PVDC Food Packaging Market Size, Overview, and Growth Outlook (2025–2034)

PVDC Food Packaging Market Set to Surge to $1.46 Billion by 2034 Driven by Superior Barrier Properties

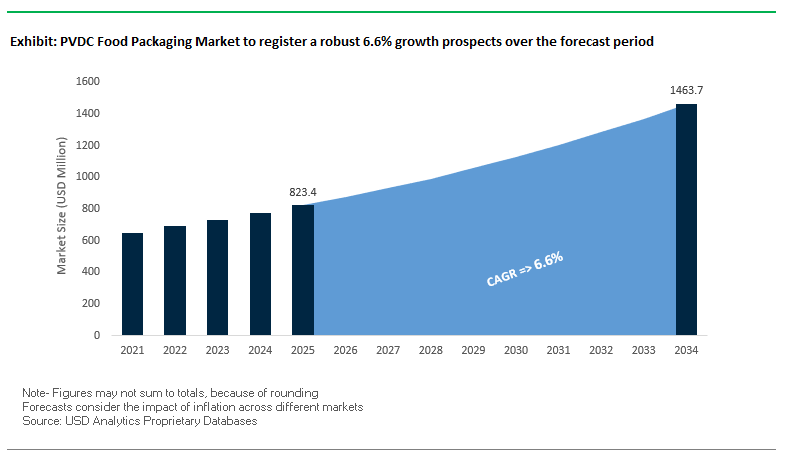

The global PVDC food packaging market is projected to grow from $823.4 million in 2025 to $1,463.6 million by 2034, registering a CAGR of 6.6%. PVDC (Polyvinylidene chloride) remains a preferred choice for high-barrier food packaging, offering unmatched protection against oxygen, moisture, and aroma loss, which is crucial for perishable and high-value food products. Its durability, low humidity dependency, and pinhole resistance make it a reliable solution for packaging across supply chains.

Key Insights for industry professionals and buyers:

- Superior Oxygen and Moisture Barrier: PVDC films significantly extend shelf life while maintaining product freshness.

- Aroma Retention Preserves Product Quality: Ideal for coffee, spices, cheese, and other aroma-sensitive foods.

- Pinhole Resistance Ensures Packaging Integrity: Durable enough for heavy or irregularly shaped items during transport.

- Consistent Performance Across Humidity Levels: Reliable barrier properties even under variable environmental conditions.

- Versatility Across Food and Pharmaceutical Packaging: From retort pouches to specialty labels, PVDC films enhance performance and safety.

Market Analysis: Recent PVDC Innovations and Strategic Investments Are Shaping High-Barrier Food Packaging

The PVDC food packaging industry has witnessed technological advancements and strategic expansions aimed at improving barrier performance and sustainability. In August 2025, a study in Nano Letters introduced an inhibitor-modified atomic layer deposition (ALD) strategy for ultrathin films, representing a breakthrough for high-performance PVDC coatings. Earlier in April 2025, Nfinite Nanotechnology partnered with Amcor to enhance oxygen barrier performance in recyclable and compostable packaging, reflecting the industry’s focus on next-generation barrier solutions.

Regulatory changes have also influenced PVDC adoption. In October 2024, new EU food packaging regulations mandated stricter environmental compliance, prompting innovations in PVDC formulations. Capacity expansions and material innovations are supporting market growth: in June 2023, Kureha GmbH expanded PVDC production to meet rising demand, while in October 2023, Solvay launched an ultra-high barrier PVDC coating for sustainable pharmaceutical blister films, demonstrating the material’s versatility beyond traditional food applications.

Acquisitions and product innovations have further strengthened market positions. In April 2022, Jindal Poly Films acquired SMI Coated Products to expand into labels and related segments. In August 2020, Cosmo Films introduced a transparent antifog PVDC film, enhancing product visibility for packaged foods. Historical strategic moves, such as Transcendia’s acquisition of Purestat Engineered Technologies in March 2019, illustrate long-term growth trends in PVDC barrier technologies and portfolio diversification.

PVDC Food Packaging Market: Emerging Trends and New Opportunities

Adoption of Strategic Phase-Out and Replacement in Consumer-Facing Packaging

A key trend in the PVDC food packaging market is the structured phase-out of PVDC from mainstream consumer-facing applications. Leading food and beverage companies are under mounting pressure from both regulators and consumers to prioritize recyclability and circular economy practices. Nestlé’s 2019 release of a “negative list” of materials including PVDC served as a major industry signal, discouraging new product launches using this material due to its incompatibility with conventional recycling systems. Similarly, regulatory action such as New Zealand’s Ministry for the Environment ban, effective October 2022, targeted pre-formed PVC and PVDC trays for meat, poultry, fish, and produce, further accelerating the pivot towards alternatives. This trend has made recyclable polymers such as PET and PP the preferred substitutes, aligning with corporate sustainability pledges and international regulatory frameworks like the EU PPWR. For food packaging producers, the shift away from PVDC requires investment in retooling and integration of new mono-material or recyclable multi-layer solutions.

Sustained Niche Application in High-Barrier Medical and Technical Packaging

Despite the decline in consumer packaging, PVDC continues to thrive in sectors where its barrier properties remain irreplaceable. Pharmaceutical blister packaging stands out as a critical use case, as highlighted by Asahi Kasei’s technical documentation, where PVDC laminates ensure protection against moisture and oxygen ingress, thereby safeguarding drug efficacy and extending shelf life. Beyond pharmaceuticals, PVDC maintains a presence in specialized technical packaging such as electronic component wraps, where moisture-induced corrosion could compromise safety and performance. Even in certain long-shelf-life food packaging niches, PVDC’s unmatched barrier performance keeps it in demand. These applications confirm that PVDC will not disappear entirely from the market but instead shift towards domains where performance is prioritized over recyclability.

Development of Drop-In, Recyclable High-Barrier Alternatives

One of the most promising opportunities lies in the development of recyclable, drop-in replacements that can mimic PVDC’s high-barrier performance without creating end-of-life waste challenges. Companies like Mondi are pioneering paper-based “FunctionalBarrier Papers,” engineered with advanced coatings to deliver moisture and oxygen resistance while remaining recyclable in standard paper streams. Similarly, polymer-based solutions are advancing, with ExxonMobil’s 95% polyethylene thermoformed barrier package combined with Kuraray’s EVOH achieving comparable performance to PVDC without compromising recyclability. These innovations are particularly attractive for food manufacturers seeking solutions compatible with existing filling and sealing equipment, minimizing switching costs while enhancing sustainability credentials.

Advanced Chemical Recycling Pathways for PVDC Waste

While most innovation focuses on substitution, another emerging opportunity is the advancement of recycling technologies capable of handling PVDC waste directly. In early 2025, Syensqo achieved a breakthrough by proving that its Ixan® PVDC structures could be mechanically recycled alongside polyethylene through grinding, washing, and extrusion. This was a landmark development, countering the historical challenge of chlorine release during conventional disposal. Complementing this, academic research has demonstrated electrochemical deconstruction as a method for breaking down PVDC into valuable chlorinated compounds and stable unsaturated materials, mitigating harmful emissions associated with incineration. Together, these breakthroughs point towards a dual strategy: reducing reliance on PVDC in mainstream food packaging while simultaneously enabling a more sustainable end-of-life pathway for existing PVDC-based products.

Competitive Landscape: Leading PVDC Food Packaging Companies Are Leveraging Technology and Sustainability to Gain Global Market Share

The PVDC food packaging market is dominated by companies focusing on high-performance barrier technologies, global expansions, and sustainability initiatives. These leaders are leveraging proprietary technologies, strategic acquisitions, and partnerships to provide differentiated solutions for the food and pharmaceutical sectors.

Kureha Corporation: Driving Global Expansion with High-Performance PVDC Films

Kureha, a Japanese specialty chemicals leader, offers PVDC-based food packaging films under its Krehalon Film brand. Its strategy, “Grow Globally,” includes a new production facility in Vietnam and increased PVDC exports to China. Kureha emphasizes originality and quality, using proprietary technologies to develop innovative films that meet the growing global demand for high-barrier food packaging.

Solvay S.A.: Pioneering Sustainable PVDC Coatings with High-Barrier Performance

Solvay’s Diofan® PVDC waterborne dispersions provide high barriers against water, oxygen, and aroma, ensuring product integrity. In September 2021, Solvay demonstrated PVDC recycling from post-industrial waste, marking a key step toward a circular packaging economy. The company actively collaborates to establish infrastructure for segregating PVDC-containing packaging, emphasizing sustainability and high-performance solutions.

Asahi Kasei Corporation: Committing to Innovation and Consistent High-Barrier PVDC Solutions

Asahi Kasei produces PVDC Latex and Resin for food and pharmaceutical coatings. Manufactured at its Nobeoka facility, the company maintains rigorous quality control and technological innovation. Its products are widely used in meat, dairy, confectionery, and retort pouch applications, reflecting reliability and superior barrier properties. The company’s focus on sustainable and protective solutions underlines its commitment to life and living.

Dow Chemical Company: Enabling PVDC Ecosystem with Advanced Polymer Modifiers

Dow’s RETAIN™ polymer modifiers support PVDC barrier film production, even though Dow is not a direct PVDC resin producer. Through collaborations like the July 2021 partnership with Vishakha Group in India, Dow helped develop recyclable barrier films for wheat packaging, highlighting its role in integrating new materials into sustainable packaging solutions. Its Pack Studios platform accelerates packaging innovation and adoption.

Jindal Poly Films Ltd.: Strengthening PVDC Offerings through Strategic Acquisitions and Large-Scale Production

Jindal Poly Films, a leading Indian manufacturer, provides PVDC-coated films across flexible packaging, labels, and specialty products. Its April 2022 acquisition of SMI Coated Products diversified its portfolio. With one of the world’s largest BOPP and BOPET film production facilities, Jindal Poly Films offers high-barrier PVDC films suitable for a range of food packaging applications, reinforcing its strong global market position.

PVDC Food Packaging Market Share Insights, 2025-2034

PVDC-Coated Films Dominate Market Share by Film Type in the PVDC Food Packaging Industry

PVDC-coated films command a decisive 70% share of the PVDC packaging industry, owing to their superior barrier efficiency combined with cost-effectiveness. By applying an ultra-thin PVDC coating onto substrates like PET or BOPP, these films deliver exceptional oxygen and moisture resistance while minimizing material usage, making them indispensable for flexible food packaging applications such as snacks, coffee, and processed meats. Pharmaceutical blister packaging contributes about 20% of demand, acting as a compliance-driven stronghold where PVDC remains unmatched in ensuring stability of moisture-sensitive drugs. PVDC monolayer films, with a declining 10% share, are being phased out due to higher material consumption, environmental scrutiny, and manufacturing complexity. This distribution underscores how coated PVDC films remain the performance-to-cost benchmark, while pharmaceutical packaging secures the material’s role in irreplaceable, high-value applications.

Food & Beverages Secure the Largest Market Share by End-Use in the PVDC Packaging Industry

The food and beverage sector accounts for 75% of PVDC packaging demand, reflecting its reliance on superior barrier properties to extend shelf life and preserve product integrity. PVDC films are uniquely positioned to protect dry foods from aroma loss and oily or high-fat products, such as cheese and processed meats, where competing materials like EVOH underperform in humid conditions. Pharmaceuticals represent 20% of end-use share, where PVDC remains a gold-standard packaging material for blister packs, ensuring stability of moisture-sensitive tablets and capsules across diverse climates. Personal care and cosmetics, at 5%, leverage PVDC to safeguard fragrance integrity and prevent evaporation of volatile compounds in premium creams and lotions, though alternatives are gaining traction. This segmentation confirms that food and pharma provide PVDC its defensible base, while cosmetics remain a smaller but brand-sensitive growth niche.

European Union: Regulatory Pressure Pushing PVDC Toward Sustainable Alternatives

The European Union is one of the most highly regulated markets for PVDC food packaging, with oversight led by the European Food Safety Authority (EFSA) under Regulation (EC) No 1935/2004, which ensures that food-contact materials do not release harmful substances or alter food composition. The Packaging and Packaging Waste Regulation (PPWR), which came into force in February 2025, is reshaping packaging strategies by setting strict targets for recyclability and reusability, directly impacting the role of PVDC films. Since PVDC has traditionally been used in multilayer structures that are difficult to recycle, the industry faces mounting pressure to redesign toward mono-material structures that can integrate into recycling streams.

The Recycled Plastic Regulation (EU) 2022/1616 adds another layer of compliance by governing recycled plastic use in food-contact applications, further pushing companies to innovate. For example, Kureha Corporation withdrew from its European heat-shrink multilayer film business, shifting its focus toward PVDC films with in-house raw materials to increase efficiency while complying with sustainability mandates. These transitions illustrate how EU policy is accelerating the market shift toward eco-friendly, recyclable PVDC solutions.

United States: FDA Oversight and High-Barrier Packaging Driving PVDC Demand

In the United States, the Food and Drug Administration (FDA) is the key regulator, requiring all food packaging materials, including PVDC, to undergo safety approval petitions before use. The Food Safety and Inspection Service (FSIS) under the USDA adds another compliance layer, requiring meat and poultry processors to keep supplier guarantees that materials meet FFDCA standards. These regulatory mechanisms ensure PVDC continues to play a role in high-barrier packaging for sensitive food categories.

The U.S. market is seeing rising investment in high-barrier packaging solutions designed to extend shelf life for processed foods, cheese, and meat. PVDC’s exceptional moisture, gas, and aroma barrier properties make it a material of choice for these applications. Additionally, companies such as Tekni-Plex, Inc. have expanded capacity for five-layer blown films, meeting demand not only in food but also in pharmaceutical and healthcare packaging, where similar multilayer barrier film technology is applied. These expansions highlight how PVDC continues to secure strong relevance in both food safety and healthcare compliance.

China: Domestic Manufacturing Strength and Thinner Multilayer PVDC Structures

China is a major global hub for PVDC resin and film production, supported by a localized supply chain that significantly reduces costs and increases competitiveness. Regulatory oversight from the National Health Commission (NHC) and the State Administration for Market Regulation (SAMR) reinforces food safety, ensuring PVDC’s strong role in packaging for fresh meat, seafood, and processed foods.

A growing trend in China is the development of thinner multilayer PVDC structures that incorporate recycled content without compromising barrier performance. This approach addresses environmental concerns while maintaining PVDC’s oxygen and moisture barrier strengths. Local manufacturers are also upgrading quality to compete with global brands, supporting the country’s rising consumption of packaged foods. Strategic investments include Kureha Corporation’s 2022 joint venture in China, which boosts local PVDC production capacity and leverages the country’s large-scale demand for advanced food packaging.

India: Regulatory Compliance and Bioplastic Alternatives Shaping PVDC Packaging

India’s PVDC food packaging market is underpinned by regulatory guidance from the Food Safety and Standards Authority of India (FSSAI). The Food Safety and Standards (Packaging) Regulations, 2018 require that multilayer packaging materials do not compromise food safety or quality, supporting the use of BOPP substrates with PVDC coatings in applications like snacks, dairy, and ready-to-eat meals.

At the same time, India is aligning with sustainability commitments through the India Plastics Pact, a collaboration between the Confederation of Indian Industry (CII) and WWF India, which targets 100% reusable or recyclable plastic packaging by 2030. This is encouraging innovation in PVDC-coated films that are thinner, recyclable, and compatible with EPR frameworks. Rising urbanization and consumer demand for processed foods, dairy products, and convenience meals are major growth drivers, ensuring PVDC’s continued relevance while the industry simultaneously explores bioplastics derived from agricultural and dairy waste as supplementary solutions.

Japan: Strong Food Safety Regulations and Advanced PVDC Film Applications

Japan is a mature and innovation-driven PVDC market, regulated by the Ministry of Health, Labour, and Welfare (MHLW), which enforces strict safety standards for food-contact materials. Companies such as Kureha Corporation and Asahi Kasei dominate the market, with Kureha’s “Krewrap” PVDC film being a household name and a benchmark for high-quality food packaging.

Japanese manufacturers are pioneering in barrier film innovation, producing PVDC-based multilayer films that excel against moisture, oxygen, and aroma loss. Heat-shrink multilayer PVDC films are especially important in meat and sausage packaging, where extended shelf life and product integrity are critical. With a culture of precision and food quality assurance, Japan remains a global leader in premium PVDC applications, setting high standards in both domestic and export packaging markets.

PVDC Food Packaging Market Report Scope

PVDC Food Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$823.4 Million

|

|

Market Size (2034)

|

$1463.6 Million

|

|

Market Growth Rate

|

6.6%

|

|

Segments

|

By Film Type (PVDC Coated Films, PVDC Monolayer Films), By Application (Food Packaging, Pharmaceutical Blister Packaging), By End-Use Industry (Food & Beverages, Pharmaceuticals, Personal Care & Cosmetics)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Asahi Kasei Corporation, Kureha Corporation, Dow Inc., Solvay S.A., Tekni-Plex, Inc., Bilcare Ltd., Mondi Group, Cosmo Films Ltd., SKC Co., Ltd., Klöckner Pentaplast GmbH & Co. KG, Innovia Films Ltd., Amcor plc, Perlen Packaging, Krehalon Food Packaging, Jindal Poly Films Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

PVDC Food Packaging Market Segmentation

By Film Type

- PVDC Coated Films

- PVDC Monolayer Films

By Application

- Food Packaging

- Pharmaceutical Blister Packaging

By End-Use Industry

- Food & Beverages

- Pharmaceuticals

- Personal Care & Cosmetics

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in PVDC Food Packaging Market

- Asahi Kasei Corporation

- Kureha Corporation

- Dow Inc.

- Solvay S.A.

- Tekni-Plex, Inc.

- Bilcare Ltd.

- Mondi Group

- Cosmo Films Ltd.

- SKC Co., Ltd.

- Klöckner Pentaplast GmbH & Co. KG

- Innovia Films Ltd.

- Amcor plc

- Perlen Packaging

- Krehalon Food Packaging

- Jindal Poly Films Ltd.

* List Not Exhaustive

Methodology

The research methodology for the PVDC Food Packaging Market combines robust primary and secondary approaches to ensure comprehensive market accuracy and actionable insights. Primary research involved interviews with industry executives, packaging engineers, sustainability specialists, and supply chain stakeholders across key regions including North America, Europe, and Asia-Pacific. Secondary research included detailed analysis of company reports, regulatory databases, patents, sustainability disclosures, scientific journals, and trade publications, focusing on PVDC-coated films, monolayer films, and high-barrier packaging applications. Advanced data triangulation validated market sizing, CAGR projections, and regional demand patterns, integrating factors such as regulatory changes, raw material availability, and technological innovations in barrier performance. Forecasting utilized both top-down and bottom-up approaches, while regional insights were contextualized with local food safety standards, sustainability mandates, and consumer trends. This multi-layered methodology by USDAnalytics ensures that the report delivers precise, fact-based intelligence aligned with real-world industry dynamics and strategic decision-making needs.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.