Global Adhesion Laminated Surface Protection Films Market Overview: Safeguarding Surfaces with Precision and Sustainability

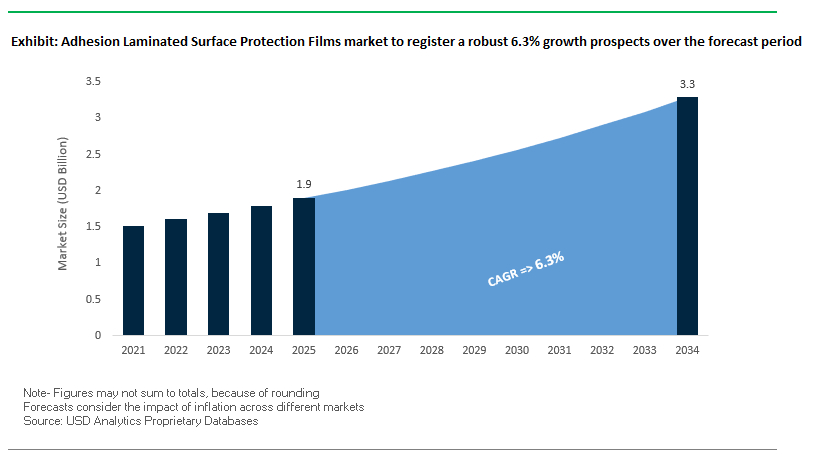

The global adhesion laminated surface protection films market is projected to grow from USD 1.9 billion in 2025 to USD 3.3 billion by 2034, at a steady CAGR of 6.3%. These films have become indispensable in industries where surface integrity directly impacts quality, safety, and customer satisfaction. For buyers and industry professionals, surface protection films are not only damage-prevention tools but also critical enablers of precision manufacturing, cost efficiency, and sustainability goals.

Applications now span electronics, automotive, and construction, each with unique performance requirements. With residue-free removal, UV resistance, and high transparency as baseline expectations, the market is rapidly shifting toward eco-friendly adhesives, solvent-free laminations, and recyclable film carriers. This transformation reflects a broader industrial priority: flawless product delivery with minimal environmental footprint.

Key Insights for Industry Stakeholders

- Electronics Sector Demand: Surface films protect high-value panels and components, reducing failure rates in displays and precision electronics.

- Automotive Dominance: Films safeguard paint, trim, and glass during transit, a critical step in ensuring aesthetic integrity and consumer satisfaction.

- Construction Materials Boom: With rising use of specialty glass and high-gloss finishes, protection films help avoid costly rework during installation.

- Residue-Free & UV-Resistant Adhesives: Next-gen formulations ensure clean removal and long-term durability, particularly for outdoor and sun-exposed surfaces.

Market Analysis: Recent Strategic Developments in Adhesion Laminated Surface Protection Films

The past year has been marked by strategic acquisitions, sustainability programs, and a wave of R&D investments reshaping the adhesion laminated surface protection films industry. In September 2024, Nitto Denko Corporation expanded its R&D programs targeting electronics protection films designed to resist static and micro-scratches. This highlighted growing demand from high-value display and optics applications. By November 2024, 3M Company updated its Scotchgard™ Paint Protection Films, improving durability for automotive and aerospace surfaces exposed to harsh conditions.

Momentum continued into January 2025, when Tesa SE introduced professional-grade films tailored to construction applications, with features such as ease of application and clean removal. In February 2025, Sekisui Chemical advanced its functional foam tapes and adhesive film portfolio, underscoring its role in mobility and electronics. March 2025 saw a spotlight on solvent-free lamination technologies at the Adhesion and Adhesives Symposium, marking a clear industry pivot toward sustainable alternatives.

By May 2025, automotive demand for next-gen adhesion laminated protection films was a major theme at the Automotive Coatings and Lamination Conference, emphasizing high-gloss and interior trim needs. Sustainability leadership was reinforced in June 2025, when Saint-Gobain Surface Solutions launched its Supplier Green Deal program, embedding decarbonization in supply chains. Finally, August 2025 marked a major milestone with Covestro’s acquisition of Pontacol, adding adhesive film production capabilities and strengthening its position in industrial applications. Collectively, these developments showcase how sustainability, innovation, and cross-sector adoption are shaping market growth.

Emerging Trends and Opportunities Transforming the Adhesion Laminated Surface Protection Films Market

Accelerated Adoption of Low/No VOC and Silicone-Free Adhesive Chemistries

The adhesion laminated surface protection films market is witnessing a rapid shift toward advanced adhesive technologies that eliminate volatile organic compounds (VOCs) and remove silicone from the formulation. This change is driven by the dual requirements of manufacturing purity and compliance with stringent environmental regulations. In the electronics sector, where even trace amounts of silicone contamination can disrupt display production or semiconductor fabrication, producers like Nitto and Shin-Etsu are introducing pressure-sensitive adhesives (PSAs) with variable adhesion strengths that leave minimal residue while eliminating silicone entirely. Beyond performance, worker health and safety are also key drivers. A 2024 report by Sika Industry highlighted how sustainable vehicle manufacturing is transitioning to water-based and solvent-free adhesive systems, which reduce the need for complex ventilation systems and lower overall plant operating costs. Environmental sustainability adds a further layer of momentum, with players such as Evonik prioritizing eco-conscious adhesives designed to emit minimal or zero VOCs while delivering high levels of adhesion and durability for automotive and electronic applications. Together, these developments underscore how low/no VOC and silicone-free chemistries are becoming the new standard for high-value protective film applications.

Integration of Functional and Smart Properties into Protective Films

Surface protection films are no longer passive layers but are evolving into multi-functional materials with embedded smart features that enhance both manufacturing efficiency and end-user experiences. In the automotive industry, companies such as Argotec have advanced paint protection films (PPF) made from thermoplastic polyurethane (TPU), which offer scratch resistance, UV stability, and self-healing capabilities that restore the surface when exposed to heat or sunlight. At the frontier of electronics and automotive design, Covestro has showcased films that integrate lighting and sensor functions into 3D plastic surfaces, creating seamless human-machine interfaces (HMI). This convergence of protective films and electronic functionality is redefining product design and user engagement. Meanwhile, asset tracking is emerging as a futuristic application, with experimental protective films embedding RFID tags to enable real-time inventory management and secure the movement of high-value components across supply chains. As manufacturers increasingly demand materials that not only protect but also enhance product functionality, the integration of smart properties is set to become a defining trend in next-generation protective films.

Capitalizing on the Expansion of Electric Vehicle (EV) Battery Manufacturing

The global surge in EV adoption is creating unprecedented opportunities for surface protection films in battery manufacturing, a highly sensitive and safety-critical sector. Protective films play a pivotal role in maintaining the cleanliness of battery cell production, safeguarding coatings from scratches and preventing contamination by metal particles during assembly. Avery Dennison has developed dielectric films tailored for cell wrapping, offering both electrical insulation and corrosion resistance within battery packs. Beyond cleanliness, films are increasingly used for thermal management, ensuring that components can withstand high temperatures. For example, Versiv Composites highlighted the role of polyimide films in EV motor windings and battery packs due to their outstanding insulation and thermal stability. 3M has further extended protective film applications to structural reinforcement, producing tapes and adhesives designed to guard against thermal runaway, improve pack integrity, and enhance crash resistance. With global EV battery manufacturing capacity expected to grow exponentially through 2030, the integration of surface protection films into battery cells, modules, and packs represents a major revenue driver for the industry.

Addressing the Demand for Sustainable and Monomaterial Film Constructions

Sustainability imperatives are pushing the surface protection film industry to redesign products with recyclability and circularity in mind. The emphasis is now on mono-material innovation, with leading companies such as Mondi and Dow adapting high-barrier mono-material packaging film technology for protective applications. These new designs replace complex multi-layer laminates with single-material films made entirely from PE or PP, ensuring compatibility with mainstream recycling systems. Another critical lever is the incorporation of Post-Consumer Recycled (PCR) content, enabling manufacturers to reduce their reliance on virgin feedstocks and align with corporate environmental, social, and governance (ESG) goals. The principle of design for recyclability is also gaining traction, requiring film constructions to be conceived from the outset with recycling efficiency in mind. This not only satisfies regulatory expectations but also resonates with end-use industries under pressure to decarbonize their value chains. As global demand for sustainable materials intensifies, protective films engineered for recyclability and circularity will command a competitive edge, making this one of the most significant opportunities for manufacturers in the coming decade.

Competitive Landscape: Global Leaders Driving Innovation in Surface Protection Films

The adhesion laminated surface protection films industry is consolidated among a few powerful players who leverage material science expertise, acquisitions, and advanced R&D to maintain leadership. Companies are innovating in areas like UV stability, clean removability, and solvent-free adhesive chemistry, while tailoring portfolios for electronics, automotive, and construction sectors.

Nitto Denko Corporation strengthens electronics and automotive protection

Nitto Denko’s E-MASK™ and SPV™ series dominate in electronics, optics, and automotive. With expertise in adhesive chemistry, the company delivers clean-removable, highly specific adhesion levels for delicate panels and metal finishes. In addition to screen and optics protection, its portfolio includes innovations like SLIPGUARD™ anti-slip films and advanced materials for laser cutting processes. Continuous R&D investment ensures Nitto Denko stays ahead in precision and high-value applications.

3M Company leverages brand power and polymer chemistry expertise

3M’s Scotchgard™ and Scotchlite™ films are widely adopted across automotive, aerospace, and construction. The company’s strength lies in polymer chemistry IP and adhesive application know-how, with innovations like 3M™ Comply™ Adhesive Technology for bubble-free application. Its November 2024 Scotchgard update boosted durability, targeting vehicles and aircraft exposed to extreme environments. 3M’s films are also integral to architectural finishes and industrial manufacturing, making it a cross-industry leader.

Covestro AG advances sustainability through material science and acquisitions

Covestro supplies polycarbonate and polyurethane films and in August 2025 acquired Pontacol, entering the adhesive film production space directly. This move extends Covestro’s footprint beyond raw materials into finished solutions. Its edge lies in bio-based, recycled, and ISCC PLUS-certified mass-balanced materials, aligning with circular economy principles. Covestro’s innovation pipeline is focused on residue-free, durable, and recyclable adhesive formulations, making sustainability its primary market differentiator.

Sekisui Chemical Co. Ltd. expands advanced co-extrusion solutions

Sekisui Chemical specializes in multi-layer co-extrusion technologies delivering high transparency, stain resistance, and heat durability for films used in displays and EV batteries. It remains a critical supplier to the electronics and automotive sectors, including interior and exterior parts for EVs. With a focus on reducing VOCs and enhancing thermal resistance, Sekisui is innovating adhesive films that align with next-generation mobility and electronics manufacturing needs.

Tesa SE introduces professional-grade construction protection films

Tesa SE, part of Beiersdorf, is well known for adhesive tapes and films designed for construction, renovation, and painting. Its January 2025 product launch showcased films designed for windows, flooring, and spray-painting applications, featuring anti-spotting technology and user-friendly dispensers. Tesa’s strength lies in brand trust, ease-of-use, and clean removal, making it a preferred supplier for craftsmen and contractors in the construction sector.

Adhesion Laminated Surface Protection Films market Share Insights

Market Share by Adhesive Type in Adhesion Laminated Surface Protection Films

Acrylic-based adhesives dominate the adhesion laminated surface protection films market with a 48% share in 2025, driven by their superior balance of adhesion strength, clarity, durability, and resistance to UV and oxidation. These qualities make acrylic formulations the preferred choice for protecting high-value materials such as stainless steel, painted finishes, and engineered plastics that require long-term, residue-free performance. Their versatility across multiple industries including automotive, aerospace, and electronics cements their leadership. Rubber-based adhesives hold a significant 25% share, particularly in short-term and aggressive bonding applications. Their high tack and ability to adhere to low-energy plastics like polyethylene and polypropylene make them essential for plastic fabrication and construction industries. However, their poor UV resistance and residue issues limit their use to indoor or temporary applications. Silicone-based adhesives, while a smaller portion of the market, are critical for specialized, high-value applications. Their unique ability to withstand extreme temperatures such as powder coating or soldering environments and leave no residue on delicate surfaces like polished metals or optical-grade plastics justifies their premium pricing. Finally, the “other adhesives” category includes declining solvent-based systems, constrained by VOC regulations, and innovative bio-based or hot-melt adhesives. These emerging solutions reflect the industry’s push toward sustainability and regulatory compliance, although they are still evolving in performance and adoption.

Market Share by Application in Adhesion Laminated Surface Protection Films

Metal surfaces lead the application segment with a 32% share in 2025, reflecting the massive global demand for protective films in automotive body panels, aerospace components, and stainless-steel appliances. The need to maintain pristine finishes through manufacturing and logistics makes films with high durability and controlled adhesion essential. Plastic surfaces follow closely with a 28% share, underscoring their role in industries such as construction, electronics, and consumer goods. Acrylic sheets, polycarbonates, and composite panels rely heavily on protection films to avoid scratches and chemical exposure during fabrication and installation. Glass and mirrors represent a high-value niche within the market. The replacement cost of large architectural glass panels or decorative mirrors is immense, making protection films indispensable. Here, optical clarity and residue-free removal are non-negotiable, often requiring premium acrylic or silicone adhesives. Painted surfaces form another critical application area, particularly in automotive and appliance industries. Films designed for this segment must balance adhesion strength to ensure stability during transit while avoiding damage or residue upon removal. Decorative laminates and other specialty applications, including textiles and carpets in construction projects, illustrate the diversification of use cases. These segments are expanding steadily as industries recognize the cost savings and quality assurance benefits of laminated protection films, extending the market beyond its traditional strongholds.

United States: Self-Healing Films and Sustainable Adhesives Reshaping Market Demand

The United States is one of the most technologically advanced and innovation-driven markets for adhesion laminated surface protection films, with self-healing films leading adoption in the automotive sector. Paint protection films (PPF) embedded with heat-activated self-repair properties are becoming increasingly common as automakers and aftermarket providers prioritize vehicle aesthetics and longevity. Sustainability is also gaining traction, with manufacturers exploring bio-based plastics and recyclable solutions in response to consumer demand and corporate sustainability pledges. Another crucial growth factor is the advancement in adhesive technology, particularly the shift toward solvent-free, water-based, and UV-curable adhesives that provide high-performance bonding without leaving residues upon removal. The U.S. market also benefits from strong uptake in consumer electronics, where films protect smartphones, tablets, and flat-screen displays during manufacturing and distribution. Strategic moves, such as XPEL, Inc.’s acquisition of POLIFILM Australia’s division, underline the U.S. industry’s emphasis on global expansion and reinforcing supply chain networks.

China: Construction Growth and Cost-Effective Manufacturing Driving Film Adoption

China represents one of the largest markets for adhesion laminated surface protection films, supported by rapid urbanization and the country’s construction boom. The surge in infrastructure development and decorative material usage fuels demand for protective films for laminates, glass, and metals. At the same time, China’s position as a global automotive and electronics manufacturing hub makes it a critical consumer of these films to safeguard high-value products during assembly and transit. Government policies emphasizing environmental responsibility are pushing domestic manufacturers to adopt sustainable production practices and develop eco-friendly alternatives, aligning with the broader green manufacturing trend. However, the market remains defined by cost efficiency, with Chinese manufacturers focusing on delivering high-quality but competitively priced films for both domestic use and exports, strengthening China’s global dominance in protective film supply.

Germany: Precision Engineering and R&D Setting Industry Standards

Germany’s adhesion laminated surface protection films market thrives on its leadership in precision engineering and high-tech manufacturing, especially in the automotive and industrial sectors. German automakers’ stringent quality requirements make surface protection films indispensable for safeguarding vehicles throughout production and delivery. Strong EU-driven environmental regulations, coupled with Germany’s own circular economy goals, are accelerating the transition toward recyclable and sustainable protective films. Germany also stands out as a hub for R&D in advanced material science, with manufacturers developing films that offer superior UV and chemical resistance along with tailored adhesion characteristics for specialized substrates. This innovation-driven ecosystem cements Germany’s role as a leader in next-generation protective film technologies while setting benchmarks for global quality standards.

India: Infrastructure Growth and Domestic Manufacturing Boosting Demand

India’s adhesion laminated surface protection films market is being reshaped by rapid infrastructure and housing growth, where protective films safeguard surfaces such as marble, stone, windows, and doors during construction projects. The government’s “Make in India” initiative has further accelerated the expansion of local manufacturing, encouraging domestic producers to meet the rising demand across industries. The automotive sector is another strong contributor, with increasing car production necessitating films to protect vehicle exteriors and interiors during logistics. Domestic companies like Ecoplast Ltd. are expanding their offerings to serve niche applications, such as construction site protection, positioning themselves as key players in meeting India’s fast-growing consumption needs. This combination of infrastructure expansion, manufacturing momentum, and rising automotive output makes India one of the most promising growth frontiers for protective films in Asia.

Japan: Electronics Precision and Adhesive Innovation Defining Market Growth

Japan’s adhesion laminated surface protection films market is strongly influenced by its advanced electronics sector, where manufacturers rely on high-performance, residue-free films to safeguard delicate displays and precision components. The market also reflects Japan’s emphasis on product durability and longevity, with demand skewed toward high-quality films engineered for extended use in challenging environments. Japanese firms are global leaders in adhesive technology, investing heavily in R&D for self-adhesive systems that ensure maximum protection without damaging sensitive surfaces upon removal. These innovations align closely with the premium standards of Japan’s electronics and automotive sectors, underscoring the country’s role as a pioneer in high-performance protective film technologies.

South Korea: Display Manufacturing and Hydrophobic Film Innovation Powering Growth

South Korea’s adhesion laminated surface protection films market is fueled by its dominance in global display technology, with protective films playing a vital role in safeguarding television, smartphone, and advanced screen surfaces during manufacturing and shipment. The country’s vibrant automotive aftermarket is another significant driver, where consumers increasingly adopt paint protection films (PPF) to preserve vehicle aesthetics and resale value. Beyond these sectors, Korean manufacturers are innovating with hydrophobic films that resist stains and enable easier cleaning, appealing to both electronics and automotive applications. This combination of leadership in display technology, automotive aftermarket expansion, and advanced material innovation positions South Korea as a high-value contributor to the global protective film landscape.

Adhesion Laminated Surface Protection Films Market Report Scope

Adhesion Laminated Surface Protection Films market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.9 Billion

|

|

Market Size (2034)

|

$3.3 Billion

|

|

Market Growth Rate

|

6.3%

|

|

Segments

|

By Material Type (Polyethylene, Polypropylene, Polyurethane, Polyvinyl Chloride, Polyethylene Terephthalate, Others), By Adhesive Type (Solvent-Based Adhesives, Water-Based Adhesives, Rubber-Based Adhesives, Acrylic-Based Adhesives), By End-Use Industry (Automotive, Construction & Interior, Electrical & Electronics, Industrial Manufacturing, Healthcare, Others), By Application (Plastic Surfaces, Metal Surfaces, Glass & Mirror, Painted Surfaces, Textiles & Carpets, Decorative Laminates, Others)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Nitto Denko Corporation, DuPont de Nemours, Inc., Saint-Gobain Performance Plastics, Avery Dennison Corporation, LINTEC Corporation, SEKISUI CHEMICAL CO., LTD., XPEL, Inc., POLIFILM PROTECTION GmbH, Shurtape Technologies, LLC, Tesa SE, Pregis LLC, Pregis PolyMask, Ecoplast Ltd., ECHOtape, Chargeurs S.A.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Adhesion Laminated Surface Protection Films market Segmentation

By Material Type

- Polyethylene

- Polypropylene

- Polyurethane

- Polyvinyl Chloride

- Polyethylene Terephthalate

- Others

By Adhesive Type

- Solvent-Based Adhesives

- Water-Based Adhesives

- Rubber-Based Adhesives

- Acrylic-Based Adhesives

By End-Use Industry

- Automotive

- Construction & Interior

- Electrical & Electronics

- Industrial Manufacturing

- Healthcare

- Others

By Application

- Plastic Surfaces

- Metal Surfaces

- Glass & Mirror

- Painted Surfaces

- Textiles & Carpets

- Decorative Laminates

- Others

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Adhesion Laminated Surface Protection Films market

- Nitto Denko Corporation

- DuPont de Nemours, Inc.

- Saint-Gobain Performance Plastics

- Avery Dennison Corporation

- LINTEC Corporation

- SEKISUI CHEMICAL CO., LTD.

- XPEL, Inc.

- POLIFILM PROTECTION GmbH

- Shurtape Technologies, LLC

- Tesa SE

- Pregis LLC

- Pregis PolyMask

- Ecoplast Ltd.

- ECHOtape

- Chargeurs S.A.

* List Not Exhaustive

Research Coverage

This report investigates the global adhesion laminated surface protection films market with a focus on performance-driven innovations and sustainability transitions; it synthesizes recent breakthroughs in adhesive chemistries and solvent-free laminations, analysis reviews of sector-specific use-cases (electronics, automotive, construction, EV batteries) and highlights commercial pilots, M&A moves, and material-science roadmaps that materially affect specification and sourcing decisions this report is an essential resource for procurement leads, OEM engineers, product-quality teams, and sustainability officers. USDAnalytics combines primary interviews with R&D heads, converter executives and end-user buyers, with proprietary scenario modelling to quantify adoption pathways, lifecycle trade-offs, and cost-to-protect metrics; the study maps high-value use cases, supplier capabilities, and priority R&D pockets so decision-makers can rapidly translate technical options into procurement specifications and circularity roadmaps.

Scope Highlights

- Segmentation: By Material Type (Polyethylene, Polypropylene, Polyurethane, Polyvinyl Chloride, Polyethylene Terephthalate, Others); By Adhesive Type (Solvent-Based, Water-Based, Rubber-Based, Acrylic-Based); By End-Use Industry (Automotive, Construction & Interior, Electrical & Electronics, Industrial Manufacturing, Healthcare, Others); By Application (Plastic Surfaces, Metal Surfaces, Glass & Mirror, Painted Surfaces, Textiles & Carpets, Decorative Laminates, Others).

- Geographic Scope: “Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.”

- Timeframe: Historical data from 2021–2024 and forecast horizon 2025–2034.

- Companies: Detailed analysis and profiles of 15+ leading suppliers and innovators (material producers, adhesive formulators, converters, and specialty film manufacturers).

Methodology

The study applies a mixed-methods approach combining structured primary research (executive and technical interviews with coating/adhesive scientists, converter plant managers, OEM specifiers, and procurement teams) and extensive secondary research (corporate filings, patent landscapes, trade conference proceedings, standards and regulatory texts). Market sizing uses a hybrid bottom-up/top-down model that reconciles installed capacity, historical shipment and replacement cycles, and end-use consumption by application; technology-adoption curves were derived from pilot deployments and licensing activity, and lifecycle impacts were estimated using standard LCA inputs adjusted for regional recycling-stream assumptions. Findings were validated through cross-checks with CAPEX announcements, supplier roadmaps, and trade-show product launches to ensure practical, procurement-grade recommendations and scenario-tested forecasts.

Deliverables:

• Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

• Country-Specific Forecasts & Analysis.

• Segment-Wise Revenue Forecasts (2025–2034).

• Competitive Analysis, Benchmarking, and SWOT Profiles.

• Recent Developments & Innovation Tracker.

• Executive Summary & Analyst Commentary.

• Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.