Sterilized Packaging Market Size, Overview, and Growth Outlook (2025–2034)

Sterilized Packaging Market Set to Reach $35.7 Billion by 2034 Driven by Patient Safety and Regulatory Compliance

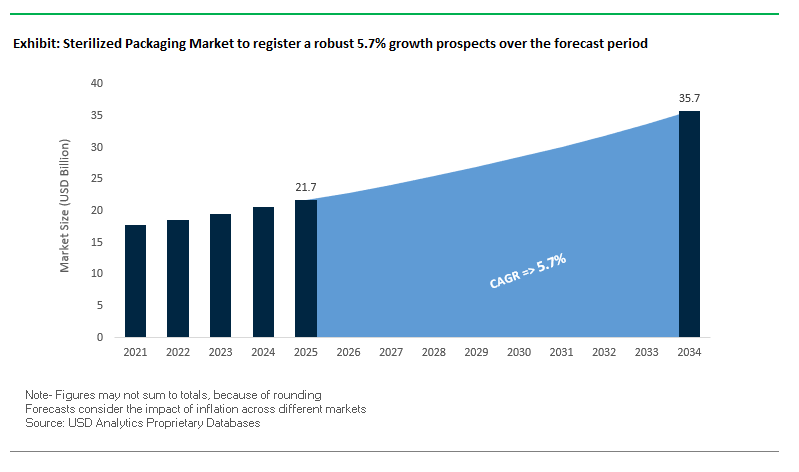

The global sterilized packaging market is projected to grow from $21.7 billion in 2025 to $35.7 billion by 2034, registering a CAGR of 5.7%. Sterilized packaging—including pouches, trays, and rigid containers—is critical for maintaining product integrity and microbial safety in the healthcare and pharmaceutical sectors.

Key Insights for Industry Professionals:

- Patient safety and hygiene remain the primary drivers, with sterile packaging acting as the first line of defense against contamination for medical devices, implants, and pharmaceuticals.

- Stringent regulatory compliance, such as ISO 11607 and EU Medical Device Regulations, mandates investment in validation, traceability, and material science.

- Innovations in sterilization methods, including low-temperature sterilization like vaporized hydrogen peroxide and e-beam, require specialized barrier materials.

- Regional manufacturing and supply chain resilience are critical post-COVID-19, with companies localizing production to ensure continuous supply.

- Sustainability considerations are emerging, with industry leaders exploring eco-friendly materials and circular economy initiatives.

The industry continues to focus on advanced materials, sterilization compatibility, and supply chain optimization, making sterilized packaging a core enabler of safe, compliant, and sustainable healthcare delivery.

Market Analysis: Strategic Developments in Sterilized Packaging Highlight Innovation, Sustainability, and Supply Chain Resilience

The sterilized packaging market has seen significant innovation in recent years. In August 2025, DuPont announced the winners of its 2025 Tyvek® Sustainable Healthcare Packaging Award, underlining its commitment to eco-friendly materials for medical applications. That same month, a review article highlighted advanced additives enhancing mechanical and antimicrobial properties of sterile films. In July 2025, Huhtamaki earned an EcoVadis gold medal for sustainability efforts for the fifth consecutive year, emphasizing the industry’s focus on environmentally responsible solutions.

Market expansion and capacity development are driving growth. In June 2025, Oliver Healthcare Packaging opened a new manufacturing facility in Johor, Malaysia, the largest in the APAC region, aimed at building a resilient supply chain and improving regional service. In May 2025, Solventum launched a preassembled VH2O2 test pack, improving efficiency in low-temperature sterilization processes. Earlier in March 2025, the company introduced its Attest™ eBowie-Dick Test System, enhancing sterilization assurance for healthcare facilities.

Strategic acquisitions and innovation in sustainable materials are also shaping the market. In October 2024, Amcor acquired Phoenix Flexibles in India, strengthening its presence in the rapidly growing Indian market. The same month, Bayer introduced PET blister packaging for Aleve in partnership with Liveo Research, reducing carbon footprint by 38%. In February 2024, 3M spun off Solventum, focusing on specialized healthcare packaging solutions, reflecting the trend of market consolidation and specialization.

Trends and Opportunities Shaping the Future of the Sterilized Packaging Market

Adoption of Recyclable and Reduced-Plastic Material Structures

One of the most defining trends in the sterilized packaging market is the industry-wide transition toward recyclable and reduced-plastic solutions. Historically, sterile packaging formats relied heavily on multi-material laminates—such as paper/film or Tyvek®/film combinations—that provided strong microbial barriers but created severe recycling challenges. These mixed-material structures were incompatible with most recovery systems, resulting in landfill disposal despite growing corporate commitments to sustainability.

Today, a strategic pivot is underway toward mono-material solutions. A notable development is the use of DuPont™ Tyvek® made from 100% HDPE, which has been certified as fully recyclable in compatible recycling streams. Such mono-material packaging not only ensures microbial protection and durability but also integrates seamlessly into established HDPE recycling infrastructure. This innovation reduces material complexity, lowers waste volumes, and helps medical device manufacturers meet stringent ESG targets tied to plastic reduction.

Furthermore, extrusion advancements allow sterile barrier systems to be made entirely of polyethylene-based structures, replacing conventional laminated materials. By removing unnecessary layers, manufacturers can reduce raw material usage by up to 15% while maintaining sterility assurance. This combination of eco-efficiency and technical reliability highlights why recyclable sterile packaging is rapidly becoming the industry standard.

Integration of Smart Features for Enhanced Traceability and Integrity

Alongside material innovation, the sterilized packaging market is embracing smart packaging technologies to improve traceability, security, and compliance. The integration of RFID tags into sterile packaging systems enables real-time supply chain visibility, automates work-in-process tracking, and supports compliance with Unique Device Identification (UDI) regulations, which mandate globally standardized identifiers for medical devices. This creates a powerful digital layer that strengthens anti-counterfeiting efforts while streamlining inventory management.

In addition to RFID, color-changing sterility indicators are gaining adoption as a cost-effective smart feature. Developed by companies such as SpotSee, these irreversible inks provide clear visual evidence of exposure to sterilization agents or critical temperature thresholds. They serve dual purposes: confirming proper sterilization and acting as tamper-evident seals. For hospitals, clinicians, and end-users, these indicators significantly reduce risks by offering instant visual confirmation of sterility and package integrity—a critical factor in patient safety and regulatory compliance.

Development of Packaging for Novel Sterilization Modalities

As medical devices become increasingly complex and integrate sensitive electronics, sensors, and polymers, traditional sterilization methods like high-temperature steam or radiation pose risks of product damage. This creates a major opportunity for packaging systems compatible with low-temperature sterilization processes.

One of the most promising approaches is designing packaging tailored for vaporized hydrogen peroxide (VHP) sterilization, a low-temperature method that is particularly suited for heat-sensitive devices. Technical research highlights the effectiveness of packaging structures combining transparent polyethylene/polyester composite films with Tyvek®, which allow sterilant penetration while maintaining barrier integrity post-process. By innovating around sterilant-specific compatibility, manufacturers can position themselves as leaders in enabling the next wave of advanced medical device packaging.

Additionally, packaging designed for compatibility with emerging sterilants such as ozone or chlorine dioxide gas represents a high-value niche. Companies that can engineer reliable, low-temperature-compatible sterile barrier systems will find strong demand as medical device portfolios continue to diversify.

Advanced Seal Integrity Testing Technologies

Another significant opportunity lies in next-generation quality assurance systems. Conventional sterile packaging validation has relied heavily on destructive testing methods like burst or dye-penetration tests, which waste valuable products and provide only sample-level assurance. The market is now shifting toward non-destructive, high-speed testing technologies that enable 100% inspection on production lines.

Advanced methods such as vacuum decay testing and tracer gas detection are increasingly being deployed for sterile packaging validation. For example, Emerson’s Rosemount leak detection system leverages quantum cascade laser (QCL) technology to test packages in real-time. Capable of detecting leaks as small as 0.3 mm at speeds of up to 200 packs per minute, these systems offer unmatched accuracy and throughput.

This transformation of seal integrity testing from batch sampling to inline, real-time verification not only strengthens patient safety but also reduces manufacturing waste and lowers quality control costs. With regulators demanding stronger sterility assurance levels, investment in non-destructive seal testing represents one of the most lucrative opportunities in the sterilized packaging sector.

Competitive Landscape: Industry Leaders Drive Sterilized Packaging Market Growth Through Innovation, Material Expertise, and Sustainability

The global sterilized packaging market is shaped by companies leveraging materials science, manufacturing expertise, and sustainability initiatives to provide reliable, high-performance solutions for medical and pharmaceutical applications.

DuPont de Nemours, Inc.: Leading Sterile Barrier Innovations with Tyvek® Materials

DuPont is renowned for its Tyvek® sterile barrier packaging, offering superior microbial protection, tear resistance, and breathability compatible with multiple sterilization methods. In August 2025, the company recognized winners of its Tyvek® Sustainable Healthcare Packaging Award and promoted Tyvek® with Renewable Attribution, supporting the circular economy. DuPont’s strengths lie in materials science expertise, brand recognition, and R&D-driven innovation, with a strategy focused on high-performance, sustainable healthcare packaging.

Amcor plc: Advancing Recyclable Sterile Packaging for Global Healthcare Markets

Amcor provides a range of sterile pouches, lids, and blister packs for medical devices and pharmaceuticals. The company is committed to making all packaging recyclable or reusable by 2025. Amcor’s core strengths include a global manufacturing network, expertise across multiple materials, and a vertically integrated model. Its strategic focus is on supporting the circular economy while ensuring patient safety and product integrity.

Oliver Healthcare Packaging: Expanding APAC Presence to Strengthen Supply Chain Resilience

Oliver Healthcare Packaging specializes in die-cut lids, roll stock, and pouches for sterile applications. In June 2025, it opened its largest APAC facility in Johor, Malaysia, enhancing regional supply resilience. The company emphasizes quality, innovation, and compliance, operating with a level of validation and precision comparable to medical device standards. Its strategic focus is on providing validated, sustainable, and customer-focused sterile solutions.

West Pharmaceutical Services, Inc.: Ensuring Sterile Packaging Integrity for Injectable Medicines

West manufactures stoppers, seals, and containment components essential for sterile injectable drug packaging. In February 2025, its High-Value Products business returned to organic growth, driven by biologics and generics. West’s core strengths include elastomer expertise, regulatory compliance, and global brand recognition, with a strategy focused on innovative, high-quality solutions for injectable drug delivery.

Sterile Services, a STERIS Company: Delivering Specialized Sterilization Solutions Globally

STERIS provides sterilization services, including gamma irradiation, e-beam, and ethylene oxide, crucial for medical device packaging. Its AST segment reported 10% organic revenue growth in Q4 2025. STERIS’s strengths lie in sterilization expertise and a global network of facilities, with a strategic focus on infection prevention and comprehensive sterilization services supporting product safety and compliance.

Sterilized Packaging Market Share Insights, 2025-2034

Bags & Pouches Lead Market Share by Product Type in Sterilized Packaging Industry

Bags and pouches hold 28% of the sterilized packaging market, making them the most widely used format due to their adaptability across diverse sterilization methods such as steam, ethylene oxide, and gamma radiation. Their dominance stems from their critical role in packaging single-use surgical instruments, implants, and medical kits, where sterility assurance and barrier integrity are non-negotiable. Sterile pouches, often combining Tyvek® and medical-grade plastics, provide excellent peelability, lightweight transport efficiency, and compatibility with varying device sizes, giving them a versatility unmatched by trays, vials, or blister formats. As hospitals and surgical centers increasingly rely on ready-to-use sterile instruments, demand for sterile pouches continues to expand, cementing their leadership in this segment.

Medical Devices Dominate Market Share by End-Use Industry in Sterilized Packaging Industry

Medical devices account for 55% of the sterilized packaging industry, underscoring their status as the primary growth engine of this regulated market. The scale of single-use medical products—from syringes and catheters to complex surgical procedure kits—requires packaging that not only maintains sterility but also withstands handling, transport, and clinical environments without compromise. The dominance of this segment is driven by the global rise in surgical volumes, aging populations requiring more medical interventions, and the increasing use of minimally invasive devices that depend on sterile packaging to preserve functionality. Pharmaceutical and food applications remain important niches, but the medical device sector’s stringent safety requirements and regulatory oversight ensure its position as the anchor of market demand.

United States: FDA Standards and Sustainable Sterile Packaging Innovation

The United States sterilized packaging market is driven by stringent regulatory oversight from the U.S. Food and Drug Administration (FDA) and standards set by organizations such as the Association for the Advancement of Medical Instrumentation (AAMI). These agencies enforce detailed requirements for barrier performance, seal integrity, and sterility assurance, which continue to shape packaging innovations. In addition, ASTM International standards—including ASTM F2096 for leak detection and ASTM F1980 for accelerated aging—define the benchmarks for sterile packaging performance.

Sustainability has emerged as a key focus, with companies adopting recyclable and bio-based materials. In April 2024, Nelipak Healthcare Packaging integrated Eastman Renew’s materials into its rigid thermoformed sterile barrier solutions, aligning with the healthcare sector’s sustainability goals. Demand is also growing for smart packaging with sensors for real-time monitoring of temperature, humidity, and pressure, particularly in pharmaceuticals and biologics. Industry investment continues to expand—Packaging Compliance Labs LLC invested $2.57 million in 2020 to expand sterile packaging testing facilities, while DuPont recognized leaders in eco-friendly packaging with its Tyvek® Sustainable Healthcare Packaging Awards in September 2024.

European Union: PPWR, MDR Compliance, and Digital Product Passports

The European Union sterilized packaging market is experiencing a regulatory transformation led by the Packaging and Packaging Waste Regulation (PPWR), effective February 2025, which mandates minimum percentages of post-consumer recycled content in plastic packaging by 2030. For sterile packaging, this shift encourages the use of recyclable mono-material films while maintaining product sterility. The Ecodesign for Sustainable Products Regulation (ESPR) further promotes eco-designed packaging solutions that enhance recyclability.

The EU Medical Device Regulation (MDR), fully effective since 2021, has intensified requirements for medical device packaging, focusing on traceability, clinical evaluations, and safety standards. Additionally, the upcoming Digital Product Passport will demand material composition and recyclability disclosure, improving transparency across healthcare supply chains. Restrictions on PFAS in food contact packaging by August 2026 are pushing sterile packaging manufacturers toward alternative coatings and advanced barrier technologies, aligning safety with sustainability.

China: Rising Demand for Advanced Sterile Packaging in Healthcare

The China sterilized packaging market is supported by regulatory reforms under the “14th Five-Year Plan” and packaging mandates effective June 1, 2025, prioritizing eco-friendly, reduced, and reusable packaging. While initially targeted at e-commerce, these initiatives extend to medical supply chains, increasing adoption of sustainable sterile solutions.

Growing demand for high-end pharmaceuticals and medical devices is fueling investments in sophisticated sterile packaging with enhanced barrier properties and anti-counterfeiting features. For instance, Amcor invested $35 million in 2021 in a new innovation center in Jiangyin, China, to advance sterile packaging innovation. With government tax incentives supporting green technology and remanufacturing, domestic manufacturers are expected to strengthen their role in both local and export sterile packaging markets.

India: EPR Enforcement and Healthcare Sector Growth

The India sterilized packaging market is heavily shaped by the Plastic Waste Management (Amendment) Rules, 2024, effective April 2025, which impose strict Extended Producer Responsibility (EPR) on packaging manufacturers. By July 1, 2025, all sterile packaging must be traceable via barcodes or QR codes, ensuring accountability and lifecycle monitoring. Although MSMEs are exempt from direct compliance, larger manufacturers and importers supplying raw materials bear the responsibility.

The rise of the healthcare and hospital infrastructure sector is a major growth driver for sterilized packaging, as demand increases for medical devices, pharmaceutical products, and sterile surgical kits. Domestic initiatives, combined with stricter environmental accountability, are prompting manufacturers to invest in sustainable sterilized packaging solutions tailored to India’s expanding medical ecosystem.

Japan: Plastic Resource Circulation Strategy and Bio-Based Packaging Growth

The Japan sterilized packaging market is transitioning under the Plastic Resource Circulation Strategy, which mandates all packaging to be reusable or recyclable by 2025. The Plastic Resource Circulation Promotion Law, also effective 2025, requires redesign of 12 categories of single-use plastics, encouraging the adoption of bio-based and compostable packaging alternatives for sterile products.

In September 2025, LyondellBasell introduced bio-based polypropylene (PP) for Shiseido’s packaging, marking a broader industry shift toward sustainable materials, with applications extending to healthcare and sterile packaging. Food and healthcare sectors are further influenced by the Ministry of Health, Labor and Welfare’s (MHLW) positive list system, effective June 1, 2025, which clarifies safe materials for food contact and sterilized applications. Combined, these initiatives are positioning Japan as a hub for next-generation sterile packaging innovations.

Brazil: Reverse Logistics and Strengthened Recycling Policies

The Brazil sterilized packaging market is shaped by the National Solid Waste Policy (PNRS), which enforces responsible recycling, reuse, and reduction across industries. The January 2025 implementation of Law No. 15,088, banning imports of plastic waste, has strengthened domestic demand for sustainable materials and packaging innovation.

The government’s promotion of reverse logistics systems requires producers to manage post-consumer collection and recycling of sterile packaging, creating accountability for manufacturers and brand owners. With a strong focus on circular economy practices, these initiatives are fostering investment in eco-friendly healthcare packaging solutions that reduce environmental impact while maintaining sterile integrity for medical and pharmaceutical products.

Sterilized Packaging Market Report Scope

Sterilized Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$21.7 Billion

|

|

Market Size (2034)

|

$35.7 Billion

|

|

Market Growth Rate

|

5.7%

|

|

Segments

|

By Material (Plastics, Paper & Paperboard, Glass, Metal, Composites), By Product Type (Bags & Pouches, Vials & Ampoules, Bottles, Trays, Containers, Blister Packs, Wraps & Films), By Sterilization Method (Gamma Radiation, Ethylene Oxide, E-beam, Steam, Other), By End-Use Industry (Medical Devices, Pharmaceuticals & Drugs, Food & Beverages, Cosmetics & Personal Care, Others)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, DuPont de Nemours, Inc., Berry Global, Inc., 3M Company, Tekni-Plex, Inc., Gerresheimer AG, Wipak Group, Nelipak Healthcare Packaging, Sealed Air Corporation, Oliver Healthcare Packaging, B. Braun SE, West Pharmaceutical Services, Inc., Sonoco Products Company, SteriPackGroup, Nelplast ECO Ghana Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Sterilized Packaging Market Segmentation

By Material

- Plastics

- Paper & Paperboard

- Glass

- Metal

- Composites

By Product Type

- Bags & Pouches

- Vials & Ampoules

- Bottles

- Trays

- Containers

- Blister Packs

- Wraps & Films

By Sterilization Method

- Gamma Radiation

- Ethylene Oxide

- E-beam

- Steam

- Others

By End-Use Industry

- Medical Devices

- Pharmaceuticals & Drugs

- Food & Beverages

- Cosmetics & Personal Care

- Others

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Sterilized Packaging Market

- Amcor plc

- DuPont de Nemours, Inc.

- Berry Global, Inc.

- 3M Company

- Tekni-Plex, Inc.

- Gerresheimer AG

- Wipak Group

- Nelipak Healthcare Packaging

- Sealed Air Corporation

- Oliver Healthcare Packaging

- B. Braun SE

- West Pharmaceutical Services, Inc.

- Sonoco Products Company

- SteriPackGroup

- Nelplast ECO Ghana Ltd.

* List Not Exhaustive

Methodology

The Sterilized Packaging Market report by USDAnalytics has been prepared using a robust research methodology that combines both primary and secondary research to deliver precise, actionable insights for industry professionals. Primary research involved consultations with packaging engineers, R&D specialists, regulatory compliance officers, and supply chain managers from leading companies such as DuPont, Amcor, Oliver Healthcare Packaging, West Pharmaceutical Services, and SteriPackGroup, focusing on innovations in sterile barrier materials, sterilization methods, and sustainable solutions. Secondary research encompassed a thorough analysis of company reports, scientific journals, trade publications, patent filings, and regulatory documents including ISO 11607, EU MDR, FDA standards, and national EPR mandates to assess market trends, growth drivers, and regional dynamics. Market sizing and forecasts were calculated through a combination of top-down and bottom-up approaches, factoring in material types, product formats, sterilization techniques, and end-use industries. Data triangulation and cross-validation ensured the reliability of projections, while comprehensive analysis of regional regulatory frameworks, technological innovations, and sustainability initiatives provided a holistic view of the global sterilized packaging landscape, highlighting strategic opportunities, competitive positioning, and adoption patterns across key markets.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.