packaging Technique (MAP, Vacuum, Active & Intelligent, Shrink), By Application (Fresh Meat, Frozen Meat, Processed Meat, Eggs)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, Berry Global, Inc., Mondi Group, Sealed Air Corporation, Sonoco Products Company, Tekni-Plex, Inc., Novolex Holdings, LLC, DS Smith Plc, Huhtamaki Oyj, Silgan Holdings Inc., ProAmpac, WestRock Company, Greif, Inc., Graphic Packaging Holding Company, International Paper Co.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Poultry Packaging Market Segmentation

By Material

- Plastic

- Paper & Paperboard

- Molded Fiber

- Others

By Product Type

- Trays

- Bags & Pouches

- Films & Wraps

- Boxes & Cartons

- Poultry Containers

By Packaging Technique

- MAP

- Vacuum

- Active & Intelligent

- Shrink

By Application

- Fresh Meat

- Frozen Meat

- Processed Meat

- Eggs

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Poultry Packaging Market

- Amcor plc

- Berry Global, Inc.

- Mondi Group

- Sealed Air Corporation

- Sonoco Products Company

- Tekni-Plex, Inc.

- Novolex Holdings, LLC

- DS Smith Plc

- Huhtamaki Oyj

- Silgan Holdings Inc.

- ProAmpac

- WestRock Company

- Greif, Inc.

- Graphic Packaging Holding Company

- International Paper Co.

* List Not Exhaustive

Methodology

USDAnalytics employs a rigorous, multi-dimensional research methodology to provide comprehensive insights into the Poultry Packaging Market. Our analysis combines primary research—interviews with packaging manufacturers, poultry processors, sustainability experts, and regulatory authorities—with secondary research sourced from company reports, industry journals, regulatory frameworks, trade publications, and press releases. Market sizing, growth projections, and segmentation are quantified across material types (plastic, paper & paperboard, molded fiber), product types (trays, bags & pouches, films & wraps, boxes & cartons, poultry containers), packaging techniques (MAP, vacuum, active & intelligent, shrink), and applications (fresh meat, frozen meat, processed meat, eggs). USDAnalytics also evaluates emerging trends including bio-based and compostable films, high-barrier and leak-resistant MAP, post-consumer recycled (PCR) content integration, and smart packaging technologies for traceability and cold chain management. Regional regulatory landscapes in North America, Europe, China, India, Brazil, and the UK are incorporated to assess compliance, sustainability initiatives, and market dynamics. The methodology emphasizes actionable insights on innovation, operational efficiency, regulatory compliance, and consumer-driven preferences, delivering strategic intelligence for industry professionals, investors, and supply chain stakeholders.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.