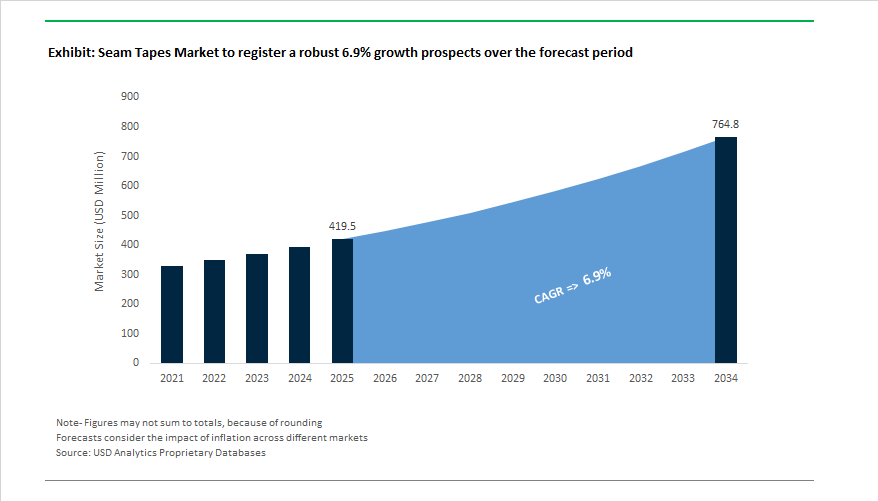

The Global Seam Tapes Market is projected to grow from $419.5 million in 2025 to $764.8 million by 2034, expanding at a CAGR of 6.9%. This market serves as a cornerstone of the global waterproofing and bonding ecosystem, bridging the textile, construction, automotive, and protective apparel industries. Seam tapes are critical to ensuring the structural integrity and waterproof performance of garments, industrial fabrics, and sealing systems, particularly in sectors where high mechanical stress, chemical resistance, and long-term durability are essential.

Over 90% of high-performance outdoor apparel globally relies on polyurethane (PU) and thermoplastic polyurethane (TPU) seam tapes, as these materials provide elasticity, hydrostatic pressure resistance, and superior adhesion under fluctuating temperatures. The sportswear and all-weather clothing segments, including hiking, skiing, and mountaineering gear, dominate this demand. In parallel, protective clothing and personal protective equipment (PPE) applications have surged following updates to EN 14325:2018, which mandates minimum seam strength and permeation resistance levels. This regulatory shift has increased the use of chemically resistant, multi-layer seam sealing systems in medical, chemical, and industrial safety apparel.

A major shift toward bio-based materials is underway, with leading global producers introducing tapes made from renewable polymers and sustainable paper backings — such as a recently launched 92% bio-based carbon paper tape certified by DIN CERTCO. This trend signals the future direction of the broader adhesive and seam sealing industry, where sustainability and recyclability are becoming decisive purchasing criteria.

Additionally, industrial use cases are expanding rapidly. Asia-Pacific manufacturers, particularly in Indonesia and China, are investing heavily in sealing systems for construction waterproofing, façade protection, and roofing applications, underscoring the crossover potential of seam tape technologies into urban infrastructure and industrial sealing. The evolution of multi-layer seam tapes—offering improved abrasion resistance, flexibility, and tensile strength—positions the sector for accelerated growth across multiple high-value verticals.

The Seam Tapes Industry is entering a period of strategic convergence between performance innovation, material sustainability, and cross-industry applications. In October 2025, Toray Industries, Inc. announced its participation in the Hydrogen Technology World Expo, signaling an expansion of its material science R&D toward advanced sealing and bonding materials used in next-generation energy systems. This move demonstrates how polymer innovation in textiles often transfers into industrial applications such as hydrogen storage, automotive fuel cells, and pressure-sealed environments — sectors requiring advanced seam tape functionality.

In September 2025, Ahlstrom strengthened its foothold in life sciences and protective textiles through the acquisition of EBF, a strategic expansion that enhances its portfolio in specimen collection materials and medical nonwovens. This acquisition reinforces Ahlstrom’s commitment to precision-engineered substrates—a category vital to medical seam tape applications where sterility, adhesion stability, and barrier integrity are non-negotiable. Further underlining its material leadership, Ahlstrom introduced a flame-resistant facer in August 2025, suitable for integration with fire-retardant seam tapes in construction safety assemblies, HVAC duct insulation, and façade systems compliant with EU fire safety codes.

The construction segment continues to emerge as a key growth driver. In April 2025, Sika AG opened a new production facility in Ust-Kamenogorsk, Kazakhstan, expanding its mortar and concrete admixtures production capacity to support sealing, waterproofing, and bonding solutions across Eurasia. Shortly after, in March 2025, BASF and Sika collaborated to launch a sustainable epoxy hardener system aimed at reducing VOC emissions, setting a new environmental benchmark for adhesive formulations used in structural and industrial sealing—technologies closely aligned with the chemistry of modern seam tapes.

Sustainability trends continue to reshape adhesive formulations. In December 2024, Tesa SE unveiled its tesa® 60408 bio-based paper tape, containing 92% bio-based carbon, reinforcing the industry’s focus on renewable feedstocks and eco-friendly adhesive systems. These bio-based advancements are expected to migrate into seam tape and textile sealing products, aligning with the global movement toward PFAS-free waterproofing and recyclable materials in sportswear and protective equipment manufacturing.

Simultaneously, Toray’s TORAIN™ fabric line (September 2024)—integrating proprietary waterproof membranes and seam tape systems—continues to define the premium technical apparel market, particularly in Japan and Europe. Toray’s fully integrated production chain, encompassing everything from polymer synthesis to finished apparel, exemplifies the next phase of closed-loop textile innovation, where adhesive and membrane technologies are engineered simultaneously for optimal compatibility.

Financially, the sector remains robust. Sika AG’s integration of MBCC Group (January 2025) is expected to generate CHF 180–200 million in synergies by 2026, bolstering its leadership across the global bonding and sealing ecosystem.

Market Trend 1: Rapid Adoption of Thermoplastic Polyurethane (TPU) Films for High-Frequency and Ultrasonic Welding in Technical Textiles

The demand for high-seam integrity, durability, and chemical-free bonding in technical textiles is propelling the adoption of Thermoplastic Polyurethane (TPU) films as an advanced alternative to conventional chemical seam tapes. The transition aligns with manufacturers’ need for higher productivity, eco-efficiency, and compliance with stringent cleanroom and sterility standards—particularly in sectors like medical devices, outdoor apparel, and industrial inflatables.

Recent patent data from a global material technology firm reported a continuous extrusion and welding process using TPU film layers, designed for sterile coverings in surgical robotics. The seamless tubular form eliminates traditional stitched or adhesive seams, ensuring superior sterility and mechanical durability—a major leap forward in medical textile seam sealing innovation.

In industrial-scale performance testing, 0.31 mm TPU films welded using ultrasonic rotary machines exhibited enhanced waterproofing and airtightness, outperforming stitched seams and solvent-based tapes in tensile strength and hydrostatic resistance. The empirical data validates TPU’s role as a high-strength seam sealing material for critical applications like protective clothing, marine gear, and inflatable structures, where seam failure poses significant safety and economic risks.

Further, High-Frequency (HF) Welding technology is emerging as a leading manufacturing process for TPU film seam integration. By stimulating molecular vibration under an electromagnetic field, HF welding achieves precise molecular-level fusion—delivering cleaner seams, lower waste, and higher repeatability in mass production. As industries like outdoor gear, hydration systems, and footwear continue to prioritize performance and durability, TPU film seam tapes are fast becoming the standard in advanced textile bonding.

Market Trend 2: Reformulation to Eliminate PFAS and Phthalates Amid Intensified Global Regulation

The global campaign against hazardous substances, notably PFAS (“forever chemicals”) and phthalates, is compelling the Seam Tapes Industry to undergo one of its most significant chemical reformulations in decades. Heightened consumer scrutiny, coupled with aggressive regulatory and corporate ESG mandates, is pushing material suppliers toward fully PFAS-Free and Phthalate-Free adhesive and film systems that ensure safety, compliance, and long-term brand viability.

A landmark corporate decision announced in late 2022 by a leading global chemical manufacturer to exit all PFAS production and usage by 2025 marked a turning point for the global sealing materials supply chain. The industry-wide pivot has forced outdoor apparel and technical textile brands to rapidly requalify suppliers capable of delivering equivalent PFAS-Free waterproof seam tapes with comparable chemical and temperature resistance.

In parallel, under EU REACH regulations, the cumulative restriction of the four key phthalates—DEHP, BBP, DBP, and DIBP—to concentrations below 0.1% in plastics has redefined formulation standards for all textile adhesives and coatings. The mandates new non-phthalate plasticizer systems, especially in apparel and footwear applications, ensuring compliance with consumer safety standards and Green Label Certification programs.

The trend is further reinforced by policy precedents such as the U.S. FDA’s 2025 phase-out of PFAS-based grease-proofing agents, signaling a future wave of restrictions targeting human-contact materials like performance apparel and footwear membranes. Consequently, material R&D is focused on bio-derived plasticizers, siliconized polyolefins, and alternative fluorine-free hydrophobics, enabling manufacturers to meet sustainability targets while maintaining high-performance adhesion and seam protection.

Market Opportunity 1: Development of Phase Change Material (PCM)-Integrated Seam Tapes for Adaptive Thermal Regulation

The next generation of performance wear and technical garments is being defined by active temperature regulation, creating a lucrative opportunity for Phase Change Material (PCM)-integrated seam tapes. These functional tapes not only seal fabric joints but also enhance wearer comfort by storing and releasing thermal energy, effectively transforming seams into dynamic thermal management systems.

Scientific studies demonstrate that PCM-embedded textiles can reduce internal temperature fluctuations by approximately 30%, offering measurable thermal stabilization across varying environmental conditions. The makes PCM-enhanced seam tapes particularly relevant for workwear, military uniforms, sportswear, and medical garments, where maintaining thermal equilibrium is vital.

R&D advancements in microencapsulation technology allow PCMs to be embedded directly into the polymer or adhesive matrix of seam tapes. The technique ensures phase change cycles occur without leakage or mechanical degradation, enabling long-term durability under repeated thermal cycling. The seamless integration of PCMs within the adhesive layer or film substrate provides a platform for adaptive, comfort-optimized textiles that combine sealing, insulation, and energy buffering in a single component.

Market Opportunity 2: Electrically Conductive Seam Tapes for Smart Garments and Wearable Data Systems

The convergence of wearable electronics and advanced textiles is opening a high-growth opportunity for electrically conductive seam tapes, designed to serve as flexible electrical interconnects that maintain structural integrity and wash durability. As smart apparel integrates heating, sensing, and communication functionalities, seam tapes are emerging as invisible wiring systems—enabling power and data transmission while preserving garment comfort and flexibility.

Studies in smart e-textile design have identified interconnects as the most common failure points due to stress, folding, and laundering. Conductive seam tapes address the challenge by embedding conductive fillers such as carbon nanotubes (CNTs), silver nanowires, or conductive polymers within the adhesive or film matrix. These materials deliver conductivities between 10⁶ and 10⁷ S/m, ensuring stable electrical performance for low-voltage heating or sensor signal transmission.

Unlike traditional soldered or stitched circuits, seam-integrated conductive adhesives offer superior flexibility, abrasion resistance, and water resilience, making them ideal for smart uniforms, medical monitoring garments, and outdoor wearables. Additionally, the seamless bonding process reduces weight, enhances aesthetic appeal, and supports scalable manufacturing for next-generation wearable electronics.

Seam Tapes Market Share Insights, 2025-2034

Market Share by Type

Single-layered seam tapes hold a commanding 66.2% share of the global seam tapes market in 2025, underscoring their dominance as the preferred choice across the apparel, footwear, and general-purpose waterproofing sectors. Their widespread adoption is primarily attributed to cost efficiency, ease of application, and compatibility with various fabrics such as nylon, polyester, and polyurethane-coated textiles. Single-layer tapes offer reliable waterproofing and durability for standard use cases, making them indispensable in outdoor apparel, sportswear, and consumer goods manufacturing. The growing demand for lightweight and flexible waterproof materials in the global textile industry further strengthens the segment’s leadership. In addition, continuous advancements in thermoplastic polyurethane (TPU)-based single-layer tapes have improved adhesion, flexibility, and eco-compliance, aligning with the industry’s move toward sustainable manufacturing practices.

On the other hand, multi-layered seam tapes cater to the high-performance and technical segment of the market, where superior waterproofing, thermal stability, and mechanical strength are critical. These tapes, often designed with two- or three-layer constructions, are gaining popularity in specialized applications such as defense gear, extreme weather apparel, industrial protective suits, and advanced outdoor equipment. Their higher cost is justified by their ability to withstand harsh environmental conditions and repeated wash cycles, offering extended product life and reliability. As premium apparel brands and safety gear manufacturers increasingly focus on performance differentiation, the demand for multi-layered seam tapes is expected to rise steadily.

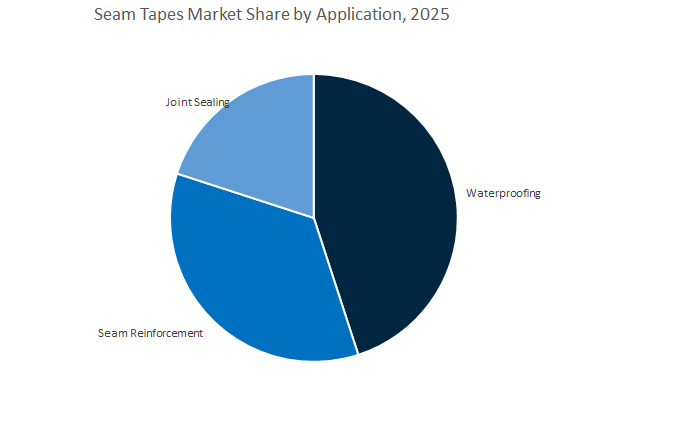

Market Share by Application

Waterproofing applications dominate the global seam tapes industry, capturing 45.7% of the market share in 2025, driven by the rapidly expanding outdoor, sportswear, and protective apparel sectors. Seam tapes are essential in ensuring garment waterproofing performance by sealing stitch holes, preventing leakage, and maintaining the garment’s integrity under wet or humid conditions. Their adoption has grown significantly alongside consumer demand for functional clothing that combines comfort, style, and weather protection. Manufacturers in the apparel and footwear industries rely heavily on waterproof seam tapes to achieve international waterproofing standards, such as ISO 811 and JIS L 1092, ensuring global compliance and premium product positioning. Furthermore, the rising production of eco-friendly breathable membranes and laminates continues to drive the need for compatible high-performance waterproofing seam tapes.

Seam reinforcement remains a strong and stable application segment, crucial in technical textiles, automotive interiors, and heavy-duty industrial fabrics. In these applications, seam tapes enhance mechanical strength, abrasion resistance, and load-bearing capacity at stress points, particularly in seat covers, industrial tarpaulins, and upholstery materials. Meanwhile, joint sealing applications represent a growing segment, driven by their increasing use in construction membranes, automotive assembly, and marine equipment where strong adhesion and long-term resistance to temperature and moisture are vital. The application mix within the global seam tapes market highlights the dual importance of functional performance (waterproofing) and structural reinforcement (seam and joint sealing) across a diverse range of industries.

The Global Seam Tapes Market is defined by a blend of technological depth, manufacturing integration, and sustainability leadership. The following key players—Sika AG, Toray Industries, Tesa SE, Bemis Associates Inc., and Himel Material Technology Co., Ltd.—are leading innovation across their respective niches, collectively shaping the evolution of bonding and sealing solutions for textiles, construction, and industrial systems.

Sika AG continues to dominate the global bonding and sealing ecosystem, leveraging its deep expertise in polymer science, construction chemistry, and waterproofing systems. Its focus on high-growth verticals such as data centers, mining infrastructure, and façade sealing underpins its strong industrial base. With new plants opened in Peru, China, and Kazakhstan (2024–2025), Sika enhances its regional supply capabilities. The acquisition of Kwik Bond Polymers (October 2024) reinforces its expertise in bridge deck and public works sealing, while SBTi validation (July 2024) confirms its commitment to achieving net-zero emissions by 2050—a critical advantage in sustainable construction chemistry.

Toray Industries operates one of the world’s most vertically integrated textile ecosystems, from polymer synthesis (nylon, polyester) to finished apparel, enabling total control over seam sealing quality and performance. Its TORAIN™ all-weather apparel exemplifies the fusion of breathable waterproof membranes and precision-engineered seam tapes for professional and recreational use. Beyond apparel, Toray’s expansion into infection-control textiles and wearable smart fabrics positions it at the forefront of functional and responsive material design, critical for next-generation seam sealing technologies across medical and industrial markets.

Tesa SE, a subsidiary of Beiersdorf AG, leads the European market in industrial-grade adhesive and specialty tapes. With a clear focus on sustainable product innovation, Tesa’s bio-based paper tape (tesa® 60408) has set a new benchmark for renewable adhesive materials. Its engineering excellence spans thermal management and high-voltage insulation tapes used in EV and industrial systems, many of which overlap with high-heat seam sealing applications. By aligning with EU eco-design regulations, Tesa reinforces its leadership in low-emission, recyclable tape technologies, offering critical insight into the future of bio-based adhesive evolution.

Bemis Associates remains a technological leader in thermoplastic films and hot-melt adhesives, defining the performance apparel bonding landscape. Its flagship Sewfree® and Flow-Coat film systems deliver stretchable, breathable, and waterproof sealing for next-generation athletic wear and soft goods. By integrating flow control and substrate-specific adhesion science, Bemis ensures unmatched seam durability without compromising garment comfort. Its growing focus on lightweight and recyclable materials aligns with global apparel sustainability trends, positioning the company as a critical enabler of PFAS-free and stitchless textile design.

Himel Material Technology, headquartered in China, has rapidly emerged as a high-volume producer of PU and TPU seam sealing tapes for outerwear, tents, rainwear, and technical workwear. The company emphasizes formulation flexibility, excellent wash durability, and enhanced softness, addressing the tactile and functional needs of the apparel industry. With expanding production capabilities in Asia-Pacific, Himel delivers cost-effective, high-performance sealing solutions to global brands seeking dependable quality and rapid supply. Its ongoing R&D focus on lightweight TPU compounds aligns with the region’s sustainability drive and increasing demand for low-VOC, flexible bonding materials.

Country Analysis: Strategic Developments and Manufacturing Dynamics in the Global Seam Tapes Industry

United States: Digital Integration and Sustainable Innovation Reshaping Seam Tape Manufacturing

The United States seam tapes industry is witnessing strong momentum in product innovation, digital transformation, and sustainability, driven by global apparel brands’ need for efficiency and eco-friendly solutions. In May 2024, Bemis Associates Inc., one of the leading U.S. manufacturers of thermoplastic films, adhesive products, and seam tapes, partnered with Optitex to digitize its product offerings. The collaboration introduced a new 3D Digital Material Library, integrating Bemis’ advanced seam reinforcement tapes, Sewfree® adhesives, and embellishments into virtual product creation (DPC) workflows for apparel and technical textiles. The move significantly reduces design lead times and material wastage while enhancing precision for performance brands in outdoor and sportswear segments.

Sustainability continues to define Bemis’s innovation roadmap, with the company emphasizing eco-friendly seam tapes manufactured from recycled materials that cater to growing environmental mandates and brand circularity commitments. Demand for seam tapes for water-resistant and stretch fabrics remains robust across high-value industries like protective apparel, military gear, and luxury activewear, where thermoplastic polyurethane (TPU) and polyamide-based tapes dominate due to their elasticity, durability, and chemical stability. As U.S. manufacturers move toward low-VOC, solvent-free formulations, the country continues to play a leading role in advancing sustainable adhesive technologies for technical textiles and fashion innovation.

Japan: Precision Engineering and Advanced Polymer Chemistry Driving Seam Tape Excellence

Japan stands as a center of excellence in advanced materials and polymer chemistry, shaping the development of high-performance multi-layer seam sealing tapes. Toray Industries, Inc., a global leader in polymer-based innovation, is at the forefront of developing synthetic organic and high-purity polymer materials integral to technical seam tape manufacturing. The company’s technological breakthroughs in polyimide products, water treatment membranes, and hybrid bonding materials have direct implications for next-generation seam sealing applications, particularly those involving electronic textiles, performance outerwear, and industrial protective clothing.

Japan’s R&D focus on film precision, flexibility, and temperature resistance ensures its continued dominance in premium-grade seam tapes for sportswear, aerospace uniforms, and high-performance outerwear. The nation’s meticulous production standards and leadership in high-spec polyurethane (PU) films and elastomeric materials have positioned its seam tapes as benchmarks for durability, peel resistance, and uniform bonding integrity. Moreover, Japan’s integration of electronic components and smart textiles opens pathways for sensor-embedded, conductive seam sealing technologies, reinforcing its role as a global innovator in functional and performance-based adhesives.

South Korea: Strengthening Regional Production and Advancing Protective Apparel Tapes

South Korea’s seam tapes industry has evolved into a global powerhouse in protective apparel, industrial workwear, and sportswear applications. Major domestic players, such as Himel Corp. (HiMEL) and Sealon Co., Ltd., are expanding production and regional influence. In September 2024, HiMEL inaugurated a 25,000-square-meter manufacturing facility in Vietnam, aimed at meeting the surging Asia-Pacific demand for 2-layer and 3-layer waterproof seam tapes used in activewear, performance apparel, and footwear.

Korean manufacturers are also advancing the field of heat-sealable seam tapes engineered for chemical-resistant, leakproof, and airtight protective clothing used in construction, mining, and hazardous material handling. R&D centers in the region are heavily investing in enhanced durability and elongation performance, ensuring compliance with ISO and EN 343 waterproofing standards for industrial apparel. South Korea’s emphasis on innovation, lightweight materials, and high-stretch thermoplastic adhesives reinforces its position as a global hub for technical textile reinforcement tapes, bridging high-volume production with cutting-edge engineering.

Taiwan: Global Leadership in Thermoplastic Polyurethane (TPU) Films and Sustainable Materials

Taiwan has established itself as a key manufacturing and innovation hub for TPU-based seam sealing materials, underpinned by companies like DingZing Advanced Materials Inc. Known for its mastery in thermoplastic polyurethane film and composite materials, DingZing continues to lead in producing environmentally responsible, high-performance TPU films that form the foundation for premium-grade seam sealing tapes. The films offer exceptional elasticity, abrasion resistance, and waterproof bonding, making them ideal for outdoor gear, technical textiles, and medical applications.

Taiwanese manufacturers are focusing on versatility and sustainability, introducing TPU materials as eco-friendly alternatives to conventional PVC-based adhesives. Their seam tapes are specifically designed for multi-directional stress environments, ensuring consistent performance in activewear, footwear, and industrial safety clothing. As Taiwan deepens its expertise in flexible films and composite bonding systems, the country remains integral to the global supply chain of lightweight, high-strength, and sustainable seam sealing materials.

Germany: European Hub for Technical Textiles and High-Performance Seam Sealing Systems

Germany remains a leader in the European technical textiles and specialty adhesives market, with a strong focus on industrial, automotive, and protective textile applications. Companies such as Gerlinger Industries GmbH spearhead advancements in heat-sealable seam tapes designed for high-performance textile bonding and waterproofing systems. The country’s adherence to stringent EU environmental and fire protection regulations drives the development of low-VOC, halogen-free seam tapes that meet safety and sustainability standards under frameworks like REACH and the European Green Deal.

Germany’s robust automotive and construction sectors further stimulate demand for polyurethane and hot melt adhesive tapes used for moisture control, vibration damping, and seam reinforcement in complex assemblies. Meanwhile, the continued expansion of the technical textile sector—which supplies materials for professional workwear, outdoor apparel, and medical garments—strengthens the nation’s leadership in specialized seam sealing technologies. Through its emphasis on engineering precision, circular material innovation, and industrial automation, Germany stands as the benchmark for premium, eco-conscious seam sealing tape manufacturing in Europe.

China: Industrial Expansion and Diverse Seam Tape Applications Across Sectors

China continues to dominate the global seam tapes market as both a mass producer and key innovator in performance wear, footwear, and industrial applications. The nation’s expansive textile and apparel manufacturing base ensures massive internal demand for polyurethane, TPU, and PVC seam tapes, particularly in outdoor sportswear, protective clothing, and fashion manufacturing. Domestic brands investing in high-performance outdoor and athletic wear are driving rapid adoption of waterproof, breathable, and stretchable seam sealing tapes to meet international performance standards.

Beyond textiles, China’s ongoing infrastructure boom and rapid electrification are expanding the use of industrial-grade seam sealing tapes across roofing, HVAC systems, and electrical insulation. The government’s emphasis on energy-efficient construction and green manufacturing is spurring growth in low-VOC, flame-retardant, and recyclable sealing materials. Major domestic producers are scaling up their capacity to meet both domestic and export demand, reinforcing China’s role as a central hub for volume production and technology adoption in the global seam tapes ecosystem.

Seam Tapes Market Report Scope

Seam Tapes Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$419.5 Million

|

|

Market Size (2034)

|

$764.8 Million

|

|

Market Growth Rate

|

6.9%

|

|

Segments

|

By Type (Single-layered, Multi-layered), By Material (Thermoplastic Polyurethane, Polyurethane, Polyvinyl Chloride, Polyamide/Nylon-based, Polyolefin, Butyl Rubber, Ethylene Propylene Diene Monomer), By Application (Waterproofing, Seam Reinforcement, Joint Sealing, Control Joint, Expansion Joint, Vibration Dampening, Electrical Insulation), By End-Use Industry (Apparel & Footwear, Protective Clothing, Automotive, Construction, Electronics, Healthcare

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Bemis Associates Inc., Toray Industries, Inc., 3M Company, DingZing Advanced Materials Inc., Sealon Co., Ltd., Himel Corp., Gerlinger Industries GmbH, Loxy AS, Shikishima Canvas Co., Ltd., Sika AG, Adhesive Films, Inc., Jingcheng New Material (J-Tape), T&T Industry Group Ltd., Trivantage LLC

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Type

- Single-layered

- Multi-layered

By Material

- Thermoplastic Polyurethane

- Polyurethane

- Polyvinyl Chloride

- Polyamide/Nylon-based

- Polyolefin

- Butyl Rubber

- Ethylene Propylene Diene Monomer

By Application

- Waterproofing

- Seam Reinforcement

- Joint Sealing

- Control Joint

- Expansion Joint

- Vibration Dampening

- Electrical Insulation

By End-Use Industry

- Apparel & Footwear

- Protective Clothing

- Automotive

- Construction

- Electronics

- Healthcare

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Seam Tapes Market

- Bemis Associates Inc.

- Toray Industries, Inc.

- 3M Company

- DingZing Advanced Materials Inc.

- Sealon Co., Ltd.

- Himel Corp.

- Gerlinger Industries GmbH

- Loxy AS

- Shikishima Canvas Co., Ltd.

- Sika AG

- Adhesive Films, Inc.

- Jingcheng New Material (J-Tape)

- T&T Industry Group Ltd.

- Trivantage LLC

*- List not Exhaustive

Research Coverage

Prepared by USDAnalytics, this report investigates the Global Seam Tapes Market through an executive-level lens that connects demand shifts with material science breakthroughs, manufacturing upgrades, and regulatory change; our analysis reviews how multi-layer TPU and PU systems are redefining waterproofing, reinforcement, and joint sealing across apparel, PPE, construction, automotive, electronics, and healthcare, and it highlights the rise of bio-based inputs, PFAS/phthalate-free reformulations, and welding-ready films that boost throughput and quality—this report is an essential resource for sourcing leaders, product managers, and operations teams seeking defensible forecasts, specification guidance, and go-to-market clarity for 2025–2034.

Scope Highlights

Segmentation:

- By Type: Single-layered; Multi-layered.

- By Material: Thermoplastic Polyurethane; Polyurethane; Polyvinyl Chloride; Polyamide/Nylon-based; Polyolefin; Butyl Rubber; Ethylene Propylene Diene Monomer.

- By Application: Waterproofing; Seam Reinforcement; Joint Sealing; Control Joint; Expansion Joint; Vibration Dampening; Electrical Insulation.

- By End-Use Industry: Apparel & Footwear; Protective Clothing; Automotive; Construction; Electronics; Healthcare.

- By Region: North America (United States, Canada, Mexico); Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe); Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC); South & Central America (Brazil, Argentina, Rest of SCA); Middle East & Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa).

Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

Time Horizon: Historic data 2021–2024 and forecast data 2025–2034.

Companies Covered: Analysis / profiles of 15+ companies.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.