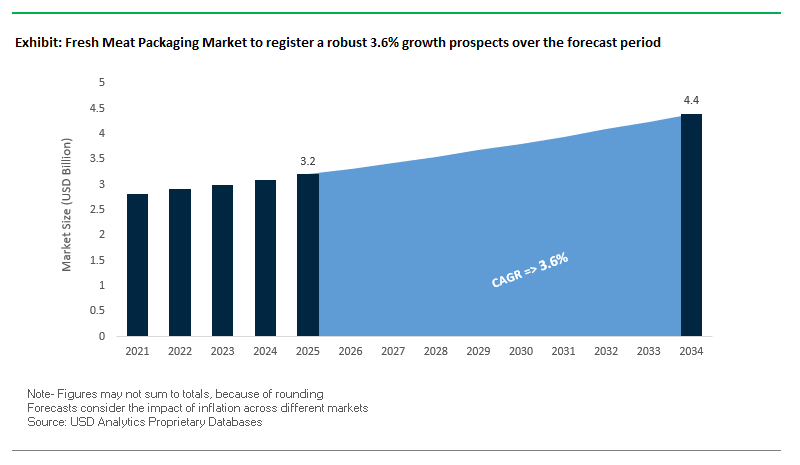

Market Overview: Fresh Meat Packaging Market to Reach $4.4 Billion by 2034

The global fresh meat packaging market is valued at $3.2 billion in 2025 and is projected to reach $4.4 billion by 2034, expanding at a CAGR of 3.6%. For food processors and retailers, packaging is no longer just about preservation it is a central tool for ensuring safety, transparency, shelf life extension, and sustainability. Industry professionals and buyers recognize fresh meat packaging as a driver of both operational efficiency and consumer trust.

The adoption of case-ready packaging by major retailers is streamlining in-store operations while improving hygiene and consistency. Vacuum Skin Packaging (VSP) and Modified Atmosphere Packaging (MAP) are becoming standards, helping to extend shelf life and reduce waste. Simultaneously, material innovation is enabling the use of mono-material recyclable films and paperboard trays that replace traditional foams. These factors are positioning fresh meat packaging as a critical enabler of both food waste reduction and circular economy targets.

Key Insights for Industry Professionals:

- Shift to Case-Ready Packaging: Improves hygiene, reduces labor, and enables consistent branding.

- Consumer Transparency: Clear, high-barrier films enhance product visibility and trust.

- Shelf Life Extension: MAP can extend freshness by up to seven days compared to traditional packaging.

- Sustainable Material Innovation: Mono-material films and paperboard trays are replacing plastic foams.

Market Analysis: Strategic Developments Reshaping Fresh Meat Packaging

The fresh meat packaging industry has seen major developments in sustainability, mergers, and new packaging formats that align with global consumer and retailer expectations.

In August 2025, Amcor reported strong fiscal Q4 results, reflecting its growth in sustainable high-barrier packaging solutions for fresh meat. The July 2025 merger between Smurfit Kappa and WestRock created Smurfit WestRock, a global packaging leader with increased focus on recyclable trays and liners. Around the same time, UK retailer Tesco expanded its use of pillow packs in May 2025, a format using 70% less plastic for minced beef, lamb, and pork, demonstrating how retail chains are accelerating sustainable adoption.

Also in May 2025, Graphic Packaging partnered with WM Morrison to replace plastic steak trays with recyclable printed board, while in April 2025, WestRock partnered with Recipe Unlimited in Canada to reduce plastic container usage through recyclable paperboard packaging. MULTIVAC’s partnership with Watttron in March 2025 introduced “Smart Heating,” improving the thermoforming of recyclable packs.

Earlier moves included Amcor’s November 2024 launch of Eco-Tite® R, the industry’s first PVDC-free recyclable shrink bag for fresh meat, poultry, and cheese. On the supply chain side, Greater Omaha Packing’s January 2024 acquisition of Heartland Proteins reinforced vertical integration in beef processing. Collectively, these events highlight how the market is being shaped by sustainability mandates, technological innovation, and industry consolidation.

Trends and Opportunities Transforming the Fresh Meat Packaging Market

E-commerce Logistics Demanding Performance-Engineered Durability

The surge in direct-to-consumer (DTC) and third-party delivery models is reshaping the fresh meat packaging market, exposing new performance demands that traditional retail formats were not designed to withstand. Packages are now expected to survive automated sortation systems, long-haul distribution, and last-mile handling, while also ensuring thermal integrity until they reach the consumer. The FDA’s observation that household refrigerators often exceed the recommended 38°F (3.3°C) underscores the importance of packaging capable of mitigating fluctuating temperature conditions.

Studies in logistics and cold chain packaging show that materials like aluminum foil paper (AFP) boxes provide both temperature stability and mechanical protection, significantly reducing product spoilage during transit. This need for dual protection has accelerated the adoption of hybrid packaging structures, combining corrugated outer shells with sustainable insulating layers such as recycled pulp or lightweight foams. These designs enhance shock absorption, leak-proofing, and thermal resistance, providing the durability required for long e-commerce journeys while maintaining food safety and quality.

Regulatory Scrutiny on Plastic Waste Driving Material Substitution

The global push to eliminate expanded polystyrene (EPS) from food packaging has become one of the strongest compliance-driven shifts in the meat packaging industry. The EU’s Single-Use Plastics Directive (SUPD) has already banned EPS in many applications, while the Packaging and Packaging Waste Regulation (PPWR) mandates full recyclability by 2030. In parallel, U.S. states such as Washington and California have imposed EPS bans on food containers, and India’s nationwide single-use plastics ban further accelerates this trend.

The pressure is not only regulatory but also financial. Under revised Extended Producer Responsibility (EPR) schemes, companies using difficult-to-recycle plastics face higher compliance fees, making EPS alternatives not only environmentally preferable but also cost-efficient. Global food and retail companies are publicly committing to phase out EPS trays and insulated coolers, replacing them with molded fiber, paperboard, and bio-based alternatives. This regulatory and corporate alignment is rapidly shifting market demand toward next-generation sustainable materials.

Development of High-Performance Molded Fiber with Integrated Insulation

The transition away from EPS opens a large-scale opportunity to develop molded fiber packaging solutions engineered for high thermal and structural performance. Academic studies show that increasing molded pulp thickness from 1mm to 5mm dramatically improves insulation properties, enabling molded fiber to approach or exceed EPS in thermal performance.

The innovation frontier is in monomaterial insulated fiber containers solutions that integrate air-trapping geometries and bio-based coatings to achieve oil, grease, and moisture resistance without plastic liners. Packaging innovators are now producing water-resistant molded fiber containers made from recycled paper, suitable for direct contact with raw or frozen meats. These fully recyclable, curbside-compatible solutions reduce contamination risks in recycling streams and align with both regulatory mandates and consumer demand for plastic-free food packaging.

Integration of Time-Temperature Indicators (TTIs) for Quality Assurance

As fresh meat distribution increasingly relies on DTC and meal-kit models, there is heightened risk of temperature abuse in last-mile delivery. Time-Temperature Indicators (TTIs) present a practical, low-cost solution that enhances safety and consumer confidence by providing a visual indicator of exposure to unsafe temperature conditions. The FDA has endorsed TTIs for seafood monitoring, highlighting their ability to alert consumers to potential spoilage risks.

For brands, TTIs provide not only consumer-facing quality assurance but also legal and operational safeguards. A study from Rutgers–Tennessee State University found that 47% of meal kit items exceeded safe surface temperature thresholds, a risk that could have been mitigated by integrated TTIs. Emerging technologies are advancing beyond basic color-change indicators to enzymatic TTIs calibrated to spoilage kinetics, delivering real-time insights into product freshness. These smart indicators reduce waste, lower liability, and can be seamlessly integrated into carton labels, film wraps, or molded fiber lids without significant cost.

Competitive Landscape: Global Leaders Advancing Fresh Meat Packaging Solutions

The fresh meat packaging market is highly competitive, with multinational corporations leveraging innovation, acquisitions, and sustainability to secure leadership positions.

Amcor: Leading with Recyclable Eco-Tite® R Shrink Bags

Amcor is a global leader in flexible and rigid packaging solutions, including MAP films, shrink bags, and thermoforming materials. In November 2024, it launched Eco-Tite® R, a recyclable PVDC-free shrink bag designed for meat and poultry, aligning with PE recycling streams. Amcor’s 2025 merger with Berry Global expanded its portfolio and operational scale, reinforcing its position in high-barrier sustainable meat packaging.

Sealed Air: Strengthening Position with Cryovac® Solutions

Sealed Air is renowned for its Cryovac® brand, which includes VSP and shrink bag solutions. These technologies not only extend shelf life but also enhance product presentation with 3D displays. Sealed Air’s integrated approach, combining packaging materials with machinery and technical support, provides end-to-end solutions for meat processors and retailers. Its strategic focus remains on food safety, waste reduction, and circular packaging innovation.

Coveris: Expanding European Leadership in Recyclable Films

Coveris holds a strong position in Europe with flexible films, pouches, and trays tailored for fresh meat. The company is investing in mono-material solutions and recently launched recyclable films with higher recycled content. Its printing expertise and material science innovations allow for customizable, visually engaging packaging that enhances shelf appeal while ensuring freshness and safety.

Berry Global: Focusing on Circularity in Meat Packaging

Berry Global, a leader in plastic packaging, has redirected focus on consumer and industrial packaging following its health and hygiene spin-off. With strong expertise in rigid and flexible plastics, Berry is expanding the use of post-consumer recycled content in its meat packaging products. Its portfolio of tubs, trays, and flexible containers supports both foodservice and retail fresh meat applications, reinforcing its commitment to circularity.

Fresh Meat Packaging Market Share Insights

Modified Atmosphere Packaging (MAP) Leads Market Share by Packaging Type in Fresh Meat Packaging

In 2025, modified atmosphere packaging (MAP) accounts for 35% of the fresh meat packaging market, making it the most widely adopted technology due to its unmatched ability to extend shelf life while maintaining product visibility. MAP trays dominate in retail for red meat and poultry, as they use carefully balanced gas mixtures typically oxygen for color retention and carbon dioxide for microbial suppression to preserve both safety and the bright red appearance consumers associate with freshness. Vacuum packaging retains a major share as the workhorse for bulk transport and primal cuts, anchoring the supply chain efficiency of case-ready meat systems. Standard flexible films continue to serve high-turnover local retail formats, while vacuum skin packaging (VSP) is the fastest-growing premium solution, eliminating purge, reducing plastic use, and enhancing visual appeal for high-value cuts and seafood. Rigid trays, though niche, remain important for marinated or value-added products requiring structured containment. This segmentation reflects how MAP dominates on shelf life and retail appeal, vacuum packaging ensures supply chain resilience, and VSP captures growth in premium and sustainable meat packaging.

Poultry Leads Market Share by Application in Fresh Meat Packaging

By application, poultry represents 30% of the fresh meat packaging market in 2025, cementing its position as the volume driver. Its global affordability, shorter production cycles, and high spoilage risk make poultry packaging innovation essential, with MAP trays widely used to maintain both appearance and safety. Beef at 25% is the value-critical segment, where MAP’s high-oxygen blends are indispensable for preserving the bright oxymyoglobin color consumers expect at retail. Pork follows closely, using similar MAP systems to balance freshness and shelf life, reflecting its global role as a staple protein. Seafood presents the most challenging category, heavily reliant on vacuum packaging to prevent rapid spoilage, with growing adoption of VSP for superior presentation and reduced purge in retail fillets. Lamb, game, and niche meats remain small but significant in markets with longer supply chains, where vacuum packaging ensures durability. Overall, the application mix shows how poultry anchors market volume, beef drives color-critical innovation, and seafood pushes technical boundaries for perishable protein packaging.

United States: Sustainability and Smart Packaging Driving Market Transformation

The U.S. fresh meat packaging market is witnessing a strong push toward sustainability and innovation, driven by consumer awareness and regulatory pressure. Companies are increasingly adopting vacuum skin packaging and shrink bags, which extend shelf life and reduce food waste, addressing critical environmental concerns. Major players like Volpi Foods are introducing recyclable packaging with reduced plastic content, supporting curbside recycling programs. Consumer safety remains a priority, with the industry moving toward BPA-free coatings and linings. Innovation in case-ready packaging, including modified atmosphere packaging (MAP) and vacuum packaging, is enhancing product efficiency and shelf life for retailers. Additionally, the rise of e-commerce is fueling demand for durable, temperature-controlled packaging that can withstand shipping. Technological solutions, such as QR codes and traceability tools, are enabling transparency in meat provenance, sourcing, and nutritional information, aligning with growing consumer demand for information and accountability.

Germany: Circular Economy Leadership and High-Performance Fresh Meat Packaging

Germany is a leader in Europe’s circular economy for fresh meat packaging, with strict regulations like the German Packaging Act (VerpackG) and the upcoming EU Packaging and Packaging Waste Regulation (PPWR) driving high recycling rates. The market is increasingly focused on developing recyclable materials such as glass, paper, and aluminum, as well as sustainable vacuum-sealed and modified atmosphere packaging (MAP) with smart functionalities. The country’s stringent food safety standards ensure the production of high-quality packaging for diverse meat products. Innovation in extending shelf life is a key trend, helping reduce food waste while supporting sustainable retail operations. German companies are also integrating smart features into packaging, such as freshness indicators, to enhance consumer experience and product safety.

China: Regulatory Reforms and Smart Packaging Innovations Fueling Market Growth

China’s fresh meat packaging market is shaped by strict regulations on food labeling and safety. New measures, effective from March 2027, will standardize the appearance and layout of packaging to ensure clarity and consumer protection. National standards, including GB 4806.15-2024 for adhesives in food packaging, are enforcing compliance and product safety. Rising domestic demand is driven by urbanization and the expansion of processed food and ready-to-eat sectors, creating a need for convenient, safe, and attractively packaged meat products. The market is also seeing rapid adoption of smart packaging technologies, including time-temperature indicators and gas sensors, which monitor freshness and quality throughout the supply chain, enhancing food safety and reducing losses.

India: Government Initiatives and E-Commerce Driving Sustainable Packaging Solutions

India’s fresh meat packaging market is being transformed by government support and market modernization initiatives. The “Make in India” program and the Production Linked Incentive (PLI) Scheme are driving capital investments in automated food and packaging lines, boosting the country’s food processing capabilities. Sustainability is a growing priority, with the FSSAI approving recycled PET as a food-contact material, promoting recyclable packaging solutions. The rapid growth of modern retail and e-commerce platforms is increasing demand for lightweight, durable packaging that ensures product safety during shipping and handling. Strict regulations for food-grade materials and hygiene standards are driving innovation in safe and sustainable fresh meat packaging solutions.

Brazil: Bioplastics and Regulatory Support Strengthening Fresh Meat Packaging

Brazil’s fresh meat packaging industry is a leader in bioplastics innovation, with green polyethylene from sugarcane ethanol reducing reliance on fossil fuels and promoting sustainability. Regulatory compliance is a critical driver, with Anvisa establishing clear frameworks for food contact materials and packaging registration, ensuring consumer safety. The circular economy is supported through initiatives like “eureciclo,” which provides Packaging Recycling Certificates to companies committed to waste compensation. These measures are encouraging the adoption of sustainable packaging practices while strengthening the market for innovative, eco-friendly fresh meat packaging solutions.

Japan: High-Barrier Packaging and Automation Addressing Safety and Labor Challenges

Japan’s fresh meat packaging market emphasizes high-barrier technology, with transparent films offering properties comparable to aluminum foil to extend product shelf life while improving recyclability. Hygiene and safety are critical, governed by the Japanese Sanitation Act, leading to the production of packaging that minimizes contamination risks. Labor shortages due to an aging workforce are driving demand for automated systems and advanced packaging machinery. The market is adapting by developing packaging that can be efficiently handled by automated systems, ensuring both operational efficiency and food safety.

Fresh Meat Packaging Market Report Scope

Fresh Meat Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$3.2 Billion

|

|

Market Size (2034)

|

$4.4 Billion

|

|

Market Growth Rate

|

3.6%

|

|

Segments

|

By Material Type (Plastics, Paper & Paperboard, Metal, Glass, Bioplastics), By Packaging Type (Flexible Packaging, Rigid Packaging, Modified Atmosphere Packaging, Vacuum Packaging, Vacuum Skin Packaging), By Application (Beef, Pork, Poultry, Seafood, Others), By End-Use (Retail, Foodservice, Industrial)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, Tyson Foods, Inc., Cargill, Inc., JBS S.A., Crown Holdings Inc., Pactiv Evergreen Inc., Silgan Holdings Inc., Berry Global Group, Inc., Sealed Air Corporation, Mondi Group, WestRock Company, Huhtamaki Oyj, Sonoco Products Company, Novamont S.p.A., Coveris Holdings S.A.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Fresh Meat Packaging Market Segmentation

By Material Type

- Plastics

- Paper & Paperboard

- Metal

- Glass

- Bioplastics

By Packaging Type

- Flexible Packaging

- Rigid Packaging

- Modified Atmosphere Packaging

- Vacuum Packaging

- Vacuum Skin Packaging

By Application

- Beef

- Pork

- Poultry

- Seafood

- Others

By End-Use

- Retail

- Foodservice

- Industrial

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Fresh Meat Packaging Market

- Amcor plc

- Tyson Foods, Inc.

- Cargill, Inc.

- JBS S.A.

- Crown Holdings Inc.

- Pactiv Evergreen Inc.

- Silgan Holdings Inc.

- Berry Global Group, Inc.

- Sealed Air Corporation

- Mondi Group

- WestRock Company

- Huhtamaki Oyj

- Sonoco Products Company

- Novamont S.p.A.

- Coveris Holdings S.A.

*List not Exhaustive

Research Coverage

This report by USDAnalytics investigates the global fresh meat packaging market, providing an in-depth analysis of recent breakthroughs, technological innovations, and strategic developments that are shaping the sector. The analysis reviews historical data from 2021 to 2024 and delivers comprehensive forecasts from 2025 to 2034, highlighting opportunities in vacuum skin packaging (VSP), Modified Atmosphere Packaging (MAP), and high-barrier mono-material solutions. The report emphasizes sustainability-driven developments, such as recyclable films, paperboard trays, and bioplastics, alongside automation trends that enhance hygiene, shelf-life extension, and operational efficiency. Key insights include the growing demand for e-commerce-ready packaging, smart time-temperature indicators, and high-performance molded fiber solutions. For industry professionals, this report is an essential resource for understanding market dynamics, regulatory impacts, competitive strategies, and emerging opportunities, equipping decision-makers to optimize packaging processes, reduce food waste, and meet evolving consumer expectations in the fresh meat sector.

Scope Highlights:

- Segmentation: By Material Type (Plastics, Paper & Paperboard, Metal, Glass, Bioplastics), By Packaging Type (Flexible Packaging, Rigid Packaging, Modified Atmosphere Packaging, Vacuum Packaging, Vacuum Skin Packaging), By Application (Beef, Pork, Poultry, Seafood, Others), By End-Use (Retail, Foodservice, Industrial)

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa

- Historical & Forecast Data: Historical insights from 2021–2024 and projections from 2025–2034

- Companies: Detailed analysis and profiles of 15+ key players, including Amcor, Tyson Foods, Cargill, JBS, Berry Global, Sealed Air, WestRock, and others

Methodology

The study adopts a robust research methodology combining primary and secondary sources to provide actionable insights for industry professionals. Primary research included interviews with packaging executives, R&D teams, and supply chain specialists to capture firsthand insights on technological adoption, material innovation, and regulatory compliance. Secondary research involved analysis of company reports, industry publications, press releases, and government regulations to evaluate market trends, competitive strategies, and sustainability initiatives. Data triangulation was applied to reconcile discrepancies and ensure accuracy, covering production volumes, packaging types, material adoption, and regional deployment. Forecasts from 2025 to 2034 were generated using CAGR-based models, market penetration metrics, and technological adoption rates. Competitive benchmarking and SWOT analyses were conducted to highlight strategic positioning, innovation capabilities, and growth opportunities across leading manufacturers. USDAnalytics’ approach ensures a holistic, data-driven understanding of the global fresh meat packaging market.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.