Surfactant EOR Market 2025–2034: $121.2 Million to $168.1 Million at 3.7% CAGR Driven by Nano-Darcy Reservoir Chemistry, Digital Reservoir Modeling, and Deepwater Injection Systems

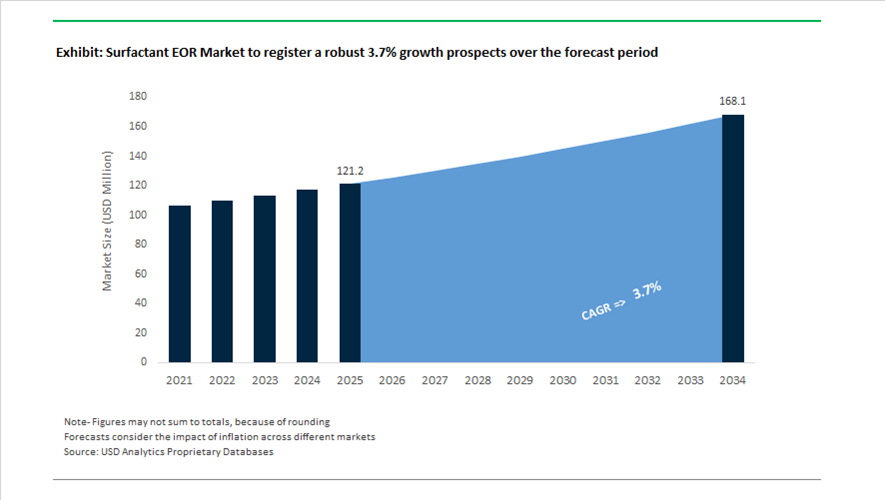

The global surfactant enhanced oil recovery (EOR) market is valued at $121.2 million in 2025 and is projected to reach $168.1 million by 2034, expanding at a CAGR of 3.7%. Market expansion is supported by rising demand for advanced oilfield surfactants, interfacial tension (IFT) reduction chemistries, wettability alteration agents, alkali-surfactant-polymer (ASP) formulations, and high-salinity tolerant EOR fluids deployed in mature reservoirs and ultra-tight unconventional formations. Operators are prioritizing chemical EOR solutions capable of performing in permeability environments as low as one nano-Darcy, high-temperature deepwater reservoirs, and carbonate formations with complex wettability profiles. Integration of digital reservoir modeling, CCUS-compatible injection systems, and carbon-reduced surfactant supply chains is redefining project economics and lifecycle efficiency.

Industry consolidation and technology integration accelerated beginning in April 2024, when SLB announced a $7.7 billion agreement to acquire ChampionX. The transaction cleared major UK CMA regulatory hurdles in early 2025, creating a vertically integrated EOR platform combining SLB’s digital reservoir simulation capabilities with ChampionX’s Production Enhancement (PROE) surfactant technology. Throughout 2024 and 2025, ChampionX expanded its PROE program, deploying customized surfactant blends engineered to reduce IFT and alter formation wettability in ultra-tight formations. In early 2025, new U.S. tariff measures on imported chemical precursors increased formulation costs, prompting operators to shift from continuous injection strategies to slug injection programs to conserve high-value surfactants. In April 2025, Roquette finalized its acquisition of IFF Pharma Solutions, strengthening its portfolio of high-purity bio-based intermediates used in specialty biosurfactant formulations designed for environmentally sensitive EOR applications. In October 2025, BASF completed the divestment of its decorative paints business to refocus capital on its Performance Chemicals division, including oilfield surfactants and EOR polymers.

Deployment of advanced injection systems and regional capacity optimization intensified in 2026. In January 2026, Halliburton and Singapore’s A*STAR launched the NEX Lab℠, dedicated to developing next-generation well completion and chemical EOR fluids capable of withstanding harsh subsea and high-pressure environments. In February 2026, Halliburton introduced the XTR CS injection system, engineered to deliver surfactant chemistries under extreme temperature and pressure conditions relevant to deepwater EOR and CCUS-linked applications. In early 2026, Stepan Company confirmed start-up of its Pasadena, Texas facility, strengthening localized manufacturing of oilfield surfactants and supporting year-over-year growth in its higher-margin specialty segment. In February 2026, Baker Hughes signed a multi-year agreement with Marathon Petroleum covering downstream chemical treatments and specialty demulsifiers across 12 refineries, reinforcing integration between upstream EOR chemistry and downstream processing. In February 2026, BASF launched AdBlue GE produced using 100% renewable electricity, supporting reduced Scope 3 carbon intensity targets for oilfield chemical customers. These structural consolidations, nano-Darcy optimized formulations, digital reservoir integration, and deepwater-compatible injection technologies are shaping the next phase of growth in the surfactant EOR market through 2034.

Strategic Trends and Opportunity Landscape in the Surfactant Enhanced Oil Recovery Market

CCUS–EOR Integration Accelerated by 45Q Tax Credit Parity under the OBBBA

The most consequential shift in the Surfactant Enhanced Oil Recovery market in 2025 stems from the One Big Beautiful Bill Act, which fundamentally alters the economic logic of tertiary recovery projects in mature basins. By establishing tax parity between permanent CO₂ sequestration and CO₂ utilization in EOR, the revised Section 45Q framework has transformed surfactant-assisted CO₂ flooding from a marginal recovery technique into a core capital allocation strategy.

Under the updated regime, the tax credit for CO₂ utilized in EOR increased from USD 60 to USD 85 per metric ton, eliminating the historical bias toward pure sequestration projects. This change directly incentivizes operators to deploy surfactants that stabilize CO₂ foams and carbonated water, improving sweep efficiency while still qualifying for the full federal credit. In practical terms, surfactant EOR now operates as both a production-enhancement tool and a monetized carbon management pathway.

Economic modeling released in December 2025 by Enverus Intelligence illustrates the magnitude of this shift. Conventional EOR project costs have fallen by more than 40%, with PV-10 breakeven prices in several Permian Basin assets declining from approximately USD 28 per barrel to nearly USD 16 per barrel. At these levels, surfactant-enhanced CO₂ flooding is outperforming new unconventional drilling economics, repositioning chemical EOR as the lowest-risk growth lever for operators managing late-life reservoirs.

NOC-Driven Qualification of High-Temperature, High-Salinity Surfactants in Carbonates

A parallel structural trend is unfolding in the Middle East, where National Oil Companies are accelerating the qualification of High-Temperature, High-Salinity surfactants to unlock carbonate reservoirs that dominate global remaining conventional reserves. Operators such as Saudi Aramco and ADNOC are prioritizing chemical EOR systems capable of withstanding temperatures above 120°C and salinity levels approaching 170,000 ppm.

Field and pilot programs conducted during 2024–2025, including collaborative research with Khalifa University, have validated advanced Guerbet alkoxy betaine and zwitterionic surfactant blends under true reservoir conditions. These pilots demonstrated reductions in residual oil saturation from roughly 26% to 15%, translating into recovery factors as high as 68% of Original Oil in Place. Such performance metrics are redefining expectations for carbonate EOR, a segment long constrained by oil-wet rock behavior and surfactant instability.

The technical success is rooted in wettability alteration. Next-generation HTHS surfactants modify surface charge on carbonate minerals, driving a transition from oil-wet to water-wet conditions. This mechanism improves spontaneous imbibition and displacement efficiency, positioning surfactant EOR as a scalable solution for the Middle East’s most strategic assets rather than a niche chemical intervention.

Transition toward Bio-Based and Renewable-Carbon Surfactants

As ESG scrutiny intensifies across upstream portfolios, operators are increasingly evaluating bio-based surfactants not only for remediation but for active reservoir injection. Fermentation-derived biosurfactants such as rhamnolipids, sophorolipids, and amino-acid-based surfactants are gaining traction as lower-toxicity alternatives that align chemical EOR with corporate sustainability mandates.

In early 2025, chemical suppliers including Evonik and Stepan Company expanded qualification programs for glycolipid-based surfactants in oilfield applications. These materials offer superior biodegradability and reduced aquatic toxicity, mitigating environmental risk in the event of breakthrough to groundwater or offshore discharge zones.

Performance data is reinforcing adoption. A 2024 study from Changzhou University highlighted sodium cocoyl alaninate as a high-stability foaming agent in extreme salinity, outperforming several synthetic surfactants that suffer precipitation or phase separation. For offshore China, the North Sea, and other environmentally sensitive regions, this combination of reservoir performance and eco-compliance represents a structural opportunity rather than a branding exercise.

Viscoelastic Surfactants for Precision Conformance Control in Heterogeneous Reservoirs

One of the most compelling growth opportunities lies in Viscoelastic Surfactants designed for targeted conformance control. These systems form wormlike micellar networks that temporarily plug high-permeability thief zones, redirecting injected fluids into under-swept, oil-rich regions of the reservoir. Unlike polymer gels, VES systems offer reversible behavior that minimizes long-term formation damage.

Field applications expanded rapidly through 2025, particularly in structurally complex reservoirs. In the Sichuan Basin, nano-silica-modified VES systems demonstrated thermal stability at 140°C while achieving imbibition oil recovery rates exceeding 47% in tight formations. These results materially outperform conventional polymer diversion methods, especially in reservoirs where mechanical isolation is impractical.

The strategic advantage for operators is the self-breaking nature of VES chemistry. Upon contact with hydrocarbons or formation water, micellar structures disassemble naturally, restoring permeability without secondary chemical breakers. This reduces operational complexity, lowers post-treatment risk, and positions VES-enabled surfactant EOR as a precision tool for maximizing recovery in both conventional and unconventional settings.

Surfactant EOR Market Share and Segmentation Insights

Anionic Surfactants Lead Surfactant EOR Market with High Efficiency in Reservoir Conditions

Anionic surfactants accounted for 52.8% of the surfactant EOR market in 2025, driven by their superior interfacial tension reduction, low adsorption characteristics, and cost-effective performance in chemical enhanced oil recovery processes. Widely used in surfactant-polymer flooding and alkali-surfactant-polymer flooding, these surfactants enable efficient oil mobilization, particularly in sandstone reservoirs, where their negative charge minimizes retention. Their compatibility with large-scale EOR operations across mature oilfields reinforces demand. The 2025 technology trend focuses on high-salinity and high-temperature surfactant systems, where advanced sulfonate chemistries and co-surfactant formulations are engineered to maintain performance in harsh reservoir environments, expanding the applicability of chemical EOR in complex fields.

Onshore EOR Dominates Deployment Due to Operational Feasibility and Mature Field Economics

Onshore EOR accounted for 88.6% of surfactant EOR market demand in 2025, reflecting the operational advantages of deploying chemical EOR in land-based oilfields. Onshore environments provide better access to chemical injection infrastructure, storage, logistics, and produced fluid handling, making large-scale surfactant flooding economically viable. Mature oilfields in North America, China, and the Middle East continue to drive sustained demand for surfactant-based recovery techniques. The 2025 market trend highlights emerging offshore EOR opportunities, where declining recovery rates are prompting interest in compact, high-efficiency surfactant systems designed to address platform space constraints, chemical dosing limitations, and complex offshore production conditions.

Surfactant EOR Market Competitive Landscape

The surfactant EOR market in 2026 is driven by reservoir-specific formulations, HSHT-stable chemistries, and integrated ASP flooding systems. Competition focuses on ultra-low interfacial tension performance, biosurfactants, and digitalized injection monitoring to maximize oil recovery from complex deepwater and unconventional reservoirs.

BASF Advances Ultra-Low IFT Surfactants and Bio-Based cEOR Solutions via Verbund Integration

BASF leads the surfactant EOR market through advanced chemical flooding technologies and vertically integrated production. Its APG® and Aspiro® portfolios are engineered to achieve ultra-low interfacial tension below 10⁻³ mN/m, even under high-salinity and high-temperature reservoir conditions. The Zhanjiang Verbund site strengthens localized supply for Asia-Pacific EOR demand. BASF’s €1.7 billion cost optimization program supports reinvestment into green transformation and bio-based surfactants. The company is targeting CO2 emissions between 17.2 and 18.2 million metric tons in 2026, aligning with low-carbon oilfield operations. Its integration of sustainability and performance positions BASF as a benchmark in chemical EOR systems.

Stepan Expands Biosurfactant EOR and Alkoxylation Capacity for Unconventional Reservoir Applications

Stepan is strengthening its position in surfactant EOR through biosurfactant commercialization and regional production expansion. Its Pasadena alkoxylation facility supports customized surfactant blends for the Permian Basin and Gulf Coast projects. The acquisition of NatSurFact enables large-scale deployment of rhamnolipid-based surfactants with superior biodegradability. Stepan reported strong EBITDA growth driven by oilfield applications and increasing surfactant demand. Its PETROSTEP® series is widely used for wettability alteration in carbonate reservoirs, enhancing oil displacement efficiency. The company’s focus on unconventional shale and huff-and-puff operations supports growth in high-complexity reservoirs.

SNF Delivers Integrated ASP EOR Systems Through Syensqo Acquisition and Polymer Leadership

SNF has emerged as a dominant player in surfactant EOR by integrating polymer and surfactant technologies into unified ASP systems. The €135 million acquisition of Syensqo’s Oil & Gas division expands its portfolio with Geropon® and Rhodapex® surfactants. This enables single-source procurement for large-scale EOR projects, reducing operational complexity. SNF’s leadership in polyacrylamides ensures optimal viscosity control, improving sweep efficiency and minimizing fingering effects. The company achieved EcoVadis Platinum status, strengthening its position in environmentally regulated markets like the North Sea. Its combined polymer-surfactant expertise supports high-performance recovery in mature and offshore reservoirs.

Halliburton Integrates Digital Monitoring with Low-Dosage Surfactant Systems for Optimized Recovery

Halliburton is advancing surfactant EOR through digital integration and service-led chemical optimization. Its StreamStar™ technology enables real-time monitoring of surfactant breakthrough, improving injection efficiency and reservoir management. The company reported $22.2 billion in 2025 revenue, with strong contributions from its Completion and Production segment. Partnerships such as the PT Pertamina MOU support deployment of advanced EOR solutions in complex Indonesian reservoirs. Its LeFrac™ and Sustane™ surfactant lines are designed for effectiveness at lower concentrations, reducing chemical usage and operational costs. Halliburton’s closed-loop digital ecosystem enhances precision in chemical flooding applications.

ChampionX Focuses on Persistent Wettability Alteration and Integrated Chemical-Mechanical EOR Systems

ChampionX is positioning itself as a leader in production chemistry with advanced surfactant solutions for enhanced oil recovery. Its ParaClear system combines wax dispersion and surfactant functionality to improve flow assurance and recovery rates. The company is investing in persistent wettability alteration technologies that extend treatment effectiveness in reservoir rock formations. Localized blending facilities in the Permian Basin and Montney enable real-time customization of surfactant formulations. Its ESP Digital Ecosystem monitors the interaction between surfactants and pumping systems to optimize performance and equipment longevity. ChampionX’s integrated approach enhances recovery efficiency across unconventional and mature oilfields.

United States Surfactant EOR Market Driven by Permian Optimization and Carbon-Negative Integration

The United States surfactant EOR landscape is undergoing a technical recalibration centered on the Permian Basin, where operators have expanded the deployment of alkali-surfactant-polymer flooding to unlock incremental recovery from low-permeability reservoirs. These late-2025 programs are increasingly reliant on advanced anionic surfactants engineered to retain interfacial tension reduction at reservoir temperatures exceeding 85°C, addressing historical thermal degradation challenges. The integration of EOR chemistry with federal environmental priorities has become a defining theme, as 2025 guidelines accelerated the transition toward biodegradable biosurfactants derived from waste oils. This shift is directly linked to produced-water management, with operators reporting meaningful toxicity reductions relative to conventional petroleum sulfonates.

Carbon management incentives are reinforcing chemical EOR economics. Section 45Q tax credits have catalyzed projects that combine surfactant flooding with carbon capture and storage, enabling “carbon-negative oil” concepts in which surfactants enhance CO2 solubility in the oil phase. At the formulation level, Dow announced the commercialization of EOR-grade polyolefin elastomers in mid-2025, designed to stabilize surfactant micelles in ultra-high-salinity brines approaching 200,000 ppm TDS. Service integration is also deepening, with the Stepan-Nalco Tiorco joint venture expanding its reservoir cleaning and efficiency platforms, while early-2026 pilots in the deepwater Gulf of Mexico signal a gradual extension of surfactant EOR concepts into subsea environments where low-viscosity formulations are essential to minimize pumping energy.

India Surfactant EOR Market Anchored in Fiscal Stability and Digital Reservoir Intelligence

India’s surfactant EOR industry is transitioning from pilot-scale experimentation toward structured scale-up, underpinned by regulatory reforms that directly address investor risk. The Oilfields Regulation and Development Amendment Act of 2025 introduced fiscal stabilization clauses that shield chemical flooding projects from abrupt policy shifts, materially improving the investment profile of high-CAPEX EOR developments. Within this framework, ONGC initiated three new large-scale surfactant-polymer flooding projects across mature Western Offshore fields, explicitly targeting natural decline mitigation rather than frontier exploration.

Policy alignment extends beyond upstream regulation. The Hydrocarbon Exploration and Licensing Policy, particularly OALP Bid Round X, has embedded concessional royalty structures for operators deploying advanced recovery techniques, creating a financial incentive for surfactant-based EOR adoption. Sustainability credentials are also gaining prominence, with Indian Oil Corporation securing international certification for bio-intermediate production feeding into green EOR surfactant manufacturing. Complementing these moves, the Mission Anveshan digital upstream reform has enabled a national reservoir data bank, allowing formulators to simulate surfactant performance across diverse Indian basin chemistries. This data-driven approach is reducing formulation uncertainty and shortening field-deployment cycles.

China Surfactant EOR Market Defined by Scale, Custom Chemistry, and AI-Enabled Optimization

China remains the global reference market for surfactant EOR at scale, anchored by the Daqing Oilfield, which continues to refine its alkali-surfactant-polymer flooding architecture. In late 2025, operators reported a breakthrough in in-situ soap generation synergy, enabling a 15% reduction in injected surfactant volumes without compromising recovery efficiency. This optimization is particularly significant given national mandates under the 14th Five-Year Plan, which require EOR-derived oil to contribute 12% of total domestic production by 2026.

Technological depth is expanding through both formulation chemistry and manufacturing innovation. Sinopec successfully piloted zwitterionic surfactants capable of maintaining ultra-low interfacial tension at temperatures up to 120°C, addressing one of the most challenging high-temperature reservoir environments globally. Parallel to this, BASF has advanced circular chemical production concepts in Shanghai, adapting loop-based technologies to generate lower-carbon precursors for EOR surfactants. The launch of AI-controlled reactors in late 2025 has further enabled rapid synthesis of reservoir-specific surfactants, shortening development timelines for complex heavy-oil fields and reinforcing China’s leadership in custom EOR chemistry.

Oman Surfactant EOR Market Emerging Through Solar-Thermal and Regional Supply Integration

Oman is positioning itself as a testbed for low-carbon surfactant EOR integration, leveraging its solar resources and favorable project governance. In late 2025, Petroleum Development Oman inaugurated a pilot at the Amal field that combines solar-generated steam with surfactant injection, creating a hybrid thermal-chemical EOR model designed to materially reduce the carbon intensity of heavy-oil recovery. This approach aligns with broader Middle Eastern strategies to decarbonize enhanced recovery while sustaining production from mature assets.

Supply chain localization is reinforcing these pilots. SABIC expanded its regional specialty surfactant manufacturing footprint in 2025 to provide just-in-time delivery for Oman’s chemical EOR programs, cutting logistics costs and improving formulation responsiveness. Together, these developments highlight Oman’s role as a strategic demonstration market where renewable energy integration, specialty surfactant chemistry, and operational pragmatism intersect.

Comparative Snapshot: Surfactant EOR Industry by Country

Surfactant EOR Market County Level Snapshot

|

Country

|

Primary EOR Focus

|

Policy or Incentive Lever

|

Structural Differentiator

|

|

United States

|

ASP flooding and CCS integration

|

Section 45Q tax credits, green chemistry guidelines

|

Carbon-negative oil and high-salinity formulation expertise

|

|

India

|

SP flooding in mature offshore fields

|

Fiscal stabilization, OALP concessions

|

Digital reservoir simulation and investor de-risking

|

|

China

|

Large-scale ASP and HT reservoirs

|

14th Five-Year Plan EOR mandates

|

AI-tailored surfactants and unmatched deployment scale

|

|

Oman

|

Hybrid thermal-chemical EOR

|

Solar integration and regional supply hubs

|

Low-carbon EOR pilots with rapid logistics support

|

Surfactant EOR Market Report Scope

Surfactant EOR Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$121.2 Million

|

|

Market Size (2034)

|

$168.1 Million

|

|

Market Growth Rate

|

3.7%

|

|

Segments

|

By Surfactant Type (Anionic Surfactants, Non-Ionic Surfactants, Cationic Surfactants, Amphoteric and Zwitterionic Surfactants, Biosurfactants), By EOR Technique (Surfactant-Polymer Flooding, Alkali-Surfactant-Polymer Flooding, Micellar Flooding, Foam-Based EOR), By Reservoir Rock Type (Sandstone Reservoirs, Carbonate Reservoirs), By Application (Onshore EOR, Offshore EOR)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Schlumberger Limited, Halliburton Company, Baker Hughes Company, BASF SE, Dow Inc., Stepan Company, SABIC, Huntsman Corporation, Solvay SA, Clariant AG, Evonik Industries AG, SNF Group, Petroleum Development Oman, Oil and Natural Gas Corporation, Shell Chemicals

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Surfactant EOR Market Segmentation

By Surfactant Type

By EOR Technique

- Surfactant-Polymer Flooding

- Alkali-Surfactant-Polymer Flooding

- Micellar Flooding

- Foam-Based EOR

By Reservoir Rock Type

- Sandstone Reservoirs

- Carbonate Reservoirs

By Application

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Surfactant EOR Industry

- Schlumberger Limited

- Halliburton Company

- Baker Hughes Company

- BASF SE

- Dow Inc.

- Stepan Company

- SABIC

- Huntsman Corporation

- Solvay SA

- Clariant AG

- Evonik Industries AG

- SNF Group

- Petroleum Development Oman

- Oil and Natural Gas Corporation

- Shell Chemicals

*- List not Exhaustive