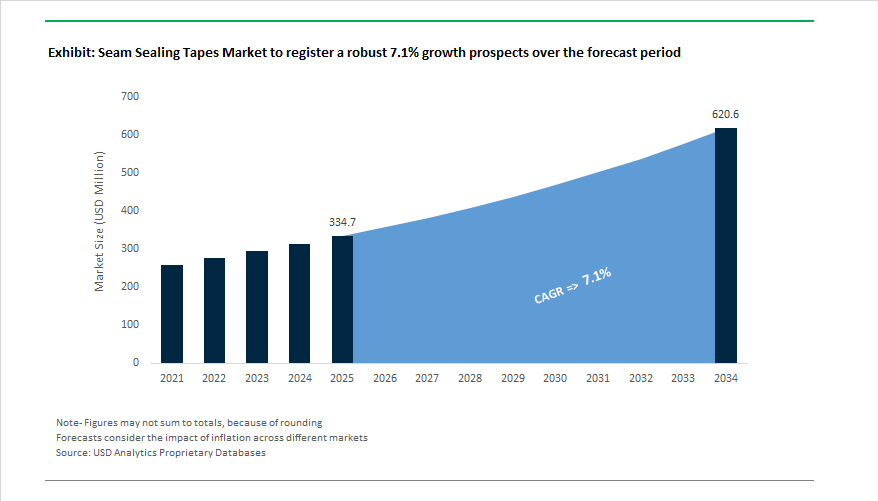

The Global Seam Sealing Tapes Market is projected to grow from $334.7 million in 2025 to $620.5 million by 2034, registering a CAGR of 7.1%. The industry is undergoing a material and technological transformation driven by sustainability mandates, advanced textile engineering, and the shift toward PFAS-free waterproofing technologies. Seam sealing tapes have evolved into high-precision components critical to the integrity, performance, and longevity of waterproof garments, medical protective wear, and industrial fabrics — sectors where moisture ingress control and material flexibility define end-user safety and comfort.

The apparel segment dominates the market, particularly within outdoor sportswear, mountaineering gear, and professional rainwear. These applications require hydrostatic pressure ratings of 20,000mm to 40,000mm water column, making adhesive formulation, layer construction, and substrate compatibility essential to performance durability. In parallel, the medical and chemical protective clothing segment has emerged as a technically demanding growth area, where seam sealing tapes are engineered to comply with EN 943 Type 3 and Type 5 standards for liquid-tight and dry particulate barrier protection.

Across manufacturing sectors, direct sales channels are, led by industrial OEMs and Tier 1 suppliers requiring bulk adhesive integration with automated production lines. This shift reflects the complexity of applications — from hot-melt polyurethane (TPU) and solvent-based adhesives for apparel to specialized water-based systems used in cleanroom garments and automotive interiors.

The multi-layer seam tape segment, especially three-layer constructions, remains the industry standard for extreme-wear and military-grade textiles, offering superior adhesion, tensile strength, and wash durability at temperatures up to 60°C. As the industry transitions toward PFAS-free, recyclable, and breathable tape formulations, the balance between environmental compliance and high-performance durability will be a decisive factor for manufacturers and buyers alike.

The Global Seam Sealing Tapes Industry is rapidly modernizing as sustainability, material substitution, and smart manufacturing technologies redefine product design and sourcing strategies. In March 2025, Ahlstrom completed the strategic repositioning of its Performance Materials division, following the acquisition of its Stevens Point operation. This repositioning strengthens its footprint in technical paper and nonwoven substrates, both essential to multi-layer adhesive constructions used in seam sealing tapes and protective laminates. Ahlstrom’s continued investment in sustainable material innovation reinforces the growing alignment between adhesive chemistry and substrate engineering for high-value textile applications.

In May 2025, Ahlstrom expanded production capacity with a new parchmentizer unit at its Saint-Séverin facility, directly supporting scalable manufacturing of release liners and nonwoven carrier films—key base materials in heat-sealed seam tapes. These moves coincide with growing end-user demand for custom-engineered tape systems tailored for medical protective garments, outdoor apparel, and industrial workwear.

Meanwhile, the technical apparel industry marked a major sustainability milestone in April 2025, when a leading global outdoor brand introduced its first PFAS-free rainwear collection, integrating non-fluorinated seam sealing technology. This move echoes a global trend: the shift toward fluorine-free waterproofing and low-VOC adhesives as brands aim to eliminate persistent chemicals from supply chains. The PFAS phase-out is a dominant driver of innovation in seam sealing materials across sportswear and military textile production.

The industrial and automotive segments also witnessed key advancements. In Q3 2024, a major European automotive supplier invested in ultrasonic welding and robotic heat-sealing technology, signaling a shift from traditional stitching toward automated bonding and moisture-control systems that depend on precision-engineered seam tapes. Concurrently, Ding Zing Advanced Materials Inc. (January 2025) launched biocompatible TPU films engineered for wearable devices and smart medical textiles, underscoring the convergence of adhesive science, comfort optimization, and bio-integration.

In the latter half of 2024, Bemis Associates Inc., a global pioneer in thermoplastic adhesive film technology, expanded its Sewfree® NET and WEB adhesive line, offering improved bond strength, stretch recovery, and breathability for high-performance activewear. This innovation strengthens the role of heat-activated adhesives in replacing conventional stitching, particularly in compression and aerodynamic sportswear.

However, the sector faces macro-level challenges such as tariff-induced raw material cost volatility (February 2025) affecting key adhesive inputs. Industry participants are reconfiguring supply chains to mitigate risk, particularly for solvent and TPU-based adhesives, which are critical for maintaining material consistency and production flow in apparel and medical protective wear. These developments indicate that the seam sealing tape industry’s competitive differentiation will increasingly hinge on process adaptability, eco-design, and performance consistency across diverse end-use environments.

Market Trend 1: Shift Toward Silicone-Based and Non-PU Hot Melt Tapes for Electric Vehicle Battery Safety

The accelerated electrification of the automotive industry is creating strong momentum for silicone-based seam sealing tapes engineered for EV battery pack assembly, replacing traditional polyurethane (PU) systems. As global automakers scale up lithium-ion battery production, the requirement for high-temperature stability, chemical resistance, and automated process compatibility is pushing the adoption of advanced adhesive tapes designed to perform under extreme operating conditions.

Thermal management has become a key differentiator for EV battery safety. Leading adhesive manufacturers have developed thermally conductive pressure-sensitive adhesive (PSA) tapes exhibiting conductivities up to 2 W/m·K, ensuring efficient heat transfer across the battery enclosure to maintain optimal cell temperatures (20–35°C). The dual-functionality—providing both adhesion and heat dissipation—minimizes overheating risks and extends battery life.

In addition, the industry is rapidly transitioning toward non-PU, silicone-based hot melts that comply with UL 94 V-0 flame-retardant standards, meeting stringent fire safety and sustainability requirements. These solvent-free, halogen-free materials reduce toxic emissions during processing while maintaining excellent electrical insulation and mechanical durability.

From a manufacturing perspective, reactive silicone hot-melt adhesives are becoming the preferred choice for EV gigafactories due to their immediate “green strength.” Once heated and dispensed, these adhesives solidify rapidly, enabling immediate handling and faster assembly cycles. The eliminates curing delays inherent to liquid sealants, significantly increasing line efficiency and throughput in high-volume EV battery manufacturing.

Market Trend 2: Rapid Reformulation Toward PFAS-Free and Bio-Based Waterproof Construction Membranes

The global regulatory crackdown on Per- and Polyfluoroalkyl Substances (PFAS) is accelerating the development of PFAS-free seam sealing tapes and bio-based waterproof membranes for the construction sector. With environmental policies tightening across North America, Europe, and Asia, manufacturers are under growing pressure to eliminate persistent “forever chemicals” from waterproofing and building envelope applications.

In 2025, a major global elastomer manufacturer announced it had eliminated PFAS surfactants from 98% of its fluorocarbon-based product range, achieving full performance equivalence through reformulation. The milestone proves that high-performance PFAS-free waterproofing tapes are technically feasible without compromising durability, adhesion, or weather resistance.

Simultaneously, bio-based polyurethane (BPU) membranes are gaining traction as sustainable waterproofing alternatives. Research data show BPUs achieving a water contact angle of 133.2° and hydrostatic resistance of 48.2 kPa, matching or exceeding petroleum-based products. These performance benchmarks validate the potential for renewable feedstock-based sealing tapes in demanding construction applications such as vapor barriers and roofing membranes.

Government regulations and green building incentives—such as the EU Energy Performance of Buildings Directive (EPBD)—are reinforcing the trend by requiring energy-efficient, low-emission materials. In response, architects are specifying vapor-permeable sealing tapes that regulate both air and moisture transfer, ensuring superior indoor environmental quality while enhancing building longevity.

Market Opportunity 1: Conductive and Thermally Efficient Tapes for EMI Shielding and Electronic Assembly

The growing convergence between thermal management and electromagnetic shielding is unlocking high-value growth opportunities for conductive seam sealing tapes in electronics and 5G infrastructure applications. As devices become smaller and operate at higher power densities, maintaining both electrical continuity and EMI protection has become essential.

Modern conductive foil and fabric-backed tapes with conductive PSAs can achieve shielding effectiveness (SE) levels of 60–70 dB, comparable to metallic enclosures while being lightweight and flexible. These materials ensure effective EMI suppression in communication equipment, base stations, and sensors while offering simplified installation over complex geometries.

In flexible electronics, single-sided conductive tapes are used to secure circuit components and stabilize grounding planes in flexible printed circuit boards (FPCBs), helping reduce RF noise and ensuring high signal integrity. The dual function—mechanical bonding and electrical grounding—supports the integration of miniaturized electronic systems with reduced weight and fewer assembly steps.

The adoption of conductive sealing tapes in automotive electronics and data centers also offers a significant manufacturing advantage. Their peel-and-stick application eliminates the need for heavy, space-consuming metal shielding components, streamlining assembly and improving overall device efficiency.

Market Opportunity 2: Advanced Breathable and Vapor-Permeable Tapes for Medical and Protective Garments

The rising demand for high-performance protective and medical apparel is fueling the development of breathable, vapor-permeable seam sealing tapes that balance protection and comfort. The trend is particularly evident in medical PPE, chemical suits, and extreme-weather gear, where tapes must ensure complete barrier protection while allowing controlled vapor transmission for thermal comfort.

In high-risk medical environments, tapes are engineered to achieve the ISO 16603 6/6 standard—the highest resistance rating against synthetic blood penetration—proving their suitability for infectious disease control. During the COVID-19 pandemic, heat-activated PPE sealing tapes meeting these standards became vital for ensuring safe and durable seam sealing across gowns and coveralls.

To enhance wearer comfort, recent innovations focus on moisture vapor transmission rate (MVTR) optimization. Research shows that while seam taping typically reduces fabric air permeability, modern vapor-permeable adhesives maintain a favorable microclimate by allowing controlled moisture escape without sacrificing waterproofing.

Additionally, specialized EVA antibacterial adhesive systems are being deployed to resist sterilization and chemical exposure from cleaning agents and autoclaving, ensuring long-term functionality and hygiene in medical garments. The evolution marks a crucial intersection between adhesive performance, human comfort, and biosafety, positioning vapor-permeable seam sealing tapes as indispensable in healthcare, defense, and technical textile applications.

Seam Sealing Tapes Market Share Insights, 2025-2034

Market Share by Product Type

Single-layered seam sealing tapes dominate the global market, accounting for approximately 62.6% share in 2025, owing to their cost-effectiveness, processing simplicity, and widespread suitability across apparel, footwear, and general waterproofing applications. These tapes are favored by manufacturers for their ease of heat application, lightweight nature, and high compatibility with commonly used fabrics such as nylon, polyester, and Gore-Tex. The continued expansion of the outdoor apparel, sportswear, and rainwear segments, particularly in Asia-Pacific manufacturing hubs like China, Vietnam, and Bangladesh, has significantly reinforced the dominance of single-layered tapes. Their excellent balance between performance and cost efficiency positions them as the go-to solution for most commercial-scale apparel and consumer goods applications.

Meanwhile, multi-layered seam sealing tapes maintain a substantial share, primarily driven by demand from high-performance industries such as defense, automotive, and protective clothing. These tapes offer superior bonding strength, enhanced flexibility, and advanced barrier properties against water, chemicals, and heat, making them indispensable for heavy-duty applications. Multi-layered seam tapes are also gaining traction in industrial protective garments, medical isolation suits, and specialty outerwear, where durability and compliance with international waterproofing standards (ISO, ASTM) are non-negotiable. As the market shifts toward technical textiles and performance-based products, the premium segment for multi-layered seam tapes is expected to expand, especially in Europe, Japan, and North America, where consumer expectations for quality and performance are driving innovation in seam-sealing technologies.

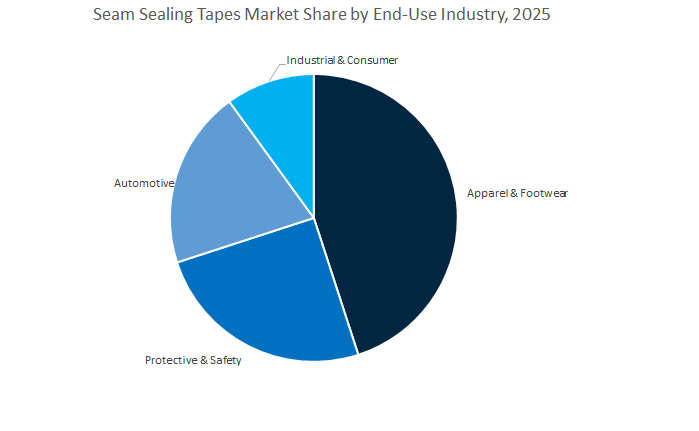

Market Share by End-Use Industry

Apparel & Footwear is the dominant end-use sector, capturing an estimated 47.9% share of the global seam sealing tapes market by 2025, fueled by the explosive growth of the outdoor apparel, athleisure, and functional footwear industries. Seam sealing is critical for ensuring waterproofing, wind resistance, and comfort in products such as jackets, ski wear, activewear, and performance shoes, where consumers demand high technical functionality. The global shift toward premium and performance-oriented textiles, combined with rising participation in outdoor recreation and sports, continues to bolster demand for seam sealing solutions. Major apparel brands are increasingly integrating eco-friendly polyurethane-based seam tapes that offer flexibility, breathability, and compliance with sustainability initiatives such as bluesign® and OEKO-TEX® certification.

The Protective & Safety segment represents the second-largest and one of the fastest-growing sectors, driven by increasing investments in industrial PPE, firefighting suits, military uniforms, and hazmat gear. Seam sealing in this category ensures chemical, fluid, and pathogen barriers, critical for worker and first-responder safety. Automotive applications are expanding rapidly as manufacturers use seam tapes in convertible roof systems, interior acoustic panels, and water barrier assemblies to improve vehicle sealing efficiency and passenger comfort. The Industrial & Consumer segment, though smaller, showcases steady demand across marine, camping, and outdoor equipment manufacturing, where waterproofing performance remains a key design requirement.

The Global Seam Sealing Tapes Market is led by Bemis Associates Inc., Sealon Inc., Ding Zing Advanced Materials Inc., Gerlinger Industries GmbH, and 3M Company—each offering distinct technological strengths across adhesive chemistry, material processing, and application engineering. These players are spearheading the global shift toward sustainable, multifunctional, and high-performance seam sealing technologies.

Bemis Associates remains the market leader in heat-activated adhesive films and seam tapes. Its Sewfree® bonding technology eliminates stitching while maintaining waterproofing, breathability, and flexibility, serving brands in performance apparel, footwear, and wearables. The company provides end-to-end services, including trend research, prototyping, and substrate compatibility testing under its "Sewfree® Ecosystem." Its RS4500 Reflective Stretch Embellishment Films integrate visibility enhancement with durable waterproof bonding, while new 3-layer seam tapes ensure structural integrity in extreme-weather garments. Bemis continues to set the global benchmark for textile bonding innovation.

Sealon Inc. distinguishes itself through its OEKO-TEX STANDARD 100® and bluesign® certified production, offering PFAS-free seam tapes for premium outdoor and protective wear. Its advanced adhesive films enhance garment flexibility, ensuring seamless integration into stretch and activewear fabrics. In 2025, Sealon introduced a new line of anti-microbial and anti-viral tapes addressing the medical and protective apparel market, reinforcing its dual focus on functionality and sustainability. As consumer demand pivots toward eco-friendly textile solutions, Sealon’s ethical manufacturing standards make it a preferred supplier for environmentally responsible brands.

Ding Zing is an innovation-driven leader specializing in TPU-based seam sealing materials, focusing on lightweight, elastic, and high-strength films for technical, medical, and industrial applications. Its “Innovation Playground” R&D model fosters cross-disciplinary collaboration to create next-generation biocompatible, flexible, and recyclable TPU products. The firm’s ongoing expansion into bio-based TPU systems aligns with circular economy principles, enabling manufacturers to reduce the environmental footprint of waterproof textiles and wearable technologies while maintaining durability under harsh conditions.

Gerlinger Industries GmbH combines 5-layer co-extrusion technology with advanced adhesive chemistry to produce breathable and UV-resistant seam sealing tapes for industrial protective gear, military clothing, and high-performance outdoor textiles. Its multi-layer systems deliver high tensile strength and abrasion resistance even after repeated industrial laundering. Gerlinger’s products support cross-seam sealing and ensure moisture permeability, maintaining garment breathability. The company’s expertise in custom co-extrusion and hot-melt film engineering reinforces its status as a key European supplier for functional textile applications.

3M Company brings its vast adhesive and material science expertise to the seam sealing market, supplying specialized tapes for aerospace, medical, and industrial use. Its products meet high-pressure, flammability, and abrasion-resistance standards, making them indispensable for aerospace insulation blankets, HVAC duct sealing, and automotive interiors. Leveraging one of the world’s largest patent portfolios in adhesive materials, 3M offers customized bonding solutions that ensure structural integrity and compliance with stringent industry safety norms. Its integration of seam sealing with performance coatings exemplifies 3M’s leadership in applied materials engineering.

Country Analysis: Global Seam Sealing Tapes Industry – Regional Manufacturing, Innovation, and Regulatory Trends

China: Industrial Expansion and Technical Textile Innovation Fueling Seam Sealing Tape Growth

China dominates the global Seam Sealing Tapes market, driven by technical textile expansion, protective clothing manufacturing, and rapid automotive growth. The government’s commitment to upgrading industrial capability through the Amended Technology Upgradation Fund Scheme (ATUFS) and similar modernization initiatives has accelerated domestic production of advanced seam sealing tapes for waterproof and breathable garments. The enforcement of the GB/T 32614-2023 standard for outdoor sportswear sets new benchmarks for water resistance and breathability, reinforcing demand for polyurethane (PU) and thermoplastic polyurethane (TPU) seam tapes in technical apparel and outdoor wear manufacturing.

China’s leadership as the world’s largest PPE producer has sustained exceptionally high consumption of chemical- and heat-resistant seam tapes for protective suits and healthcare applications. Manufacturers such as Jiangmen M.F.B.S. Machinery are expanding production capacity and export networks to serve the increasing demand for multi-layer seam tapes in industrial and military-grade garments. Additionally, China’s projected automotive output of 35 million units by 2025 creates new opportunities for moisture-resistant seam sealing tapes in vehicle interiors, wire harnessing, and insulation components. The rising domestic outdoor apparel industry, backed by the booming sportswear segment, is fueling R&D in flexible, lightweight TPU tapes that balance comfort, adhesion, and durability — reinforcing China’s strategic dominance in both industrial and consumer seam tape applications.

United States: Sustainable and High-Performance Seam Sealing Tapes for Specialty Applications

The United States seam sealing tapes market is driven by innovation in high-performance adhesives, stringent PFAS regulatory oversight, and rapid adoption in technical and defense-grade textiles. Major adhesive leaders, including 3M Company and Bemis Associates Inc., are investing heavily in reactive hot melt and eco-friendly polyurethane-based seam sealing technologies. In 2023, 3M launched a reactive hot melt adhesive system for electronics and wearable devices, enhancing moisture and heat resistance — a technology that is now influencing smart fabric and wearable textile tape formulations.

The U.S. Department of Defense continues to drive demand for flame-resistant polyamide and polyester seam sealing tapes used in tactical, combat, and field uniforms. Simultaneously, state-level PFAS restrictions, such as Washington’s 2024 draft rulings on apparel chemicals, are compelling manufacturers to develop bio-based, solvent-free seam tape alternatives. Companies like Adhesive Films Inc. are leading efforts to customize multi-layered seam sealing films for medical devices, industrial equipment, and waterproof apparel. The country’s outdoor recreation industry, worth over USD 1 trillion, supports the growing market for UV-stable and abrasion-resistant seam tapes for tents, backpacks, and outdoor protective gear. With continued investment in sustainable adhesive technologies and a clear regulatory roadmap, the U.S. remains a front-runner in eco-innovation and specialty adhesive manufacturing.

Germany: Engineering Precision and Sustainable Material Development in Seam Sealing Applications

Germany serves as a European hub for advanced engineering and high-performance adhesive systems, with a strong focus on automotive, construction, and technical textile sectors. Henkel AG & Co. KGaA’s acquisition of Seal for Life Group (February 2024) expanded its product portfolio to include advanced corrosion prevention and sealing systems, enabling integration of high-performance hot melt seam tapes for industrial and infrastructure use. The company’s partnership with Kraton Corporation (March 2024) underscores a national trend toward bio-based polymers and sustainable adhesive technologies in construction and textile applications.

The automotive sector, a key pillar of Germany’s economy, relies heavily on moisture- and heat-resistant polyurethane seam tapes for internal bonding, acoustic sealing, and water ingress control in premium vehicles. Furthermore, EU-driven sustainability mandates have encouraged R&D investment in low-VOC, solvent-free, and recyclable tape formulations by companies like Gerlinger Industries GmbH. Germany’s established leadership in technical textiles and protective apparel is boosting demand for three-layer seam sealing systems that combine waterproofing and breathability, crucial for professional uniforms, medical fabrics, and outdoor gear. The synergy between engineering precision, green chemistry, and advanced material science solidifies Germany’s role as Europe’s center of excellence for high-end seam sealing tapes.

India: Expanding Technical Textile Infrastructure and Domestic Seam Sealing Production

India’s seam sealing tapes industry is growing rapidly, driven by government-backed textile modernization, export-oriented garment production, and large-scale infrastructure development. The Production-Linked Incentive (PLI) Scheme for Textiles, with an outlay of INR 10,683 crore, and the PM-MITRA Park initiative are enabling large-scale investments in technical textile clusters, positioning India as a key global supplier of waterproof and performance apparel. As one of the top three global textile exporters (USD 37 billion in 2024), India’s apparel and technical fabric producers increasingly demand export-grade seam sealing tapes that meet European and North American performance standards.

Local adhesive producers like San Chemicals Ltd. are expanding product lines to include PU- and TPU-based seam tapes for applications in medical PPE, military gear, and outdoor apparel. Simultaneously, the nation’s growing infrastructure projects and industrial manufacturing base are fueling the use of heavy-duty seam sealing tapes in geomembranes, moisture barriers, and construction sheeting. With the integration of advanced production technologies and the government’s continued investment in modern textile infrastructure, India is quickly evolving from a cost-competitive producer to a regional hub for high-quality, globally certified seam sealing materials.

Japan: Pioneering Polymer Innovation and Ultra-Precision Seam Tape Manufacturing

Japan stands at the forefront of precision-engineered seam sealing technologies, driven by advanced polymer science, rigorous quality standards, and integration with smart textile systems. Industry leaders like Toray Industries Inc. are continuously advancing polyurethane and copolymer-based seam sealing solutions that deliver superior elasticity, adhesion, and waterproof performance. Meanwhile, Toyobo Co. Ltd. has pioneered biaxially oriented polypropylene (BOPP) films, offering enhanced dimensional stability and durability for next-generation technical and outdoor seam tapes.

Japan’s focus on ultra-high-quality, non-peeling performance has made it a global benchmark for multi-layered seam sealing tapes used in premium sportswear, outerwear, and mountaineering gear. Additionally, the growing wearable electronics market is encouraging the development of ultra-thin, flexible seam tapes capable of integrating sensors and conductive fibers. Japanese manufacturers’ relentless pursuit of precision, combined with their deep R&D expertise, ensures the continued dominance of Japanese seam sealing tapes in high-value, performance-critical applications.

South Korea: High-Elasticity Seam Tapes Powering Sportswear and Smart Manufacturing Growth

South Korea has established itself as a major global supplier of high-durability, stretchable seam sealing tapes, catering primarily to the sportswear, outdoor apparel, and industrial workwear segments. Leading manufacturers like Sealon Co., Ltd. and Himel Corp. have positioned the country as a specialized production base for heat-activated and pressure-bonded polyurethane seam sealing films, widely used in jackets, footwear, and technical uniforms.

Beyond textiles, South Korea’s high-tech sectors—notably automotive and consumer electronics—drive the use of precision adhesive tapes and sealing films that can endure extreme temperature, chemical, and humidity cycles. Korean companies are increasingly investing in abrasion- and impact-resistant formulations, aligning with the growing domestic demand for protective gear and industrial safety wear. The nation’s continued integration of smart manufacturing technologies and focus on export-oriented product innovation ensure South Korea’s enduring position as a global hub for advanced seam sealing solutions across apparel, electronics, and engineering applications.

Seam Sealing Tapes Market Report Scope

Seam Sealing Tapes Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$334.7 Million

|

|

Market Size (2034)

|

$620.5 Million

|

|

Market Growth Rate

|

7.1%

|

|

Segments

|

By Product Type (Single-layered, Multi-layered), By Backing Material (Polyurethane, Thermoplastic Polyurethane, Polyvinyl Chloride, Polyamide, Polyester), By Application Method (Hot Melt, Solvent-Based, Water-Based/Waterborne), By End-Use Industry (Apparel & Footwear, Protective & Safety, Automotive, Industrial & Consumer

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Bemis Associates Inc., 3M Company, Toray Industries Inc., Henkel AG & Co. KGaA, Sealon Co., Ltd., Himel Corp., DingZing Advanced Materials Inc., Gerlinger Industries GmbH, Loxy AS, Adhesive Films, Inc., San Chemicals, Ltd., Essentra PLC, Ardmel Automation, Vetex, H.B. Fuller

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Product Type

- Single-layered

- Multi-layered

By Backing Material/Composition

- Polyurethane

- Thermoplastic Polyurethane

- Polyvinyl Chloride

- Polyamide

- Polyester

By Application Method

- Hot Melt

- Solvent-Based

- Water-Based/Waterborne

By End-Use Industry

- Apparel & Footwear

- Protective & Safety

- Automotive

- Industrial & Consumer

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Seam Sealing Tapes Market

- Bemis Associates Inc.

- 3M Company

- Toray Industries Inc.

- Henkel AG & Co. KGaA

- Sealon Co., Ltd.

- Himel Corp.

- DingZing Advanced Materials Inc.

- Gerlinger Industries GmbH

- Loxy AS

- Adhesive Films, Inc.

- San Chemicals, Ltd.

- Essentra PLC

- Ardmel Automation

- Vetex

- H.B. Fuller

*- List not Exhaustive

Research Coverage

Prepared by USDAnalytics, this report investigates the Global Seam Sealing Tapes Market across demand drivers, manufacturing shifts, and end-use performance requirements; our analysis reviews PFAS-free breakthroughs in waterproofing science, advances in TPU/PU film engineering, and automation-ready hot-melt processes for apparel, medical PPE, industrial fabrics, and mobility interiors; it highlights how hydrostatic pressure thresholds, wash durability, and breathability targets intersect with brand sustainability roadmaps and regulatory change, mapping specification trends from single-layer utility tapes to multi-layer military-grade systems and EV-ready thermal solutions—this report is an essential resource for product managers, sourcing leaders, and technical designers seeking defensible insights to guide portfolio strategy, qualification, and 2025–2034 planning.

Scope Highlights

Segmentation:

- By Product Type: Single-layered; Multi-layered.

- By Backing Material/Composition: Polyurethane; Thermoplastic Polyurethane; Polyvinyl Chloride; Polyamide; Polyester.

- By Application Method: Hot Melt; Solvent-Based; Water-Based/Waterborne.

- By End-Use Industry: Apparel & Footwear; Protective & Safety; Automotive; Industrial & Consumer.

- By Region: North America (United States, Canada, Mexico); Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe); Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC); South & Central America (Brazil, Argentina, Rest of SCA); Middle East & Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa).

Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

Time Horizon: Historic data 2021–2024 and forecast data 2025–2034.

Companies Covered: Analysis / profiles of 15+ companies.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.