Rigid Packaging in the Pharmaceuticals Market Overview: Growing Demand for Sterility and Sustainability

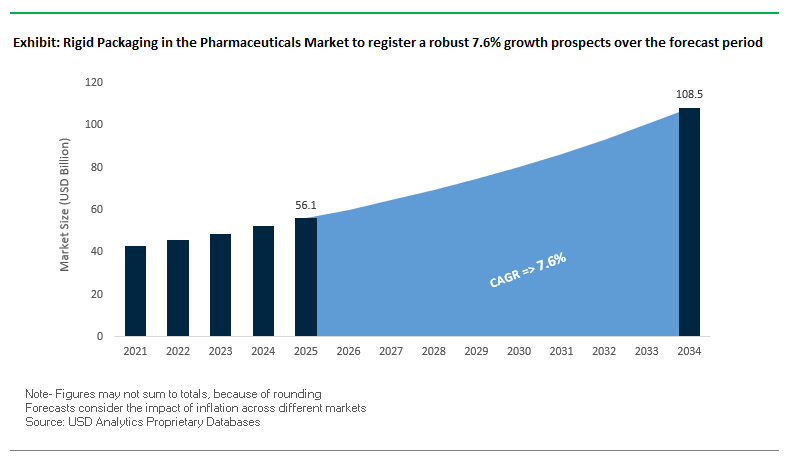

The Global Rigid Packaging in the Pharmaceuticals Market is valued at $56.1 billion in 2025 and is projected to reach $108.5 billion by 2034, growing at a robust CAGR of 7.6%. Rigid pharmaceutical packaging plays a critical role in ensuring product safety, sterility, and patient compliance, particularly in biologics, vaccines, and high-value injectable therapies. Plastics and polymers dominate the market due to their cost-effectiveness, versatility, and superior barrier properties, making them indispensable for vials, bottles, syringes, and containers.

The rising demand for vials and ampoules driven by injectable drugs and global vaccine programs further fuels market expansion. In addition, the market is undergoing a notable transformation toward child-resistant and senior-friendly rigid packaging, ensuring safety while supporting adherence to medication schedules. With biologics and specialty medicines gaining momentum, these packaging formats are no longer simply protective but are increasingly designed to enhance the patient experience.

Sustainability is another defining factor. A Jabil 2024 survey revealed that 68% of packaging decision-makers have publicly committed to sustainable packaging, signaling a shift from petroleum-based plastics toward bio-based polymers, recyclable rigid containers, and circular material streams. Companies are innovating to meet ESG targets, regulatory expectations, and consumer preference for greener healthcare solutions.

Key Insights for Industry Professionals

- Plastics dominate rigid pharmaceutical packaging for their versatility, durability, and barrier properties.

- Vials and ampoules are critical for injectable drugs and vaccines, sustaining strong market demand.

- Sustainability commitments are accelerating adoption of recyclable and bio-based rigid packaging solutions.

- Patient safety and compliance drive innovations in child-resistant and senior-friendly rigid packaging.

Market Analysis: Strategic Developments in Rigid Pharmaceutical Packaging

The rigid pharmaceutical packaging industry is being shaped by mergers, acquisitions, product innovations, and sustainability-driven investments. In August 2025, Nuoyuan Medical completed a Phase I clinical trial in China for a new fluorescent imaging agent, underlining the rising demand for specialized pharmaceutical packaging that ensures drug safety in advanced diagnostics. Also in August 2025, Currier Plastics Inc. appointed a new Business Development Manager to expand healthcare partnerships, reinforcing the importance of rigid plastics in medical packaging.

In July 2025, Amcor significantly expanded its healthcare packaging network in Costa Rica, strengthening its presence in Latin America’s fast-growing pharmaceutical sector. Around the same time, Aptar Pharma introduced its first nasal pump with 52% bio-based material, showing how rigid healthcare packaging is aligning with sustainability imperatives. Further in June 2025, Neopac won a WorldStar Award for its recyclable Polyfoil® Mono-Material Barrier Tube, highlighting advances in high-barrier rigid packaging solutions.

Industry consolidation remains a powerful driver. In April 2025, Amcor completed its acquisition of Berry Global, creating a new global giant in consumer and healthcare rigid plastic packaging, with projected cost savings exceeding $650 million by FY 2028. This followed the initial merger announcement in November 2024, valued at $8.4 billion, positioning Amcor as a dominant player in rigid pharma packaging. Meanwhile, in March 2025, Constantia Flexibles and Aluflexpack AG joined forces to enhance their leadership in premium sustainable packaging, expanding product synergies across rigid and flexible categories.

Rigid Packaging in the Pharmaceuticals Market: Emerging Trends and Strategic Opportunities

Accelerated Adoption of Recyclable Mono-Material Polymer Structures

A defining trend in the rigid pharmaceutical packaging market is the accelerated adoption of recyclable mono-material polymer structures, such as all-polypropylene (PP) or polyethylene (PE) designs. Traditionally, pharmaceutical packaging has relied on multi-layer laminates, but these have posed significant challenges for recycling. Regulatory mandates and corporate sustainability pledges are now forcing the shift to fully recyclable solutions. The European Union’s Circular Economy Action Plan, which mandates that all packaging must be recyclable by 2030, has become a key compliance driver. This legislation directly impacts the pharmaceutical industry, where rigid containers like blister packs and bottles are being redesigned to ensure they are compatible with recycling streams.

The momentum is not limited to regulation corporate ESG strategies are equally influential. Companies like Johnson & Johnson, Novartis, and Merck have pledged to make all packaging recyclable, reusable, or compostable within the next decade. Packaging innovators are responding with technologies such as Constantia Flexibles’ PERPETUA ALTA, a mono-material polypropylene laminate tailored to pharmaceutical needs. These advances combine recyclability with high-performance barrier properties, addressing the dual challenge of sustainability and drug integrity. By aligning with both compliance pressures and corporate commitments, recyclable mono-material packaging is establishing itself as the new standard for the sector.

Integration of Connected Packaging for Patient Adherence and Authentication

Another transformative trend is the integration of smart, connected packaging solutions. Pharmaceutical packaging is moving beyond containment to become an interactive platform that enhances patient safety, adherence, and supply chain security. Labels, bottle caps, and blister foils embedded with QR codes, NFC chips, and RFID tags are increasingly being deployed to tackle the global issue of counterfeit drugs and to support patient-centric healthcare models.

The scale of the counterfeit challenge is significant: the WHO estimates that up to 10% of medical products in low- and middle-income countries are falsified or substandard. To counter this, industry-wide collaborations such as the MediLedger Project are using blockchain and IoT-enabled packaging to verify authenticity across the supply chain, in compliance with U.S. DSCSA regulations. Beyond security, connected packaging plays a pivotal role in medication adherence. Research from the AARDEX Group highlights that smart packaging can achieve 97% adherence accuracy, compared with just 27% from patient self-reporting. This has implications not only for improving patient health outcomes but also for increasing the statistical reliability of clinical trials, where non-adherence rates can reach as high as 40% after a year. By embedding digital technologies, rigid pharmaceutical packaging is becoming an enabler of both healthcare delivery and regulatory compliance.

Development of High-Barrier, Glass-Free Solutions for Biologics

A critical growth opportunity lies in replacing traditional glass containers with advanced rigid polymer solutions that offer comparable barrier performance against oxygen and moisture. While glass has long been the benchmark for packaging biologics and injectable drugs, it presents drawbacks such as fragility, weight, and the risk of delamination. These limitations become particularly challenging in cold chain logistics, where breakage can compromise sensitive biologics and vaccines.

Polymer-based innovations are addressing these gaps. Companies are developing nanocomposite films and high-barrier biopolymers that provide the required protection while offering advantages in weight reduction and durability. Glass-free polymer packaging also enables cost savings in logistics by reducing freight weight and minimizing the risk of damaged shipments. With the biologics segment expected to dominate future pharmaceutical pipelines, high-barrier polymer packaging represents a sustainable, cost-effective, and performance-driven alternative to glass.

Implementation of Child-Resistant and Senior-Friendly Features for Home Healthcare

The expansion of self-administered therapies and home healthcare has created strong demand for packaging that balances child resistance (CR) with senior-friendly (SF) usability. Packaging must meet strict international standards to prevent accidental ingestion by children, while also being accessible to elderly patients who often struggle with dexterity.

Innovative solutions are emerging to address this dual requirement. HERMES PHARMA has introduced stick packs with laser-cut designs that are proven child-resistant yet easy for adults to open. Similarly, new blister pack formats with “peel-and-push” mechanisms maintain safety compliance while improving usability for seniors. As the aging population grows and more therapies shift toward home administration, CR/SF packaging features are becoming a strategic differentiator. Manufacturers that successfully deliver safety without sacrificing accessibility will gain a competitive advantage in patient-centric pharmaceutical markets.

Competitive Landscape: Leading Companies in Global Rigid Pharmaceutical Packaging

The rigid packaging in pharmaceuticals market is highly competitive, with leading players focusing on sterility, sustainability, and patient-centric design.

Gerresheimer AG: A Global Leader in Primary Glass and Plastic Packaging

Gerresheimer specializes in vials, syringes, ampoules, and cartridges, serving pharmaceutical companies worldwide. In late 2024, the company invested €100 million in a new facility in Querétaro, Mexico, enhancing production capacity to meet rising regional demand. Gerresheimer is committed to cutting CO2 emissions by 50% by 2030, with all energy sourced from renewables. Its InnoSafe® syringe line exemplifies its focus on patient safety and compliance in rigid pharma packaging.

Amcor plc: Expanding Rigid Pharma Leadership Through Strategic Acquisitions

Amcor offers rigid bottles, vials, and containers tailored for sterile applications in the pharmaceutical sector. With the Berry Global acquisition (2024–2025), Amcor emerged as a global powerhouse in rigid healthcare packaging, combining portfolios for stronger customer reach. Its AmPrima™ Recycle Ready rigid packaging sets new standards for recyclability without compromising barrier performance, aligning with its 2025 goal for fully recyclable solutions.

AptarGroup, Inc.: Driving Innovation in Drug Delivery and Rigid Components

AptarGroup is a pioneer in drug delivery devices and rigid packaging components such as rigid needle shields (RNS) and pre-filled syringe plungers. In July 2025, it launched APF Futurity™, a recyclable, metal-free nasal spray pump, certified Class A.A. by Cyclos-HTP. Its HeroTracker® Sense digital solution integrates rigid packaging with digital adherence monitoring, strengthening Aptar’s role in patient-centered drug delivery.

Constantia Flexibles: Sustainable High-Barrier Pharma Packaging Solutions

Constantia Flexibles plays a critical role in rigid packaging when paired with barrier foils, labels, and laminates for pharmaceutical applications. In 2025, it won two WorldStar Global Packaging Awards for sustainable solutions like EcoPeelCover and EcoLamHighPlus, underscoring its innovation credentials. Its March 2025 acquisition of Aluflexpack AG boosts its influence in premium packaging, combining flexible and rigid systems to meet pharma-grade requirements.

Sonoco Products Company: Cold Chain Rigid Packaging Specialist

Sonoco, through its ThermoSafe division, is a leading player in temperature-assured rigid packaging for biologics, vaccines, and specialty drugs. Its ISC Labs® design services provide customized validation and testing to ensure regulatory compliance in the cold chain. In April 2025, Sonoco divested its thermoformed and flexible packaging unit to TOPPAN Holdings, streamlining its focus on core pharma cold chain solutions. With ThermoSafe, Sonoco ensures product integrity and safety across global supply chains.

Rigid Packaging in the Pharmaceuticals Market Share Insights

Bottles and Containers Lead Market Share by Product Type in Pharmaceutical Rigid Packaging

Bottles and containers command the largest share of rigid pharmaceutical packaging, accounting for around 35% of the market in 2025. Their leadership is underpinned by unmatched versatility across oral solid dosage forms (tablets, capsules), OTC medications, and liquid formulations such as syrups and suspensions. Cost efficiency, scalability for mass production, and ease of global distribution further solidify their position. Pharmaceutical manufacturers prefer bottles because they are adaptable to high-volume prescriptions, comply with tamper-evidence and child-resistance requirements, and offer large labeling surfaces for regulatory and branding information. With the rise of chronic diseases, the volume of oral medications continues to climb, ensuring bottles remain the backbone of pharmaceutical rigid packaging despite rising competition from blister packs and pre-filled formats.

Pharmaceutical Manufacturing Dominates Market Share by End-User in Rigid Packaging

Pharmaceutical manufacturers hold the majority share at 65%, making them the most influential end-users in the rigid pharmaceutical packaging market. Their dominance stems from the fact that packaging is locked into drug regulatory filings at the development stage, meaning manufacturers control long-term material choices. This entrenched decision-making process ensures that bottles, blisters, vials, and ampoules are designed for compliance with stability testing, sterility, and serialization requirements. Regulatory authorities such as the FDA and EMA demand that packaging specifications are validated for each drug product, further reinforcing the manufacturers’ central role. As biologics and injectables gain prominence, manufacturers are also driving innovation in sterile packaging formats, underscoring their strategic control of packaging adoption and investment.

United States: Sustainability and Smart Rigid Packaging Transforming Pharmaceutical Supply Chains

The U.S. rigid packaging market for pharmaceuticals is being reshaped by a rising emphasis on sustainability and consumer awareness. Demand for recyclable and compostable packaging solutions for over-the-counter (OTC) medications and nutraceuticals is driving manufacturers to explore bio-based plastics and lightweighting strategies, reducing the environmental footprint while ensuring compliance with safety regulations.

Technological advancements are a critical growth driver. The Drug Supply Chain Security Act (DSCSA) mandates robust track-and-trace systems, fueling demand for smart packaging solutions with barcodes and RFID tags to prevent counterfeiting and enhance patient safety. Government support, such as the Department of Energy’s $52 million funding toward cellulose-based films, highlights the shift toward next-generation sustainable materials. Corporations like Amcor are leading with innovations such as AmLite Ultra Recyclable, a high-barrier polyolefin film, which significantly reduces the carbon footprint of rigid packaging. Additionally, FDA regulations on tamper-evident closures, child-resistant features, and clear labeling continue to shape the design and functionality of pharmaceutical rigid packaging, ensuring product integrity and consumer safety.

Germany: Circular Economy and High-Tech Rigid Packaging Driving Compliance

Germany’s rigid pharmaceutical packaging market is governed by a stringent regulatory framework, including the EU Packaging and Packaging Waste Regulation (PPWR 2025), which emphasizes eco-friendly and highly recyclable solutions. The Packaging Act (Verpackungsgesetz) incentivizes manufacturers to adopt mono-material films like polyethylene (PE) and polypropylene (PP), driving innovation in recyclable packaging materials.

Technological advancements are central to market growth. German converters are embedding oxygen-barrier labels with unique device identification (UDI) data, ensuring drug stability and compliance with EU MDR regulations. Investments in high-speed, high-precision filling and sealing equipment enhance production efficiency and product quality, reinforcing Germany’s position as a hub for advanced pharmaceutical rigid packaging. The combination of governmental mandates and advanced manufacturing capabilities is driving adoption of sustainable and technologically advanced rigid packaging solutions.

China: Policy-Driven Sustainability and Smart Automation in Pharmaceutical Rigid Packaging

China’s rigid packaging market for pharmaceuticals is experiencing rapid transformation due to government initiatives targeting the dual carbon goals of carbon peak and carbon neutrality. Policies promoting eco-friendly and reusable materials are influencing healthcare packaging design and production, especially for over-the-counter (OTC) medications.

Technological investments, including automation, AI, and 5G-enabled industrial internet integration, are optimizing production efficiency and flexible manufacturing capacity. Regulatory reforms, such as the NMPA’s June 2025 Good Manufacturing Practice announcement, require comprehensive quality management systems for pharmaceutical excipients and packaging materials, which elevates the standards for rigid packaging materials. The growth of e-commerce platforms is also boosting demand for secure, tamper-proof rigid packaging, while industry innovations driven by regular supplier quality assessments ensure high-quality, reliable packaging solutions.

India: Domestic Production and Smart Label Integration Driving Pharmaceutical Rigid Packaging

India’s rigid pharmaceutical packaging industry is benefitting from governmental initiatives like Make in India and Zero Effect Zero Defect, which encourage high-quality domestic manufacturing supported by robust industrial infrastructure investments. The Production Linked Incentive (PLI) Scheme, with an outlay of INR 10,900 crore, is enhancing India’s capabilities in producing standardized, high-quality rigid packaging solutions.

Regulatory measures, including the Plastic Waste Management (Amendment) Rules and Food Safety and Standards Packaging and Labelling Regulations, are accelerating the shift toward eco-friendly packaging alternatives. Additionally, the adoption of RFID and smart labeling technologies is increasing, exemplified by Epson India’s December 2024 launch of a high-speed color inkjet label printer, enabling pharmaceutical companies to integrate advanced labels into rigid packaging. These developments are strengthening India’s position in the sustainable and technology-driven pharmaceutical packaging market.

Rigid Packaging in the Pharmaceuticals Market Report Scope

Rigid Packaging in the Pharmaceuticals Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$56.1 Billion

|

|

Market Size (2034)

|

$108.5 Billion

|

|

Market Growth Rate

|

7.6%

|

|

Segments

|

By Material Type (Plastics, Glass, Metal, Paper & Paperboard, Bioplastics), By Product Type (Blister Packs, Bottles & Containers, Vials & Ampoules, Jars & Tubes, Other Product Types), By Application (Solid Dosage, Liquid Dosage, Parenterals, Medical Devices, Powders & Granules, Other Applications), By End-User (Pharmaceutical Manufacturing, Medical Device OEMs, Contract Packaging Organizations, Retail Pharmacies, Other End-Users)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, Gerresheimer AG, Berry Global Inc., AptarGroup, Inc., West Pharmaceutical Services, Inc., SGD Pharma, Mondi Group, Becton Dickinson and Company, Nippon Paper Industries Co., Ltd., Huhtamaki Oyj, WestRock Company, CCL Industries Inc., Sonoco Products Company, Origin Pharma Packaging, Constantia Flexibles

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Rigid Packaging in the Pharmaceuticals Market Segmentation

By Material Type

- Plastics

- Glass

- Metal

- Paper & Paperboard

- Bioplastics

By Product Type

- Blister Packs

- Bottles & Containers

- Vials & Ampoules

- Jars & Tubes

- Other Product Types

By Application

- Solid Dosage

- Liquid Dosage

- Parenterals

- Medical Devices

- Powders & Granules

- Other Applications

By End-User

- Pharmaceutical Manufacturing

- Medical Device OEMs

- Contract Packaging Organizations

- Retail Pharmacies

- Other End-Users

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Rigid Packaging in the Pharmaceuticals Market

- Amcor plc

- Gerresheimer AG

- Berry Global Inc.

- AptarGroup, Inc.

- West Pharmaceutical Services, Inc.

- SGD Pharma

- Mondi Group

- Becton Dickinson and Company

- Nippon Paper Industries Co., Ltd.

- Huhtamaki Oyj

- WestRock Company

- CCL Industries Inc.

- Sonoco Products Company

- Origin Pharma Packaging

- Constantia Flexibles

* List Not Exhaustive

Methodology

USDAnalytics has conducted an extensive and data-driven study of the global Rigid Packaging in the Pharmaceuticals Market, integrating both primary and secondary research to provide actionable insights for industry professionals. Our methodology includes consultations with pharmaceutical manufacturers, packaging designers, regulatory experts, and logistics operators, complemented by analysis of corporate reports, mergers and acquisitions, sustainability initiatives, and technological innovations. Market sizing and growth projections are based on historical trends, the rising adoption of recyclable mono-material polymers, connected smart packaging, and high-barrier polymer solutions replacing glass. Segmentation analysis encompasses material type, product type, application, and end-user, while regional insights cover key markets including the U.S., Germany, China, and India. Competitive intelligence evaluates strategic developments, sustainability commitments, and product innovations by leading players such as Amcor, Gerresheimer, AptarGroup, and Constantia Flexibles. By combining regulatory analysis, ESG considerations, and patient-centric packaging trends, USDAnalytics delivers precise, professional, and market-ready insights for stakeholders navigating the evolving pharmaceutical rigid packaging landscape.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.