Tallow Fatty Acid Market 2025–2034: $88.5 Billion to $120.6 Billion at 3.5% CAGR Driven by Biofuel Feedstock Competition, EUDR Shifts, and Oleochemical Integration

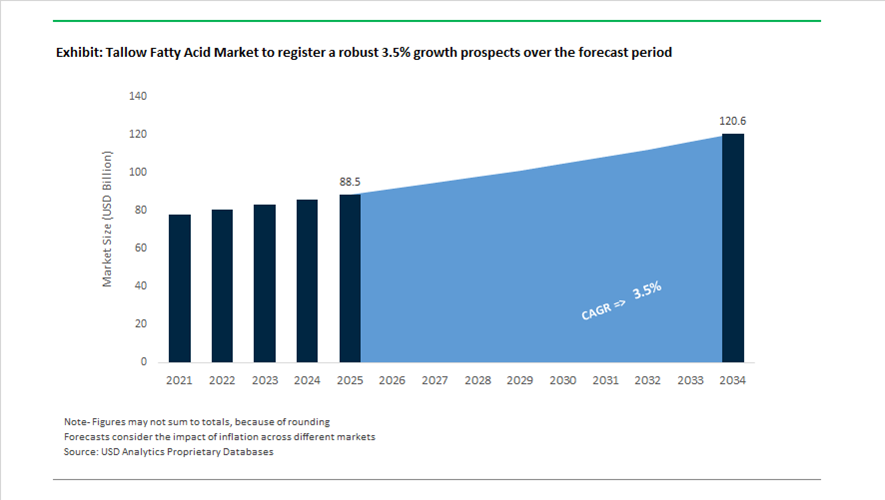

The global tallow fatty acid market is valued at $88.5 billion in 2025 and is projected to reach $120.6 billion by 2034, expanding at a CAGR of 3.5%. Tallow-derived fatty acids remain critical feedstocks for soaps, detergents, surfactants, lubricants, biodiesel, sustainable aviation fuel (SAF), and industrial oleochemicals. Market dynamics are increasingly shaped by biofuel policy incentives, renewable diesel tax credits, EU deforestation regulations, and traceable animal fat supply chains. As vegetable oil markets face sustainability scrutiny and price volatility, tallow has emerged as a deforestation-free alternative for European oleochemical producers and a premium feedstock for renewable diesel and SAF conversion, intensifying competition between energy and chemical end uses.

Strategic restructuring and regulatory developments accelerated during 2024 and 2025. In April 2024, Vantage Specialty Chemicals expanded its Leuna, Germany facility, increasing capacity for N-Methyl Taurine, a surfactant building block derived from fatty acids used in personal care and industrial formulations. In July 2024, Godrej Industries acquired an ethoxylation unit to strengthen downstream processing of fatty acid derivatives into specialty surfactants. In August 2024, JBS Foods redirected significant volumes of beef tallow toward SAF production, highlighting feedstock competition between fuels and traditional oleochemical sectors. In October 2024, Emery Oleochemicals expanded its bio-based polymer additive portfolio with USDA BioPreferred-certified fatty acid derivatives. In January 2025, implementation of the EU Deforestation Regulation tightened vegetable oil sourcing rules, prompting European manufacturers to pivot toward tallow as a compliant alternative. In February 2025, Brazil halted its biodiesel blend increase to B15, stabilizing local tallow prices after earlier speculative spikes. In June 2025, Wilmar International acquired full control of PZ Wilmar, consolidating its West African soap and oleochemical operations where tallow remains a core feedstock.

Industry consolidation and trade protection measures intensified in late 2025 and early 2026. In December 2025, Darling Ingredients and Tessenderlo Group agreed to combine collagen and gelatin businesses into a new entity, allowing Darling to sharpen its strategic focus on rendering and fats operations supporting biofuel markets. In the same month, Darling announced the sale of approximately $110 million in production tax credits generated by its Diamond Green Diesel joint venture, underscoring the financial scale of tallow-to-renewable diesel conversion. In March 2025, Vantage introduced a sustainable personal care ingredient range incorporating premium tallow derivatives for moisture barrier and bio-based skincare applications. In January 2026, Vantage filed anti-dumping and countervailing duty petitions against fatty acid imports from Indonesia and Malaysia, with investigations initiated in February 2026 to protect U.S. domestic producers.

Structural Trends and Commercial Opportunities in the Tallow Fatty Acid Market

Strategic Substitution in Metalworking Fluids Amid Vegetable Oil Price Volatility

The tallow fatty acid market is benefiting from a structural reformulation trend within industrial lubricants and metalworking fluids, driven primarily by cost volatility and supply risk in vegetable oil markets. As of mid-2025, the FAO Vegetable Oils Price Index recorded an 18.2% year-on-year increase, materially disrupting formulation economics for semi-synthetic and synthetic metalworking fluids. In response, lubricant formulators are accelerating the substitution of vegetable oil oleics with tallow-derived fatty acids to stabilize input costs while maintaining performance standards.

Price differentials are now sufficiently wide to drive non-discretionary switching. In September 2025, U.S. tallow fatty acid prices averaged around USD 1,431 per metric ton, supported by predictable domestic rendering supply chains. By contrast, palm oil prices exhibited sharp month-to-month volatility, including a near-5% rise in June 2025 alone. This divergence has made tallow-based oleic fractions increasingly attractive in machining, grinding, and cutting fluids, where lubricity, corrosion inhibition, and emulsion stability are critical but do not justify exposure to agricultural commodity shocks.

OEM-driven reformulation is reinforcing this trend. Advanced coolant systems launched during 2024–2025 increasingly rely on animal-derived fatty acids to achieve low-foaming behavior and extended sump life under high-speed machining conditions. High-performance fluid suppliers such as Master Fluid Solutions have integrated these feedstocks into next-generation products to meet the stringent ferrous rust protection and biostability requirements of aerospace and automotive manufacturing, effectively embedding tallow fatty acids deeper into industrial lubricant value chains.

Hydrogenation Capacity Expansion for Premium Soap and Surfactant Feedstocks

A second structural trend is the acceleration of hydrogenation and fractionation investments aimed at upgrading crude tallow into high-purity stearic acid and specialty fatty intermediates. Demand growth in personal care, industrial soaps, and surfactants is increasingly skewed toward “high-hardness” and performance-consistent formulations, where hydrogenated tallow fatty acids offer competitive advantages over both palm-based and petroleum-derived alternatives.

Strategic capacity expansion near feedstock sources is becoming a defining competitive advantage. In August 2025, Kao Chemicals commissioned a new tertiary amine production facility in Texas, leveraging proximity to U.S. meat-processing hubs. This integration reduces logistics costs, improves feedstock traceability, and supports the production of uniform soap noodles and fatty alcohol intermediates for global export markets.

Process innovation is further improving competitiveness. Enzymatic pretreatment and advanced hydrogenation technologies introduced in 2024–2025 have enhanced chain-length consistency and thermal stability of tallow-derived stearics. Companies such as Emery Oleochemicals have expanded European capacity specifically to serve textile finishing and industrial surfactant applications, where performance variability has historically constrained animal-fat-based inputs. These advances are repositioning hydrogenated tallow fatty acids from cost-driven substitutes to specification-grade ingredients.

Tallow-Based Bio-Lubricants for Agriculture and Construction Equipment

One of the most commercially attractive opportunities lies in the expansion of tallow-based bio-lubricants into agriculture, mining, and construction equipment. Environmental regulation is no longer confined to marine applications; terrestrial operations increasingly mandate Environmentally Acceptable Lubricants that meet OECD 301B “readily biodegradable” criteria. Tallow fatty acid esters provide a cost-effective pathway to meet these standards while delivering high load-carrying capacity.

Field validation in 2025 demonstrated that bio-based Universal Tractor Transmission Oils formulated with animal-derived esters maintained functional integrity for over 600 operating hours under real-world agricultural conditions. These results confirm that tallow-based EALs can withstand sustained mechanical stress, high torque, and variable temperatures without seal degradation or leakage.

Regulatory momentum further strengthens this opportunity. Mining and agriculture now represent the largest end-use segments for biolubricants, with operators increasingly specifying formulations that achieve at least 60% biodegradation within 28 days. Tallow-derived lubricants occupy a unique position by combining mineral-oil-like lubricity with renewable feedstock credentials, making them a “zero-compromise” solution for soil-sensitive environments.

Tallow Fatty Acid Derivatives as Sustainable Asphalt Modifiers

A second high-growth opportunity is emerging in infrastructure materials, where tallow fatty acid derivatives are being adopted as bio-modifiers for asphalt. Tallow-based amines and amides function as plasticizers and adhesion promoters, improving aggregate binding and pavement durability while reducing lifecycle emissions.

Quantified sustainability benefits are driving interest from transport authorities. Late-2025 research indicates that incorporating just 1% bio-oil or fatty-acid-based modification into annual asphalt output could recycle more than 6,200 tonnes of waste oil and avoid approximately 31,300 tonnes of CO2 emissions per year. Performance gains are equally compelling, with dynamic stability improvements of up to 87%, directly addressing rutting and deformation in high-traffic corridors.

Warm-Mix Asphalt technologies further amplify demand. Tallow fatty acid derivatives enable asphalt production and laying at lower temperatures, cutting fuel consumption and reducing exposure to hazardous fumes during paving. As infrastructure agencies in Europe, China, and other major markets increasingly mandate low-carbon construction practices, these bio-binders are transitioning from pilot-scale trials to standardized procurement specifications, positioning the tallow fatty acid market as an indirect beneficiary of global infrastructure decarbonization.

Tallow Fatty Acid Market Share and Segmentation Insights

Saturated Fatty Acids Lead Tallow Fatty Acid Market with Stability and Industrial Performance Benefits

Saturated fatty acids accounted for 48.60% of the tallow fatty acid market in 2025, driven by their critical role in delivering oxidative stability, hardness, and consistent performance across industrial and consumer applications. Key components such as stearic acid and palmitic acid are widely used in soap manufacturing, rubber processing, lubricants, and cosmetics, where solid structure and thermal stability are essential. Their compatibility with large-scale processing supports high-volume consumption. The 2025 trend centers on tallow fractionation and value-added derivatives, where producers isolate high-purity saturated fractions to meet demand for precision melting points and functional performance, particularly in pharmaceutical and personal care formulations.

Soaps and Detergents Segment Drives High-Volume Tallow Fatty Acid Consumption

Soaps and detergents accounted for 42.80% of tallow fatty acid market demand in 2025, reflecting the material’s long-standing role as a primary feedstock for bar soap production and cleaning formulations. Tallow-derived fatty acids provide excellent lathering, hardness, and durability, making them ideal for both mass-market and specialty soaps. The scale of global hygiene product consumption ensures stable demand. The 2025 market dynamic highlights natural and heritage soap positioning, where tallow-based formulations gain traction in artisanal and premium segments, while industrial manufacturers increasingly adopt blended feedstocks combining tallow and vegetable oils to optimize cost, performance, and sustainability.

Tallow Fatty Acid Market Competitive Landscape

The tallow fatty acid market in 2026 is shaped by vertical integration, tariff-driven feedstock volatility, and circular bio-refining investments. Leading producers are advancing selective hydrogenation and fractionation to deliver high-purity fatty acids for surfactants, polymers, and renewable fuels, aligning with global mandates for bio-based and low-carbon chemical inputs.

Darling Ingredients Leverages Render-to-Refine Integration to Dominate Low-Carbon Tallow Value Chains

Darling Ingredients leads the tallow fatty acid market through its fully integrated rendering and refining model, generating $6.1 billion in revenue and $1.03 billion EBITDA in 2025. Portfolio optimization included $58 million in restructuring to prioritize high-margin oleochemicals and fuel streams. The company monetized $255 million in IRA tax credits, funding upgrades in fractionation for ultra-pure stearic acid production. Its Diamond Green Diesel joint venture sold over 1 billion gallons, establishing a major demand sink for low-carbon tallow feedstocks. Strong vertical integration mitigates tariff-driven price volatility and ensures consistent feedstock supply. Focus remains on renewable fuels and high-performance fatty acid derivatives.

Godrej Industries Expands Global Bio-Chemical Footprint with Large-Scale Capacity Investments

Godrej Industries is scaling its oleochemicals business with a ₹750 crore investment to expand fatty alcohol, erucic acid, and specialty chemical capacities. The company is tripling specialty chemicals output to target Europe and North America demand for bio-based surfactants and polymers. Its manufacturing network across India supports exports to over 80 countries, strengthening global supply capabilities. Integration of biocatalysis and fermentation reduces carbon intensity of fatty acid derivatives. Renewable energy adoption is expected to reach 75% across operations in 2026, enhancing ESG positioning. Strategic focus is on customized fatty acid solutions for personal care, agrochemicals, and oilfield applications.

Vantage Specialty Chemicals Focuses on Traceable High-Purity Tallow Derivatives for Life Sciences and Polymers

Vantage is strengthening its position in high-value tallow fatty acid derivatives through advanced distillation and fractionation technologies. Its strategy emphasizes traceability and chain-of-custody certification, addressing rising demand for sustainable oleochemicals. Supply chain optimization in North America reduces exposure to import tariffs and volatile global pricing. The company produces high-purity fatty acid isomers for pharmaceutical excipients and specialty lubricants. Tallow-based stearates remain a core offering for rubber and plastics, enhancing stability and processing efficiency in automotive applications. Focus on circular alternatives positions Vantage as a key supplier in bio-based industrial materials.

Twin Rivers Technologies Enhances Domestic Supply Security with Versatile Fat Processing Capabilities

Twin Rivers Technologies is a major North American producer of distilled tallow fatty acids, leveraging its strategically located deepwater port facility in Massachusetts. Its integrated logistics network supports large-scale imports and domestic distribution of animal fats. The company manufactures over 80 fatty acid and glycerin products using hydrolysis, crystallization, and hydrogenation processes. TRT is intensifying its focus on sustainable, naturally derived ingredients for personal care and health sectors. Its DTFA products serve as key inputs for detergents and textile chemicals requiring consistent quality. Domestic production capability strengthens supply assurance amid global trade disruptions.

Kao Corporation Integrates Enzyme Technology to Develop Low-Carbon Surfactant-Grade Fatty Acids

Kao Corporation is advancing its chemical segment through bio-based innovation and enzyme-driven processing technologies. The company targets ¥1,750 billion in sales for 2026, supported by growth in high-margin chemical products. Its participation in NEDO-backed biomass saccharification projects enhances feedstock diversification for fatty acid production. Kao is integrating enzyme platforms into tallow processing to create milder, eco-friendly surfactants. Expansion under the K27 strategy focuses on global personal care and industrial chemical markets. Bio-aromatic and sustainable chemistry innovations strengthen its position in renewable oleochemical applications.

Emery Oleochemicals Advances High-Performance Green Lubricants Using Tallow-Based Feedstocks

Emery Oleochemicals is a global leader in natural-based oleochemicals, focusing on high-performance esters derived from tallow fatty acids. Its strategy emphasizes green lubricants as alternatives to synthetic PAOs in industrial and automotive applications. Advanced digital process controls enhance purity and consistency in splitting and distillation operations. Emery’s stearic acid grades are widely used in elastomers and textiles, offering superior oxidative stability and moisture resistance. Procurement restructuring mitigates the impact of tariff-driven feedstock price spikes. Strong global sourcing network supports resilient supply of tallow-based intermediates for specialty chemical markets.

United States Tallow Fatty Acid Market Accelerated by Biofuels Policy and Domestic Capacity

The United States has emerged as a pivotal market where tallow fatty acids are transitioning from secondary oleochemical inputs to strategic biofuel feedstocks. According to the U.S. Energy Information Administration, tallow inputs for biodiesel rose sharply in early 2025, increasing by 26.5% between January and May to reach 3.6 billion pounds. This surge temporarily exceeded soybean oil usage during Q1, underscoring a structural pivot toward animal fats as refiners seek lower-carbon, non-food competing feedstocks. The shift is reinforced by downstream investments, including Coast Packing Co.’s new refinery project in Amarillo, Texas, which will materially expand domestic processing of animal fats into shortenings and fatty acids when commissioned in 2026.

Policy architecture is amplifying this momentum. The U.S. Treasury’s Clean Fuel Production Credit under Section 45Z, effective January 2025, introduced carbon-intensity scoring that directly rewards rendering and fractionation efficiency. Tallow processors have responded by optimizing temperatures and refining protocols to reduce CI scores for renewable diesel and SAF blending. Trade protection has further tightened the domestic loop, with a 10% levy on imported tallow imposed in April 2025 to secure local supply for aviation fuels. Commercial validation arrived in late 2024 when Darling Ingredients and its Diamond Green Diesel joint venture delivered the first SAF batch derived from animal tallow to Avfuel Corporation, confirming tallow fatty acids as a high-value energy carrier rather than a residual byproduct.

Brazil Tallow Fatty Acid Market Redirected Toward Domestic Biodiesel and Certified Exports

Brazil’s tallow fatty acid landscape has been reshaped by external trade barriers and strong internal demand. Following U.S. tariff implementation in 2025, Brazil’s biodiesel sector rapidly absorbed surplus animal fats, lifting the tallow inclusion rate in biodiesel blends from 5% in July to 9.5% by October 2025. This domestic pull has reduced exposure to volatile export channels while stabilizing utilization across rendering operations tied to Brazil’s large beef and pork industries.

At the same time, exporters have recalibrated toward higher-compliance markets. Major integrated meat processors such as JBS have prioritized ISCC certification to access the European renewable energy value chain under revised RED III rules. Beyond fuels, Brazil is pushing functional diversification, with rendering innovation programs announced in 2024 to channel beef tallow and pork lard into aviation fuel and industrial ester initiatives. Pricing dynamics support this strategy, as late-2025 FOB Santos tallow prices stabilized near USD 1,050 to 1,080 per metric ton, maintaining competitiveness versus plant-derived oleic acids in soaps and detergents while preserving margins for energy applications.

China Tallow Fatty Acid Market Shaped by Import Reconfiguration and Specialty Applications

China’s tallow fatty acid market is increasingly characterized by supply chain diversification and application upgrading. After tariffs on certain animal fat imports escalated to 54% in early 2025, Chinese oleochemical producers reduced reliance on Western suppliers and diversified sourcing toward Southeast Asia and Latin America to maintain feedstock continuity for rubber, plastics, and surfactant manufacturing. This shift has reinforced China’s procurement flexibility while insulating downstream industries from geopolitical volatility.

Domestically, investment is moving up the value curve. In late 2025, Zhejiang Jinke Household Chemical Materials expanded specialty oleochemical units in the Tianjin Nangang Industrial Zone, targeting high-purity stearic and oleic acid derivatives for electronics coatings. R&D momentum is also evident, with Chinese material scientists prototyping tallow-derived fatty acid salts for OLED encapsulation in 2025, exploiting the molecular stability of bovine lipids. Under the Ministry of Industry and Information Technology modernization plan, enzymatic hydrolysis is being mandated across fatty acid production to cut the surfactant sector’s carbon footprint by 15%, reinforcing sustainability credentials without sacrificing scale.

India Tallow Fatty Acid Market Supported by Upgrading and Fiscal Incentives

India’s tallow fatty acid market is transitioning from volume-driven soap inputs to higher-purity personal care and functional intermediates. In 2025, domestic processors including Godrej Agrovet and Amar Tallow Industries announced refining upgrades aimed at producing low-color, cosmetically acceptable fatty acids for premium soaps and personal care formulations. This technical upgrading aligns with rising domestic demand for differentiated, biodegradable ingredients in FMCG and institutional cleaning products.

Fiscal and regulatory levers are reinforcing adoption. The Ministry of Finance’s 2025 tax rationalization reduced GST on biodegradable surfactants derived from tallow fatty acids, improving cost parity with petroleum-based alternatives. Beyond detergents, agrochemical manufacturers increased the use of tallow-based emulsifiers by 12% in 2025 as they sought natural stabilizers that comply with tighter EU residue limits on exported crop protection products. This cross-sector pull is positioning tallow fatty acids as a versatile, compliance-friendly oleochemical input within India’s broader specialty chemicals ecosystem.

Comparative Snapshot: Tallow Fatty Acid Market by Country

Tallow Fatty Acid Market County Level Snapshot

|

Country

|

Primary Driver

|

Strategic Shift

|

Industrial Outcome

|

|

United States

|

Biofuels policy and SAF demand

|

CI-optimized rendering and trade protection

|

Tallow repositioned as premium energy feedstock

|

|

Brazil

|

Biodiesel absorption and export realignment

|

ISCC-certified diversification

|

Stable domestic demand and EU market access

|

|

China

|

Tariff-driven sourcing change

|

Enzymatic, low-carbon processing

|

Move toward electronics and specialty uses

|

|

India

|

Refining upgrades and tax incentives

|

Higher purity and functional emulsifiers

|

Expansion beyond soaps into personal care and agrochemicals

|

Tallow Fatty Acid Market Report Scope

Tallow Fatty Acid Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$88.5 Billion

|

|

Market Size (2034)

|

$120.6 Billion

|

|

Market Growth Rate

|

3.5%

|

|

Segments

|

By Product Type (Saturated Fatty Acids, Monounsaturated Fatty Acids, Polyunsaturated Fatty Acids), By Form (Solid, Liquid), By Grade (Food Grade, Technical Grade, Pharmaceutical and Cosmetic Grade), By Application (Soaps and Detergents, Rubber and Plastics, Personal Care and Cosmetics, Biofuels, Lubricants and Greases, Animal Feed)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Darling Ingredients Inc., BASF SE, Oleon NV, Emery Oleochemicals, Twin Rivers Technologies, Inc., VVF LLC, Vantage Oleochemicals, Inc., JBS S.A., Cargill, Incorporated, Godrej Agrovet, Saria SE & Co. KG, Acme-Hardesty Co., Wilmar International Ltd., Kuala Lumpur Kepong Berhad

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Tallow Fatty Acid Market Segmentation

By Product Type

- Saturated Fatty Acids

- Monounsaturated Fatty Acids

- Polyunsaturated Fatty Acids

By Form

By Grade

- Food Grade

- Technical Grade

- Pharmaceutical and Cosmetic Grade

By Application

- Soaps and Detergents

- Rubber and Plastics

- Personal Care and Cosmetics

- Biofuels

- Lubricants and Greases

- Animal Feed

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Tallow Fatty Acid Industry

- Darling Ingredients Inc.

- BASF SE

- Oleon NV

- Emery Oleochemicals

- Twin Rivers Technologies, Inc.

- VVF LLC

- Vantage Oleochemicals, Inc.

- JBS S.A.

- Cargill, Incorporated

- Godrej Agrovet

- Saria SE & Co. KG

- Acme-Hardesty Co.

- Wilmar International Ltd.

- Kuala Lumpur Kepong Berhad

*- List not Exhaustive