Tube and Stick Packaging Market Overview: Growth Driven by Convenience and Sustainable Innovation

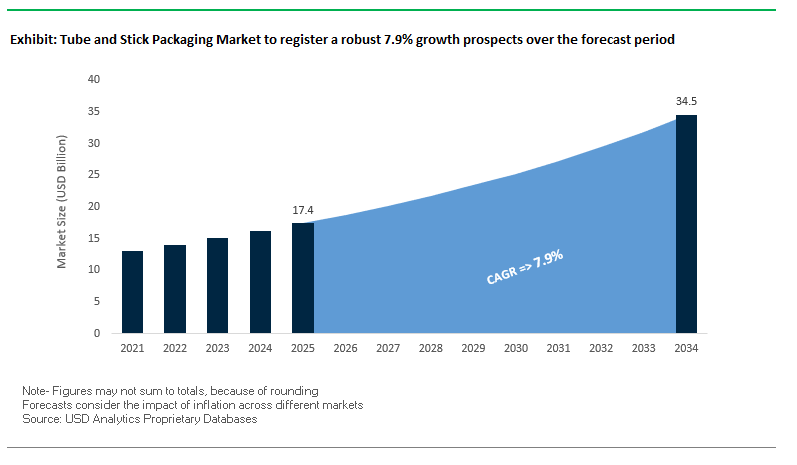

The Global Tube and Stick Packaging Market is projected to reach $17.4 billion in 2025 and is expected to grow to $34.5 billion by 2034, expanding at a robust CAGR of 7.9%. This growth is fueled by the rising demand for portable, portion-controlled packaging formats in personal care, cosmetics, food, and pharmaceuticals. Tubes and sticks have emerged as highly functional solutions, offering consumers easy dispensing, reduced product waste, and enhanced portability qualities aligned with today’s on-the-go lifestyle.

Plastic and laminated tubes continue to dominate the market, particularly in oral care and beauty applications, where barrier performance and lightweight design are crucial. However, sustainability trends are reshaping the sector, with growing adoption of PCR-based tubes, bio-plastics, and paper formats. The surge in e-commerce has further boosted demand for visually appealing packaging that elevates the unboxing experience, making tube and stick packaging not only a protective medium but also a brand communication tool.

Key Insights for Industry Professionals

- Plastic and laminated tubes dominate due to superior barrier properties, flexibility, and lightweight design.

- Convenience and portability drive demand in personal care, cosmetics, and pharmaceuticals.

- Sustainability is reshaping the industry, with brands investing in PCR plastics, bio-based tubes, and recyclable paper formats.

- E-commerce unboxing experiences are accelerating demand for premium, visually appealing tubes and sticks.

Market Analysis: Strategic Developments in the Tube and Stick Packaging Industry

The tube and stick packaging industry has witnessed major strategic shifts and innovations, highlighting a transition toward sustainable solutions and operational efficiency. In August 2025, EPL Limited announced its 11th consecutive quarter of margin expansion, underlining its success in operational excellence and sustainable growth. During the same month, Packsys introduced its “noSho” cap-free tube, a high-end cosmetic innovation that reduces plastic usage by up to 80%, a breakthrough in material reduction.

In July 2025, Neopac strengthened its leadership team by appointing a new Chief Sales Officer, positioning itself to capture global sales opportunities. Just a month earlier, in June 2025, Neopac earned a WorldStar Award for its Polyfoil® Mono-Material Barrier Tube developed for Colgate’s Elmex toothpaste, showcasing its advancements in recyclable, high-barrier packaging. Its innovation streak continued in May 2025, when Neopac India won dual honors at the FIPS Awards for its PaperX Tube and PCR-infused tube, marking significant recognition in both sustainability and product innovation.

Strategic realignment is also shaping the industry. In April 2025, Hoffmann Neopac divested its tin business to Massilly Group, allowing sharper focus on its tube packaging segment. Earlier, in October 2024, Neopac expanded its pharmaceutical portfolio by introducing Polyfoil® Mono-Material Barrier Mini Tubes at CPHI Milan. Meanwhile, industry consolidation gained pace when Impel Services of India acquired Wimco Ltd. in September 2024, signaling expansion into primary packaging machinery to strengthen upstream capabilities.

Tube and Stick Packaging Market: Emerging Trends and Growth Opportunities

Strategic Shift Towards Monomaterial Plastic Structures

The tube and stick packaging market is experiencing a decisive transformation as manufacturers move from traditional multi-layer laminated tubes toward fully recyclable monomaterial polypropylene (PP) and polyethylene (PE) structures. This shift is being accelerated by Extended Producer Responsibility (EPR) regulations, which require producers to assume financial and logistical accountability for packaging end-of-life management. Industry groups such as the European Tube Manufacturers Association (ETMA) are prioritizing recyclable tube solutions, while multinational corporations including Colgate-Palmolive and Unilever have pledged to transition their portfolios toward monomaterial designs.

Technological advancements are making monomaterial structures viable substitutes for multi-material laminates. Modern PP and PE tubes now incorporate integrated EVOH barrier layers, ensuring effective protection against oxygen and moisture without disrupting recycling compatibility. Neopac’s award-winning Polyfoil® Mono-Material Barrier Tube for Elmex exemplifies this balance of sustainability and product protection. Beyond compliance, monomaterial adoption is also streamlining manufacturing workflows: production runs benefit from reduced injection cycle times, lower energy usage, and simplified assembly processes. For recyclers, these designs increase the purity of recovered material streams, making the monomaterial trend a dual solution for operational efficiency and sustainability.

Proliferation of Stick Formats for Precision Dosing and Portability

Stick packaging formats are rapidly expanding into new product categories, evolving beyond their traditional role in lip balms and pharmaceuticals. The format’s success stems from its ability to deliver portability, convenience, and precision dosing, attributes that resonate strongly with consumers in health, wellness, and food sectors. As demand for single-serve, on-the-go solutions grows, stick formats are being widely adopted in skincare serums, protein powders, nutraceuticals, and instant beverages.

The appeal of stick packs lies in their pre-measured, single-use convenience. For supplements, pre-workout powders, or probiotics, the format ensures accurate dosage, minimizes waste, and enhances hygiene by eliminating the need for shared scoops or utensils. This trend aligns with the consumer shift toward healthier lifestyles, where portion control and portability are paramount. Moreover, brands are extending stick applications into innovative areas such as concentrated cleaning solutions, premium coffee, and even liquid serums, positioning them as a mess-free and modern alternative to bulky jars or bottles. As more categories embrace this format, stick packaging is cementing its role as a high-growth packaging solution across diverse industries.

Integration of Barrier Technologies for Sensitive Biologics

A major growth opportunity lies in the development of advanced barrier technologies tailored for biologics, probiotics, and nutraceuticals, where packaging integrity directly impacts product efficacy and shelf life. These products are highly sensitive to oxygen and moisture, demanding robust barrier solutions to maintain stability under stringent regulatory and storage conditions. Emerging innovations, such as transparent vacuum-deposited coatings and barrier-enhanced polymers, are raising performance benchmarks.

For instance, multilayer EVOH integration at critical tube points, like the molded shoulder, significantly enhances oxygen resistance. Aisa’s Bacomex™ technology demonstrates how embedded EVOH layers can deliver barrier improvements up to 18 times greater than conventional designs. Such solutions are crucial for pharmaceutical-grade applications where sterility, durability, and regulatory compliance are non-negotiable. As biologics and functional health products continue to dominate the market, the need for specialized barrier technologies positions tubes and sticks as a competitive packaging choice capable of safeguarding product value while meeting sustainability mandates.

Development of Water-Soluble or Edible Film Stick Packaging

An emerging frontier for the stick packaging market is the introduction of water-soluble and edible films, particularly for single-dose applications in food, beverage, agriculture, and household products. By replacing traditional wrappers with polyvinyl alcohol (PVA) or bio-based edible films, this innovation eliminates post-consumer packaging waste altogether.

The consumer experience is central to this opportunity. For instant coffee or dietary supplements, a water-soluble stick can be dropped directly into a cup, dissolving without residue and releasing the product seamlessly. This user-friendly functionality, already proven in laundry and dishwasher pods, is now being extended into food, beverage, and agricultural applications such as fertilizers and pesticides. By combining convenience with sustainability, water-soluble stick packaging aligns with consumer expectations for eco-friendly solutions while unlocking new product delivery formats. As adoption scales, this innovation could redefine how single-serve packaging is perceived, opening growth pathways in markets demanding sustainability without compromising convenience.

Competitive Landscape: Global Leaders in Tube and Stick Packaging

The competitive landscape is shaped by a mix of global packaging giants and specialized tube manufacturers, each investing in sustainability, material innovation, and regional expansions to strengthen their market share.

Albéa Group: Leading Beauty and Personal Care Tube Solutions

Albéa Group is a global leader in personal care and beauty packaging, producing more than 8 billion tubes annually. Its innovation strategy is anchored in sustainability, exemplified by its partnership with L’Oréal to launch a cardboard-based tube that reduces plastic content by 45%. Albéa is targeting full recyclability across its cosmetic and oral care tubes by 2025, with greater use of PCR content and lightweight designs. With 23 industrial sites across 14 countries, Albéa ensures localized supply chains and reduced carbon footprints, supporting its global customer base.

EPL Limited: Driving Global Expansion and Sustainability Commitments

EPL Limited (formerly Essel Propack) is a key player in laminated and co-extruded tubes across oral care, cosmetics, and pharma. The company is expanding its footprint, with a greenfield project in Thailand announced in 2024 to meet rising Asian demand. EPL’s sustainability agenda is reinforced by its commitment to SBTi and a CDP ‘A’ rating in Climate, Water, and Supplier Engagement. Operating 21 plants in 11 countries, EPL continues to expand through acquisitions and joint ventures, underscoring its vision to become the most sustainable packaging company worldwide.

Berry Global: Expanding Reach Through Acquisitions and Innovation

Berry Global leverages its global scale to dominate plastic tube and stick packaging, particularly in deodorants, personal care, and flexible tubes. Its landmark 2019 acquisition of RPC Group positioned Berry as a leading force in plastic packaging with expanded design and manufacturing capabilities. The company emphasizes circularity and recyclability, while also excelling in high-impact decoration and printing technologies. Its award-winning tube designs demonstrate expertise in premium graphics and advanced finishing that enhance brand differentiation.

Hoffmann Neopac AG: Innovating High-Barrier and Sustainable Tubes

Hoffmann Neopac specializes in high-barrier tubes for pharmaceuticals, cosmetics, and oral care. In April 2025, it sold its tin division to Massilly Group to sharpen focus on tubes, reinforcing its strategy to lead in sustainable innovations. Its Polyfoil® Mono-Material Barrier Tubes deliver strong protection against oxygen, light, and moisture while being fully recyclable. The company’s PaperX Tube, a fiber-based solution with excellent sealability, further emphasizes its leadership in sustainable and high-performance packaging.

Constantia Flexibles: Championing Flexible and Eco-Friendly Packaging

Constantia Flexibles delivers laminates, pouches, and tubes for food, pharma, and pet care. A pioneer in sustainable packaging, it has won multiple awards, including two WorldStar Global Packaging Awards in 2025 for its EcoPeelCover and EcoLamHighPlus solutions. The company’s Centers of Competence drive innovations in material science, food compliance, and raw material optimization. Constantia’s portion-control and single-serve packs are widely used across nutraceutical and food sectors, aligning with the growing consumer demand for convenient and sustainable stick packaging formats.

Tube and Stick Packaging Market Share Insights

Squeeze Tubes Hold the Largest Market Share by Product Type in Tube & Stick Packaging

Squeeze tubes command 45% of the tube and stick packaging market, underscoring their unmatched versatility, superior barrier protection, and user-friendly functionality across industries ranging from personal care to pharmaceuticals and industrial adhesives. Their leadership is anchored in material innovation laminate tubes with high-barrier layers combine lightweight convenience with superior product protection while collapsibility minimizes waste. While aluminum tubes retain a premium image in select categories, mono-material recyclable plastics are rapidly gaining traction to meet global sustainability mandates. The format’s ability to support clean dispensing, portability, and premium aesthetics ensures that squeeze tubes remain the preferred choice for both mass-market and luxury applications.

Cosmetics & Personal Care Dominate Market Share by End-Use Industry in Tube & Stick Packaging

Cosmetics and personal care applications hold the largest 35% share of the tube and stick packaging market, driven by their dual requirement for functional protection and high-end branding. Tubes safeguard sensitive formulations such as serums, creams, and lotions from oxygen and light exposure while providing portability and consumer convenience. At the same time, their customizable shapes, premium laminate finishes, and advanced applicator tips transform them into critical brand-building tools on the retail shelf and in the consumer’s daily routine. The dominance of this segment is reinforced by the growth of premium skincare, travel-sized products, and the rising emphasis on sustainable beauty packaging, with brands adopting recyclable laminates and mono-material solutions to align with eco-conscious consumer values.

United States: Innovation and Sustainability Transform Tube and Stick Packaging

The U.S. tube and stick packaging market is being driven by rising demand for convenient, on-the-go products, particularly in the cosmetics, personal care, and food and beverage sectors. Consumers increasingly prefer portable, single-serve formats, fueling innovation in stick packs for dietary supplements and OTC medications, as well as tubes for lotions and sunscreens. Technological advancements in high-speed, multi-lane packaging machinery and barrier technologies are enhancing production efficiency and extending product shelf life.

Sustainability remains a key trend, with manufacturers adopting recyclable, paper-based, and mono-material solutions. Leading players like Berry Global are expanding product lines and investing in lightweighting and post-consumer recycled (PCR) content, reflecting growing corporate initiatives toward eco-friendly tube and stick packaging. The market also emphasizes pre-measured stick packs, offering convenience and discretion for health-conscious consumers.

Germany: Circular Economy and Advanced Machinery Driving Market Leadership

Germany’s tube and stick packaging industry is shaped by a stringent regulatory framework, including the EU Packaging and Packaging Waste Regulation (PPWR 2025), which drives demand for eco-friendly and fully recyclable packaging. The country is a leader in the circular economy, with packaging designed for high recyclability and recycled content, enforced by laws such as the Verpackungsgesetz (Packaging Act).

Technological innovation is another critical factor. German manufacturers are exploring mono-material films for recyclability and collaborating to integrate stick packaging into supply chains efficiently. Additionally, advanced high-speed filling and sealing machinery enhances production quality and efficiency. The combination of regulatory support, innovation, and machinery capability positions Germany as a global hub for sustainable and technologically advanced tube and stick packaging solutions.

China: E-Commerce Expansion and Carbon-Neutral Goals Accelerate Market Growth

China’s tube and stick packaging market is being driven by governmental initiatives aimed at achieving dual carbon goals, promoting eco-friendly and reusable materials across the packaging sector. Technological investments, including automation, AI, and “5G plus industrial internet”, are optimizing production processes and improving flexible manufacturing capacity.

Rapid urbanization, rising incomes, and changing lifestyles are fueling demand for convenient, ready-to-use products, including stick packs for instant coffee and nutraceutical powders and tubes for personal care products. E-commerce growth is a significant driver, with a focus on secure, tamper-proof packaging made from recyclable or biodegradable materials. The cosmetics and personal care sector particularly benefits from sophisticated tube and stick packaging for facial cleansers, lotions, and sunscreens.

India: Regulatory Support and Infrastructure Investments Boost Sustainable Packaging

India’s tube and stick packaging industry is benefiting from government initiatives such as Make in India and Zero Effect Zero Defect, which promote quality domestic production and sustainable packaging solutions. The National Packaging Initiative (2021) also encourages logistics efficiency, product safety, and sustainable practices.

Growing demand is driven by rising disposable income, urbanization, and changing consumer preferences toward convenient, single-serve products. Investments in high-speed stick and tube packaging machinery are scaling production to meet new government mandates. Regulatory measures like the Plastic Waste Management (Amendment) Rules are accelerating the shift toward eco-friendly laminated and paper-based tubes, positioning India as a rapidly expanding market for sustainable and technologically advanced packaging solutions.

Tube and Stick Packaging Market Report Scope

Tube and Stick Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$17.4 Billion

|

|

Market Size (2034)

|

$34.5 Billion

|

|

Market Growth Rate

|

7.9%

|

|

Segments

|

By Material Type (Plastics, Paper, Aluminum, Bioplastics, Laminated Materials, Other Materials), By Product Type (Squeeze Tubes, Twist Tubes, Cartridges, Stick Packs, Other Product Types), By End-Use Industry (Food & Beverages, Pharmaceuticals & Healthcare, Cosmetics & Personal Care, Industrial & Household, Other Industries), By Filler Type (Powders & Granules, Liquids, Semi-Solids)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, Albéa Group, EPL Limited (formerly Essel Propack), Berry Global Inc., Mondi Group, Sonoco Products Company, Constantia Flexibles, Huhtamaki Oyj, CCL Industries Inc., Hoffmann Neopac, Unither Pharmaceuticals SAS, Glenroy, Inc., Montebello Packaging, AptarGroup, Inc., Greiner Packaging International GmbH

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Tube and Stick Packaging Market Segmentation

By Material Type

- Plastics

- Paper

- Aluminum

- Bioplastics

- Laminated Materials

- Other Materials

By Product Type

- Squeeze Tubes

- Twist Tubes

- Cartridges

- Stick Packs

- Other Product Types

By End-Use Industry

- Food & Beverages

- Pharmaceuticals & Healthcare

- Cosmetics & Personal Care

- Industrial & Household

- Other Industries

By Filler Type

- Powders & Granules

- Liquids

- Semi-Solids

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Tube and Stick Packaging Market

- Amcor plc

- Albéa Group

- EPL Limited (formerly Essel Propack)

- Berry Global Inc.

- Mondi Group

- Sonoco Products Company

- Constantia Flexibles

- Huhtamaki Oyj

- CCL Industries Inc.

- Hoffmann Neopac

- Unither Pharmaceuticals SAS

- Glenroy, Inc.

- Montebello Packaging

- AptarGroup, Inc.

- Greiner Packaging International GmbH

* List Not Exhaustive

Methodology

USDAnalytics employed a comprehensive research methodology to provide a robust and actionable analysis of the global Tube and Stick Packaging Market. Our approach combined extensive primary research, including interviews with packaging manufacturers, brand owners in personal care, cosmetics, pharmaceuticals, and food sectors, as well as sustainability and supply chain experts, with secondary research from industry publications, company filings, press releases, and trade events like FIPS and CPHI Milan. Market sizing, growth forecasts, and CAGR estimates were derived from historical trends, emerging innovations in monomaterial and barrier technologies, and the rapid adoption of stick formats and sustainable tubes. Segmentation covered material type, product type, end-use industry, and filler type, while qualitative insights highlighted strategic initiatives, mergers, acquisitions, technological advancements, and regulatory impacts, including Extended Producer Responsibility (EPR) and national sustainability mandates. This methodology ensures USDAnalytics delivers industry professionals a forward-looking, data-driven perspective on market opportunities, competitive dynamics, and sustainability-driven growth trends shaping tube and stick packaging worldwide.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.