Water Utility Management Systems Market Overview

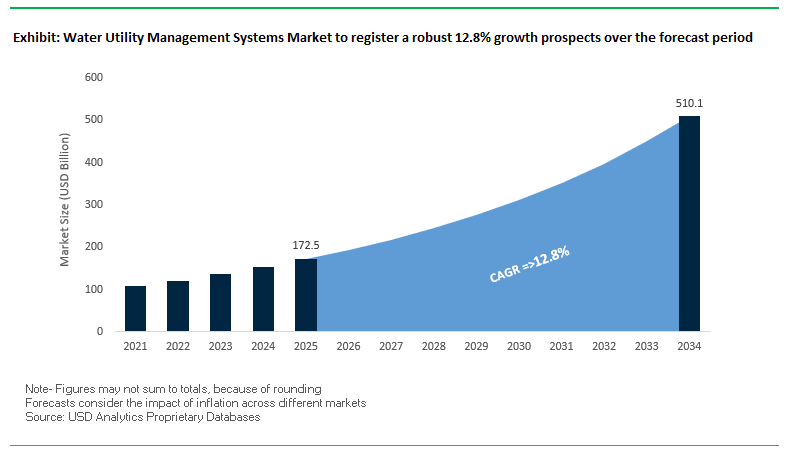

The global water utility management systems market is projected to grow from $172.5 billion in 2025 to $510 billion by 2034, representing a robust CAGR of 12.8%. This rapid growth is being fueled by increasing urbanization, escalating non-revenue water (NRW) concerns, climate change-induced water stress, and widespread digitalization of water networks. Utilities are under significant pressure to modernize aging infrastructure while adopting smart and resilient management systems that integrate predictive analytics, IoT, and AI technologies.

Rising global water scarcity and growing regulatory mandates are accelerating the adoption of digital utility management solutions. Smart water platforms enable utilities to monitor network efficiency, reduce water losses, and enhance operational reliability. Moreover, cybersecurity is emerging as a critical requirement as digital infrastructure becomes more integrated with cloud-based platforms and IoT-connected devices.

Key Insights for Industry Stakeholders:

- Urbanization is stressing existing water networks, creating opportunities for modernization using smart utility management systems.

- Non-revenue water remains a significant challenge, with some regions losing up to 47% of produced water.

- Climate change and water scarcity are driving demand for resilient, predictive, and efficient utility management solutions.

- Digitalization introduces operational efficiencies but also increases the need for cybersecurity in critical water infrastructure.

- Integration of AI, cloud computing, and IoT is reshaping water utility operations, enabling real-time monitoring and analytics.

Market Analysis: Recent Developments in Water Utility Management Systems

The water utility management systems market has experienced a surge in innovative deployments and strategic partnerships. In August 2025, Itron Inc. partnered with the Water Authority of Fiji to launch the first smart water metering project in the Fiji Islands, leveraging Cyble communication modules and the Temetra cloud platform to reduce NRW, which is estimated at 47%. During the same month, the European Investment Bank (EIB) committed €250 million to support modernization efforts at EYDAP, Athens Water Supply and Sewerage Company, targeting smart meters and digital systems.

In May 2025, the New Zealand government passed legislation for its "Local Water Done Well" reform plan, restructuring water asset management and promoting the adoption of advanced utility management systems. Earlier, in April 2025, OTT HydroMet launched its OTT Flood Monitoring System, integrating IoT devices with radar sensors for high-accuracy water level and quality measurement to improve flood risk management. Meanwhile, in February 2025, Veolia Environnement partnered with Mistral AI to develop the Veolia Secure GPT, integrating generative AI for enhanced resource management and operational optimization.

Key strategic acquisitions and technology integrations have further shaped the market. In November 2024, In-Situ Inc. acquired ChemScan to expand its real-time monitoring capabilities. Earlier, in October 2023, SUEZ and SAMP partnered to accelerate digital twin deployment in water and wastewater infrastructure. Additionally, Schneider Electric’s automation of India’s largest water treatment plant in January 2024 demonstrated the practical application of IoT-enabled platforms to improve operational efficiency for millions of residents.

Key Trends Driving Digital Water Utility Management

Digital Transformation and the Rise of Digital Twins

The water utility management systems market is being transformed by digital twin technology, AI, and IoT-enabled monitoring. A 2025 academic review highlights how utilities are leveraging digital twins to simulate real-time operational scenarios, predict maintenance needs, and optimize system performance. For example, the Alder Dam project in Washington, operated by Tacoma Public Utilities and supported by the U.S. Department of Energy, uses digital twins to simulate turbine operations under varying conditions like low water flow or high energy demand. Companies like Xylem are deploying "smart sewer" technologies, achieving up to 80% reduction in Combined Sewer Overflow (CSO) and avoiding hundreds of millions in capital expenditure. This trend emphasizes the industry’s shift toward data-driven, predictive water management.

Non-Revenue Water (NRW) Reduction as a Strategic Imperative

Reducing Non-Revenue Water (NRW) water lost through leaks, bursts, or theft is a critical trend for utilities globally. Advanced metering infrastructure (AMI), real-time analytics, and AI algorithms are enabling precise detection of leaks and anomalies, minimizing water loss, and enhancing revenue protection. The Jal Jeevan Mission in India demonstrates a decentralized, data-driven approach, training women to use Field Testing Kits (FTKs) and upload water quality data online. Such initiatives highlight how technology and community engagement are increasingly integrated to improve water system efficiency and public health outcomes.

Climate Resilience and Sustainability Integration

Utilities are prioritizing resilient, climate-ready water infrastructure to withstand extreme weather and environmental challenges. The U.S. Infrastructure Investment and Jobs Act of 2021 allocates significant federal funding for modernization and resilience in water utilities. Corporates like Veolia Water Technologies and Solutions are implementing holistic sustainability strategies, recovering energy from wastewater and nutrients for fertilizer, turning water systems into revenue-generating and environmentally sustainable operations. These trends indicate a strong market push toward green, efficient, and climate-resilient water utility management.

Strategic Opportunities in Water Utility Management Systems

The Water Utility Management Systems Market offers robust opportunities for vendors providing integrated SCADA, AMI, asset management, and leak detection solutions. Utilities are seeking platforms that enable proactive asset management, NRW reduction, and digital integration. Cloud-based deployment, predictive analytics, and mobile workforce tools represent high-growth avenues. Additionally, sustainability initiatives and customer engagement technologies create long-term opportunities for solutions that optimize operational efficiency, reduce losses, and improve transparency.

Market Share Insights of Water Utility Management Systems

Market Share by Solution Type: SCADA Leads with Strategic Asset Management Growth

By solution type, SCADA systems (20.9%) remain the backbone of operations, providing real-time control over pumps, valves, and treatment processes. AMI/AMR drives revenue protection and operational efficiency by enabling accurate billing, remote reads, and leak alerts. Asset Management Systems (13.2%) and Leak Detection Systems (7–9%) reflect the shift toward proactive infrastructure maintenance. Other solutions like CIS, GIS, Workforce Management, MDM, Water Quality Monitoring, Hydraulic Modeling, LIMS, and EAM integrate operational, financial, and compliance functions, creating a unified data ecosystem. The trend toward integrated and proactive water utility management is clearly reflected in this segmentation.

Market Share by Deployment Mode: Cloud-Based Solutions Dominate

Cloud-based (SaaS) deployment (65%) leads the market, offering utilities lower upfront costs, scalability, and automatic updates. On-premise solutions (35%) remain relevant for large utilities requiring customized, secure systems with direct control over servers. The growing preference for cloud reflects the industry’s move toward flexible, scalable, and cost-efficient digital water solutions, especially for small and medium-sized utilities lacking extensive IT infrastructure.

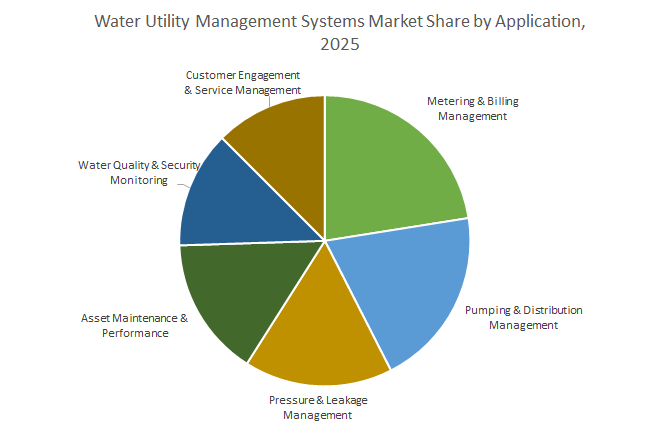

Market Share by Application: Metering, Pumping, and Leakage Management Lead

Metering & Billing Management (22.5%) is the largest application, driven by AMI-enabled revenue protection and customer interaction. Pumping & Distribution Management (20.9%) optimizes energy and system reliability, while Pressure & Leakage Management targets reduction of NRW, which can reach 25–50% of produced water in some networks. Asset Maintenance & Performance (14.9%), Water Quality & Security Monitoring (13.2%), and Customer Engagement & Service Management represent critical applications that improve operational efficiency, regulatory compliance, and customer satisfaction, emphasizing the multi-dimensional value of modern water utility management systems.

United States: AI-Driven Water Utility Management for Infrastructure Modernization

The United States water utility management systems (WUMS) market is strongly influenced by federal initiatives, regulatory support, and technological innovations. The U.S. Environmental Protection Agency (EPA) actively promotes the Effective Utility Management (EUM) framework, focusing on ten attributes of well-managed water systems. The Bipartisan Infrastructure Law (BIL) provides over $50 billion to enhance water infrastructure, with significant portions allocated to the adoption of digital WUMS solutions. Updated guidance, such as the August 2024 EUM Primer, emphasizes asset management, risk and resilience, and customer satisfaction, which are all strengthened through WUMS integration. Additionally, programs like the USDA Rural Energy for America Program (REAP) provide grants and loan guarantees for WUMS-integrated projects, including farm-based anaerobic digesters. Corporate innovations, exemplified by Itron’s 2024 upgrade of the Temetra platform with AI-driven analytics, enable early fault detection, leak prevention, and improved network resilience. The market is primarily driven by the need to modernize aging infrastructure, reduce non-revenue water (NRW), and comply with expanding federal and state regulations.

China: Smart Water Governance and Sponge City Initiatives

China’s WUMS market growth is propelled by urban modernization projects and government-backed infrastructure initiatives. The "Sponge City" program aims for more than 80% of urban built-up areas to meet stormwater management standards by 2030, necessitating sophisticated WUMS for real-time monitoring and management. Large-scale infrastructure projects, including the Yarlung Zangbo hydropower dam, require advanced water management systems to ensure water security and flood mitigation. Regulatory reforms, such as the "Strictest Water Resources Management System," create a demand for data-driven governance, while technological advancements in smart water management (SWM) leveraging IoT, AI, and big data enable predictive maintenance and operational efficiency. Key applications include urban flood control, sustainable stormwater management, and compliance with water pollution regulations.

India: IoT-Enabled Water Monitoring and Rural Water Supply Enhancement

India’s water utility management systems market is driven by government programs, infrastructure investments, and AI-based technological adoption. The "Jal Jeevan Mission" deploys sensor-based IoT devices to monitor rural drinking water supply systems in over six lakh villages, providing near real-time data without manual intervention. The Union Budget for 2025–26 allocated significant funding for water management, further boosting demand for WUMS. Regulatory frameworks such as the Central Pollution Control Board’s (CPCB) National Water Quality Monitoring Programme (NWMP) depend on WUMS for accurate, timely, and publicly available water quality data. Technological partnerships, including Pani Energy and Murugappa Water Technology & Solutions in November 2024, emphasize AI-driven solutions for proactive water management. Market applications include improving rural water quality, enhancing urban water network efficiency, and supporting sustainable sanitation.

Germany: Digital Twins and AI-Enhanced Water Management

Germany’s WUMS market is shaped by regulatory compliance, climate adaptation strategies, and digital transformation initiatives. The revised EU Urban Wastewater Treatment Directive (January 2025) requires wastewater plants to implement a "4th purification stage" to remove micropollutants, driving innovation in advanced monitoring and management systems. German cities, guided by the Federal Environment Agency (UBA), are adopting digital twins, AI, and IoT-enabled monitoring for optimized water management, critical for remote operations and WUMS integration. Corporate initiatives, such as the German Water Partnership’s "WATER 4.0" working group, highlight the role of IoT and service-based solutions in resource-efficient, flexible, and competitive water utility management. Applications focus on compliance, climate resilience, and operational optimization.

United Kingdom: Regulatory Frameworks and Real-Time Monitoring

The UK water utility management systems market benefits from regulatory oversight, corporate innovation, and infrastructure modernization. The Water Industry National Environment Programme (WINEP) outlines environmental obligations and allocates £22.1 billion for asset improvements, including sludge management and other water infrastructure upgrades. Innovative solutions such as Siemens’ Water Quality Analytics as a Service (WQAaaS), introduced in 2024, provide real-time data and predictive analytics for asset optimization, making WUMS a critical tool for operational efficiency. Market drivers include modernization of aging infrastructure, enhanced service resilience, and integration of digital monitoring for proactive water management.

Australia: Remote Monitoring and Digital Twin Integration for Water Utilities

Australia’s WUMS market is supported by significant infrastructure investments, technological innovation, and corporate leadership in digital solutions. Sydney Water announced a $34 billion investment over the next 10 years to renew existing assets and implement new projects, including advanced remote monitoring systems. The Commonwealth Scientific and Industrial Research Organisation (CSIRO) leads in remote sensing and data analytics, employing satellite imagery and ground-based sensors to track water quality across large water bodies. Companies like Aqua Analytics are pioneering digital twin development for water networks, enabling non-revenue water reduction, operational efficiency, and informed decision-making. Key applications include water conservation, network optimization, and sustainable management of urban and regional water systems.

Competitive Landscape of Water Utility Management Systems Market

The water utility management systems market is highly competitive, with leading players emphasizing digital transformation, AI integration, and IoT-enabled solutions. Companies offer end-to-end platforms that enable utilities to reduce water loss, optimize network performance, and improve operational sustainability.

Xylem Inc. excels in smart water solutions and network optimization

Xylem Inc. combines advanced water technologies with digital analytics and services. Its Sensus smart meters and Xylem Vue platform enable real-time monitoring and decision support for utilities. Strategic acquisitions, including Evoqua Water Technologies for $7.5 billion (2024), have expanded Xylem’s portfolio across treatment and utility management. With a presence in over 150 countries, Xylem also contributes to community resilience via its Xylem Watermark program, supporting education and access to safe water.

SUEZ S.A. leads in predictive and integrated water management

SUEZ S.A. provides end-to-end water cycle services with its AQUADVANCED® suite, offering real-time monitoring and predictive analytics. In a 2023 Macao case study, SUEZ achieved a water loss rate of under 9%, outperforming national targets. The company also leverages digital twin technology in partnership with SAMP and has expanded in Asia through strategic projects, reinforcing its position in advanced water utility management.

Veolia Environnement S.A. drives AI-powered operational efficiency

Veolia Environnement specializes in optimized resource management, focusing on circular economy principles. Its Hubgrade platform integrates AI and analytics for predictive maintenance and operational optimization. In February 2025, Veolia partnered with Mistral AI to incorporate generative AI into its operations, aiming to prevent 18 million tons of CO₂ equivalent at client sites by 2027. The company emphasizes sustainability, decarbonization, and resource efficiency in water utility operations.

Itron Inc. provides scalable smart metering and data management

Itron Inc. offers advanced metering infrastructure (AMI) solutions and cloud-based platforms. Its Temetra system enables multi-vendor data management for utilities. The August 2025 smart water project in Fiji demonstrated Itron’s ability to convert mechanical meters into smart devices using clip-on communication modules, facilitating phased and cost-effective digital transformation for utilities worldwide.

Schneider Electric SE leads in IoT-enabled water infrastructure automation

Schneider Electric delivers digital and automation solutions through its EcoStruxure platform, offering IoT-enabled monitoring of water treatment plants and distribution networks. The January 2024 automation of Mumbai’s largest water treatment plant showcases the scalability and efficiency of Schneider’s solutions. The company focuses on sustainability, achieving up to 30% energy savings and significant CO₂ reduction for water utilities.

Water Utility Management Systems Market Report Scope

Water Utility Management Systems Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$172.5 Billion

|

|

Market Size (2034)

|

$510 Billion

|

|

Market Growth Rate

|

12.8%

|

|

Segments

|

By Solution Type (Customer Information Systems & Billing, Asset Management Systems, Supervisory Control and Data Acquisition, Geographic Information Systems, Advanced Metering Infrastructure & Automatic Meter Reading, Meter Data Management, Laboratory Information Management Systems, Workforce Management Systems, Hydraulic Modeling & Simulation Software, Enterprise Asset Management, Leak Detection Systems, Water Quality Monitoring Systems), By Deployment Mode (On-premise, Cloud-based), By Application (Water Quality & Security Monitoring, Pumping & Distribution Management, Pressure & Leakage Management, Metering & Billing Management, Asset Maintenance & Performance, Customer Engagement & Service Management), By Utility Size (Large Utilities, Medium Utilities, Small Utilities), By End-User (Municipal Water Utilities, Industrial Water Utilities, Private Water Utilities)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Xylem Inc., Veolia, SUEZ, Evoqua Water Technologies, Itron Inc., ABB Ltd., Trimble Inc., Siemens, Bentley Systems, Incorporated, Schneider Electric, Hach (Danaher Corporation), Badger Meter, Oracle Corporation, Rockwell Automation, Inc., Emerson Electric Co.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Water Utility Management Systems Market Segmentation

By Solution Type

- Customer Information Systems (CIS) & Billing

- Asset Management Systems

- Supervisory Control and Data Acquisition (SCADA)

- Geographic Information Systems (GIS)

- Advanced Metering Infrastructure (AMI) & Automatic Meter Reading (AMR)

- Meter Data Management (MDM)

- Laboratory Information Management Systems (LIMS)

- Workforce Management Systems

- Hydraulic Modeling & Simulation Software

- Enterprise Asset Management (EAM)

- Leak Detection Systems

- Water Quality Monitoring Systems

By Deployment Mode

By Application

- Water Quality & Security Monitoring

- Pumping & Distribution Management

- Pressure & Leakage Management

- Metering & Billing Management

- Asset Maintenance & Performance

- Customer Engagement & Service Management

By Utility Size

- Large Utilities

- Medium Utilities

- Small Utilities

By End-User

- Municipal Water Utilities

- Industrial Water Utilities

- Private Water Utilities

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in the Water Utility Management Systems Industry include-

- Xylem Inc.

- Veolia

- SUEZ

- Evoqua Water Technologies

- Itron Inc.

- ABB Ltd.

- Trimble Inc.

- Siemens

- Bentley Systems, Incorporated

- Schneider Electric

- Hach (Danaher Corporation)

- Badger Meter

- Oracle Corporation

- Rockwell Automation, Inc.

- Emerson Electric Co.

*- List not Exhaustive

Research Coverage

The latest Water Utility Management Systems Market Report by USDAnalytics investigates the transformative role of digital platforms, predictive analytics, IoT, and AI in modernizing water infrastructure and addressing global water scarcity challenges. This report highlights breakthroughs in digital twin deployments, smart metering projects, and AI-driven predictive maintenance while providing detailed analysis reviews on the integration of cybersecurity, sustainability, and climate resilience in water management. By examining strategic acquisitions, regulatory frameworks, and real-world case studies across utilities, this report is an essential resource for decision-makers, policymakers, and industry leaders seeking to optimize operational efficiency, reduce non-revenue water, and implement future-ready utility management strategies. Scope Includes-

- Segmentation: By solution type, deployment mode, application, utility size, and end-user

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa

- Historic & Forecast Data: Historic data from 2021 to 2024 and forecast data from 2025 to 2034

- Companies: Analysis/profiles of 15+ companies including Xylem Inc., Veolia, SUEZ, Evoqua Water Technologies, Itron Inc., ABB Ltd., Trimble Inc., Siemens, Bentley Systems, Schneider Electric, Hach (Danaher Corporation), Badger Meter, Oracle Corporation, Rockwell Automation, and Emerson Electric Co.

Methodology

The methodology adopted by USDAnalytics combines primary and secondary research with data triangulation to deliver fact-based insights. Primary research involved interviews with utility operators, technology providers, policymakers, and industry experts, while secondary research encompassed government reports, regulatory filings, company disclosures, and technical journals. Advanced modeling tools were used to forecast market growth across segments and geographies, ensuring accurate projections from 2025 to 2034. The study also integrates SWOT analysis, technology benchmarking, and recent case studies to present a holistic and practical view of market opportunities and risks for industry professionals.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.

Table of Contents: Water Utility Management Systems Market

1. Executive Summary

1.1. Market Highlights & Key Projections

1.2. Global Market Snapshot

1.3. Key Findings

2. Water Utility Management Systems Market Outlook (2025–2034)

2.1. Introduction: Digitalization of Water Networks

2.2. Market Valuation and Growth Projections (2025–2034)

2.2.1. Current Market Size (2025): $172.5 Billion

2.2.2. Forecasted Market Size (2034): $510 Billion

2.2.3. Projected Compound Annual Growth Rate (CAGR): 12.8%

2.3. Market Drivers and Challenges

2.3.1. Drivers: Urbanization, Non-Revenue Water, Climate Change, and Regulatory Mandates

2.3.2. Challenges: Cybersecurity Risks and High Implementation Costs

2.4. Key Insights for Industry Stakeholders

3. Key Market Trends and Recent Developments (2024–2025)

3.1. Market Trend: Digital Transformation and the Rise of Digital Twins

3.2. Market Trend: Non-Revenue Water (NRW) Reduction as a Strategic Imperative

3.3. Market Trend: Climate Resilience and Sustainability Integration

3.4. Recent Developments & Strategic Moves

4. Water Utility Management Systems Market – Segmentation Insights

4.1. By Solution Type

4.1.1. SCADA Systems (20.9% Market Share)

4.1.2. Advanced Metering Infrastructure (AMI) & Automatic Meter Reading (AMR)

4.1.3. Asset Management Systems (13.2% Market Share)

4.1.4. Leak Detection Systems (7–9% Market Share)

4.1.5. Other Solutions (CIS, GIS, Workforce Management, MDM, etc.)

4.2. By Deployment Mode

4.2.1. Cloud-based (65% Market Share)

4.2.2. On-premise (35% Market Share)

4.3. By Application

4.3.1. Metering & Billing Management (22.5% Market Share)

4.3.2. Pumping & Distribution Management (20.9% Market Share)

4.3.3. Pressure & Leakage Management

4.3.4. Asset Maintenance & Performance (14.9% Market Share)

4.3.5. Water Quality & Security Monitoring (13.2% Market Share)

4.3.6. Customer Engagement & Service Management

4.4. By Utility Size

4.4.1. Large Utilities

4.4.2. Medium Utilities

4.4.3. Small Utilities

4.5. By End-User

4.5.1. Municipal Water Utilities

4.5.2. Industrial Water Utilities

4.5.3. Private Water Utilities

5. Country Analysis and Outlook: Water Utility Management Systems Market

5.1. United States: AI-Driven Water Utility Management for Infrastructure Modernization

5.2. China: Smart Water Governance and Sponge City Initiatives

5.3. India: IoT-Enabled Water Monitoring and Rural Water Supply Enhancement

5.4. Germany: Digital Twins and AI-Enhanced Water Management

5.5. United Kingdom: Regulatory Frameworks and Real-Time Monitoring

5.6. Australia: Remote Monitoring and Digital Twin Integration for Water Utilities

6. Market Size Outlook by Region (2025-2034)

6.1. North America Water Utility Management Systems Market Size Outlook to 2034

6.1.1. By Solution Type

6.1.2. By Deployment Mode

6.1.3. By Application

6.1.4. By Utility Size

6.1.5. By End-User

6.1.6. By Country (U.S., Canada, Mexico)

6.2. Europe Water Utility Management Systems Market Size Outlook to 2034

6.2.1. By Solution Type

6.2.2. By Deployment Mode

6.2.3. By Application

6.2.4. By Utility Size

6.2.5. By End-User

6.2.6. By Country (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

6.3. Asia Pacific Water Utility Management Systems Market Size Outlook to 2034

6.3.1. By Solution Type

6.3.2. By Deployment Mode

6.3.3. By Application

6.3.4. By Utility Size

6.3.5. By End-User

6.3.6. By Country (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

6.4. South America Water Utility Management Systems Market Size Outlook to 2034

6.4.1. By Solution Type

6.4.2. By Deployment Mode

6.4.3. By Application

6.4.4. By Utility Size

6.4.5. By End-User

6.4.6. By Country (Brazil, Argentina, Rest of South America)

6.5. Middle East and Africa Water Utility Management Systems Market Size Outlook to 2034

6.5.1. By Solution Type

6.5.2. By Deployment Mode

6.5.3. By Application

6.5.4. By Utility Size

6.5.5. By End-User

6.5.6. By Country (Saudi Arabia, UAE, South Africa, Egypt, Rest of MEA)

7. Company Profiles: Leading Players

7.1. Xylem Inc.

7.1.1. Company Overview

7.1.2. Digital Water Solutions and Strategic Acquisitions

7.2. SUEZ S.A.

7.2.1. Company Overview

7.2.2. AQUADVANCED® Suite and Digital Initiatives

7.3. Veolia Environnement S.A.

7.4. Itron Inc.

7.5. Schneider Electric SE

7.6. Other Key Players

7.6.1. ABB Ltd.

7.6.2. Trimble Inc.

7.6.3. Siemens

7.6.4. Bentley Systems, Incorporated

7.6.5. Hach (Danaher Corporation)

7.6.6. Badger Meter

7.6.7. Oracle Corporation

7.6.8. Rockwell Automation, Inc.

7.6.9. Emerson Electric Co.

8. Methodology

8.1. Research Scope

8.2. Market Research Approach

8.3. Data Sources and Validation

8.4. Assumptions and Limitations

9. Appendix

9.1. Acronyms and Abbreviations

9.2. List of Tables

9.3. List of Figures