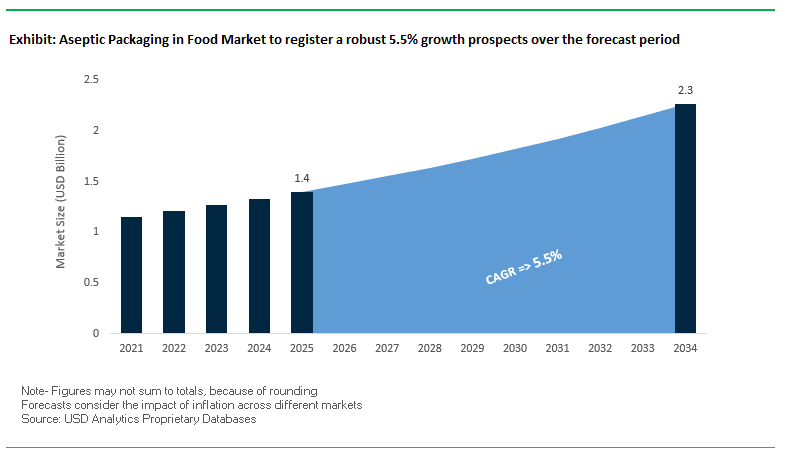

Food Security, Waste Reduction, and Sustainability Push Aseptic Packaging in Food Market to USD 2.3 Billion by 2034

The global aseptic packaging in food market is valued at USD 1.4 billion in 2025 and is projected to reach USD 2.3 billion by 2034, advancing at a steady CAGR of 5.5%. The market’s growth is driven by its ability to extend shelf life without preservatives or refrigeration, ensuring safe transport and storage of food products such as milk, juices, soups, and sauces across global supply chains. By eliminating the dependency on cold chains, aseptic packaging reduces energy consumption while delivering convenience to consumers.

Another key factor is food waste reduction, where aseptic cartons provide robust barriers against light, oxygen, and moisture to minimize spoilage. This is crucial in combating the fact that nearly one-third of global food production is wasted each year. The dominance of paperboard cartons, a renewable material, is also shaping the industry’s sustainability outlook, aligning with consumer preferences and regulatory frameworks demanding eco-friendly solutions. Furthermore, aseptic packaging ensures that products retain their nutritional integrity, flavor, and appearance for up to 12 months, giving both consumers and manufacturers confidence in product quality.

Key Insights for Professionals

- Extended shelf life without refrigeration improves logistics efficiency and consumer accessibility.

- Food waste mitigation is a major sustainability advantage of aseptic packaging.

- Paperboard-based cartons remain the most adopted format, supporting eco-friendly transitions.

- Nutritional preservation ensures that milk, juices, and other liquid foods retain quality for up to a year.

Recycling Recognition, Industry Mergers, and Low-carbon Innovations Redefine Aseptic Food Packaging

The market has seen transformative moves across sustainability, mergers, and material innovation. In August 2025, SIG earned formal recognition from the Association of Plastic Recyclers (APR) for its recycle-ready bag-in-box wine package, validating its focus on circular packaging. In the same month, Smurfit WestRock debuted in New York and London after completing its merger, boosting its influence in paper-based aseptic solutions for industrial food sectors.

Sustainability milestones are reshaping competitive dynamics. In July 2025, Tetra Pak secured the EcoVadis Platinum medal, the highest sustainability rating, further strengthening its ESG credentials. In June 2025, Elopak opened its first U.S. carton converting plant in Arkansas, ensuring localized production to serve growing North American demand. Also in May 2025, DS Smith merged with International Paper, creating a global packaging giant with strong competencies in paper-based aseptic alternatives.

Key product innovations reflect a shift toward low-carbon packaging structures. In May 2025, SIG launched the world’s first aluminum-layer-free aseptic carton material, cutting the carbon footprint by up to 61% while maintaining performance. In April 2025, Tetra Pak and Lactalis introduced a pioneering carton made with certified recycled polymers. Earlier, in January 2025, Elopak’s LCA study showed its D-PAK™ cartons had a significantly smaller footprint than plastic pouches, evidence supporting wider adoption in food packaging.

Breakthrough Trends Redefining the Aseptic Packaging in Food Market

Strategic Shift Towards Full Portfolio Conversion to Plant-Based Polymers

A defining trend in the aseptic packaging in food market is the full-scale shift from fossil-based plastics to plant-based polymers across entire portfolios, not just limited eco-friendly lines. This transformation is driven by brand owner sustainability mandates and rising consumer demand for renewable packaging. Tetra Pak provides a strong case study: in 2022, it sold 8.8 billion packages and 11.9 billion caps with plant-based plastic, representing a 24% and 12% increase respectively from 2021. According to its climate accounting, this transition alone saved 131 kilotonnes of CO₂ compared to fossil-based plastics. Partnerships, like the collaboration with Braskem in Brazil, ensure 100% Bonsucro-certified sugarcane bioethanol sourcing, reinforcing supply chain transparency. Moreover, with 10 factories achieving ISCC Plus certification in 2023, Tetra Pak is enabling its customers to certify their packaging as Carbon Trust carbon neutral, offering brands a powerful consumer-facing sustainability credential. This holistic shift demonstrates how the industry is embedding renewable content into every layer of the aseptic packaging supply chain, making plant-based aseptic packaging a mainstream reality.

Expansion into High-Growth, Non-Traditional Food Categories

Another major trend shaping the global aseptic food packaging market is its rapid expansion beyond traditional dairy and juice applications into high-growth categories such as plant-based beverages, soups, sauces, ghee, and liquid eggs. For example, Asepto in India has pioneered aseptic cartons for ghee, highlighting the adaptability of the technology to local and non-traditional products. The benefits are multifold: extended shelf life without refrigeration, reduced spoilage, and the ability to reach new markets including remote regions. Aseptic processing also preserves sensitive nutrients in juices, baby food, and nutraceutical drinks by minimizing oxidation during heat processing. Furthermore, the versatility of aseptic packaging formats cartons, bottles, and pouches has facilitated its adoption in plant-based milks and desserts, a segment witnessing explosive demand from health-conscious and lactose-intolerant consumers. This growing footprint across diverse food categories signals a structural broadening of aseptic technology’s role, positioning it as a vital enabler of food security, convenience, and sustainability worldwide.

Emerging Opportunities Unlocking Growth in the Aseptic Packaging Industry

Integration of Digital Watermarks to Enable a Circular Economy

A revolutionary opportunity for the aseptic food packaging market lies in adopting digital watermarking technologies, such as those pioneered under the HolyGrail 2.0 initiative. This technology embeds imperceptible codes onto packaging, enabling high-precision sorting in recycling plants. At a trial in Swisttal, Germany, the detection efficiency ranged from 87.9% to 93.8%, processing nearly 56,000 detections per day. Unlike traditional NIR (near-infrared) spectroscopy, watermarking can distinguish between food-grade and non-food packaging at SKU-level precision, unlocking the potential for separate high-quality recycled streams. With backing from over 130 industry players including AIM – European Brands Association, the technology demonstrates scalability and industry-wide momentum. By aligning with strict EU packaging regulations and driving higher-value recyclates, digital watermarks can transform aseptic cartons into circular economy leaders while offering manufacturers a competitive edge in sustainability compliance and recycling efficiency.

Development of Advanced Barriers to Replace Aluminum Foil

One of the most promising opportunities is the replacement of aluminum foil barriers with advanced paper-based or polyolefin-based alternatives to improve recyclability. In 2023, Tetra Pak and Lactogal validated a paper-based barrier aseptic carton across 25 million flavored milk packages, achieving equivalent shelf life performance without the traditional aluminum layer. This innovation reduced the carbon footprint by 33% while boosting the renewable content of the package to 90% (with paperboard at 80%). Such mono-material structures simplify recycling, making them compatible with future circular economy systems. Beyond material innovation, Tetra Pak is committing €100 million over the next decade toward new sealing technologies such as ultrasonic sealing to ensure smooth adoption across food and beverage manufacturers. These advancements represent a paradigm shift in barrier design, moving aseptic cartons toward a fully renewable, recyclable, and low-carbon future while helping brand owners achieve aggressive sustainability targets.

Global Leaders Compete on Sustainability, Efficiency, and Innovation in Aseptic Food Packaging

The competitive landscape is shaped by a handful of global leaders and regional challengers who are investing in sustainability, recyclable materials, and new product formats to strengthen market presence.

Tetra Pak International: Strengthening Global Leadership with Recyclable and Renewable Cartons

Tetra Pak continues to dominate aseptic food packaging, offering seven packaging systems and innovative carton shapes such as the Tetra Prisma Aseptic 300 Edge, launched in collaboration with a European soft drinks brand. Its strategy revolves around food safety, sustainability transformation, customer integration, and innovation for growth. With deep vertical integration and global presence, Tetra Pak is uniquely positioned to deliver on both performance and eco-friendly objectives.

SIG Combibloc: Launching Aluminum-free Aseptic Cartons to Cut Carbon by 61%

SIG is pushing the boundaries of sustainable food packaging. In May 2025, it launched the world’s first aluminum-layer-free aseptic carton material, reducing carbon emissions significantly while maintaining compatibility with existing filling lines. Its SIG Terra portfolio and modular filling systems provide flexibility for diverse food applications. SIG’s expertise in aseptic carton technology and its sustainability-driven product strategy cement its role as a key innovator in the market.

Elopak ASA: Expanding North America and Driving Pure-Pak Sustainability Leadership

Elopak is reinforcing its global reach through the June 2025 opening of its first U.S. carton converting plant. Its 2024 record revenues and target to double revenue by 2030 highlight its growth ambition. Elopak’s flagship Pure-Pak brand emphasizes paper-based designs with tethered caps, while its Pure-Pak Sense Aseptic carton offers extended shelf life with premium aesthetics. Its sustainability-forward strategy, encapsulated in its “Repackaging tomorrow” vision, strengthens its competitive advantage.

Greatview Aseptic Packaging: Providing Cost-competitive Alternatives in Dairy and Beverages

Greatview focuses on serving dairy and non-carbonated beverage sectors with cost-competitive aseptic packaging solutions. The company faced trading suspensions but is restructuring operations, with August 2025 unaudited accounts confirming its recovery path. As an alternative supplier to major incumbents, Greatview offers competitive pricing, responsive customer service, and solid experience in aseptic technology, ensuring it remains a viable challenger in the global market.

Aseptic Packaging in Food Market Share Insights

Standard Aseptic Cartons Remain the Backbone of Food Industry Packaging by Product Type

In the broader aseptic packaging for food industry applications, standard aseptic cartons dominate with 68% share, reflecting their unmatched efficiency in packaging large-scale volumes of liquid dairy and juices. Their high throughput capabilities and superior material efficiency make them indispensable for multinational food producers. Cartons with straws, accounting for 17%, remain integral to the single-serve beverage market, particularly in school nutrition programs and convenience-driven consumption. Shaped cartons continue to carve a premium niche by enhancing brand identity and consumer perception in specialty beverages, while bag-in-box formats are entrenched in the B2B and foodservice supply chains, especially for liquid eggs, bulk soups, and wine. Collectively, this segmentation underscores the balance between cost leadership, convenience, and premiumization within aseptic food packaging formats.

Dairy Products Lead Market Share by Application in Aseptic Food Packaging

Dairy products hold the largest share at 40%, positioning aseptic packaging as the enabler of modern global dairy logistics. By ensuring sterility and long shelf-life without refrigeration, aseptic cartons have transformed milk and liquid dairy distribution in regions lacking robust cold chain infrastructure. Juices and nectars continue as a stronghold, leveraging aseptic technology to preserve natural flavor, vitamins, and freshness without artificial preservatives. Ready-to-drink (RTD) beverages are the fastest-growing application, with plant-based milks, protein shakes, and coffee drinks relying heavily on aseptic formats to balance convenience, portability, and extended shelf life. Soups and sauces benefit from aseptic packaging’s lightweight and non-metallic profile, offering a premium alternative to cans for both consumers and foodservice operators. Baby food, though the smallest segment, is strategically vital: stringent regulatory oversight and parental expectations make aseptic cartons the gold standard for safety and nutritional preservation.

United States: FDA Oversight and Rising Demand for Sustainable Aseptic Cartons

The United States aseptic packaging in food market is shaped primarily by the Food and Drug Administration (FDA), which plays a pivotal role in regulating packaging materials through its database of substances and pre-market consultation program. This structured oversight provides companies with a clear regulatory pathway for the adoption of innovative aseptic packaging technologies that ensure consumer safety. Corporate initiatives are gaining momentum, with companies like Gehl Food & Beverage Companies investing in Tetra Pak® aseptic cartons, meeting the rising consumer preference for convenience, recyclable formats, and long shelf-life products.

Sustainability is at the heart of U.S. aseptic packaging innovation, with companies reducing plastic and aluminum layers to design recyclable cartons that resonate with eco-conscious buyers. The market is also witnessing advancements in smart and active packaging technologies that extend shelf life without refrigeration, directly benefiting dairy, juice, and plant-based beverage producers. The FDA’s stringent food safety mandates not only drive innovation but also reinforce trust, making aseptic packaging indispensable in beverages and dairy, two of the fastest-growing applications in the U.S.

Germany: Regulatory Pressure Fuels Next-Generation Aseptic Carton Innovations

Germany’s aseptic packaging in food industry operates under one of the world’s most rigorous frameworks, with the EU Packaging and Packaging Waste Regulation (PPWR) mandating all packaging to be fully recyclable or reusable by 2030. This regulatory shift is accelerating the adoption of sustainable aseptic packaging, with companies like Hochwald pioneering SIG Terra Alu-free cartons, eliminating aluminum layers and cutting carbon emissions by up to 34%. Such initiatives highlight Germany’s leadership in sustainable innovation and its commitment to reducing environmental impact.

German manufacturers are spearheading the development of next-generation packaging substrates such as grass paper and high-strength recycled fibers, responding to the dual pressure of regulatory compliance and consumer demand for greener products. The food and beverage industry, particularly milk, juices, and soups, remains the core demand driver, supported by heavy R&D investments. Germany’s strong research ecosystem ensures continuous breakthroughs in lighter, stronger, and more eco-friendly aseptic packaging, reinforcing its position as Europe’s innovation hub.

China: Dual Carbon Goals and AI-Driven Aseptic Packaging Manufacturing

China’s aseptic packaging for food sector is expanding rapidly, driven by the government’s “dual carbon” goal, which prioritizes greener industrial practices and restricts the use of non-degradable plastics. This has catalyzed the shift toward paper-based aseptic cartons, making them an essential solution for liquid foods, especially milk and juices. Domestic substitution is a key trend, with local players scaling up to reduce reliance on imports while meeting surging domestic demand.

At the same time, technological modernization is transforming production lines, with the integration of AI, 5G, and industrial internet solutions for smarter and more efficient packaging. Regulatory updates from the State Administration for Market Regulation (SAMR), including the GB standards for packaging safety and additives, ensure that China’s aseptic carton industry aligns with international norms. The rise of e-commerce-driven food sales further strengthens demand for safe, shelf-stable packaging. Combined with new nutrition labeling standards (GB 28050-2025), these reforms position China as a fast-evolving powerhouse in aseptic carton adoption.

India: Government Support and Expanding Dairy Processing Drive Aseptic Carton Adoption

India’s aseptic packaging in food industry is thriving under the government’s “Make in India” and “Zero Effect Zero Defect” initiatives, which encourage local manufacturing excellence and regulatory compliance. The Food Safety and Standards Authority of India (FSSAI) enforces strict packaging norms, ensuring safe and traceable aseptic cartons with regulated migration limits and labeling standards. This regulatory clarity is boosting confidence among both multinational and domestic players investing in India’s food packaging sector.

Technology adoption is another defining trend, with automated packaging systems and QR code-based traceability enhancing consumer engagement and product safety. Global leaders like Tetra Pak are making significant investments in India, further signaling the country’s importance as a growth hub. The rapid expansion of the **food processing sector particularly dairy, fruit-based beverages, and juices **is fueling demand for tamper-evident and recyclable aseptic cartons. Sustainability initiatives, including biodegradable and compostable carton materials, are gaining traction, aligning India’s packaging ecosystem with global environmental priorities.

Brazil: Regulatory Flexibility and AI Integration Enhance Aseptic Packaging Growth

Brazil’s aseptic carton packaging market is undergoing rapid transformation, guided by regulatory updates from ANVISA. The recent RDC 983/2025 introduced a transition period allowing depletion of existing packaging stock, minimizing waste while ensuring compliance with new rules that mandate regulatory numbering on packaging. This regulatory flexibility is helping companies smoothly adapt to reforms without disrupting supply chains.

Technological modernization is evident, with Brazilian packaging companies embracing robotics and AI for defect detection, automated sorting, and quality control, making aseptic packaging more efficient and cost-competitive. The strong growth of the food and beverage sector, particularly in dairy, juices, and soy-based drinks, has spurred investments in safe, sterile packaging solutions. In parallel, sustainability goals are reshaping the industry, with eco-friendly cartons gaining popularity. Brazil’s regulatory alignment with Mercosur standards (RDC No. 961/2025) ensures compliance with broader regional norms, cementing its role as a regional growth hub for aseptic carton packaging.

Japan: Smart Packaging and Biopolymer Innovation Define Market Leadership

Japan’s aseptic packaging for food industry is distinguished by precision manufacturing and smart packaging technologies, making it a leader in innovation-driven growth. The Ministry of Health, Labour and Welfare’s 2025 Food Sanitation Act revisions introduced a positive list system for food-contact packaging, ensuring only approved substances are used. This regulatory clarity provides a secure foundation for technological advancements in aseptic cartons.

A defining trend in Japan is the rise of smart packaging, where sensors and digital tools track freshness, safety, and shelf life, adding new value to aseptic cartons beyond preservation. Companies like Toyo Seikan Group are pioneering lightweight, recyclable aseptic packaging, while academic institutions contribute with research on biopolymers and natural agents to create sustainable alternatives. Functional innovations, such as high dimensional stability and resistance to deformation, highlight Japan’s commitment to high-performance packaging solutions. Together, corporate collaboration, academic research, and regulatory clarity make Japan one of the most advanced markets for aseptic packaging in food.

Aseptic Packaging in Food Market Report Scope

Aseptic Packaging in Food Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.4 Billion

|

|

Market Size (2034)

|

$2.3 Billion

|

|

Market Growth Rate

|

5.5%

|

|

Segments

|

By Product Type (Standard Cartons, Shaped Cartons, Bag-in-Box, Packs with Straws), By Material Type (Paperboard, Plastic, Aluminum), By Application (Dairy Products, Juices & Nectars, Soups & Sauces, RTD Beverages, Baby Food), By End-Use Industry (Food Industry, Beverage Industry

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Tetra Pak, SIG Combibloc Group AG, Elopak ASA, Amcor plc, Mondi Group, Greatview Aseptic Packaging Co., Ltd., DS Smith Plc, Smurfit Kappa Group Plc, Nippon Paper Industries Co., Ltd., Huhtamäki Oyj, Sonoco Products Company, WestRock Company, IPI Srl, Uflex Limited, Toyo Seikan Group Holdings, Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Aseptic Packaging in Food Market Segmentation

By Product Type

- Standard Cartons

- Shaped Cartons

- Bag-in-Box

- Packs with Straws

By Material Type

- Paperboard

- Plastic

- Aluminum

By Application

- Dairy Products

- Juices & Nectars

- Soups & Sauces

- RTD Beverages

- Baby Food

By End-Use Industry

- Food Industry

- Beverage Industry

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Aseptic Packaging in Food Market

- Tetra Pak

- SIG Combibloc Group AG

- Elopak ASA

- Amcor plc

- Mondi Group

- Greatview Aseptic Packaging Co., Ltd.

- DS Smith Plc

- Smurfit Kappa Group Plc

- Nippon Paper Industries Co., Ltd.

- Huhtamäki Oyj

- Sonoco Products Company

- WestRock Company

- IPI Srl

- Uflex Limited

- Toyo Seikan Group Holdings, Ltd.

* List Not Exhaustive

Methodology

USDAnalytics employs a comprehensive, multi-layered research methodology to deliver precise insights into the global aseptic packaging in food market. This approach integrates primary research through in-depth interviews with packaging manufacturers, food and beverage producers, regulatory bodies, and technology innovators, alongside secondary research from company reports, industry journals, patent filings, regulatory frameworks, and credible news sources. Market sizing and forecasting are conducted using proprietary quantitative models that factor historical trends, technological innovations, supply chain dynamics, and evolving consumer preferences for sustainable, plant-based, and renewable packaging materials. Competitive analysis encompasses mergers, acquisitions, capacity expansions, and sustainability initiatives, highlighting the strategies of global leaders such as Tetra Pak, SIG Combibloc, Elopak, and regional challengers. Regional assessments cover key markets including the U.S., Germany, China, India, Brazil, and Japan, focusing on regulatory impacts, local production, material innovations, and sector-specific adoption across dairy, juices, soups, sauces, plant-based beverages, and emerging applications. USDAnalytics triangulates multiple data sources and cross-verifies market trends to ensure actionable, reliable, and forward-looking insights that enable industry professionals to make informed decisions on investment, product development, and sustainability strategies.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.