Refrigeration Insulation Materials Market Size, Overview, and Growth Outlook (2025–2034)

Refrigeration Insulation Materials Market Set for Sustained Growth with Energy Efficiency at Its Core

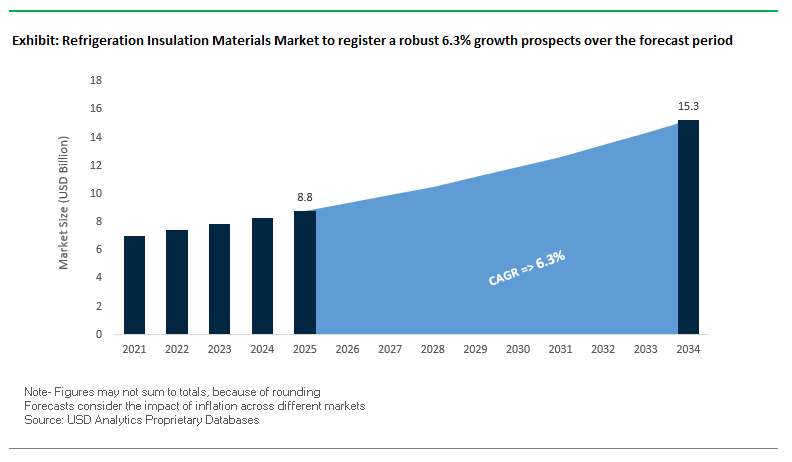

The global refrigeration insulation materials market is projected to grow from $8.8 billion in 2025 to $15.3 billion by 2034, at a CAGR of 6.3%. This growth is primarily driven by the food and beverage industry, which relies heavily on precise temperature control to ensure food safety, quality, and shelf life. Innovations in thermal insulation technologies and a shift toward low GWP materials are reshaping the market, enabling manufacturers to meet both environmental regulations and operational efficiency goals.

Key Insights for industry professionals and buyers:

- Food and Beverage Demand: Temperature-controlled storage and transport are key drivers for refrigeration insulation material adoption.

- PU/PIR Foams Dominate: Polyurethane and polyisocyanurate foams are preferred due to high thermal efficiency, fire resistance, and durability.

- Energy Efficiency Focus: Materials like aerogels and vacuum insulated panels (VIPs) are enhancing thermal performance, reducing energy consumption and operating costs.

- Shift to Sustainable Materials: Low GWP blowing agents and eco-friendly formulations are increasingly adopted to meet regulatory and sustainability requirements.

- Cost-Effective Performance: Advanced insulation materials contribute to operational savings by minimizing energy losses.

- Innovation Opportunities: The adoption of recycled content and high-performance panels supports both sustainability and performance goals.

Market Analysis: Strategic Expansions and Regulatory Shifts Are Driving Demand for Advanced Insulation Materials

The refrigeration insulation materials market is experiencing significant growth due to increased demand for energy-efficient systems and sustainable solutions. In August 2025, Magnavale expanded its frozen storage facility in Lincolnshire, UK, increasing the requirement for high-performance insulation materials to maintain precise cold chain conditions. Around the same time, Arkema commissioned a new production unit for Forane 1233zd at its Kentucky facility, reinforcing its position in the low GWP blowing agent market.

Industry focus on sustainability is evident through material innovation and recycled content. In March 2025, BASF piloted an insulation board with 10% recycled EPS, demonstrating circular economy integration. Earlier, in February 2024, BASF introduced its HFO-blown PIR system with significantly lower GWP, now applied in continuous sandwich panels for the cold chain sector.

Policy developments and global standards are also shaping market dynamics. In December 2024, the US Department of Energy introduced stricter efficiency standards for residential refrigerators and freezers, prompting manufacturers to adopt advanced insulation solutions. Other notable initiatives include the GIZ tender in July 2025 to implement a Qualification, Certification, and Registration (QCR) system in Brazil’s refrigeration sector, signaling increased emphasis on industry qualifications and compliance with insulation standards.

Refrigeration Insulation Materials Market: Trends and Opportunities Driving Efficiency and Sustainability

Regulatory-Driven Shift to Low-Global Warming Potential (GWP) Blowing Agents

A defining trend in the refrigeration insulation materials market is the regulatory-driven transition away from high-GWP hydrofluorocarbons (HFCs) towards more sustainable blowing agents. The Kigali Amendment to the Montreal Protocol, ratified by the U.S. in October 2022, mandates an 85% phasedown in HFC production and consumption by 2036. This global agreement has created a clear pathway for material innovation, requiring insulation manufacturers to accelerate the development and adoption of alternatives with a lower climate impact. At the national level, the U.S. Environmental Protection Agency’s (EPA) AIM Act is enforcing phasedown schedules and use restrictions, with new regulations taking effect in January 2025 that ban higher-GWP HFCs in new foams and refrigeration equipment. These policies are reshaping the competitive dynamics of the market, pushing manufacturers to adopt hydrofluoroolefins (HFOs), hydrocarbons, and other emerging low-GWP blowing agents. Compliance with these mandates not only supports sustainability goals but also enhances the marketability of insulation solutions for global appliance and cold chain manufacturers increasingly prioritizing environmental performance.

Adoption of Vacuum Insulation Panels (VIPs) for Ultra-Thin, High-Efficiency Applications

Another key trend is the rapid adoption of vacuum insulation panels (VIPs) for applications requiring superior energy efficiency and space savings. VIPs deliver thermal conductivity values significantly lower than conventional polyurethane foams, enabling thinner insulation walls without compromising performance. A 2025 research study demonstrated that refrigerators with 56% VIP coverage reduced energy consumption by 21% compared to models using standard foam insulation. For appliance manufacturers, this creates a unique value proposition: thinner walls mean larger internal capacity, a feature particularly attractive in premium product lines. Beyond residential and commercial refrigeration, VIPs are transforming cold chain logistics for pharmaceuticals, vaccines, and perishable foods. Companies like Kingspan highlight that their VIP solutions can maintain precise temperature conditions over extended periods, meeting stringent regulatory requirements for safe transport. This dual appeal—higher efficiency in appliances and reliability in cold chain logistics—positions VIPs as a disruptive innovation in the refrigeration insulation materials market.

Development of Bio-Based and Circular Polyol Feedstocks for Polyurethane Foams

The drive toward sustainability is opening strong opportunities for bio-based and circular polyol feedstocks in polyurethane foam insulation. Traditional rigid foams rely heavily on fossil-derived raw materials, but companies like Emery Oleochemicals are commercializing polyols derived from rapidly renewable natural oils with 70–100% bio-based content, certified by the USDA’s BioPreferred® program. These renewable feedstocks reduce carbon footprints and appeal to manufacturers under pressure to lower Scope 3 emissions. Beyond bio-based innovation, circularity is advancing through chemical recycling. Emery’s INFIGREEN® polyols, produced from scrap polyurethane foam, are creating a closed-loop system that reintroduces end-of-life foam into new insulation materials. This dual pathway—renewable inputs and chemical recycling—supports a circular economy model, enhancing brand positioning and regulatory compliance. For manufacturers and end-users, the adoption of bio-based and recycled polyols not only supports ESG targets but also provides a competitive edge in markets with strong environmental procurement policies.

Integration of Phase Change Materials (PCMs) for Thermal Energy Storage

The integration of phase change materials (PCMs) into refrigeration insulation systems represents another breakthrough opportunity. PCMs function by absorbing and releasing latent heat during phase transitions, significantly improving thermal stability and energy efficiency. A study by London South Bank University demonstrated that encapsulated ice PCMs in domestic refrigerators enhanced “autonomy,” allowing the units to maintain stable temperatures during power outages or compressor off-cycles. This functionality is critical in regions with unstable power supply or high electricity costs. Furthermore, PCMs can flatten energy demand curves by reducing compressor cycling, which is the most energy-intensive aspect of the refrigeration process. By lowering peak energy loads, PCMs extend equipment life, reduce maintenance costs, and cut greenhouse gas emissions associated with energy consumption. As utilities and governments push for demand-side energy management, PCM-enabled insulation systems will gain traction, offering both environmental and cost-saving benefits across residential, commercial, and industrial refrigeration sectors.

Competitive Landscape: Leading Chemical and Insulation Companies Are Driving Innovation in Refrigeration Thermal Efficiency

The competitive landscape of refrigeration insulation materials is dominated by companies combining advanced materials, low GWP solutions, and sustainable innovations to meet growing market demand. Industry leaders focus on energy efficiency, regulatory compliance, and environmental sustainability.

BASF SE: Championing Low GWP Insulation Materials and Circular Economy Initiatives

BASF SE supplies raw materials for PU and PIR foams in refrigeration applications. In March 2025, the company piloted an insulation board containing 10% recycled content, emphasizing circular economy principles. BASF’s HFO-blown PIR system enhances energy efficiency and reduces environmental impact, positioning it as a key partner for green transformation in the refrigeration insulation market. Key offerings include Neopor® EPS and polyurethane foams used across appliances, cold storage, and refrigerated transport.

Covestro AG: Pioneering High-Tech Polyurethane Solutions for Energy-Efficient Refrigeration

Covestro AG is a leading producer of polyurethane foams used in refrigeration insulation. The company focuses on circularity, reducing fossil resource dependence and integrating alternative raw materials such as biomass and waste. Covestro continuously innovates to deliver lightweight, durable, and environmentally compatible insulation, supporting appliances, construction, and transport applications, and invests heavily in global production capacity to meet rising demand.

Kingspan Group Plc: Delivering High-Performance Insulated Panels for Cold Chain Applications

Kingspan provides high-performance insulation solutions, including its QuadCore® Technology, offering exceptional thermal and fire performance. Its products serve cold storage facilities, food processing plants, and pharmaceutical warehouses. Kingspan’s strategic acquisitions, including a majority stake in STEICO SE, enhance its product portfolio and global footprint. The company’s focus on energy efficiency and sustainability makes its insulation solutions ideal for refrigeration applications.

Saint-Gobain: Integrating Bio-Based and Fire-Resistant Materials for Sustainable Insulation

Saint-Gobain delivers thermal and acoustic insulation materials with fire resistance and energy efficiency, including glass wool and stone wool products under the Isover brand. Its ECOSE Technology utilizes bio-based binders, reducing VOC emissions. Strategic acquisitions, such as Kaimann in 2018, strengthened its industrial insulation offerings. The company’s focus on innovation and sustainability positions it as a key player in environmentally conscious refrigeration solutions.

Armacell International S.A.: Specializing in Flexible and Aerogel-Based Insulation for Space-Constrained Applications

Armacell leads in flexible foams for HVAC and refrigeration systems, with products like ArmaFlex to prevent condensation and energy loss. Recent innovations include ArmaGel HT, an aerogel blanket offering up to five times higher thermal efficiency, enabling thinner insulation for space-limited systems. Armacell’s products are designed for durability, ease of installation, and system integration, providing reliable, energy-efficient refrigeration solutions.

Refrigeration Insulation Materials Market Share Insights, 2025-2034

Residential Refrigeration Leads Market Share by Application in Refrigeration Insulation Materials

Residential refrigeration accounts for 30% of the market, reflecting its dominance as the highest-volume application for insulation materials across refrigerators and freezers produced globally. The driving force here is regulatory tightening on energy efficiency standards, which has compelled OEMs to adopt advanced polyurethane foams and next-generation blowing agents such as hydrocarbons and HFOs. These transitions require full production line reengineering, positioning insulation as a decisive performance factor in appliance competitiveness. Refrigerated transportation follows closely with 25% share, where insulation materials must withstand vibration, mechanical stress, and thermal cycling in trailers, shipping containers, and air cargo. Rigid polyurethane and PIR foams remain dominant, but adoption of vacuum insulation panels (VIPs) is rising in high-value shipments, including pharmaceuticals. Commercial refrigeration contributes 20%, focusing on supermarket display cases and walk-in coolers that demand low-GWP, non-flammable foams for safety in consumer-facing environments. Cold storage and warehouses represent 15%, where thick layers of spray polyurethane foams or rigid insulation panels deliver long-term ROI through lifetime energy savings. Industrial refrigeration, with 10% share, covers ultra-low-temperature environments, such as food freezing and chemical processing, requiring multilayer systems that combine PUR/PIR, XPS, and aerogels. Collectively, this segmentation highlights how efficiency mandates and application-specific performance requirements dictate insulation material adoption across refrigeration systems.

Food & Beverages Dominate Market Share by End-Use in Refrigeration Insulation Materials

The food and beverages industry is the largest consumer at 60%, cementing its status as the backbone of the refrigeration insulation materials market. From household refrigerators to industrial cold storage warehouses, F&B applications span the full cold chain, and investments are tied directly to reducing food waste and energy costs. Pharmaceuticals and healthcare account for 20%, driven by the critical need for temperature assurance in vaccine distribution, biologics storage, and clinical trial logistics. This segment increasingly adopts high-value solutions such as VIPs and phase-change materials, where precision insulation is worth the premium. Logistics and shipping represent 15%, functioning as the enabling sector for cold chain operations, requiring insulation that balances payload capacity and thermal efficiency in refrigerated trucks, marine containers, and air freight units. Chemicals at 4% use refrigeration insulation in process control, liquefaction, and safe handling of volatile products, favoring chemically resistant insulation such as foam glass or mineral wool. Oil and gas, though the smallest segment at 1%, demand insulation for LNG pipelines and terminals, requiring extreme cryogenic performance and fire safety compliance from materials like PIR, perlite, and cellular glass. Overall, the dominance of F&B underscores how sustainability, safety, and regulatory compliance drive insulation adoption, while healthcare and logistics ensure growth in high-value, precision-demanding niches.

European Union: Green Deal Policies and High-Performance Insulation Driving Market Growth

The European Union is at the forefront of the refrigeration insulation materials market, backed by a strong legislative and financial framework aligned with the European Green Deal. The Renewable Energy Directive (EU/2023/2413) places clear emphasis on renewable heating and cooling systems, positioning advanced insulation materials as a cornerstone of energy efficiency. Meanwhile, the Ecodesign Directive and Energy Labelling Regulation for refrigerating appliances establish strict minimum energy efficiency requirements, compelling manufacturers to adopt high-performance insulation foams, panels, and composites that minimize energy losses.

Funding support through the Recovery and Resilience Facility (RRF) is accelerating the replacement of outdated fossil fuel-based systems across member states with low-carbon, efficient alternatives that require insulation with low Global Warming Potential (GWP). Companies are focusing on developing next-generation insulation foams and panels, combining thermal efficiency, durability, and recyclability. Innovations such as low-GWP blowing agents and bio-based composites are particularly encouraged under EU climate goals. The bloc’s consistent policy support, along with investments in R&D, cements its role as a global leader in sustainable refrigeration insulation materials.

United States: Vacuum Insulation and Cold Chain Expansion Fueling Demand

In the United States, the EPA and Department of Energy (DOE) are advancing the refrigeration insulation materials market through regulatory frameworks and funding initiatives. The DOE’s Building Technologies Office and the EPA’s GreenChill program emphasize energy efficiency in commercial refrigeration, driving adoption of eco-friendly, low-GWP insulation foams. Significant federal support under the Infrastructure Investment and Jobs Act is channeling funds into building retrofits and energy-efficient projects, expanding the demand for insulation solutions.

A landmark technological innovation is Whirlpool’s SlimTech™ insulation technology, which replaces polyurethane foams with a proprietary powder-based vacuum insulation structure, increasing both storage capacity and thermal performance. The U.S. market also benefits from growth in the cold chain sector, where food waste reduction and pharmaceutical storage needs are spurring demand for high-performance refrigerated transport insulation. Manufacturers are also scaling bio-based composites and solvent-free coatings, aligning with consumer demand for sustainable solutions. This convergence of innovation, regulation, and infrastructure investment is positioning the U.S. as a high-potential growth hub for refrigeration insulation technologies.

China: Green Cooling Plan and Cold Chain Expansion Driving Insulation Adoption

China is experiencing rapid growth in the refrigeration insulation materials market, supported by policy measures in the 14th Five-Year Plan, which prioritize energy efficiency and carbon reduction. The General Code for Building Energy Efficiency and Renewable Energy Utilization (GB 55015-2021), effective since April 2022, establishes mandatory insulation standards for buildings, raising the demand for advanced thermal materials. The government’s Green Cooling Action Plan further targets a 25% improvement in cooling product efficiency by 2030, fueling the adoption of next-generation refrigeration insulation materials.

China’s booming cold chain and e-commerce sectors are significantly increasing the need for efficient refrigerated trucks and storage facilities. Local companies are investing in fiber-optic-enabled smart insulation systems and experimenting with eco-friendly foams, such as PIR-based insulation that meets green building standards. Furthermore, the government’s strict plastic pollution controls are accelerating the development of recyclable and sustainable insulation products. With international companies like PERMA-PIPE forming alliances with Chinese distributors, the country is emerging as both a production hub and a large consumer market for refrigeration insulation.

India: Regulatory Reforms and Cold Chain Expansion Boosting Market Growth

In India, the Refrigerating Appliances (Quality Control) Amendment Order, 2025, issued by the Bureau of Indian Standards (BIS), sets higher quality benchmarks for refrigerating appliances, reinforcing demand for premium insulation materials. Alongside this, the Energy Conservation Building Code (ECBC) mandates minimum thermal performance standards for commercial and residential buildings, pushing demand for energy-efficient insulation.

India’s rapidly growing cold chain industry, driven by food processing and pharmaceuticals, is creating substantial opportunities for refrigeration insulation suppliers. Government support for a reverse supply chain for refrigerants under the Plastic Waste Management Rules (2022 Amendment) ensures that insulation materials also align with circular economy objectives. Innovations include high-density polyurethane foams and multi-layer composite panels designed to withstand India’s extreme climates. The combination of stringent quality norms and industrial demand from pharmaceuticals and food logistics makes India a fast-growing regional market for refrigeration insulation solutions.

Japan: Advanced Materials and Circular Economy Leading Innovation

Japan is recognized as a pioneer in advanced refrigeration insulation materials, with innovations such as Tiger Corporation’s Stainless Steel Vacuum Insulation Panel (TIVIP). Supported by the Osaka Prefectural Government, this material delivers 10–25 times lower thermal conductivity compared to conventional insulators, positioning Japan at the cutting edge of thermal insulation technology.

The government’s Plastic Resource Circulation Strategy, mandating reusable and recyclable packaging by 2025, indirectly influences the refrigeration sector by promoting eco-friendly and recyclable insulation materials. Japanese companies are simultaneously focusing on durability, non-flammability, and recyclability, embedding sustainability into product design. With a strong circular economy agenda and leadership in vacuum insulation technologies, Japan is driving global best practices for next-generation refrigeration insulation materials.

Brazil: Energy Efficiency Policies and Reverse Logistics Supporting Market Adoption

In Brazil, the National Solid Waste Policy (PNRS) underpins the refrigeration insulation materials market, emphasizing recycling, reuse, and waste reduction. The government promotes a reverse logistics system, making producers responsible for post-consumer packaging and refrigeration material disposal.

The National Electricity Conservation Program (PROCEL) and the Leapfrogging to Energy-Efficient Refrigerating Appliances Project are accelerating Brazil’s transition to MEPS-compliant refrigeration systems. These policies are further supported by energy subsidies for heat pumps and efficient cooling systems, creating demand for high-performance insulation. The country’s expanding retail and food sectors are adopting MAP-enabled trays, vacuum-sealed films, and insulated storage solutions to extend product shelf life and reduce energy consumption. With this dual focus on energy efficiency and circular economy practices, Brazil is strengthening its role as a Latin American leader in refrigeration insulation adoption.

Refrigeration Insulation Materials Market Report Scope

Refrigeration Insulation Materials Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$8.8 Billion

|

|

Market Size (2034)

|

$15.3 Billion

|

|

Market Growth Rate

|

6.3%

|

|

Segments

|

By Material Type (PU & PIR Foams, Polystyrene Foams, Fiberglass, Phenolic Foams, Elastomeric Foams, Aerogels, VIPs, Mineral Wool), By Application (Refrigerated Transportation, Cold Storage & Warehouse, Commercial Refrigeration, Industrial Refrigeration, Residential Refrigeration), By End-Use Industry (Food & Beverages, Pharmaceuticals & Healthcare, Chemicals, Logistics & Shipping, Oil & Gas)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Kingspan Group Plc, Owens Corning, Saint-Gobain, BASF SE, Armacell International S.A., The Dow Chemical Company, Huntsman Corporation, Rockwool International A/S, Zotefoams plc, Johns Manville, Knauf Insulation, Aspen Aerogels, Inc., L'Isolante K-Flex S.p.A., Morgan Advanced Materials, Evonik Industries AG

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Refrigeration Insulation Materials Market Segmentation

By Material Type

- PU & PIR Foams

- Polystyrene Foams

- Fiberglass

- Phenolic Foams

- Elastomeric Foams

- Aerogels

- VIPs

- Mineral Wool

By Application

- Refrigerated Transportation

- Cold Storage & Warehouse

- Commercial Refrigeration

- Industrial Refrigeration

- Residential Refrigeration

By End-Use Industry

- Food & Beverages

- Pharmaceuticals & Healthcare

- Chemicals

- Logistics & Shipping

- Oil & Gas

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Refrigeration Insulation Materials Market

- Kingspan Group Plc

- Owens Corning

- Saint-Gobain

- BASF SE

- Armacell International S.A.

- The Dow Chemical Company

- Huntsman Corporation

- Rockwool International A/S

- Zotefoams plc

- Johns Manville

- Knauf Insulation

- Aspen Aerogels, Inc.

- L'Isolante K-Flex S.p.A.

- Morgan Advanced Materials

- Evonik Industries AG

* List Not Exhaustive

Methodology

USDAnalytics employs a rigorous, multi-step methodology to analyze the refrigeration insulation materials market, combining both quantitative and qualitative research techniques to ensure accurate, actionable insights for industry professionals. Our process begins with an extensive secondary research phase, gathering data from regulatory filings, industry reports, company press releases, patents, trade journals, and credible news sources to understand market dynamics, competitive landscapes, and technological innovations. We then validate this information through primary interviews with key stakeholders, including manufacturers, distributors, and end-users across residential, commercial, industrial, and cold chain segments. Market sizing and forecasts are determined using historical trends, current adoption rates, and policy-driven growth scenarios, with particular attention to materials such as PU/PIR foams, VIPs, aerogels, and bio-based alternatives. USDAnalytics also integrates regional regulatory frameworks, energy efficiency mandates, and sustainability initiatives into our analytical model to evaluate their impact on market growth. Finally, we synthesize data using advanced statistical and predictive modeling techniques, producing insights on material trends, application adoption, end-use segmentation, and competitive strategies, enabling decision-makers to capitalize on emerging opportunities in a market increasingly driven by energy efficiency, environmental compliance, and technological innovation.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.