Sugarcane-Based Packaging Market Size, Overview, and Growth Outlook (2025–2034)

Sugarcane-Based Packaging Market Poised to More Than Double by 2034 Amid Rising Sustainability Demands

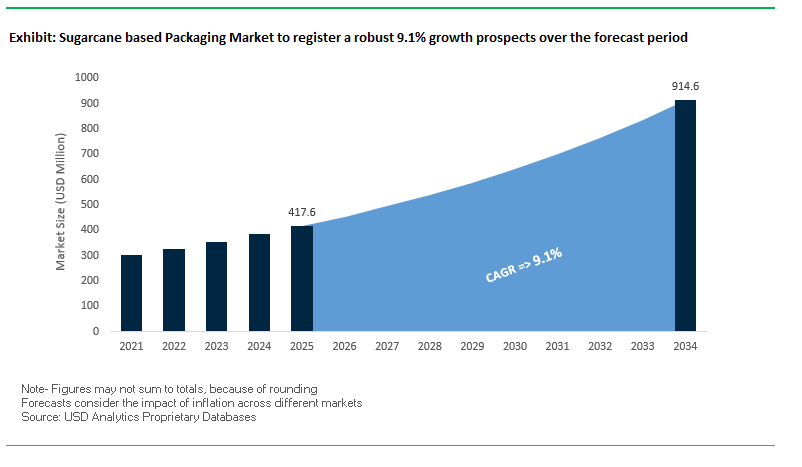

The global sugarcane-based packaging market is projected to grow from $417.6 million in 2025 to $914.5 million by 2034, representing a CAGR of 9.1%. Leveraging bagasse, the fibrous byproduct of sugarcane, the industry offers eco-friendly, biodegradable alternatives to conventional plastics and Styrofoam, positioning itself at the forefront of the global circular economy movement.

Key Insights for Industry Professionals:

- Government regulations and single-use plastic bans in regions like Europe and North America are driving the adoption of plant-based alternatives.

- Innovations in thermoforming, blending, and bio-based coatings enhance the moisture resistance, durability, and grease-proof properties of sugarcane packaging.

- Closed-loop and circular economy principles are integral, as bagasse decomposes naturally, returning nutrients to the soil and reducing landfill waste.

- Expansion into e-commerce void-fill and retail meal trays demonstrates the material’s versatility beyond foodservice applications.

- Rising consumer preference for sustainable packaging amplifies market growth across both B2B and B2C segments.

This market outlook highlights that material innovation, regulatory support, and sustainability-driven adoption are pivotal for growth in sugarcane-based packaging.

Market Analysis: Industry Dynamics Show a Strong Shift Toward Sustainable and Bio-Based Packaging Solutions

The sugarcane-based packaging industry continues to evolve with a focus on technological innovation, regulatory alignment, and eco-conscious manufacturing. In October 2024, Accredo Packaging and Fresh-Lock launched a 100% bio-based resin pouch with zipper closure, highlighting a move toward practical, sustainable packaging solutions for consumer products. Meanwhile, Huhtamaki and Danone collaborated to create yogurt cups made with sugarcane fibers, replacing traditional plastic linings and demonstrating the industry's commitment to environmentally responsible food packaging.

Sustainability recognition further validates market trends. In July 2025, Huhtamaki earned an EcoVadis gold medal for the fifth consecutive year, reinforcing its leadership in sustainable packaging solutions including sugarcane-based products. Mondi and Krones’ August 2025 partnership to produce Hug&Hold paper-based shrink wrap exemplifies the pivot toward renewable feedstocks like sugarcane, extending applications beyond traditional foodservice.

Innovation in material performance also drives adoption. Studies from October 2024 have shown that integrating 25% sugarcane bagasse fiber into biodegradable films improves water vapor permeability, tensile strength, and elongation at break, enabling broader use in both retail and industrial packaging. Companies like CHUK and Better Earth continue to expand compostable tableware lines, further establishing sugarcane packaging as a versatile and sustainable alternative in multiple end-use sectors.

Trends and Opportunities Shaping the Sugarcane-Based Packaging Market

Diversification Beyond Foodservice into Rigid Consumer Packaging

The sugarcane-based packaging market is evolving rapidly as bagasse moves beyond its traditional foodservice role into rigid consumer packaging applications. Traditionally associated with low-cost disposable plates, bowls, and trays, sugarcane bagasse is now being molded into leak-proof containers with fitted lids, making it suitable for takeaway, ready-to-eat meals, and retail food packaging. A leading supplier’s 2025 product line demonstrated this shift by offering rigid containers that can withstand both hot and cold foods, directly competing with single-use plastics.

The durability of bagasse has historically been a concern, but advances in molding techniques and fiber processing are now overcoming these limitations. Studies show that properly manufactured bagasse packaging can resist soaking, handle hot-fill conditions, and maintain structural integrity under moderate impacts, making it a credible alternative to polystyrene foam and rigid plastics in applications like multi-compartment trays, deli containers, and microwaveable clamshells. This durability enhancement is expanding the range of consumer products that can be packaged in bagasse-based solutions, aligning with both regulatory pressures on plastics and consumer demand for eco-friendly packaging.

Development of High-Barrier Coatings for Functional Performance

Another major trend reshaping the sugarcane packaging market is the development of high-barrier, bio-based coatings that enhance the material’s performance. Traditional applications of bagasse were limited by poor barrier resistance against moisture, grease, and oxygen. However, a recent academic breakthrough showed that applying a two-layer shellac coating to bagasse reduced oxygen permeability by 99.5%, extending the shelf life of packaged chips by up to 50 days.

This advancement eliminates the need for plastic liners or PE coatings, enabling fully compostable, bio-based packaging systems. Such coatings also accelerate the industry-wide “paperization” trend, where packaging traditionally made with multi-material laminates is replaced with single-stream recyclable or compostable structures. By providing a high-performance barrier while remaining biodegradable, bio-based coatings are positioning sugarcane packaging as a serious contender in categories like snacks, bakery, and frozen foods, which have historically relied on petrochemical plastics.

Leveraging “Carbon Capture” Attributes in Marketing and ESG Reporting

One of the most unique opportunities for sugarcane-based packaging lies in its carbon capture potential. Unlike many other raw materials, sugarcane actively sequesters CO₂ during its growth cycle, giving it a strong carbon-negative narrative. A techno-economic assessment of bio-energy with carbon capture and storage (BECCS) in sugarcane mills demonstrated that capturing CO₂ from fermentation streams could substantially reduce emissions, positioning sugarcane packaging as a climate-positive solution.

Brands are already using Life Cycle Assessments (LCAs) to validate these claims. Comparative studies between sugarcane bagasse and wood-based products show consistently lower environmental impacts across multiple categories, including greenhouse gas emissions and fossil resource depletion. By integrating these findings into ESG disclosures, sustainability reports, and consumer-facing marketing, companies can differentiate sugarcane packaging not just as compostable, but as carbon-negative—a positioning that resonates strongly with both regulators and eco-conscious consumers.

Establishing Efficient Collection and End-of-Life Infrastructure

The true potential of sugarcane-based packaging will only be realized through investments in collection and composting infrastructure. A U.S. EPA report estimates that nearly $43 billion in investment will be required to modernize recycling and organics management infrastructure in the United States alone. If implemented, these investments could increase organic waste recovery by over 90%, directly benefiting compostable packaging streams.

Infrastructure development also creates broader economic value. Research on compostable waste diversion highlights that scaling composting systems can reduce landfill tipping costs, create thousands of green jobs, and generate revenue through the sale of high-quality compost. For sugarcane packaging producers, aligning with municipalities, waste management companies, and private investors to build regional composting hubs represents a high-reward strategy. This will not only ensure a sustainable end-of-life pathway for bagasse-based packaging but also accelerate the transition toward a circular bioeconomy.

Competitive Landscape: Leading Sugarcane-Based Packaging Companies Are Driving Sustainability, Innovation, and Market Expansion

The global sugarcane-based packaging market is shaped by key players leveraging materials expertise, sustainable design, and global manufacturing networks to provide high-performance biodegradable solutions.

Huhtamaki Oyj: Pioneering Eco-Friendly Food Packaging with Sugarcane Fiber

Huhtamaki offers a diverse portfolio of paper and fiber-based containers, trays, and molded fiber products. In October 2024, the company partnered with Danone to create yogurt cups with sugarcane fibers using bio-based barriers. By July 2025, Huhtamaki earned its fifth consecutive EcoVadis gold medal, emphasizing leadership in sustainability. Core strengths include global manufacturing expertise and comprehensive product offerings, with a strategy focused on recyclable, reusable, or compostable packaging by 2030.

Mondi Group: Expanding Paper-Based Packaging Solutions Through Sustainable Feedstocks

Mondi specializes in paper-based packaging solutions using bio-based feedstocks like sugarcane. In August 2025, the company partnered with Krones to launch Hug&Hold shrink wrap for beverage bottles, signaling a strong pivot to eco-friendly materials. Its FunctionalBarrier Paper Ultimate product offers high performance in paper-based packaging. Mondi’s strengths lie in R&D capabilities and sustainability focus, with a strategic vision to deliver customized, environmentally responsible packaging.

Amcor plc: Driving Circular Economy with Innovative Bio-Based Packaging

Amcor provides a wide range of sustainable flexible and rigid packaging, including sugarcane-derived resins. The company is focused on recyclable and reusable solutions, with an aim for all packaging to meet circular economy standards by 2025. Core strengths include a global manufacturing footprint and vertically integrated operations, enabling Amcor to deliver high-performance packaging solutions while advancing sustainability.

Eco-Products, Inc.: Leading the Foodservice Sector with Compostable Sugarcane Solutions

Eco-Products offers compostable containers and cutlery made from sugarcane bagasse, emphasizing sustainability and product quality. In September 2024, its brand CHUK expanded compostable tableware lines. Core strengths include focus on sustainability and a broad compostable product portfolio, with a strategy centered on innovative, eco-friendly solutions for the circular economy.

World Centric: Combining Social Responsibility with High-Quality Compostable Packaging

World Centric, a certified B Corp, provides plates, bowls, and clamshells made from sugarcane and other plant-based materials. The company donates 25% of pre-tax profits to grassroots organizations, differentiating itself through social and environmental initiatives. Core strengths include brand recognition and expertise in compostable materials, with a strategy to lead the global movement toward sustainable and socially responsible packaging.

Sugarcane based Packaging Market Share Insights, 2025-2034

Clamshells & Containers Lead Market Share by Product Type in Sugarcane-Based Packaging Industry

Clamshells and containers account for 30% of the sugarcane-based packaging market, cementing their dominance as the default solution for takeaway food and foodservice applications. Derived from bagasse, these products provide microwave safety, grease resistance, and structural rigidity, making them the ideal sustainable replacement for expanded polystyrene and petroleum-based plastics. The shift toward eco-friendly food packaging in quick-service restaurants, cafés, and delivery chains has accelerated adoption, with global bans on single-use plastics reinforcing their market leadership. Their direct alignment with regulatory, consumer, and operational needs secures clamshells and containers as the most commercially viable format in the sugarcane packaging ecosystem.

Food & Beverages Account for Overwhelming Market Share by Application in Sugarcane-Based Packaging Industry

Food and beverages dominate with a 95% share of the sugarcane-based packaging market, reflecting the material’s near-exclusive alignment with foodservice and food delivery demand. Bagasse packaging was developed to meet global sustainability and regulatory shifts, offering compostable, heat-resistant, and sturdy alternatives for plates, trays, bowls, and takeaway containers. Its suitability for handling hot, greasy, and wet foods without structural compromise makes it indispensable in restaurants, cafeterias, catering services, and food delivery platforms. This sector’s regulatory tailwinds—plastic bans, compostability mandates, and circular economy policies—further cement food and beverages as the primary growth engine, leaving other applications in personal care or healthcare as marginal niches.

Brazil: Pioneering Bio-Based Innovation and Government-Led Sustainability

The Brazil sugarcane-based packaging market is positioned as a global leader due to its vast sugarcane production and strong government support for circular economy policies. Researchers at Embrapa have developed biodegradable cellulose nanocrystals from sugarcane straw, creating high-strength, eco-friendly materials from agricultural residues that would otherwise go to waste. Similarly, CNPEM’s patented antistatic packaging derived from sugarcane bagasse is revolutionizing the protection of sensitive electronic components, replacing petroleum-based plastics in applications such as mobile devices and computer parts.

From a policy perspective, Brazil’s National Solid Waste Policy (PNRS) enforces strict guidelines on producer responsibility, further strengthened by the 2025 ban on solid waste imports, which promotes reliance on domestic renewable raw materials. Industry leaders like Braskem, through its partnership with Raízen, are scaling bio-based polyethylene (PE) under the I’m green™ brand, widely adopted by global consumer goods companies. These innovations, combined with the government’s reverse logistics framework, are fueling rapid adoption of sugarcane bagasse packaging in foodservice, consumer goods, and industrial applications.

United States: Compostable Packaging and E-Commerce Demand Driving Growth

The United States sugarcane-based packaging market is growing under the influence of federal recycling initiatives and rising consumer demand for sustainable products. The EPA’s 50% recycling goal by 2030 is driving investment in compostable and recyclable foodservice packaging, with BPI (Biodegradable Products Institute) certifications becoming a market differentiator for brand credibility. A notable innovation is the introduction of tree-free paper from sugarcane pulp, which offers a plastic-free, biodegradable alternative to conventional paper, expanding adoption in packaging and stationery.

Leading companies such as Berry Global are integrating recycled and sugarcane-based content into packaging solutions to meet consumer and retailer sustainability commitments. Meanwhile, the e-commerce revolution is accelerating demand for lightweight and durable sugarcane packaging, particularly in shipping boxes, molded pulp trays, and protective inserts. The U.S. market is thus balancing performance-driven material innovation with the scalability needed for logistics and consumer goods packaging.

European Union: Regulatory Mandates and Bio-Composite Innovation

The European Union sugarcane-based packaging market is shaped by regulatory frameworks that encourage recyclability, compostability, and traceability. The Packaging and Packaging Waste Regulation (PPWR), effective from February 2025, requires packaging to achieve economic recyclability by 2030, driving companies to invest in sugarcane-derived alternatives. The Ecodesign for Sustainable Products Regulation (ESPR) complements this by promoting mono-material packaging solutions for improved compostability.

Key innovation drivers include restrictions on hazardous substances like PFAS in food contact packaging from August 2026, which accelerates the development of natural barrier coatings for sugarcane-based films and containers. Additionally, the EU’s promotion of refill and reuse systems creates opportunities for durable bio-based solutions. Regional leaders, especially in Italy and Spain, are investing heavily in compostable infrastructure, while collaborations with research centers focus on marine-safe films and dual-layer cellulose packaging, boosting the application of sugarcane packaging in food, retail, and healthcare markets.

China: Bagasse-Based Packaging for E-Commerce and Consumer Electronics

The China sugarcane-based packaging market is expanding rapidly, supported by the “14th Five-Year Plan”, which emphasizes the reduction of plastic pollution. Effective June 2025 regulations require express delivery companies to prioritize reusable and eco-friendly packaging, directly benefiting bagasse-based molded pulp packaging for logistics and e-commerce. China’s large sugarcane output provides abundant bagasse feedstock, increasingly converted into molded pulp trays, food containers, and electronics packaging.

Academic institutions are enhancing the sector’s innovation ecosystem. For instance, partnerships such as the Ellen MacArthur Foundation and Tsinghua University have highlighted the need for improved recycling systems, creating an enabling environment for plant-based and recyclable packaging solutions. With consumer demand for premium and sustainable packaging, sugarcane bagasse is gaining traction in high-value applications, including electronics and luxury goods, where durability and aesthetic appeal are critical.

India: Regulatory Push and Diversification of Bagasse Applications

The India sugarcane-based packaging market is being reshaped by regulatory frameworks and material diversification. The Plastic Waste Management (Amendment) Rules, 2024, implemented in April 2025, enforce Extended Producer Responsibility (EPR) for brand owners, ensuring accountability for disposal and recycling. From July 2025, all plastic packaging must carry QR code or barcode traceability, creating new opportunities for sugarcane packaging as a compliant, eco-friendly alternative.

Beyond food packaging, innovative applications are emerging. India’s National Institute for Interdisciplinary Science and Technology has partnered with industry players to create vegetable-based leather from sugarcane bagasse, targeting fashion and accessories markets. With the FSSAI drafting food safety guidelines for sustainable packaging, adoption of sugarcane bagasse products in foodservice, retail, and personal care packaging is expected to accelerate. This diversification strengthens India’s role in global sugarcane packaging innovation, driven by a booming e-commerce and FMCG sector.

Japan: Bio-Based Pharma Packaging and Sustainable Transition

The Japan sugarcane-based packaging market is advancing rapidly with both policy support and industry adoption. The Plastic Resource Circulation Strategy (2025) and Plastic Resource Circulation Promotion Law mandate reductions in single-use plastics and promote compostable alternatives, creating a favorable environment for sugarcane bagasse products. In a world-first initiative, Astellas Pharma Inc. adopted sugarcane-derived biomass plastics in blister packaging for pharmaceuticals as early as 2021, setting a benchmark for the integration of renewable materials in high-value healthcare packaging.

Government initiatives reinforce this momentum. The MHLW positive list system, effective June 2025, ensures that only approved safe materials are used in food and pharmaceutical packaging. This, combined with Japan’s goal to double renewable material usage by 2030, is driving R&D in compostable and recyclable bagasse-based solutions. With strong collaboration between regulators, research institutes, and global corporations, Japan is positioning sugarcane-based packaging as a sustainable and high-tech alternative for food, pharmaceutical, and consumer markets.

Sugarcane based Packaging Market Report Scope

Sugarcane based Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$417.6 Million

|

|

Market Size (2034)

|

$914.5 Million

|

|

Market Growth Rate

|

9.1%

|

|

Segments

|

By Product Type (Clamshells & Containers, Trays & Plates, Bowls, Cups & Lids, Bags & Pouches, Films & Wraps, Cutlery & Straws), By Application (Food & Beverages, Consumer Goods, Electronics, Healthcare & Pharmaceuticals, Home & Personal Care), By End-Use Industry (Food Service, Retail, E-commerce & Logistics, Consumer Electronics, Healthcare)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Braskem S.A., Huhtamaki Oyj, Ranpak Holdings Corp., BioBag International AS, World Centric, Vegware Ltd., Good Start Packaging, Eco-Products, Inc., Pactiv Evergreen Inc., Genpak LLC, B-Pack GmbH, Growood, Astellas Pharma Inc., Novamont S.p.A., Equo

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Sugarcane based Packaging Market Segmentation

By Product Type

- Clamshells & Containers

- Trays & Plates

- Bowls

- Cups & Lids

- Bags & Pouches

- Films & Wraps

- Cutlery & Straws

By Application

- Food & Beverages

- Consumer Goods

- Electronics

- Healthcare & Pharmaceuticals

- Home & Personal Care

By End-Use Industry

- Food Service

- Retail

- E-commerce & Logistics

- Consumer Electronics

- Healthcare

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Sugarcane based Packaging Market

- Braskem S.A.

- Huhtamaki Oyj

- Ranpak Holdings Corp.

- BioBag International AS

- World Centric

- Vegware Ltd.

- Good Start Packaging

- Eco-Products, Inc.

- Pactiv Evergreen Inc.

- Genpak LLC

- B-Pack GmbH

- Growood

- Astellas Pharma Inc.

- Novamont S.p.A.

- Equo

* List Not Exhaustive

Methodology

The Sugarcane-Based Packaging Market report by USDAnalytics has been prepared using a comprehensive research methodology combining primary and secondary approaches to provide actionable insights for industry professionals. Our primary research involved in-depth interviews with R&D managers, sustainability officers, procurement heads, and product development experts from leading companies such as Huhtamaki, Amcor, Mondi, Braskem, and Eco-Products, as well as consultations with regulatory bodies and academic researchers specializing in bio-based materials. Secondary research included analysis of corporate filings, sustainability reports, patents, conference proceedings, industry journals, and government publications. Market sizing and forecasts were derived using both bottom-up and top-down approaches, taking into account product types, applications, end-use industries, and regional dynamics across North America, Europe, Asia-Pacific, and Latin America. Special focus was placed on material innovations such as bagasse fiber processing, bio-based coatings, and carbon-negative production, as well as regulatory frameworks like single-use plastic bans, Extended Producer Responsibility (EPR), and compostability mandates. By integrating technological, regulatory, and sustainability-driven perspectives, USDAnalytics ensures a holistic and accurate representation of growth drivers, market opportunities, competitive landscape, and future trajectories for sugarcane-based packaging globally.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.