Explosive Growth Outlook for Advanced Materials in EV Charging Infrastructure Market to 2035

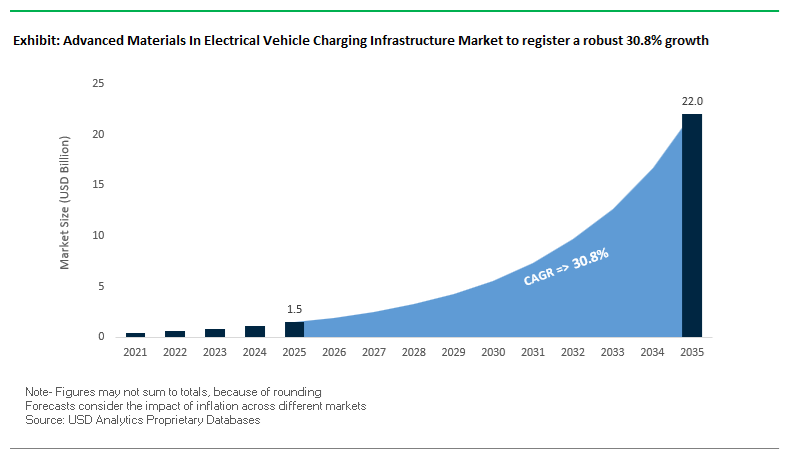

The Advanced Materials in Electrical Vehicle Charging Infrastructure Market is projected to grow from USD 1.5 billion in 2025 to around USD 22 billion by 2035, registering an exceptionally high CAGR of 30.8% (2025–2035). This surge is driven by rapid rollout of ultra-fast DC charging, 800V EV architectures, and megawatt charging systems (MCS), all of which require advanced polymers, composites, and high-performance insulators to manage heat, voltage, safety, and durability. For materials manufacturers and EV charging vendors, this means a decade of sustained demand for thermally conductive, flame-retardant, and high-dielectric-strength materials tailored for high-power, outdoor charging environments.

Advanced polymer composites in 350 kW+ DC fast-charging cables now need thermal conductivity above 5 W/m·K (often achieved using boron nitride or alumina fillers) to prevent overheating and thermal runaway during peak loads. High-voltage DC cables supporting 800 V EV architectures must maintain dielectric strength ≥ 20 kV/mm, even under harsh ambient conditions, moisture, and mechanical stress. At the same time, the industry faces a clear engineering challenge: connectors and advanced polymer housings must withstand ≥10,000 mating cycles while maintaining contact resistance below 50 micro-ohms, aligned with uptime targets such as the 97% availability goal in the US. On the safety side, all structural polymers in public DC fast-charging station enclosures are expected to comply with UL 94 V-0 self-extinguishing standards, while megawatt charging cables increasingly shift from copper to aluminum conductors with advanced jacketing, delivering 30–45% weight reduction and better ergonomics without compromising ampacity.

Key insights for manufacturers & vendors in the advanced EV charging materials market:

- Thermally conductive polymers with TC > 5 W/m·K are becoming standard for 350 kW+ DC fast-charging cables and connectors, especially when air or liquid cooling is constrained.

- High-dielectric, weatherable insulation systems (≥ 20 kV/mm) are critical for 800 V architectures and next-gen high-voltage DC bus systems in public chargers.

- Mechanical durability and low contact resistance (≥10,000 cycles, <50 μΩ) are now commercial differentiators for connector and inlet suppliers targeting 97%+ uptime requirements.

- Fire-safe, UL 94 V-0 structural polymers are mandatory for public DC charging enclosures to meet stringent building and safety codes globally.

- Lightweight aluminum-conductor cable systems with advanced jacketing are enabling 30–45% weight reduction in Megawatt Charging System (MCS) cables, improving handling and lowering system cost of ownership.

Regulatory Schemes and Material Breakthroughs Accelerate EV Charging Materials Adoption

Regulatory push, national incentive schemes, and performance-driven design changes are rapidly redefining the advanced materials in EV charging infrastructure market. In September 2024, the Government of India formally notified the PM E-DRIVE Scheme with an outlay of about ₹10,900 crore (≈USD 1.3 billion), of which ₹2,000 crore is earmarked specifically for deploying public EV charging stations. This policy directly boosts demand for high-performance polymers, insulators, and flame-retardant materials as charge point operators (CPOs) scale networks across India. In the same month, India’s Ministry of Power (MoP) issued revised EV charging infrastructure guidelines, tightening interoperability and safety requirements, translating into stricter specifications for connector materials, cable insulation, and enclosure compounds. These regulatory frameworks effectively push OEMs and material suppliers toward higher dielectric strength, enhanced fire performance, and better environmental durability in high-voltage components.

On the innovation front, leading materials companies are repositioning their portfolios around EV charging infrastructure. In 2025, BASF launched a new polyamide (PA) compound designed for high-voltage battery modules and connectors, combining enhanced thermal stability and dielectric performance—key attributes for safe fast charging at 400–800 V and above. In late 2025, DuPont introduced a high-performance fluoropolymer specifically for DC fast-charging cable jackets, engineered for flexibility and superior resistance to UV radiation, ozone, and abrasion to extend outdoor lifetime. Meanwhile, in 2025, Bolt.Earth launched the Blaze DC, India’s first universally compatible DC fast charger for 2- and 3-wheelers, catalyzing demand for impact-resistant polymer enclosures and compact, thermally stable materials for light EV charging in dense urban environments.

Material reliability and power electronics performance are also being tightened through research and cost pressures. In 2025, Teledyne FLIR highlighted the use of thermal imaging to identify material degradation in high-power DC connectors, underscoring the need for improved thermal management in polymer housings and contact systems. In ongoing 2025, Linde and BASF continued their collaboration around high-purity precursor materials for silicon carbide (SiC) power semiconductors, a core technology enabling efficient DC fast chargers and on-board power conversion. At the same time, tariffs and electricity cost dynamics are influencing material choices: the Tamil Nadu Tariff Order in July 2025 raised rates and fixed charges for high-tension EV charging connections, pushing CPOs to invest in higher-efficiency, longer-life materials for transformers, switchgear insulation, and passive components to protect margins over the asset lifetime. Collectively, these developments point to a market where advanced polymers, composites, and SiC-related materials become central levers for safety, uptime, and total cost of ownership in EV charging infrastructure.

Advanced Materials In Electrical Vehicle Charging Infrastructure Market Share Analysis

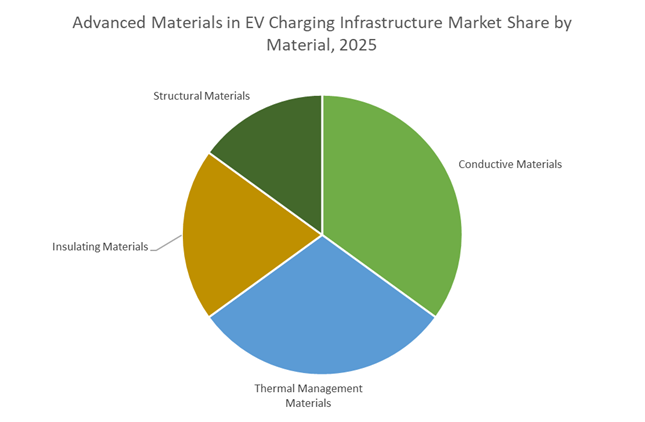

Market Share by Material Function: Conductive Materials Lead Due to High-Power Requirements of Fast-Charging Infrastructure

Conductive materials account for the largest share of the advanced materials used in EV charging infrastructure—approximately 35% in 2025—because they form the indispensable electrical pathway that carries high voltages and exceptionally high currents throughout both AC and DC charging systems. As DC Fast Charging (Level 3) expands globally, the need for high-purity copper, aluminum conductors, and advanced alloyed conductors increases substantially, since these materials must minimize resistive losses (I²R losses) while maintaining mechanical flexibility and long-term reliability. High-power charging stations routinely operate at 200–500 A and up to 1,000 V, making conductor cross-section, purity, and thermal stability critical design constraints. Cables, connectors, shielded harnesses, busbars, rectifier windings, and grid interconnection hardware all consume large volumes of conductive materials, with copper often representing the single largest cost component in a fast-charging station bill of materials. As global OEMs, utilities, and charging network operators deploy hundreds of thousands of fast-charging ports, conductive materials remain the highest-volume and highest-value category within the advanced materials landscape. Their market leadership is further reinforced by the trend toward ultra-fast charging and megawatt-scale charging, which will only increase the demand for enhanced-conductivity materials and high-power electrical components.

Market Share by Charging Level: DC Fast Charging (Level 3) Dominates Due to Its Central Role in Enabling Mass EV Adoption

DC Fast Charging (Level 3) commands the largest share of the charging infrastructure market—approximately 50% in 2025—because it is the cornerstone technology that addresses EV range anxiety and enables long-distance driving, commercial fleet electrification, and high-speed public charging networks. Delivering 50 kW to 350 kW of power, Level 3 systems drastically reduce charging times, allowing EVs to reach 20–80% state-of-charge in 20–40 minutes, a requirement for consumer convenience and operational uptime for ride-hailing fleets, logistics operators, and highway corridor charging hubs. The high power levels involved necessitate advanced conductive, insulating, and thermal management materials, making DC fast chargers significantly more material-intensive and higher-value compared to AC Level 1/2 chargers. As governments worldwide roll out aggressive EV infrastructure funding programs, and as private charging operators prioritize high-throughput stations that maximize revenue per site, Level 3 installations continue to expand faster than any other charging category. This sustained investment—combined with the technical necessity for more complex materials, liquid-cooled cables, and high-power electronics—ensures DC Fast Charging remains the dominant segment shaping the advanced materials demand profile for EV charging infrastructure.

Country Analysis: Global Drivers in Advanced Materials for EV Charging Infrastructure

China: Accelerated Charging Network Expansion and High-Conductivity Copper Alloy Optimization

China holds the most influential position in the global Advanced Materials for EV Charging Infrastructure Market due to its unmatched scale in charging deployment and world-leading material processing capabilities. With over 3.2 million public charge points in operation as of mid-2024, China’s demand for advanced materials is proportionally massive, driving widespread adoption of high-conductivity copper alloys, polymeric insulation systems, and engineered plastics optimized for durability in high-traffic environments. The country’s heavy reliance on GB/T ultra-fast DC charging standards amplifies material requirements, as connectors, busbars, and high-power cables must safely handle power levels exceeding those used in typical AC installations. This results in strong market pull for nanostructured copper alloys, enhanced aluminum conductors, and high-grade thermoplastics capable of minimizing resistive losses during >350 kW charging cycles.

Policy-led durability mandates intensify the pace of material innovation. Local governments require charging infrastructure to withstand harsh environmental conditions—heat, UV radiation, particulate exposure—fueling the adoption of impact-resistant, flame-retardant polycarbonates and UV-stabilized engineered plastics for kiosks, enclosures, and housings. China’s vertically integrated metals industry also supports strategic stockpiling and processing of high-purity copper and aluminum, reducing dependence on external suppliers and enabling rapid scaling of conductor materials essential for ultra-fast charging stations. Combined, these forces position China as the global manufacturing and deployment epicenter for advanced EV charging materials.

United States: NEVI-Funded Network Standardization and the Shift Toward NACS-Compatible High-Performance Materials

The United States is shaping the future of EV charging materials through large-scale federal investment and a pivotal transition toward the North American Charging Standard (NACS). The NEVI program, backed by the Bipartisan Infrastructure Law, underpins a nationwide mission to deploy 500,000 public chargers by 2030, accelerating the procurement of certified, high-durability materials compliant with Buy American, UL, and NEC safety frameworks. This expansion accelerates industry-wide demand for advanced thermoplastics, silver-plated copper conductors, high-heat-resistant cable insulation materials, and reinforced polymer composites designed for long-term reliability under high electrical stress.

The rapid transition to the NACS connector architecture has catalyzed new R&D in high-temperature polymers and precision-engineered conductive materials. Because the NACS format is physically smaller yet capable of supporting high continuous currents, U.S. manufacturers are optimizing materials to improve thermal transfer, electrical contact integrity, and mechanical durability. Simultaneously, the rise of SiC Wide-Bandgap semiconductors in DC fast chargers has elevated demand for advanced thermal interface materials (TIMs), aluminum nitride substrates, and silicon nitride heat spreaders, which are essential for thermal stability in high-frequency switching environments. Additionally, U.S. research institutions—including the University of Michigan and Utilidata (2024)—are advancing sensor-embedded grid edge materials to support future Vehicle-to-Grid (V2G) programs. These next-generation materials enable smart load management, real-time performance monitoring, and predictive maintenance, making the U.S. a leader in intelligent, materials-driven EV charging infrastructure innovation.

European Union: AFIR-Driven Ultra-Fast Corridor Expansion and Sustainable Polymer Innovation

Europe’s EV charging materials market is shaped by stringent regulatory frameworks and cross-border interoperability targets, most notably the Alternative Fuels Infrastructure Regulation (AFIR), which mandates high-power charging corridors every 60 km by 2025. These regulations significantly increase demand for heat-tolerant polymers, high-power thermal management systems, reinforced enclosure materials, and advanced corrosion-resistant metal alloys. Ultra-fast charging stations operating across varying climates—from Mediterranean heat to Northern European winters—require materials that deliver consistent performance and long-term durability. This drives adoption of specialized stainless steel grades, anti-corrosion coatings, TPU sheathing materials, and high-impact polymer blends engineered for harsh outdoor public use.

Sustainability is a core European priority. Manufacturers such as Covestro AG are now commercializing renewable-based polycarbonates (Makrolon, Bayblend) designed specifically for EV charger housings and structural components, fulfilling EU Green Deal and circular-economy mandates. Europe’s V2G leadership—driven by large-scale pilots in countries like the Netherlands and the UK—creates additional material demand for bidirectional power components, requiring advanced magnetic materials, arc-resistant insulators, and fast-recovery dielectric compounds capable of withstanding rapid, repeated charge-discharge cycles. Collectively, these policies and innovations make the EU the global leader in sustainable, interoperable, and ultra-fast charging materials infrastructure.

India: Material Innovation Tailored to Two- and Three-Wheeler Dominance and Harsh Climate Conditions

India is rapidly emerging as a high-growth market for advanced EV charging materials, driven by a unique mobility landscape and demanding environmental conditions. Unlike Western markets dominated by four-wheel EVs, India’s charging infrastructure is optimized for two- and three-wheeler fleets, requiring smaller, cost-efficient DC fast chargers that rely heavily on lightweight copper conductors, novel polymer blends, and high-temperature-resistant plastics to withstand prolonged outdoor exposure. Companies such as Bolt.Earth and Tata Power are scaling domestic manufacturing, accelerating R&D into materials that deliver UV resistance, heat tolerance, flame retardance, and low total cost of ownership—critical performance metrics for installations across tropical cities and semi-arid regions.

India’s material innovation ecosystem is gaining momentum through targeted financing. 3ev Industries’ ₹120 crore ($14.4M) funding round (late 2025) supports expanded R&D in structural polymers, weatherproof charger enclosures, and materials for high-efficiency connectors tailored to India’s socioeconomic mobility mix. Additionally, the development of standardized Blaze DC fast chargers for lightweight EVs has accelerated the adoption of light-gauge copper wiring, reinforced polymer casings, and compact heat-dissipating housings designed for safety and affordability. With rising demand for domestically-produced charging hardware and strong government support for localized supply chains, India is becoming a strategic hub for climate-adaptive, cost-optimized advanced materials in EV charging.

Competitive Landscape: Materials Leaders Powering High-Performance EV Charging Infrastructure

The competitive landscape in the advanced materials for EV charging infrastructure market is dominated by a combination of specialty polymer producers, engineering plastics giants, and high-voltage interconnect and system solution providers. Companies such as DuPont, BASF, Covestro, TE Connectivity, and Solvay are shaping material standards for high-voltage connectors, DC fast-charging cables, station enclosures, and SiC-based power electronics. Their strategies converge on three themes: thermal management for 350 kW+ charging, dielectric integrity and fire safety, and sustainability via lightweight and recycled-content polymers. Each player is targeting specific bottlenecks—DuPont and BASF with high-performance polymers, Covestro with robust housing solutions, TE Connectivity with high-current interfaces, and Solvay with ultra-high-performance engineering resins and SiC-related materials for power semiconductors.

DuPont advances high-performance polymers for safe DC fast-charging components

DuPont de Nemours, Inc. is a key global supplier of high-performance polymers and advanced composites used extensively in EV charger connectors, housings, and cable insulation. Its portfolio includes materials such as Zytel® (polyamide) and Vespel® (polyimide), which combine high dielectric strength, thermal resistance, and mechanical stability, making them ideal for high-voltage connector bodies, inlets, and internal structural parts. In late 2025, DuPont launched a new fluoropolymer material for DC fast-charging cable jackets, optimized for flexibility under low temperatures and long-term resistance to UV radiation, ozone, and abrasion, which is critical for outdoor, high-duty-cycle chargers. DuPont’s materials are widely used in applications where connectors must meet stringent thermal cycling and flame-retardant (UL 94 V-0) requirements while safely supporting high current densities. Strategically, the company is promoting lightweight polymer solutions to replace metal in charging station structures and cable assemblies, helping OEMs reduce weight, simplify installation, and improve ergonomics without compromising safety.

BASF delivers thermally conductive polymers and encapsulants for high-voltage charging systems

BASF SE plays a foundational role as the world’s largest chemical company supplying a broad range of engineering plastics, PU systems, and thermally conductive compounds for EV charging infrastructure. Its Ultramid® (polyamide) and polyurethane platforms are widely used in charger enclosures, cable overmolding, and thermal interface materials that dissipate heat from power modules and connectors. In 2025, BASF introduced a new high-heat polyamide grade with improved dimensional stability and dielectric strength specifically targeted at EV battery components and charging connectors, addressing the rising voltage and current levels in fast chargers. BASF’s competence in thermally conductive polymer compounds (TCPCs), often loaded with specialty fillers such as boron nitride, enables effective heat management in DC fast-charger power modules without sacrificing electrical insulation. The company also supplies specialized epoxy and polyurethane resins used for potting and encapsulating power electronics and PCB assemblies within chargers, ensuring robust electrical insulation, moisture resistance, and mechanical protection under continuous high-power operation.

Covestro strengthens durable, aesthetic housings and HMIs for public charging stations

Covestro AG provides high-performance polymer materials that are central to the mechanical robustness, aesthetics, and user interface durability of public EV charging stations. The company’s polycarbonate (PC) and polyurethane (PU) materials are used in transparent covers, structural housings, and protective outer shells of chargers, where impact resistance (high IK rating) and UV/weatherability are essential for long-term outdoor deployment. Covestro’s PC blends are widely adopted for charging station housings, where they protect internal electronics from vandalism, impacts, and harsh climate conditions while maintaining good design flexibility and surface quality. The company also delivers weather-resistant coatings and polycarbonate films for human–machine interface (HMI) displays, ensuring that touchscreens and indicators maintain their optical clarity and mechanical integrity over millions of user interactions. Aligning with the European Green Deal, Covestro actively promotes mass-balance and recycled-content polymers for EV charging infrastructure components, enabling CPOs and OEMs to reduce carbon footprint without compromising performance.

TE Connectivity enables high-current, liquid-cooled connectors for megawatt charging

TE Connectivity stands out on the interconnect side, focusing on high-voltage and high-current connector systems and customized cable assemblies that form the backbone of DC fast-charger power trains and vehicle–charger interfaces. The company designs high-current connectors capable of safely carrying ≥500 A, making them suitable for Megawatt Charging System (MCS) applications and ultra-fast charging of commercial vehicles. TE’s connectors leverage advanced copper/silver contact materials optimized for low resistance and efficient heat dissipation, supporting sustained high-power transfer while limiting temperature rise. The company also integrates shielding and interference suppression materials within connector housings to maintain signal integrity for CAN bus and high-speed data communication, which is crucial for smart charging, authentication, and billing. A major pillar of TE’s strategy is its investment in liquid-cooled cable and connector systems, a technology essential for enabling >400 kW charging without exceeding the 60°C allowable touch temperature for cables, directly impacting user safety and regulatory compliance.

Solvay supplies ultra high-performance polymers and EMI-shielding solutions for power electronics

Solvay S.A. focuses on high-temperature polymers and composite materials that address the extreme performance demands of connectors, sensors, and thermal management components within EV charging infrastructure. Its portfolio includes Polyether Ether Ketone (PEEK) and Polyphenylene Sulfide (PPS), which deliver stable mechanical and electrical properties at temperatures exceeding 150°C, making them ideal for densely packed power electronics and high-voltage connector systems. Solvay places strong emphasis on inherently flame-retardant (FR) polymers that achieve UL 94 V-0 ratings without halogenated additives, helping OEMs meet strict safety and environmental regulations for public charging infrastructure. Beyond polymers, Solvay supplies precursor materials and high-purity wafers for silicon carbide (SiC) devices, contributing to the core power semiconductor technology that underpins the efficiency of modern DC fast chargers. Additionally, the company actively markets conductive polymer composites for electromagnetic interference (EMI) shielding in charger power electronics, ensuring reliable operation and compliance with FCC and CE regulations while enabling compact, high-frequency designs.

Advanced Materials In Electrical Vehicle Charging Infrastructure Market Report Scope

Advanced Materials In EV Charging Infrastructure Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.5 Billion

|

|

Market Size (2035)

|

$22 Billion

|

|

Market Growth Rate

|

30.8%

|

|

Segments

|

By Material Function (Conductive Materials, Insulating Materials, Thermal Management Materials, Structural Materials), By Component Application (Charging Cables & Connectors, Charging Station Enclosures/Housings, Power Conversion Electronics, Grid Connection/Transformers), By Charging Level (AC Charging, DC Fast Charging, Ultra-Fast DC Charging)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

TE Connectivity, Infineon Technologies, Wolfspeed, Covestro, DuPont, ABB, Delta Electronics, Molex, Rogers Corporation, Ryerson, Eaton Corporation, Siemens, Parker Hannifin, Hanwha Advanced Materials, Heraeus Group

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Advanced Materials in EV Charging Infrastructure Market Segmentation

By Material Function

- Conductive Materials

- Insulating Materials

- Thermal Management Materials

- Structural Materials

By Component Application

- Charging Cables & Connectors

- Charging Station Enclosures / Housings

- Power Conversion Electronics

- Grid Connection / Transformers

By Charging Level

- AC Charging (Level 1 & 2)

- DC Fast Charging (Level 3)

- Ultra-Fast DC Charging (>350 kW)

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Advanced Materials in EV Charging Infrastructure Market

- TE Connectivity

- Infineon Technologies

- Wolfspeed

- Covestro

- DuPont

- ABB

- Delta Electronics

- Molex

- Rogers Corporation

- Ryerson

- Eaton Corporation

- Siemens

- Parker Hannifin

- Hanwha Advanced Materials

- Heraeus Group.

*- List not Exhaustive

Research Coverage

This USDAnalytics study on the Advanced Materials in Electrical Vehicle Charging Infrastructure Market provides a deep-dive strategic intelligence framework as this report investigates how thermally conductive polymers, high-dielectric insulators, structural composites, and advanced conductive metals are reshaping next-generation AC, DC fast-charging, ultra-fast, and megawatt charging systems. The study tracks breakthroughs in 800V architectures, SiC-enabled power electronics, lightweight aluminum conductor systems, liquid-cooled high-power cables, and UL 94 V-0 fire-safe enclosure materials, while our analysis reviews the impact of policy schemes (NEVI, AFIR, PM E-DRIVE) on material specification and standards. It highlights reliability-critical metrics such as thermal conductivity, dielectric strength, mating-cycle durability, contact resistance, and weatherability, alongside evolving OEM sourcing and localization strategies. Covering value chain dynamics from material formulators to charge point operators and grid OEMs, this report is an essential resource for EV charging equipment manufacturers, polymer and composite suppliers, semiconductor and substrate vendors, utilities, fleet operators, and infrastructure investors seeking data-driven guidance on performance-critical materials for high-power EV charging networks through 2035.

Scope Highlights

- Segmentation:

By Material: Conductive Materials, Insulating Materials, Thermal Management Materials, Structural Materials

By Component Application: Charging Cables & Connectors; Charging Station Enclosures / Housings; Power Conversion Electronics; Grid Connection / Transformers

By Charging Level: AC Charging (Level 1 & 2); DC Fast Charging (Level 3); Ultra-Fast DC Charging (>350 kW)

- Geographic Scope: Analysis spans 25+ key markets across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa, mapping material demand to differing policy regimes, grid conditions, and EV adoption curves.

- Time Frame: Historic market, technology, and policy data from 2021–2025 with detailed quantitative and qualitative forecasts for 2026–2034, including CAGR trajectories by material function, component application, and charging level.

- Companies Covered: Competitive benchmarking, strategy profiling, and product portfolio analysis / reviews for 15+ leading players across materials and systems, including TE Connectivity, Infineon Technologies, Wolfspeed, Covestro, DuPont, ABB, Delta Electronics, Molex, Rogers Corporation, Ryerson, Eaton Corporation, Siemens, Parker Hannifin, Hanwha Advanced Materials, and Heraeus Group.