Sanitary Food and Beverage Packaging Market Size, Overview, and Growth Outlook (2025–2034)

Sanitary Food and Beverage Packaging Market to Reach $51.1 Billion by 2034 Driven by Hygiene and Regulatory Compliance

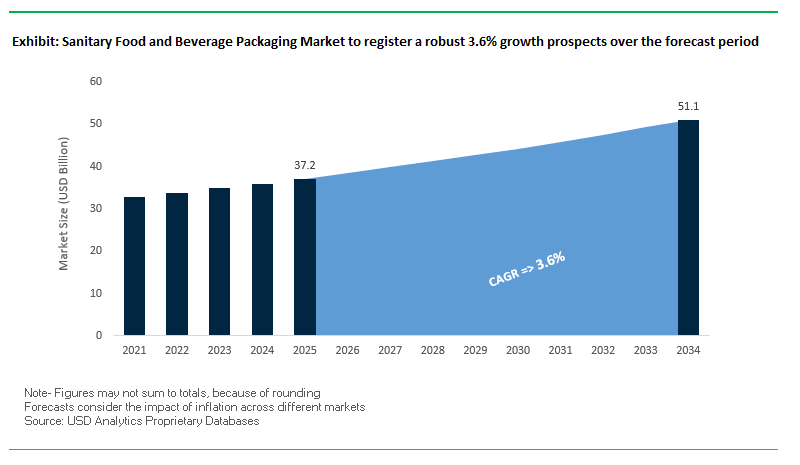

The global sanitary food and beverage packaging market is projected to grow from $37.2 billion in 2025 to $51.1 billion by 2034, at a CAGR of 3.6%. This growth is fueled by rising consumer awareness of food safety, increasing regulatory compliance, innovation in active packaging, and the shift from unpacked to packed foods, particularly in emerging economies. Industry professionals can leverage these insights to optimize product safety, ensure regulatory alignment, and adopt sustainable packaging technologies.

Key Insights for packaging decision-makers:

- Consumer-Driven Hygiene Demand: A surge in tamper-proof packaging, with a 20% increase in consumer demand over the last two years, driven by heightened awareness of food safety.

- Regulatory Alignment: Over 75% of new product launches in Europe and North America comply with FDA and FSSAI certifications.

- Active Packaging Innovation: New films and coatings with antimicrobial agents and oxygen scavengers inhibit bacterial growth by over 98%, extending shelf life of perishable goods.

- Shift from Unpacked to Packed: Emerging markets show rapid adoption of single-serve hygienically sealed foods, responding to recent food safety concerns.

- Opportunities in Sustainable Packaging: Increasing focus on eco-friendly materials and circular economy initiatives.

- Market Growth Across Segments: Expansion in ready-to-eat meals, beverages, and snacks, driven by health-conscious consumers.

The sanitary packaging market represents a strategic convergence of food safety, hygiene, and regulatory compliance, offering a roadmap for innovation and market expansion.

Market Analysis: Industry Consolidation and Sustainability Are Transforming Sanitary Food Packaging Solutions

The sanitary food and beverage packaging sector is witnessing strategic consolidation and investment in sustainable solutions. In August 2025, Constantia Flexibles acquired Aluflexpack, strengthening its presence in high-value food and pharmaceutical packaging. The same month, Amcor and Flügger introduced a 50% recycled paint container, highlighting cross-industry circularity initiatives. In July 2025, Amcor completed its acquisition of Berry Global, creating a diversified leader in both flexible and rigid sanitary packaging.

Sustainability and innovation remain central to market evolution. In May 2025, Mondi started up a €400 million paper machine at its Štětí plant, advancing production of food-contact compliant, sustainable paper packaging. Similarly, April 2025 saw Sonoco divest its Thermoformed and Flexibles Packaging business, enabling a strategic focus on sanitary rigid containers. These moves underscore the industry’s emphasis on hygiene, regulatory compliance, and eco-conscious packaging solutions.

Collaborations and mergers are also reshaping the market. In February 2025, Amcor Rigid Packaging partnered with Avantium NV to explore plant-based polyethylene furanoate for sustainable rigid packaging. In January 2025, the merger between IPL and Schoeller Allibert created a $1.4 billion reusable packaging leader, emphasizing reusable plastic containers designed for hygiene and safety.

Sanitary Food and Beverage Packaging Market: Key Trends and Opportunities Driving Transformation

Regulatory Phase-Out of Per- and Polyfluoroalkyl Substances (PFAS)

The most pressing trend impacting sanitary food and beverage packaging is the accelerated global phase-out of PFAS in food-contact materials. In Europe, the EU’s Packaging and Packaging Waste Regulation (PPWR) mandates a ban on PFAS from August 12, 2026, following Denmark’s pioneering prohibition in 2020. These measures are pushing converters and brand owners to re-engineer coatings for rigid and flexible food packaging formats. In the United States, regulation is being driven at the state level. Washington State’s February 2023 ban on PFAS in pizza boxes, wraps, and food boats set a precedent that other states are rapidly following. This patchwork of U.S. regulations creates operational challenges for multinational packaging suppliers, who must ensure compliance across multiple jurisdictions simultaneously. Beyond legislation, corporate commitments are amplifying the trend. Global restaurant and grocery chains such as Chipotle, Wendy’s, and McDonald’s have pledged to eliminate PFAS from their food packaging portfolios, creating a powerful market signal for upstream innovation. This convergence of regulatory mandates and brand-level initiatives is accelerating the industry’s pivot to PFAS-free alternatives, placing material science innovation at the center of sanitary packaging development.

Advanced Aseptic Packaging Adoption Beyond Dairy and Juice

Another defining trend is the expansion of aseptic packaging technologies beyond traditional categories such as dairy and juice. Asepto’s introduction of ghee packaging demonstrates the technology’s ability to accommodate high-fat, high-viscosity products while maintaining safety and shelf life. This diversification is opening opportunities for new applications across condiments, ready-to-drink meals, and functional beverages. In addition, aseptic packaging is making inroads into the medical and pharmaceutical sectors, where sterile cartons are increasingly used for oral rehydration solutions (ORS) and specialty medical liquids. The technology ensures efficacy without preservatives, reinforcing consumer and patient trust. From a sustainability perspective, aseptic formats are a major lever for food waste reduction, extending product shelf life while eliminating the need for cold chain logistics. By lowering energy consumption and transport costs, aseptic packaging aligns with corporate carbon reduction strategies and creates a measurable ESG impact, making it a critical growth driver in the sanitary packaging market.

Development and Commercialization of Bio-Based Barrier Coatings

The regulatory ban on PFAS creates a significant opening for bio-based barrier coatings as the next generation of sanitary food packaging solutions. Materials such as cellulose nanocrystals, chitosan, and starch derivatives are showing strong promise in delivering oxygen and grease resistance comparable to fluorinated coatings. A study in the International Journal of Engineering Research & Technology demonstrated how these materials can protect packaged food without hindering recyclability or compostability. Industry players such as H.B. Fuller are emphasizing the development of a suite of application-specific coatings rather than a single solution, reflecting the diverse performance needs across bakery, QSR (quick-service restaurant), and frozen food categories. The opportunity here is twofold: companies that commercialize bio-based coatings not only meet compliance needs but also unlock a new value chain in sustainable material science, positioning themselves as technology partners to converters and brand owners seeking PFAS-free innovation at scale.

Integration of Smart and Connected Packaging for Supply Chain Visibility

The sanitary packaging market is also witnessing a strong opportunity in the integration of smart and connected technologies to improve traceability and consumer engagement. With regulatory and consumer pressure mounting around safety and transparency, QR codes, NFC tags, and digital product passports are becoming standard features. These technologies allow end-to-end tracking of packaging, providing brands with real-time visibility into logistics conditions, storage compliance, and supply chain efficiency. For perishable or temperature-sensitive products, smart indicators such as time-temperature indicators (TTIs) add value by delivering real-time freshness monitoring—flagging when food has been exposed to unsafe temperatures. Beyond safety, connected packaging creates new consumer touchpoints. By scanning a tag, consumers can access ingredient sourcing details, sustainability claims, or promotional content, thereby strengthening brand trust and loyalty. As regulatory frameworks like the EU’s Digital Product Passport expand, the integration of smart features will become a compliance necessity as well as a competitive differentiator for sanitary food and beverage packaging suppliers.

Competitive Landscape: Leading Companies Are Driving Innovation, Sustainability, and Hygiene in Sanitary Packaging

The sanitary food and beverage packaging market is highly competitive, with key players leveraging innovation, sustainability, and strategic mergers to provide tamper-proof, high-barrier, and recyclable solutions. These companies are shaping the industry through advanced materials, aseptic technology, and global supply chain integration.

Amcor plc: Global Leader in High-Performance Sanitary Packaging

Amcor provides a wide portfolio of flexible and rigid packaging, including high-barrier films, PET bottles, and retort pouches. The mega-merger with Berry Global expanded its global footprint and product offerings. Amcor’s AmFiber Performance Paper heat-seal sachets and recycle-ready stickpacks demonstrate its commitment to sustainability and circular economy principles. Its packaging is engineered for high-speed machinery, ensuring easy-open, contamination-resistant seals for food and beverage safety.

Tetra Pak: Pioneering Aseptic and Sustainable Packaging Solutions for Extended Shelf Life

Tetra Pak is renowned for its aseptic packaging technology for milk, juices, and other beverages. The November 2022 launch of India’s first Tetra Stelo aseptic package illustrates its capability to innovate for new markets. Tetra Pak focuses on safe, sustainable, and circular packaging, ensuring food safety without refrigeration, and leveraging renewable and recycled materials.

Sealed Air Corporation (SEE): Leading with Tamper-Evident Solutions and Circular Packaging Initiatives

SEE offers tamper-evident sanitary packaging through brands like CRYOVAC® and LIQUIBOX®. Its Net Positive Circular Ecosystem strategy targets 100% recyclable or reusable materials by 2025. The January 2025 acquisition of Pitreavie Group enhanced SEE’s expertise in recyclable corrugated and foam packaging, strengthening its portfolio of hygienic solutions for meat, poultry, and perishable foods.

Sonoco Products Company: Specializing in Hygienic and Recyclable Rigid Packaging

Sonoco provides sanitary rigid and flexible packaging for snacks, coffee, and powdered beverages. The April 2025 divestment of Thermoformed and Flexibles Packaging allowed focus on sanitary food packaging. Its Sonoco Paper Can features an all-paper bottom, combining recyclability, hygiene, and durability, supported by globally integrated paper mill operations.

Huhtamaki Oyj: Advancing Mono-Material Solutions for Sustainable and Hygienic Packaging

Huhtamaki delivers flexible packaging for food and personal care, with its blueloop™ platform offering mono-material solutions in paper, PE, and PP Retort. The company targets 100% recyclable, compostable, or reusable packaging by 2030, combining sustainability with enhanced hygiene. Its products cater to beverages and other perishable foods, offering light-weighting and high-quality printing for market differentiation.

Sanitary Food and Beverage Packaging Market Share Insights, 2025-2034

Rigid Packaging Holds the Largest Market Share by Packaging Type in the Sanitary Food and Beverage Packaging Industry

Rigid packaging accounts for 55% of the sanitary food and beverage packaging market, reflecting its long-standing dominance in food safety, product protection, and consumer perception of quality. Glass jars, metal cans, PET bottles, trays, and clamshells provide the highest levels of oxygen, light, and moisture barrier properties, making them indispensable for canned goods, dairy, juices, and fresh produce. Their strength ensures durability through long supply chains, while recyclability improvements in rPET and recycled glass strengthen their sustainability profile. Although flexible packaging is growing rapidly due to its light weight and cost efficiency, rigid formats maintain their lead in applications where extended shelf life, physical protection, and tamper resistance are non-negotiable.

Food Applications Drive the Largest Market Share by Application in the Sanitary Food and Beverage Packaging Industry

The food sector dominates the sanitary food and beverage packaging industry with a commanding 70% market share, making it the cornerstone of demand. Fresh produce relies on breathable films, meat and poultry require high-barrier modified atmosphere packaging (MAP), and dry goods are secured in laminates and flexible pouches. This breadth highlights the centrality of packaging in food preservation and waste reduction. Growth is further accelerated by active and intelligent packaging technologies such as oxygen scavengers, ethylene absorbers, and time–temperature indicators, which directly address spoilage challenges. While beverages such as carbonated drinks, dairy, and juices rely on PET bottles, aseptic cartons, and HDPE containers with advanced barrier properties, food packaging remains the dominant and most innovation-intensive application segment.

European Union: PPWR, ESPR, and PFAS Restrictions Accelerating Sustainable Sanitary Packaging

The European Union sanitary food and beverage packaging market is undergoing a structural shift under the Packaging and Packaging Waste Regulation (PPWR), which came into force in February 2025. The regulation sets ambitious reuse and recycled content targets, mandating that all plastic food contact packaging contain minimum levels of post-consumer recycled content by 2030. This is driving large-scale investments in food-grade recycling technologies and advanced materials that meet strict hygiene and safety requirements. The PFAS ban effective August 2026 is another significant catalyst, pushing companies to adopt alternative barrier coatings for sanitary applications.

The Ecodesign for Sustainable Products Regulation (ESPR), effective mid-2024, is introducing a Digital Product Passport (DPP) that will require complete transparency on material origin, recyclability, and compliance. This is reshaping sourcing strategies and product labeling. On the industrial front, Stora Enso’s $1 billion investment in a new board line in Finland—adding 750,000 tons of annual capacity—is expected to strengthen supply for paperboard-based sanitary packaging, particularly for dairy and beverage cartons. Together, these measures are making the EU a hub for sustainable, regulatory-driven packaging innovation.

United States: FSMA, EPR Laws, and Sustainable Brand Initiatives Driving Sanitary Packaging

The United States sanitary packaging market is strongly influenced by the Food Safety Modernization Act (FSMA), which prioritizes preventive safety measures. The Sanitary Transportation of Human and Animal Food rule directly impacts packaging design by requiring formats that maintain product integrity across distribution chains. Additionally, seven U.S. states have passed Extended Producer Responsibility (EPR) laws, with Maryland mandating 90% cost recovery by 2030, compelling food and beverage brands to redesign sanitary packaging with recyclability and reusability in mind.

On the corporate front, companies are leading with sustainability commitments. Chlorophyll Water transitioned entirely to 100% rPET bottles, becoming the first U.S. bottled water brand with a Clean Label Project Certification. Similarly, Berry Global launched customizable PCR-based bottles, while Fresh Del Monte Produce, in partnership with Arena Packaging, adopted Reusable Plastic Containers (RPCs) for bananas, significantly reducing food waste and emissions. With upcoming requirements such as tethered caps for rigid plastic bottles, the U.S. market is advancing toward integrated sanitary, sustainable, and regulatory-compliant solutions.

China: Regulatory Mandates and Premiumization Fueling Sanitary Packaging Demand

The China sanitary food and beverage packaging market is being reshaped by the country’s 14th Five-Year Plan, which emphasizes plastic pollution control and green growth strategies. From June 1, 2025, regulations mandate eco-friendly, reduced, and reusable packaging for express delivery, extending indirectly to food and beverage sectors reliant on single-use packaging. The trend is complemented by Coca-Cola’s use of 100% rPET bottles in Hong Kong, sourced from domestic facilities, showcasing the transition to circularity in sanitary beverage packaging.

A major driver in China is the growing demand for premium food and beverage products, which requires high-quality, sanitary packaging with enhanced safety barriers. The government is also promoting the remanufacturing industry with tax incentives for companies using green technologies, encouraging large beverage and food brands to adopt recyclable and reusable sanitary packaging. Combined, these factors position China as one of the fastest-growing markets for sustainable, food-grade sanitary packaging.

India: EPR Regulations and FSSAI Guidelines Strengthening Food-Grade Packaging Compliance

The India sanitary packaging market is heavily influenced by the Plastic Waste Management (Amendment) Rules, 2024, which reinforce Extended Producer Responsibility (EPR) for producers and brand owners. A significant milestone was reached in May 2025, when the Food Safety and Standards Authority of India (FSSAI) issued guidelines for food-grade rPET packaging, mandating strict compliance criteria and introducing a new logo for rPET-certified materials. These steps mark a pivotal move toward safer, circular packaging solutions.

From July 1, 2025, all plastic sanitary packaging must carry barcodes or QR codes for traceability, ensuring accountability across the supply chain. India’s PM Gati Shakti infrastructure plan is also boosting cold-chain investments, driving demand for rigid PET preforms and high-barrier sanitary containers for dairy and juice. With migration testing requirements for packaging materials, India is steering toward a market where compliance, safety, and sustainability converge, creating a regulatory-driven growth opportunity for domestic and multinational brands.

Japan: Circular Economy Mandates and Paper-Based Sanitary Packaging Innovation

The Japan sanitary food and beverage packaging market is defined by strict Plastic Resource Circulation policies, requiring all plastic packaging to be recyclable or reusable by 2025. The Plastic Resource Circulation Promotion Law, effective in the same year, enforces the reduction or redesign of 12 single-use plastic categories, directly impacting sanitary beverage bottles, food trays, and pouches.

Innovation is central to Japan’s sanitary packaging advancements. Nippon Paper Industries’ SHIELDPLUS, a paper with oxygen- and odor-barrier properties, is a groundbreaking solution for sanitary food sachets and cartons. Additionally, Coca-Cola Bottlers Japan Inc. (CCBJI) has invested in a new aseptic production line at its Tokai Plant in Aichi Prefecture, capable of producing 600 PET bottles per minute, enhancing both sanitation and efficiency. Japan is positioning itself as a global leader in paper-based and bio-polymer sanitary packaging technologies, balancing hygiene with sustainability.

Brazil: Reverse Logistics and MAP Packaging Expanding Sanitary Solutions

The Brazil sanitary packaging market is structured around the National Solid Waste Policy (PNRS), which emphasizes recycling, reduction, and responsible waste management. The government has reinforced accountability through an expanded reverse logistics system, making producers responsible for the post-consumer recycling of sanitary packaging. A critical policy change came with Law No. 15,088 in January 2025, banning the import of foreign plastic, paper, and metal waste, thereby strengthening domestic recycling initiatives.

The market is also adopting Modified Atmosphere Packaging (MAP) films and vacuum technologies to extend the shelf life of food while maintaining sanitary integrity. This is particularly relevant for Brazil’s meat, dairy, and fresh produce sectors, which require packaging formats that minimize contamination while enhancing freshness. With regulatory enforcement and rising demand for hygienic packaging formats, Brazil is moving toward a circular, innovation-driven sanitary food and beverage packaging ecosystem.

Sanitary Food and Beverage Packaging Market Report Scope

Sanitary Food and Beverage Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$37.2 Billion

|

|

Market Size (2034)

|

$51.1 Billion

|

|

Market Growth Rate

|

3.6%

|

|

Segments

|

By Material (Plastics, Glass, Metal, Paper & Paperboard), By Packaging Type (Rigid Packaging, Flexible Packaging), By Application (Food, Beverages)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, Berry Global, Inc., Silgan Holdings Inc., Sonoco Products Company, Huhtamaki Oyj, Ball Corporation, DS Smith Plc, Mondi Group, Crown Holdings, Inc., WestRock Company, Pactiv Evergreen Inc., Orbis Corporation, Sealed Air Corporation, Tetra Pak, Greiner Packaging International GmbH

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Sanitary Food and Beverage Packaging Market Segmentation

By Material

- Plastics

- Glass

- Metal

- Paper & Paperboard

By Packaging Type

- Rigid Packaging

- Flexible Packaging

By Application

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Sanitary Food and Beverage Packaging Market

- Amcor plc

- Berry Global, Inc.

- Silgan Holdings Inc.

- Sonoco Products Company

- Huhtamaki Oyj

- Ball Corporation

- DS Smith Plc

- Mondi Group

- Crown Holdings, Inc.

- WestRock Company

- Pactiv Evergreen Inc.

- Orbis Corporation

- Sealed Air Corporation

- Tetra Pak

- Greiner Packaging International GmbH

* List Not Exhaustive

Methodology

USDAnalytics employs a comprehensive research methodology to deliver accurate, actionable insights into the global sanitary food and beverage packaging market. Our approach integrates detailed secondary research from regulatory filings, corporate reports, sustainability disclosures, and industry journals with primary consultations involving packaging manufacturers, FMCG brand owners, recyclers, and supply chain experts across food, beverage, and emerging sanitary segments. Market sizing and forecasts consider materials (plastics, glass, metal, paper & paperboard), packaging types (rigid and flexible), and regional regulations such as the EU’s PPWR and ESPR, U.S. FSMA and EPR laws, India’s FSSAI and plastic waste regulations, China’s 14th Five-Year Plan, Japan’s Plastic Resource Circulation policies, and Brazil’s PNRS framework. The methodology also examines innovations in active packaging, bio-based barrier coatings, aseptic systems, and smart/connected technologies like QR codes, NFC, and digital product passports. Additionally, USDAnalytics analyzes competitive strategies, mergers, acquisitions, and sustainability investments, ensuring professionals gain comprehensive insights into market drivers, regulatory compliance, technological advancements, and opportunities for growth in the evolving sanitary packaging industry.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.