Banana Paper Market Overview: Circularity, Premium Applications, and Agricultural Waste Valorization

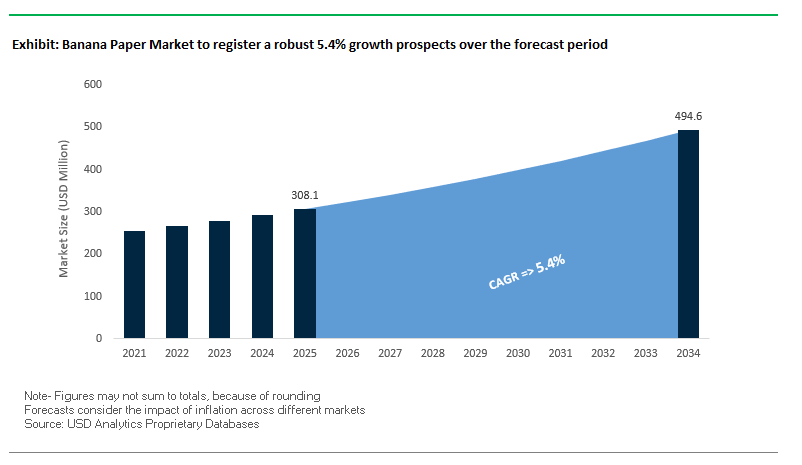

The banana paper market is projected to expand from USD 308.1 million in 2025 to USD 494.6 million by 2034, reflecting a steady CAGR of 5.4%. Positioned at the intersection of sustainability, circular economy, and innovation, banana paper represents a tree-free alternative to traditional pulp that addresses the rising global demand for eco-friendly materials. For industry professionals and procurement leaders, banana paper offers answers to pressing questions on deforestation reduction, waste valorization, premium product positioning, and regulatory alignment with green mandates. The sector is increasingly driven by its unique ability to transform agricultural waste into value-added packaging, stationery, and artisanal paper, while also fostering social impact in banana-growing economies.

Key Insights for Industry Stakeholders

- High cellulose & low lignin advantage: Banana stems contain ~65% cellulose and only 13.5% lignin, reducing the need for heavy chemical processing compared to other non-wood fibers.

- Massive raw material base: Over 50% of the banana plant becomes waste post-harvest, generating 2.5 billion tonnes annually a critical resource pool for paper manufacturing.

- Premium sustainability positioning: Banana paper is gaining adoption in luxury packaging, artisanal stationery, and specialty food packaging due to its distinctive texture and biodegradable properties.

- Community-centered production: Social enterprises in developing regions are leveraging banana paper to create local jobs, increase farmer income, and promote circular economies.

Market Analysis: Technology Breakthroughs and Strategic Collaborations Reshape 2024–2025

The past year has seen banana paper transition from a niche eco-product to a scalable solution for packaging and specialty markets. In August 2025, Papyrus Australia completed trials producing biodegradable molded food packaging at commercial scale, demonstrating the feasibility of banana fiber as a replacement for single-use plastics. This followed July 2025, when a Journal of Natural Fibers study detailed optimized extraction methods that improve fiber efficiency while lowering chemical usage. Academic contributions continued in June 2025, with Taylor & Francis research showcasing a new banana peel lye (BPL)-based pulping agent, providing an eco-friendly delignification pathway.

Strategic partnerships and product launches also accelerated. In April 2025, a European paper manufacturer partnered with a leading packaging company to launch a fiber-based packaging line leveraging banana fiber, signaling growing industrial interest. Meanwhile, in March 2025, a Japanese specialty paper company introduced an artisanal range of banana paper stationery, targeting the luxury and craft markets. Broader sustainability narratives came into focus in February 2025, as Chiquita Brands International spotlighted its “Behind the Blue Sticker” circular economy program, signaling opportunities for banana paper collaborations at scale. Policy and financial backing are also strengthening: in December 2024, a Latin American government announced subsidies for agricultural waste valorization projects, prioritizing banana and coffee byproducts. Industry consolidation remains another theme, with October 2024 reports of M&A activity targeting biodegradable and sustainable technology firms, directly influencing banana paper’s expansion pathway.

Emerging Trends and Opportunities Transforming the Banana Paper Market

Strategic Upcycling of Agricultural Waste into Premium Packaging

The banana paper market is being shaped by the innovative use of agricultural waste, particularly banana pseudostems, which traditionally pose a disposal challenge for farmers. After each harvest, banana plants leave behind massive volumes of biomass that are either burned or left to decay, contributing to pest buildup and environmental stress. However, this waste is now being recognized as a valuable raw material for high-quality paper production. According to a 2024 agricultural waste management report, India alone generates nearly 500 million tonnes of agricultural waste annually, and banana pseudostems represent a significant portion of this untapped resource. Converting this residue into paper not only reduces environmental hazards but also provides farmers with a new income stream. Policy support is reinforcing this momentum. The Government of India’s ni-msme programs on “Emerging Trends in Waste Management in Agriculture” encourage the conversion of agro-waste into commercially viable products. These initiatives, combined with corporate sustainability goals, position banana paper as a strategic innovation in both waste valorization and premium sustainable packaging.

Adoption by Luxury Brands for Sustainable Brand Storytelling

Banana paper’s rise in the luxury sector is a direct response to brands seeking authentic and eco-conscious storytelling tools. Its artisanal texture, natural irregularities, and distinctive tactile quality differentiate it from conventional wood-pulp paper. Luxury brands across stationery, cosmetics, and gourmet food packaging are leveraging banana paper not only for its premium aesthetics but also for its sustainability narrative. For example, packaging made from upcycled banana pseudostems is tree-free, biodegradable, and compostable, offering a powerful brand message to eco-conscious consumers. A study on banana fiber packaging highlights its non-toxic, compostable properties as a unique differentiator in premium markets. Brands are also using banana paper to align with consumer expectations of transparency and responsibility, embedding the material into limited-edition collections and high-value packaging. By transforming agricultural waste into luxury-grade paper, companies are creating a sustainability-driven brand identity that resonates with environmentally aware and premium-focused audiences.

Development of Technical and Industrial Grade Applications

While banana paper is gaining visibility in premium packaging, its potential extends into technical and industrial-grade applications due to its natural strength and durability. Scientific studies highlight banana fiber’s high tensile strength, making it suitable as a reinforcement material in composite applications such as car tires, panels, and industrial products. This positions it as an eco-friendly substitute for synthetic fibers in manufacturing. Academic research in 2024 also pointed to banana paper’s potential in specialty and technical paper markets, including filters, biocompatible sheets, and durable pulp products, all of which require structural integrity and biodegradability. In the logistics industry, banana paper presents opportunities as a biodegradable alternative to styrofoam for fruit and vegetable transportation, ensuring protection without adding to plastic waste. These technical applications expand banana paper’s relevance beyond niche luxury packaging, positioning it as a scalable, industrial-grade solution that can compete with synthetic materials in high-demand sectors.

Securing Supply Chains through Farmer Cooperatives and Geographic Expansion

One of the most pressing opportunities for banana paper manufacturers lies in securing consistent and high-quality raw material supply chains. Today, the sourcing of pseudostems remains fragmented, often limiting scalability. A report on India’s banana value chain demonstrated how Farmer Producer Organizations (FPOs) and cooperatives successfully transformed fragmented agricultural systems by formalizing supply chains and stabilizing farmer incomes. Applying this model to banana pseudostems would ensure consistent collection and supply while benefiting smallholder farmers. Direct partnerships with cooperatives in major banana-growing regions not only create ethical sourcing frameworks but also provide farmers with recurring revenue from agricultural residue. Globally, abundant plantations in Asia-Pacific and Africa offer expansion opportunities to establish processing hubs closer to production centers. This geographic diversification strengthens supply security and positions banana paper producers to meet growing global demand sustainably. As markets push for eco-friendly packaging and technical-grade alternatives, securing robust supply chains will be central to unlocking the full commercial potential of banana paper.

Competitive Landscape: Fragmented Innovators and Strategic Enablers Drive Growth

The banana paper industry’s competitive landscape is fragmented, defined by social enterprises, material innovators, and major agricultural producers aligning waste management with sustainability goals. Companies differentiate through patented processes, artisanal craftsmanship, or integration with global packaging supply chains.

Papyrus Australia Ltd. scales patented technology for molded packaging

Papyrus Australia leads in chemical-free conversion of banana stems into refined fiber and molded products. In August 2025, it completed successful trials producing commercial quantities of biodegradable molded food packaging, showcasing scalability. Its patented process reduces waste decomposition emissions while providing a cost-effective alternative to wood pulp and plastics. The company’s global rollout model is based on partnerships with banana-growing regions, reinforcing its role as a sustainability enabler.

The Banana Paper Company dominates artisanal and premium stationery niches

The Banana Paper Company focuses on handmade and machine-made specialty papers, including luxury stationery, gift wraps, and fine art products. Its key strength lies in unique texture, artisanal craftsmanship, and a strong sustainability narrative. By sourcing fiber from smallholder farmers under fair-trade models, it embeds ethical production and community impact into its value chain. Its offerings extend from B2B full sheets to B2C finished journals and greeting cards, catering to multiple end-use markets.

Banana Leaf Technology pioneers carbon-negative bio-augmentation

Banana Leaf Technology has developed carbon-negative technology to preserve natural leaves for up to a year without chemicals. Its innovation enables the creation of 30+ biodegradable disposable products, replacing paper and plastics. With a focus on cost-effective, scalable solutions, the company positions itself as a material science disruptor, bringing next-gen sustainable disposables to market with a competitive edge in food packaging and FMCG sectors.

Washi-paper-making factories integrate banana fiber into luxury and traditional crafts

Japanese washi-paper factories, known for centuries-old papermaking expertise, are now incorporating banana fiber into traditional and modern product lines. By partnering with social enterprises like One Planet Paper (Zambia), they combine heritage craftsmanship with sustainable sourcing. Their products, ranging from business cards to high-value packaging and art paper, are prized for strength, superior texture, and environmental credibility, appealing to luxury and design-conscious markets.

Chiquita Brands International emerges as a pivotal raw material supplier

While not a producer of banana paper, Chiquita Brands International plays a strategic enabler role. Through its “Behind the Blue Sticker” platform (February 2025), it committed to circular economy practices, creating scope for waste-to-value partnerships. Its extensive global farming operations generate vast volumes of banana stems, positioning it as a critical supplier of raw material for scaling banana paper production. By aligning sustainability goals with industrial applications, Chiquita could unlock steady raw material flows for paper manufacturers worldwide.

Banana Paper Market Share Insights

Market Share by Product Type in the Banana Paper Industry

Machine-made banana paper holds the largest share at 72% of the global market in 2025, highlighting its scalability and ability to compete with conventional wood-pulp and recycled paper products. Its success lies in the ability to deliver consistent quality in terms of thickness, sizing, and finish, which makes it viable for commercial packaging, printing, and box manufacturing at scale. With rising corporate sustainability mandates, large converters are turning to machine-made banana paper as a cost-effective, eco-friendly fiber alternative that aligns with circular economy goals. Its adoption is further supported by global regulations limiting deforestation and incentivizing the use of agricultural waste in industrial supply chains. Handmade banana paper, commanding 28% of the market, plays a crucial role in premium niches. Its artisanal appeal, unique texture, and sustainable story make it highly sought after for luxury stationery, gift packaging, and art supplies. Unlike the commoditized machine-made segment, handmade banana paper thrives on the value it brings to brands and consumers seeking authenticity, craftsmanship, and eco-conscious products. Together, these two segments reflect the market’s dual growth drivers: efficiency and scale on one side, and artisanal, high-value positioning on the other.

Market Share by End-Use Industry in the Banana Paper Industry

Paper and pulp applications dominate the banana paper market with a 55% share in 2025, as banana fiber serves as a sustainable substitute for traditional wood-based pulp. The segment includes office paper, notebooks, corrugated packaging, and carton manufacturing, where performance parity with recycled paper ensures cost competitiveness. Growing demand for sustainable and traceable fibers in mainstream paper applications further strengthens this leadership. Consumer goods, with 22% of the share, represent the value-added growth segment. Banana paper’s tactile quality and eco-friendly narrative make it ideal for gift wrap, premium greeting cards, artisanal journals, and craft products targeted toward eco-conscious consumers. This segment demonstrates how banana paper adds not only functional but also emotional value to end products. Fashion and apparel is an emerging frontier, where banana fibers are being processed into yarns (often called “banana silk”) or used in hang tags, eco-labels, and luxury apparel packaging. This aligns with the apparel sector’s increasing shift toward natural fibers and sustainability commitments. Food and beverage packaging represents a niche but premium opportunity, primarily for luxury dry food packaging and high-end brand boxes, where ethical sourcing and natural aesthetics are strong differentiators, though its adoption is limited by barrier property constraints. Other applications, including industrial filters, specialty mats, and experimental composites, reflect the future diversification potential of banana fibers, showing the material’s adaptability beyond traditional paper-making and consumer goods.

India’s Abundant Banana Waste Turns into a Global Banana Paper Advantage

India, as the world’s largest banana producer, generates vast quantities of pseudo-stems, positioning it as one of the most resource-rich hubs for banana paper production. This agricultural surplus provides manufacturers with a steady and low-cost supply of raw materials, fueling large-scale commercialization. The Indian government is playing a pivotal role in boosting this industry through its strong support for agro-waste utilization. The Technology Development Board (TDB) under the Ministry of Science & Technology has funded projects such as Om Banana Craft Private Limited, which is developing modernized fiber extraction equipment to increase productivity.

Sustainability is another cornerstone of India’s banana paper market. With national campaigns against single-use plastics and a growing preference for biodegradable alternatives, banana fiber is being used in eco-friendly products like sanitary pads and packaging solutions. Technological advancements supported by the Department of Science and Technology (DST) are making extraction processes more mechanized, scalable, and cost-efficient. This combination of raw material abundance, government backing, and eco-conscious consumer demand places India at the forefront of the global banana paper industry.

Philippines Harnesses Banana Plantations for Banana Fiber and Paper Innovation

The Philippines, a major global producer of bananas, is leveraging its agricultural by-products to fuel banana paper production. Large volumes of pseudo-stems from plantations present enormous untapped potential for sustainable manufacturing. The Philippine Textile Research Institute has been at the forefront of exploring these resources, highlighting the capability of plantations to generate hundreds of thousands of tons of fiber suitable for diverse applications, including paper and textiles.

The government, particularly through the Department of Science and Technology (DOST), is emphasizing the strategic importance of banana waste utilization in driving rural economic development. By promoting banana fiber-based industries, the Philippines is creating pathways for job creation, income diversification, and value-added agricultural exports. This positions the country not only as a major raw material supplier but also as a developing hub for eco-friendly banana paper solutions in Asia.

Japan’s Historical Expertise Fuels High-Value Banana Paper Applications

Japan stands out in the banana paper market with a legacy of banana fiber use dating back to the 13th century, giving the country a deep reservoir of expertise in processing techniques. This historical foundation is now being combined with cutting-edge technology to create high-value applications. Japanese industries have integrated banana fiber into specialized and premium products, including currency notes and luxury-grade paper, where exceptional strength and texture are essential.

The focus in Japan is on advanced processing, with companies investing heavily in patented methods and chemical preparation technologies to maximize fiber quality and yield. This technical innovation ensures consistency in high-performance applications and enables the country to position banana paper not as a low-cost alternative but as a premium material for niche markets. As a result, Japan continues to define the standards of quality and innovation in banana paper globally.

Costa Rica Drives Banana Paper Growth Through Sustainable Banana Waste Management

Costa Rica has built a global reputation for environmentally responsible banana production, with its banana sector overseen by CORBANA (Corporación Bananera Nacional). This strong regulatory environment has extended into waste management policies, where banana plantations are actively engaged in recycling and reusing by-products. One major sustainability initiative includes the reuse of banana pseudo-stems for banana paper manufacturing, aligning perfectly with the country’s eco-friendly agricultural practices.

By integrating solid waste management with industrial innovation, Costa Rica is transforming what was once agricultural waste into value-added products. The emphasis on circular economy principles and responsible production enhances Costa Rica’s position as a leader in sustainable banana paper development. This not only meets domestic sustainability goals but also strengthens the country’s appeal in eco-conscious export markets.

United States Embraces Banana Paper for Eco-Friendly and Premium Products

The United States is emerging as a strong consumer market for banana paper, driven by surging demand for eco-friendly, tree-free, and sustainable alternatives. Growing awareness around climate change and waste reduction is fueling adoption across industries such as luxury stationery, premium packaging, and eco-conscious branding. U.S. companies are using banana paper to differentiate their products, showcasing its upcycled nature as a marketing advantage to environmentally aware consumers.

Innovation and brand positioning are central to the U.S. banana paper market. By emphasizing the unique sustainability credentials of banana paper, companies are creating niche categories in high-value consumer segments. This trend is supported by a growing willingness among American buyers to pay more for sustainable, biodegradable products, making the U.S. an attractive destination for global banana paper exporters.

Germany Advances Banana Paper Through EU Circular Economy Initiatives

Germany’s banana paper market is strongly aligned with European Union sustainability mandates and research programs. The EU-funded BADANA project exemplifies this, focusing on developing advanced extraction methods for banana fibers to be applied in polymer composites and packaging solutions. Such initiatives highlight Germany’s role in pioneering industrial uses of banana waste beyond traditional paper, positioning it as a center of technological and material innovation.

The German market also benefits from a strong consumer and industrial preference for sustainable raw materials. With eco-conscious manufacturing sectors and strict environmental regulations, banana paper has gained traction as both a packaging alternative and a sustainable input for composite materials. This strong alignment with EU circular economy policies, combined with ongoing research investment, makes Germany a critical market for advancing banana paper technology and applications across Europe.

Banana Paper Market Report Scope

Banana Paper Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$308.1 Million

|

|

Market Size (2034)

|

$494.6 Million

|

|

Market Growth Rate

|

5.4%

|

|

Segments

|

By Product Type (Handmade Banana Paper, Machine-Made Banana Paper), By Application (Packaging, Stationery, Handicrafts, Textiles, Art & Printing, Other Applications), By End-Use Industry (Paper & Pulp, Food & Beverage, Consumer Goods, Fashion & Apparel, Others)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Bluecat Paper, Ecopaper, Inc., Papyrus Australia Ltd., Green Banana Paper, U.S. Alliance Paper, Inc., BG Handmade Speciality Papers Pvt. Ltd., Om Banana Craft Private Limited, Banana Fiber International, Shri Sai International, T.T. Group of Companies, Papyrus Paper Industries, Banahaw Paper, Ecofiber Pvt. Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Banana Paper Market Segmentation

By Product Type

- Handmade Banana Paper

- Machine-Made Banana Paper

By Application

- Packaging

- Stationery

- Handicrafts

- Textiles

- Art & Printing

- Other Applications

By End-Use Industry

- Paper & Pulp

- Food & Beverage

- Consumer Goods

- Fashion & Apparel

- Others

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Banana Paper Market

- Bluecat Paper

- Ecopaper, Inc.

- Papyrus Australia Ltd.

- Green Banana Paper

- U.S. Alliance Paper, Inc.

- BG Handmade Speciality Papers Pvt. Ltd.

- Om Banana Craft Private Limited

- Banana Fiber International

- Shri Sai International

- T.T. Group of Companies

- Papyrus Paper Industries

- Banahaw Paper

- Ecofiber Pvt. Ltd.

* List Not Exhaustive

Research Coverage

This report investigates the global banana paper market, mapping how agricultural-waste valorization, circularity economics, and premium-brand demand are creating commercial-scale pathways from field residue to finished materials; it synthesizes technology breakthroughs in fiber extraction and molded applications, analysis reviews of pilot-to-commercial scale transitions, and highlights commercial partnerships and policy incentives that de-risk supply chains and broaden end-use adoption this report is an essential resource for procurement teams, sustainability leads, packaging developers, and investors who need pragmatic roadmaps for sourcing, specification, and scale-up. USDAnalytics combines field-level sourcing analysis, techno-economic modelling, and buyer-focused use-case assessments to quantify cost-to-protect, quality parity versus wood pulp, and social-impact metrics delivering prioritized commercial actions, risk mitigations, and go-to-market options to accelerate banana-fiber integration across packaging, stationery, and industrial applications.

Scope Highlights

- Segmentation: By Product Type (Handmade Banana Paper, Machine-Made Banana Paper); By Application (Packaging, Stationery, Handicrafts, Textiles, Art & Printing, Other Applications); By End-Use Industry (Paper & Pulp, Food & Beverage, Consumer Goods, Fashion & Apparel, Others).

- Geographic Scope: “Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.”

- Timeframe: Historic data from 2021–2024 and forecast horizon 2025–2034.

- Companies: Includes analysis and profiles of 15+ key market participants, converters, and technology enablers.

Methodology

Our methodology blends primary field and industry engagement with rigorous desk research: structured interviews with farmers, FPOs/cooperatives, paper mill process engineers, converters and brand procurement leads provided on-the-ground sourcing and operational insight, while secondary sources (patents, academic papers, pilot reports, company disclosures) informed technology-performance baselines. Market sizing used a hybrid bottom-up/top-down model that reconciles available pseudostem volumes, fiber-yield assumptions, pilot plant throughput, and demand by application; techno-economic sensitivity scenarios evaluated chemical vs. mechanical pulping routes, molded versus sheet production, and logistics-cost breakpoints. Quality and sustainability claims were stress-tested with LCA comparators and biodegradability/food-contact requirement checks to produce investment-grade recommendations and prioritized commercialization pathways.

Deliverables:

• Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

• Country-Specific Forecasts & Analysis.

• Segment-Wise Revenue Forecasts (2025–2034).

• Competitive Analysis, Benchmarking, and SWOT Profiles.

• Recent Developments & Innovation Tracker.

• Executive Summary & Analyst Commentary.

• Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.