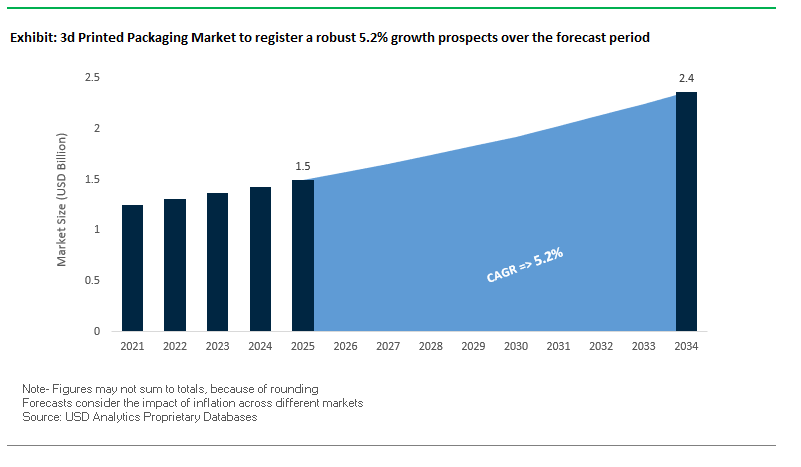

3D Printed Packaging Market Overview: Rapid Prototyping, Mass Customization and On-Demand Production Lift the Market from $1.5B (2025) to $2.4B (2034) at 5.2% CAGR

The Global 3D Printed Packaging Market is valued at USD 1.5 billion in 2025 and projected to reach USD 2.4 billion by 2034, expanding at a CAGR of 5.2%. For packaging engineering and procurement leaders, additive manufacturing (AM) is now a strategic lever: it compresses tooling lead times, enables rapid packaging prototyping, unlocks mass customization/personalization, and supports on-demand, low-inventory production. AM increasingly dovetails with sustainability roadmaps through biodegradable and recycled polymers and even edible materials, while digital workflows (simulation, DfAM, build optimizers) drive first-time-right outcomes. Notably, 3D-printed molds and tooling are accelerating conventional converting (e.g., blow molding), cutting weeks from new-pack introductions and slashing pre-production costs.

Key Insights for industry professionals

- Prototyping impact: 3D-printed tooling has demonstrated ~6-week lead-time reductions and up to ~90% cost savings in mold development, accelerating pack/closure iterations.

- Personalization at scale: AM enables intricate branding, embossed logos, and unique geometries impractical with legacy tooling vital for luxury, beauty, and CPG limited editions.

- Sustainability pivot: Expanding use of biodegradable plastics, recycled polymers, and edible substrates aligns AM with circular packaging targets.

- On-demand operations: Low-MOQs and localized production reduce waste, intermediate inventory, and obsolescence risk across seasonal or event-driven SKUs.

Market Analysis: 2023–2025 Signals Software Physics, Open Platforms, High-Speed Polymer AM, and Sustainable Pilots

Ecosystem upgrades in software, platforms, and high-speed hardware are pushing 3D printed packaging into mainstream workflows. In August 2025, Bambu Lab introduced physics-based simulation capabilities to virtually test 3D printed packaging performance prior to print supporting faster DfAM loops. Also in August 2025, Elegoo launched Nexprint, an open-source 3D model-sharing platform that streamlines collaboration between brand owners, design agencies, and converters. In July 2025, Stratasys bolstered its polymer AM position by acquiring assets from Nexa3D, expanding high-speed DLP options applicable to molds, trays, and functional pack components. Earlier pilots advanced the sustainability case: in April 2025, GaeaStar and Verve Coffee Roasters launched a U.S. pilot for sustainable, 3D-printed clay-inspired cups, addressing single-use cup waste with localized production.

AM is also collapsing prototyping timelines for thermoforming and trays. In March 2025, Harpak-ULMA debuted a 3D printing service for tray-package prototyping, shrinking development from weeks to hours and enabling faster line trials. Macro context remains supportive: January 2025 analysis indicated a DACH renovation/retrofit rebound an adjacent AM demand signal for rapid component prototyping and tooling that often shares capacity with packaging applications. Preceding this wave, HP’s Formnext 2024 (November 2024) introductions halogen-free flame-retardant polymer with ~50% reusability and new build optimization lowered cost per part and improved repeatability for packaging fixtures and inserts. Earlier still, December 2023, Oertli Instrumente AG integrated Mayku Multiplier pressure forming into a 3D workflow to speed medical-pack prototyping, exemplifying how hybrid AM + forming stacks accelerate commercial launch gates.

Key Trends and Opportunities Shaping the Future of the 3D Printed Packaging Market

Strategic Adoption by Major CPG and Pharma Brands for High-Value Customization

Additive manufacturing is rapidly transitioning from prototyping to direct integration into packaging supply chains, particularly for consumer packaged goods (CPG) and pharmaceuticals. This trend is driven by the growing demand for mass customization, limited-edition runs, and patient-specific packaging solutions that traditional manufacturing cannot economically achieve. In the pharmaceutical sector, Aprecia Pharmaceuticals’ FDA-approved 3D-printed drug, Spritam, demonstrates the capability of additive manufacturing to deliver high-dose, rapidly dissolving tablets for patient-centric treatments. On the consumer side, luxury brands like L’Oréal and Chanel are leveraging 3D printing for highly customized, limited-edition packaging that reinforces brand identity and exclusivity. Additionally, companies such as PepsiCo utilize 3D printing to rapidly iterate packaging designs, producing prototypes with full-color, high-resolution graphics, reducing time-to-market and supporting innovative packaging strategies.

Government and Defense Investment in On-Demand, Resilient Supply Chains

Governments worldwide, particularly in the U.S. and EU, are heavily investing in additive manufacturing to bolster supply chain resilience. The U.S. Department of Defense (DoD) has allocated $3.3 billion in its FY 2026 budget to additive manufacturing projects, an 83% increase from the previous year, aimed at localizing supply chains, accelerating procurement, and enabling rapid production of prototypes and spare parts. These investments create a ripple effect for the 3D printed packaging sector, as materials, processes, and logistics innovations developed for defense applications can be directly applied to industrial and specialized packaging. Additionally, the DoD’s focus on mitigating supply chain vulnerabilities through domestic additive manufacturing underscores the strategic importance of on-demand production models in enhancing resilience for high-value industrial goods.

Development of Integrated Digital Platforms for On-Demand Packaging as a Service (PaaS)

The convergence of 3D printing with digital platforms presents a major market opportunity through the creation of Packaging-as-a-Service (PaaS) models. These platforms connect brand owners with distributed 3D printing networks, allowing designs to be uploaded and produced locally in bespoke quantities. This approach reduces logistics costs, shortens lead times, and supports niche customization. Decentralized production models enable localized, on-demand manufacturing, eliminating reliance on large centralized facilities and optimizing material and production flexibility. Furthermore, in-house rapid prototyping through 3D printing streamlines the design-to-production workflow, reduces costs, mitigates intellectual property risks, and formalizes a scalable on-demand production system, enhancing operational efficiency for brands.

Advancements in Sustainable and Bio-Based Materials for Circular Packaging

Material innovation in additive manufacturing is unlocking opportunities for circular, sustainable packaging solutions. High-performance, biodegradable, or compostable polymers such as polylactic acid (PLA) and polyhydroxyalkanoates (PHA) are increasingly being engineered for 3D printing, moving beyond conventional petroleum-based plastics like ABS and nylon. These materials enable the creation of end-use, eco-friendly packaging products, reducing environmental impact while maintaining performance standards. Companies like FoamPrint3D are pioneering custom biodegradable foam packaging derived from vegetable oils, demonstrating the ability of additive manufacturing to support specialized sustainable applications that would be uneconomical with traditional mass production methods. The integration of bio-based, 3D-printable materials aligns with global sustainability goals and opens new revenue streams in eco-conscious packaging markets.

Competitive Landscape: Materials, Speed, and Digital Toolchains Define Leaders

A mix of platform OEMs and digital manufacturing services is shaping the category. Differentiation centers on materials breadth, print speed & part fidelity, software (simulation/optimizers), and the ability to bridge prototype-to-production with validated workflows for packaging lines.

HP Inc. HP scales high-speed polymer AM for packaging

HP’s Multi Jet Fusion (MJF) ecosystem targets complex, durable parts at high throughput, ideal for functional packaging fixtures, nests, jigs, and low-volume components. At Formnext 2024, HP introduced a halogen-free, flame-retardant material with a high reusability ratio and launched HP 3D Build Optimizer, using AI to reduce build costs and stabilize quality. Strategy: make industrial-grade 3D printing more accessible via materials + software that compress cost and scale. Core strength is a full-stack platform (hardware/software/materials) proven for speed, repeatability, and part integrity in packaging environments.

Stratasys Ltd. Stratasys enables color-true, multi-material prototyping and fast DLP

Stratasys offers PolyJet, FDM, and SAF, spanning concept models to functional tooling. In July 2025, it acquired assets from Nexa3D, reinforcing high-speed DLP for rapid molds and components; prior collaborations (e.g., with major CPGs) show capability in bottle and closure redesign. Strategy: cover the entire design-to-production curve with material diversity and platform choice. PolyJet enables full-color, transparent, and flexible parts in a single print ideal for consumer-facing mockups while J850/J55 class systems deliver form-fit-function prototypes for line trials.

Carbon Carbon brings production-grade lattices and smooth finishes for custom inserts

Digital Light Synthesis™ (DLS) leverages light + oxygen to produce isotropic, smooth-finish parts suitable for protective pack inserts, custom dunnage, and end-use components. Carbon’s network expanded in 2024 (new European production partners), and its track record in mass customization (e.g., footwear) showcases prototype-to-production scalability. Strategy: drive on-demand manufacturing and material cost reductions to compete with traditional processes. Strengths include high build quality, functional lattices, and fast cycle times for customized packaging applications.

Protolabs Protolabs connects AM prototyping to molded production for packaging teams

Protolabs provides 3D printing (SLA/SLS/PolyJet), CNC, and injection molding under one digital roof, enabling rapid prototyping of closures, trays, and fixtures with a seamless ramp to low-volume or bridge tooling. Integration is the advantage: designers iterate in AM plastics/elastomers, validate fit/function, and transition to molded production without changing partners. Strategy prioritizes speed, DfM feedback, and no-MOQ options, supported by continuous materials/process expansion to mirror real packaging substrates and elastomeric seals.

3d Printed Packaging Market Share Insights

Prototyping Leads Market Share by Application in the 3D Printed Packaging Industry

Prototyping accounts for the largest share, around 45%, making it the most entrenched application in the 3D printed packaging industry. Its dominance is linked to the ability of additive manufacturing to drastically shorten packaging design cycles, reduce tooling costs, and enable rapid iteration of shapes, textures, and ergonomics. This capability has become a critical enabler for brand owners in consumer goods, cosmetics, and food and beverages who seek to test packaging shelf appeal before mass production. Medical devices follow as the most regulated and value-intensive application, leveraging 3D printing for patient-specific, sterile packaging solutions. Protective and structural inserts are gaining traction for high-value electronics and luxury goods, offering superior cushioning with lightweight geometries. On-demand and customized packaging, though smaller today, represents the growth frontier, enabling personalized unboxing experiences aligned with premiumization and sustainability trends. Meanwhile, mold and tooling applications, though behind-the-scenes, secure a vital share by enhancing efficiency in thermoforming and assembly operations.

Pharmaceuticals and Healthcare Hold the Largest Market Share by End-Use in the 3D Printed Packaging Industry

Pharmaceuticals and healthcare represent the largest end-use industry with an estimated 35% share, driven primarily by the stringent requirements of customized medical device packaging. The need for biocompatibility, sterility, and regulatory compliance makes 3D printing an optimal fit, despite its higher cost compared to conventional packaging. Consumer goods hold about 25%, reflecting the growing use of additive manufacturing in prototyping and premium packaging for electronics, toys, and luxury segments. Food and beverages show cautious adoption, primarily in prototyping packaging concepts and niche chocolate or specialty product molds, constrained by regulatory hurdles in food-contact safety. Cosmetics and personal care are leveraging 3D printing for bespoke packaging, where unique shapes and personalized experiences directly enhance brand positioning. Industrial goods and automotive industries maintain a functional share, primarily through custom protective inserts and tooling jigs that optimize manufacturing and logistics operations.

United States: AI-Driven 3D Printing Innovations Transform Packaging Design

The U.S. 3D printed packaging market is being strongly influenced by governmental initiatives promoting advanced manufacturing technologies. Agencies such as the National Institute of Standards and Technology (NIST) are driving adoption of 3D printing for rapid prototyping, on-demand production, and the creation of customized, complex packaging designs. Technological advancements, including AI-driven workflow optimization and defect detection, are enhancing quality and reducing material waste, directly supporting sustainable packaging goals.

Corporate initiatives are accelerating market growth, exemplified by the January 2025 partnership between 3D Systems and Daimler Truck AG, highlighting the broader trend of additive manufacturing adoption for supply chain efficiency. The rise of e-commerce has further fueled demand for customized and protective packaging solutions. 3D printing allows for on-demand inserts, dunnage, and custom-fit boxes, minimizing material usage while ensuring product safety. Strategic acquisitions, like Qnnect’s acquisition of Hermetic Solutions Group in 2022, underscore the market trend of integrating specialized expertise, including 3D printing, into broader packaging solutions.

Germany: Circular Economy and Advanced Manufacturing Strengthen 3D Printed Packaging

Germany’s 3D printed packaging market is shaped by strict regulatory frameworks, particularly the EU Packaging and Packaging Waste Regulation (PPWR), effective February 2025. This legislation mandates that all packaging be fully recyclable or reusable by 2030, driving innovations in material and design that align with circular economy principles. Germany’s Packaging Act (VerpackG) enforces high recycling targets, and companies are leveraging AI-powered optical sorting systems to manage complex 3D printed packaging with mixed or composite materials.

Technological innovation is led by companies such as EOS GmbH, which provide industrial 3D printing systems, software, and materials for plastic and metal applications, including packaging. Corporate movements, like Palm’s 2025 offer to acquire several corrugated box plants from International Paper, reflect a broader shift toward sustainable and technologically advanced production methods. Germany’s leadership in recycling, combined with additive manufacturing capabilities, positions it as a key hub for sustainable and high-performance 3D printed packaging.

China: Government Policies and Smart Manufacturing Drive 3D Printed Packaging Growth

China’s 3D printed packaging market is being propelled by the “Made in China 2025” initiative, which encourages high-tech manufacturing and aims to increase domestic content of core materials to 70% by 2025. Technological investments in automation and AI, alongside the integration of “5G plus industrial internet,” optimize production efficiency and flexible capacity, reducing waste and turnaround times for 3D printed packaging.

A focus on miniaturization is driving demand for intricate, space-efficient packaging solutions, particularly for consumer electronics. Regulatory reforms targeting non-degradable plastics have increased adoption of sustainable materials, including paper-based and 3D printed alternatives. The rapid expansion of e-commerce platforms is further fueling demand for customizable and protective packaging, positioning China as a leading market for sustainable, high-precision 3D printed packaging solutions.

India: Startups and Government Support Accelerate 3D Printed Packaging Adoption

India’s 3D printed packaging market is benefiting from the “National Strategy for Additive Manufacturing,” which aims to contribute nearly $1 billion to the country’s GDP by 2025. The initiative supports the creation of startups, development of India-specific machines, materials, software innovations, and the training of 100,000 skilled professionals. Technological advancement is further supported by the India Semiconductor Mission (ISM), fostering 3D glass packaging innovation for advanced chip manufacturing.

A growing D2C and MSME ecosystem is driving demand for rapid prototyping and on-demand production of customized packaging. Investments in R&D, such as Tvasta Manufacturing Solutions’ Kerala-based concrete 3D printing research lab in July 2024, highlight India’s commitment to additive manufacturing innovation. New applications, including customized dental implants and flexible toys, are expanding the market for specialized 3D printed packaging, reflecting a blend of corporate initiatives and consumer-focused innovation.

Brazil: Regulatory Push and Technological Integration Foster 3D Printed Packaging Innovation

Brazil’s 3D printed packaging market is being shaped by the National Solid Waste Policy, which encourages a circular economy and the use of reusable, durable packaging, including additive manufacturing solutions. Technological advancements, such as robotics and AI, are enhancing efficiency, quality control, and operational sophistication, from automated sorting to defect detection.

Sustainability initiatives are driving the adoption of eco-friendly 3D printing materials, reinforced by the January 2025 law banning the import of solid waste, including plastics. Strategic collaborations, like the February 2024 alliance between SENAI CIMATEC and SPARE PARTS 3D, showcase efforts to optimize on-demand manufacturing and supply chain operations. These factors, combined with government support for local manufacturing, are accelerating the adoption of 3D printing technologies for sustainable industrial and consumer packaging.

Japan: Precision Manufacturing and Bio-Based Materials Boost 3D Printed Packaging

Japan’s 3D printed packaging market is anchored in advanced technologies and precision manufacturing, leveraging AI to accelerate design and enhance the accuracy of additive manufacturing processes. Regulatory updates, such as the June 2025 “positive list” for synthetic materials, ensure packaging meets stringent safety standards for imported and domestic products.

The country is increasingly focusing on bio-based materials, exemplified by LyondellBasell’s incorporation of bio-based polypropylene in Shiseido’s packaging in September 2025. Innovation in functionality is central, with 3D printed packaging designed for high dimensional stability and resistance to deformation, catering to high-performance applications. The rapid growth of e-commerce in Japan has further intensified demand for durable, customizable packaging solutions, driving advanced printing and branding technologies in the 3D printed packaging segment.

3d Printed Packaging Market Report Scope

3d Printed Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.5 Billion

|

|

Market Size (2034)

|

$2.4 Billion

|

|

Market Growth Rate

|

5.2%

|

|

Segments

|

By Material (Plastics, Metals, Composites, Paperboard & Cellulose-based Materials, Ceramics), By Technology (FDM, SLA, SLS, MJF, Others), By Application (Prototyping & Sample Creation, On-Demand & Customized Packaging, Protective & Structural Inserts, Mold & Tooling, Packaging for Medical Devices), By End-Use Industry (Food & Beverages, Pharmaceuticals & Healthcare, Cosmetics & Personal Care, Consumer Goods, Automotive, Industrial Goods)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

HP Inc., Stratasys Ltd., 3D Systems, Inc., EOS GmbH, Materialise NV, GE Additive (General Electric Company), Ricoh Company, Ltd., SABIC, Arkema S.A., Ultimaker, Voxeljet AG, Prodways Group, Renishaw plc, ExOne (Desktop Metal, Inc.), Evonik Industries AG

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

3d Printed Packaging Market Segmentation

By Material

- Plastics

- Metals

- Composites

- Paperboard & Cellulose-based Materials

- Ceramics

By Technology

By Application

- Prototyping & Sample Creation

- On-Demand & Customized Packaging

- Protective & Structural Inserts

- Mold & Tooling

- Packaging for Medical Devices

By End-Use Industry

- Food & Beverages

- Pharmaceuticals & Healthcare

- Cosmetics & Personal Care

- Consumer Goods

- Automotive

- Industrial Goods

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in 3d Printed Packaging Market

- HP Inc.

- Stratasys Ltd.

- 3D Systems, Inc.

- EOS GmbH

- Materialise NV

- GE Additive (General Electric Company)

- Ricoh Company, Ltd.

- SABIC

- Arkema S.A.

- Ultimaker

- Voxeljet AG

- Prodways Group

- Renishaw plc

- ExOne (Desktop Metal, Inc.)

- Evonik Industries AG

* List Not Exhaustive

Methodology

USDAnalytics employs a comprehensive, data-driven research methodology to deliver actionable insights into the 3D Printed Packaging Market. Our approach integrates primary research including interviews with packaging engineers, supply chain executives, brand managers, and additive manufacturing specialists with secondary research, leveraging corporate filings, sustainability reports, trade publications, and regulatory databases. Market sizing and projections, spanning USD 1.5 billion in 2025 to USD 2.4 billion by 2034 at a 5.2% CAGR, are developed through a combination of top-down and bottom-up analyses, considering product applications such as prototyping, on-demand/customized packaging, protective inserts, mold/tooling, and medical packaging. USDAnalytics also evaluates technological adoption, including FDM, SLA, SLS, MJF, and hybrid AM workflows, alongside materials such as plastics, metals, composites, paperboard, and bio-based substrates. Regional trends across the U.S., Germany, China, India, Brazil, and Japan are analyzed for regulatory impact, circular economy initiatives, and government investments in additive manufacturing. Competitive benchmarking assesses capabilities of market leaders such as HP, Stratasys, 3D Systems, Carbon, and Protolabs in delivering high-speed, scalable, sustainable, and customized packaging solutions. This methodology ensures industry professionals gain precise, forward-looking intelligence to optimize packaging design, reduce time-to-market, support sustainability, and enable cost-effective mass customization strategies.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.