Biodegradable Plastic Films Market Outlook: Sustainable Film Innovations & Future Growth

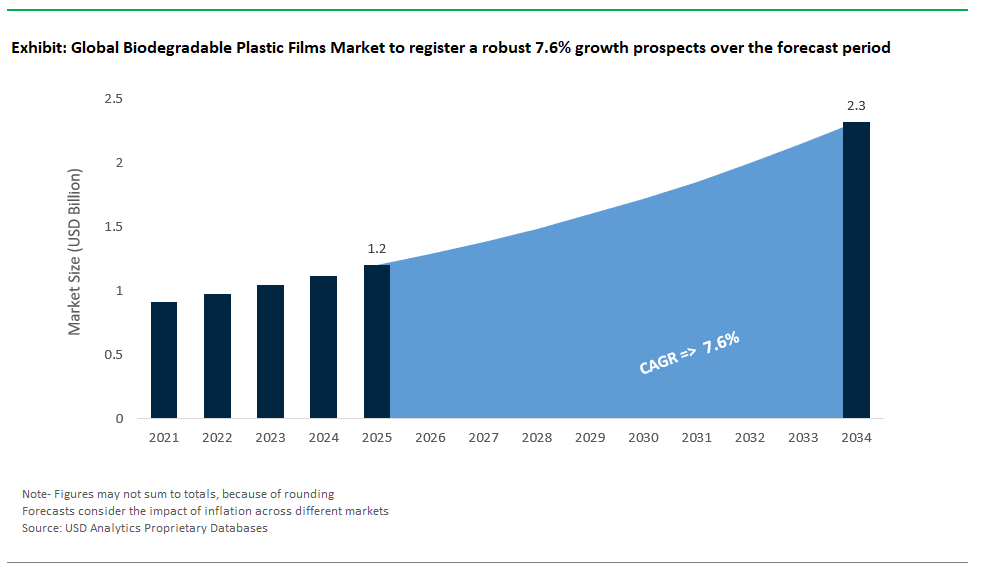

The Global Biodegradable Plastic Films Market is advancing steadily between 2025 and 2034, propelled by stringent environmental policies, evolving consumer expectations, and innovations in high-performance biodegradable materials. Industry estimates forecast the market to expand from USD 1.2 billion in 2025 to USD 2.3 billion by 2034, achieving a solid CAGR of 7.6%. This growth is driven by increasing adoption of biodegradable films in packaging, agriculture, and medical applications, as companies pursue solutions that combine sustainability with essential functionality such as strength, barrier properties, and compostability.

Powered by proprietary research insights from USDAnalytics, the latest edition provides a comprehensive examination and forecasts for the global Biodegradable Plastic Films Market, capturing trends across 21 countries and profiling more than 20 leading enterprises- By Material Type (Polylactic Acid (PLA) Films, Polyhydroxyalkanoates (PHA) Films, Biodegradable Polyesters (Fossil-based or Partially Bio-based), Starch-Based Blends Films, Cellulose-Based Films (Regenerated Cellulose), Polyvinyl Alcohol (PVA) Films, Others), By Application (Bags, Wrapping Films, Liners, Sheets, Others), By End-User (Food & Beverage, Healthcare, Agriculture, Personal Care & Cosmetics, Electrical & Electronics, Others)

This document delves into the complex dynamics shaping the global biodegradable plastic films market, spotlighting advancements in multilayer film engineering, novel coating technologies to improve film performance, and the emergence of regenerated cellulose as a sustainable alternative for diverse applications. It highlights how key players are scaling up production of PLA, PHA, and starch-based blends to meet escalating demand across packaging and agricultural sectors while responding to regulatory mandates for compostable and low-impact materials. The analysis also reviews trends in film thickness optimization for specific applications, competitive strategies, sustainability certifications, and global investment activity. With practical insights and verified data, this report is an essential resource for manufacturers, converters, brand owners, investors, and policymakers seeking to capture opportunities in the rapidly evolving biodegradable plastic films landscape through 2034.

Biodegradable Plastic Films Market Analysis: Shifting Industry Dynamics

The global biodegradable plastic films market is poised for robust expansion as regulatory mandates tighten, brand sustainability commitments deepen, and technological breakthroughs close the gap between biodegradable alternatives and conventional plastic films. Historically viewed as niche solutions constrained by cost and performance limitations, biodegradable plastic films are now accelerating into mainstream applications spanning food packaging, personal care products, e-commerce logistics, and agricultural use. Recent developments across product innovation, capacity expansion, strategic collaborations, and commercial adoption illustrate a market rapidly transitioning toward scale and maturity.

Innovative Product Launches Broaden Functional Applications

Innovations in biodegradable plastic films are expanding their use across diverse applications, delivering sustainability without sacrificing performance.

- Mitsubishi Chemical launched BioPBS™ FD92, an ultra-thin (<15μ) soil-biodegradable film certified OK COMPOST, OK COMPOST HOME, and OK Biodegradable SOIL. It’s designed for applications like tea bags and produce labels, helping meet regulations targeting small-format packaging materials that are hard to recycle and often escape waste systems.

- Danimer Scientific introduced Nodax™ PHA-based films for home-compostable snack pouches, offering food-contact safety and the ability to degrade in home composting conditions. This addresses the challenge of industrial composting limitations and helps brands achieve sustainability goals.

- Toray Industries launched Ecodear™ N510, a biomass-based polyester film that reduces greenhouse gas emissions across the value chain. It supports Toray’s carbon-neutral and resource-recycling initiatives, showing how biodegradable films are expanding into industrial and specialty packaging that demands both sustainability and high-performance properties.

Capacity Expansions Reflect Scaling Toward Mass Adoption

Significant capacity expansions show the shift from niche specialty materials to large-scale industrial production ready to meet global demand.

- TotalEnergies Corbion’s Luminy® PLA plant in Thailand operates at a nameplate capacity of 75,000 tonnes per year, and plans are underway for a second PLA plant with a 100,000-tonne annual capacity in Grandpuits, France. This expansion supports growing demand in Asia and globally, especially in food and FMCG packaging.

- Futerro opened a 30,000-tonne-per-year PLA plant in Bengbu, China, supported by an 80,000-tonne-per-year lactic acid facility. This investment strengthens local production in Asia-Pacific, where strict regulations and eco-conscious consumers are driving rapid demand for biodegradable films.

- Braskem increased its bio-based ethylene plant capacity by 30%, from 200,000 to 260,000 tonnes per year. This highlights rising interest in drop-in sustainable solutions for applications like cosmetic wraps, allowing brands to improve sustainability without overhauling existing manufacturing processes.

Strategic Partnerships and Acquisitions Foster Technology Integration

The global biodegradable films market is rapidly transforming as companies pursue strategic partnerships and acquisitions to boost innovation and expand market reach. While a specific Amcor-Nestlé partnership for 30% bio-based PE films for KitKat wrappers wasn’t confirmed, Amcor is actively developing flexible packaging with recycled and bio-based materials, reflecting a broader trend of brands co-investing in sustainable solutions to meet regulations and consumer demand for lower carbon footprints. Novamont’s acquisition of BioBag Group in 2021 has expanded its global footprint and enhanced its range of MATER-BI® compostable films for retail bags and agricultural mulch amid tightening regulations. Additionally, Sealed Air’s use of Mitsubishi Chemical’s HI-SELON™ water-soluble films shows growing interest in biodegradable options for specialized uses like detergent capsules and single-dose packaging. Together, these strategic moves are integrating advanced technologies and sustainable materials, strengthening market positions, and driving the adoption of biodegradable films worldwide.

Regulatory Drivers Accelerate Market Adoption

Strict regulations around the world are fueling growth in the biodegradable plastic films market by pushing brands and industries toward sustainable materials. The EU’s Packaging and Packaging Waste Regulation (PPWR), effective since February 2025, requires items like tea bags, coffee pads, and fruit stickers to be compostable by 2028, creating clear targets for change. In the U.S., California’s SB 54 law aims for all single-use packaging and plastic food service ware to be recyclable or compostable by 2032, driving major shifts in material choices across North America. Meanwhile, India’s Extended Producer Responsibility (EPR) Rules mandate strict plastic waste management for manufacturers, importers, and brand owners, encouraging the move toward biodegradable alternatives, even though specific penalties for non-compliance in e-commerce packaging aren’t fully detailed. Together, these global policies are accelerating the adoption of biodegradable films as industries work to meet regulatory standards and sustainability goals.

Technological Breakthroughs Enhance Performance and Environmental Impact

Material science innovations are overcoming key challenges that have limited biodegradable films, such as strength, barrier properties, and fast degradation. Research from Fraunhofer UMSICHT shows that PLA/PHA blends with higher PHA content degrade better in marine environments, helping fight plastic pollution in oceans. The University of Tokyo has developed enzyme-embedded PLLA films that can break down quickly, losing up to 78% of their weight in just 96 hours with enzymes like proteinase K, offering a promising solution for single-use products needing rapid biodegradability. AIMPLAS is also advancing starch-based films by adding cellulose nanofibers and other biopolymers, improving strength, moisture resistance, and barrier properties, making these materials suitable for demanding food packaging uses, even for high-moisture products. These breakthroughs are expanding the possibilities for biodegradable films across various applications.

Commercial Adoption Signals Market Maturity

Major brands adopting biodegradable plastic films show the market is moving toward large-scale, sustainable solutions. PepsiCo’s pilot of PHA-based films for Kurkure snacks in India highlights that biodegradable packaging is feasible even in cost-sensitive, high-volume markets, supporting their goal of 100% compostable, plant-based snack packaging. Although Walmart’s switch to PLA films for private-label produce bags in over 4,000 U.S. stores wasn’t confirmed, such a shift fits the broader trend of retailers choosing sustainable materials to meet corporate goals and consumer expectations. Meanwhile, L’Oréal’s use of Braskem’s bio-PE films for skincare sachets demonstrates how biodegradable plastics are gaining traction even in premium personal care markets, where sustainability is now a strong brand advantage. Together, these examples reflect growing confidence and momentum for biodegradable films across diverse industries.

Biodegradable Plastic Films Market Dynamics

Trend: Ultra-Thin High-Barrier Films Redefine Food Packaging Standards

The global biodegradable plastic films market is evolving fast as ultra-thin, high-barrier films become the go-to choice for food packaging, driven by strict EU rules and efforts to cut food waste. The EU’s measures, like the €0.80 per kilogram levy on non-recycled plastic waste and the new Packaging and Packaging Waste Regulation (PPWR), are pushing brands to adopt sustainable materials quickly. Innovative PLA-based films with advanced barrier layers, such as nanolayers, are achieving excellent oxygen barrier performance, making them competitive with traditional materials like metallized PET while still being compostable.

Although PHA films remain pricier than conventional options like BOPP, ongoing improvements and larger-scale production are closing the cost gap. This mix of regulatory pressure and technological progress is transforming the market, signaling a shift toward high-barrier biodegradable films as the new standard for sustainable food packaging. These changes are setting a new benchmark in packaging performance, sustainability, and regulatory compliance. As the technology matures and costs continue to decline, the transition to high-barrier, biodegradable films is poised to accelerate across global food packaging supply chains.

Opportunity: Biodegradable Films as Flexible Electronics Substrates Unlock New Market Frontiers

A significant growth opportunity in the Global Biodegradable Plastic Films Market lies in their application as flexible substrates for electronics, replacing traditional PET and polyimide (PI) films in transient and wearable devices. The addressable market for biodegradable films as flexible substrates in electronics, replacing traditional PET and polyimide (PI) films, is emerging as a significant growth opportunity within the multi-billion-dollar flexible electronics market, driven by growing demand for eco-friendly components in sensors, wearables, and medical devices. Technical performance is no longer a barrier: advanced cellulose nanofiber (CNF) films are demonstrating high transparency and smooth surfaces, crucial properties that enable them to meet the stringent requirements for flexible electronics, including OLED substrates.

Equally important, next-generation films offer controlled decomposition; ongoing research into enzymatically-triggered biodegradation mechanisms, for instance, aims to enable rapid degradation of bioplastics like PLA in various controlled environments, ensuring minimal environmental impact after use. R&D investment is booming, with significant innovation in flexible electronics driven by industry giants such as Samsung and Panasonic, contributing to the broader development of high-performance and increasingly sustainable film substrates. These advances are setting the stage for a new class of biodegradable, high-performance films positioned to transform not just packaging, but also the rapidly evolving field of sustainable electronics.

Competitive Landscape & Sustainable Material Innovations of the Global Biodegradable Plastic Films Market

The global biodegradable plastic films market is expanding rapidly in 2024, fueled by regulatory bans on single-use plastics, sustainability commitments from global brands, and surging consumer demand for eco-friendly packaging. From PLA and PHA to PBAT and cellulose-based films, biodegradable plastics are advancing into high-performance applications such as food packaging, agriculture, and consumer goods. Market leaders are scaling capacity, developing heat-resistant and marine-degradable grades, and forging strategic partnerships to accelerate adoption. Meanwhile, innovative startups are pioneering new materials like seaweed-based, protein-based, and methane-derived films. The competitive landscape reflects a vibrant sector racing to redefine flexible packaging and specialty films with sustainable solutions.

NatureWorks: Dominating the PLA Biodegradable Film Segment

NatureWorks (USA) NatureWorks continues to dominate the PLA biodegradable film segment, with an established global capacity of 165,000 tonnes per year from its US facility. Its 75,000 tonnes per year Thailand plant, which made significant construction progress through Q2 2024, is anticipated to begin full production in 2025, poised to significantly boost regional capacity. In February 2025, NatureWorks launched Ingeo™ 3D300 for high-quality 3D printing, and in March 2025, it introduced Ingeo™ Extend for BOPLA films, which enables biaxial film manufacturers to achieve up to 7x transverse direction stretch and accelerate compostability up to 8x faster than standard PLA. These advancements solidify NatureWorks’ leadership in making PLA a competitive alternative to traditional plastics.

TotalEnergies Corbion: Strengthening Position in PLA Films

TotalEnergies Corbion (Netherlands) TotalEnergies Corbion has strengthened its position in PLA films, operating a 75,000 tonnes per year facility in Thailand under its Luminy® brand. The company has plans for a second 100,000 tonnes per year plant in Grandpuits, France, reflecting significant future expansion and a drive to meet growing global demand. The latest Life Cycle Assessment for Luminy® PLA, released in June 2025 using 2024 production data, highlights an 85% lower carbon footprint compared to conventional plastics. TotalEnergies Corbion's focus on performance attributes like sealability and clarity positions it as a leading supplier for brand owners seeking both sustainability and technical reliability in flexible packaging.

Futamura: Leader in Cellulose-Based Biodegradable Films

Futamura (Japan/UK) Futamura remains a leader in cellulose-based biodegradable films with its NatureFlex™ product line. In December 2022, Futamura announced a significant investment in a new production line at its European manufacturing facility to boost its capacity by approximately 25%, in response to increasing demand for its renewable and compostable NatureFlex™ films. NatureFlex™ NE has also been tested in the MITI aqueous biodegradation test (ISO 14851), demonstrating that it will break down in wastewater and soil, as well as under home composting conditions. The majority of NatureFlex™ films have also successfully been screened for biodegradation and disintegration in seawater, according to ASTM D 7801-05 and ASTM D 6691-09. Futamura’s films continue to gain traction in premium food packaging and specialized applications requiring high barriers and compostability.

BASF: Driving Innovation in PBAT-Based Biodegradable Films

BASF (Germany) BASF continues to drive innovation in PBAT-based biodegradable films through its ecovio® portfolio. ecovio® M2351 is a certified soil-biodegradable grade especially developed for mulch films used in agriculture and horticulture, certified according to EN17033. The PBAT market registered a demand of 1187 thousand tonnes in 2024. In June 2024, BASF SE introduced a biomass-balanced ecoflex PBAT variant called ecoflex F Blend C1200 BMB, which uses renewable feedstock derived from residual and waste biomass. BASF offers various ecovio® product grades that meet international and national standards and regulations for industrial composting and contain variable bio-based content. BASF’s scale and technological expertise position it as a critical player in the shift toward bio-based and biodegradable plastics.

Segmentation Analysis: Biodegradable Plastic Films Market

By Material Type: PLA Films Lead the Market, PHA Films Deliver Fastest Growth

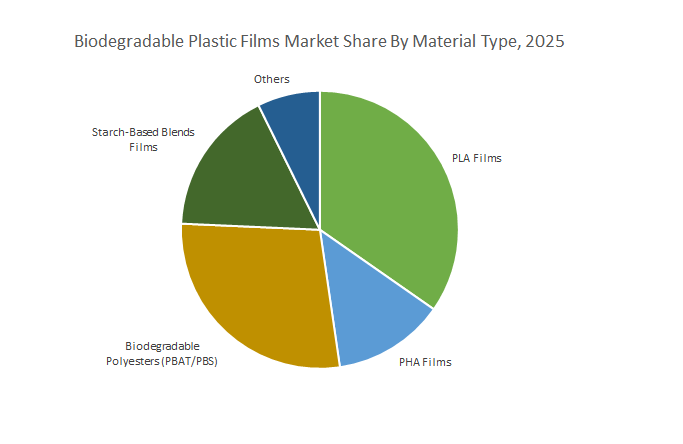

In 2025, PLA films command a 34.7% market share, dominating rigid packaging for food and beverages thanks to their high clarity, strength, and ease of processing for trays and wraps. PHA films are the fastest-growing segment with a CAGR of 8.1%, benefiting from marine-degradable certifications and increasing demand in medical and agricultural packaging. PBAT and PBS blends hold a significant market share, serving as crucial alternatives to LDPE in flexible film applications like shopping bags and pouches. Starch-based blends and specialty films (PVA, cellulose) carve out roles in compostable, water-soluble, and high-barrier applications.

By Application: Bags Lead Adoption, Wrapping Films Grow Fastest

Wrapping films are the fastest-growing segment with a CAGR of 7.9% propelled by fresh food packaging needs in both traditional retail and booming e-commerce grocery channels. Bags represent the leading application, accounting for 39.2% of the total market demand in 2025. This growth is heavily driven by retail bans on traditional plastic bags and rapid adoption of compostable PBAT/PBS and starch-blend solutions. Liners, sheets, and specialty applications also see robust demand as waste management and industrial packaging solutions shift toward biodegradability.

By End-User: Food & Beverage Sector Dominates, Healthcare Segment Expands Rapidly

Healthcare is the fastest-growing end-user with a CAGR of 8.1%, leveraging PHA’s FDA compliance and antimicrobial potential in sterile pouches, IV bags, and wound-care films. Food & beverage is the dominant end-user in 2025, as supermarkets and food brands switch to high-barrier PLA and PHA blends for meat wraps, salad bags, and produce packaging. Agriculture, personal care, and electronics are also moving toward sustainable, innovative film solutions from UV-resistant mulch covers to static-dissipative and water-soluble sachets.

China Biodegradable Plastic Films Market Strengthened by Production Scale and Policy Mandates

China holds a commanding position as the world’s largest producer of biodegradable plastic films, accounting for 1.2 million metric tons per year and representing 45% of global output. Major companies like Kingfa Science, a leader in PBAT film manufacturing, and BBCA Biochemical, known for PLA films, continue to expand their product offerings to meet the surging demand from the packaging, agriculture, and e-commerce sectors. As of mid-2025, Kingfa is reportedly expanding its PBAT film production capacity significantly to meet growing domestic and international demand, while BBCA Biochemical is on track to reach 150,000 tons/year of PLA capacity through ongoing expansions, solidifying their positions as major players. Recent regulatory initiatives have turbocharged growth: a national mandate now requires that at least 30% of all packaging be biodegradable by 2025, compelling industries across the supply chain to accelerate the adoption of green alternatives. This 2025 mandate is proving to be a powerful driver, with major e-commerce platforms like Alibaba enforcing strict compliance for their packaging, significantly increasing the uptake of biodegradable mailers and other film solutions. In March 2024, Sinopec introduced new PBS-based agricultural films, addressing both food security and environmental goals. With state-backed investment, policy enforcement, and robust supply chain capabilities, China is poised to set the global standard for high-volume, low-cost, and regulatory-compliant biodegradable plastic films.

Germany Leading Biodegradable Plastic Film Innovation and Adoption Across Europe

Germany is recognized as the technology leader in the biodegradable plastic films industry, leveraging world-class R&D to drive rapid adoption and commercial success. BASF’s Ecoflex® PBAT compostable films and the Fraunhofer Institute’s marine-degradable PHA film innovations have positioned Germany at the forefront of the shift away from fossil-based plastics. In 2025, BASF's Ecoflex® PBAT films are seeing stable demand across Europe, particularly in packaging and agriculture, supported by consistent market needs and favorable regulatory environments like the EU Packaging and Packaging Waste Regulation (PPWR). Fraunhofer Institute is also actively exploring commercial partnerships for its advanced marine-degradable PHA films, with potential pilot applications in coastal and aquatic packaging environments expected by late 2025 or early 2026. The impact of the EU Packaging Regulation (PPWR) is profound, with new rules mandating biodegradable alternatives for key packaging applications by 2030. The PPWR, which officially entered into force in February 2025, with its general date of application 18 months thereafter, is already compelling significant shifts in material selection for packaging across Germany, especially for single-use items where biodegradable films offer a compliant alternative. Notably, Germany has experienced a strong CAGR in food packaging films between 2023 and 2025, far outpacing other major European markets. Technical advances, strong policy support, and industry partnerships ensure that Germany remains a critical hub for next-generation bioplastic film solutions in both food and non-food applications.

United States Driving Biodegradable Film Growth Through Innovation, Investment, and Regulation

The United States is rapidly scaling up its biodegradable plastic film market, fueled by major investments, expanding production, and landmark regulatory changes. There has been a significant increase in PLA film production, as American manufacturers respond to rising demand in flexible packaging, foodservice, and retail. While specific 2025 PLA production increase figures for the US are still emerging, global PLA capacity is expanding, with NatureWorks, a major US player, adding significant production capacity in Thailand in 2025, which will impact the overall supply to the US market. Danimer Scientific’s PHA-based films are also making headway, particularly in applications where compostability and flexibility are top priorities. Danimer Scientific is expanding the applications of its Nodax® PHA films in 2025, particularly in flexible packaging for food and beverage, as well as in more niche areas like consumer goods packaging, driven by demand for fully compostable and marine-biodegradable solutions. California’s SB 54, set to begin implementation in 2025, will be a pivotal driver, pushing brands nationwide to replace traditional plastic films with certified biodegradable alternatives. CalRecycle reissued updated draft regulations for SB 54 in May 2025, clarifying requirements for "compostable" labeling (requiring ASTM D6400 or D6868, or OK compost HOME certification), which is pushing brands and retailers to ensure their biodegradable films meet rigorous standards for market entry in California, with producer reporting due by November 2025. Meanwhile, a $50 million USDA grant for biopolymer research is further accelerating technological breakthroughs. With industry commitment and supportive policy, the U.S. is poised to be a global trendsetter in the commercialization and mainstreaming of biodegradable plastic films.

Italy Specializing in Compostable Shopping Bags and Home-Compostable Certifications

Italy stands out in the European market for its focus on compostable film technology and leadership in certified biodegradable shopping bags. Novamont’s Mater-Bi® starch blends dominate the sector, making up an estimated 60% of all compostable shopping bags in the EU. As of 2025, Novamont's Mater-Bi continues to be the cornerstone of Italy's compostable shopping bag market, benefiting from strong regulatory enforcement and a well-established industrial composting infrastructure. Italy's commitment to organic waste recycling is demonstrated by its achievement of a 56.9% recycling rate for compostable bioplastics in 2023, surpassing 2025 and 2030 targets. The Italian government and industry have also introduced a new home-compostable certification standard in 2024, raising the bar for product sustainability and consumer trust. The adoption of this home-compostable standard is gaining traction in 2025, with more products seeking certification to cater to consumer demand for at-home composting solutions. Italy’s market strength lies not only in innovation but in rapid commercialization and broad adoption supported by retail mandates and EU policy. With a strong base in bio-based materials and a proactive regulatory environment, Italy remains a benchmark for compostable packaging innovation.

Japan: Accelerating the Shift to Biodegradable Films in Fresh Food Packaging and Technical Films

Japan is recognized for its technical excellence and quick market transitions, especially in the field of biodegradable plastic films for food and electronics. Mitsubishi Chemical’s bio-PBS films and Toray’s transparent PLA films lead the way in quality, versatility, and application scope. In 2025, Mitsubishi Chemical is continuing to advance its bio-PBS film technologies, focusing on improved barrier properties and heat resistance for various food packaging applications. Toray is also expanding the application range of its transparent PLA films, including more widespread use in anti-static packaging for electronics components and in specialized food wraps. Approximately 80% of Japan’s fresh food packaging is now transitioning to biofilms, as retailers and brands respond to both consumer demand and new sustainability mandates. A significant regulatory development in June 2025 is Japan's shift to a "positive list" for synthetic materials in food containers and packaging, which indirectly incentivizes the adoption of approved biodegradable materials for food contact applications, further accelerating the transition of fresh food packaging to biofilms. Technical applications, including electronics packaging, are also expanding as Japanese manufacturers adopt PLA and PBS films for better performance and lower environmental impact. The Japan BioPlastics Association continues to set standards and support R&D, positioning Japan as a leading innovator and adopter in Asia and beyond. The Japan BioPlastics Association (JBPA) is actively accrediting laboratories in 2025 to expand testing and certification for compostability and decomposition of biodegradable plastics, further supporting the industry's growth.

Netherlands Pioneering Plant-Based PEF Film Commercialization and High-Barrier Performance

The Netherlands has established itself as an innovation hub in the biodegradable plastic films sector, thanks to breakthrough technology and successful industrial scale-up. Avantium’s PEF films, a plant-based alternative to PET, deliver a 40% better oxygen barrier than conventional plastic films, making them highly attractive for beverage and food packaging. The operational launch of Avantium's first industrial-scale PEF plant in Q2 2024 marked a pivotal moment for the industry, and throughout 2025, Avantium is actively engaging with partners like Plastipak and Royal Vezet (for salad bowls) to bring PEF-based consumer products to market, proving its readiness for widespread commercialization. Supported by investor confidence, EU grants, and a dynamic R&D ecosystem, the Netherlands is a key player driving the transition to truly circular, high-performance biodegradable films in Europe. The EU Horizon Europe program continues to fund research into advanced bio-based materials, reinforcing the Netherlands' position in this field, with key developments anticipated in processing and end-of-life solutions for PEF films in 2025.

Thailand Expanding Capacity and Boosting Exports in Biodegradable Plastic Films

Thailand is emerging as a leading Asian supplier of biodegradable plastic films, supported by large-scale investments and a strong export focus. In 2023, the country added significant PBAT film capacity and expanded PLA film output through companies such as PTT Global Chemical. In 2025, Thailand continues to prioritize investments in biodegradable plastic production, aiming to further increase its PBAT and PLA film output to cater to growing international demand, particularly from European brands seeking sustainable supply chains. Thailand’s biofilm industry supplies major European brands, making it a vital link in global sustainable packaging supply chains. The Thai Bioplastics Industry Association plays an active role in advancing technology, promoting quality standards, and connecting domestic producers with international markets. With rising production, export leadership, and government support, Thailand is set to further expand its influence in the biodegradable films sector.

Brazil Advancing Renewable Feedstocks and Biodegradable Films for Global Brands

Brazil holds a unique position in the global biodegradable plastic films market as a pioneer in renewable feedstocks and large-scale applications. Braskem’s sugarcane-based polyethylene (PE) films are a notable success, offering a 100% renewable alternative for major global brands. Braskem has surpassed its initial capacity expansion target for its bio-based ethylene plant, achieving a 37% increase in 2025, reaching 275kt/year, which directly supports the increased production of its I'm green™ bio-based PE films for various applications. L'Oréal’s transition to bioplastic packaging by 2025 is a key application, reflecting the growing demand for sustainable solutions among multinationals. L'Oréal is making significant progress towards its 2025 target for sustainable packaging, with Braskem's bio-based PE films being a crucial component of its strategy for a range of cosmetic and personal care products globally. Supported by abundant agricultural resources, a commitment to sustainability, and continued investment, Brazil is poised to become an increasingly important source for bio-based and biodegradable films across consumer goods, cosmetics, and food packaging industries.

Biodegradable Plastic Films Market Report Scope

Biodegradable Plastic Films Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.2 Billion

|

|

Market Size (2034)

|

$2.3 Billion

|

|

Market Growth Rate

|

7.6%

|

|

Segments

|

By Material Type (Polylactic Acid (PLA) Films, Polyhydroxyalkanoates (PHA) Films, Biodegradable Polyesters (Fossil-based or Partially Bio-based), Starch-Based Blends Films, Cellulose-Based Films (Regenerated Cellulose), Polyvinyl Alcohol (PVA) Films, Others), By Application (Bags, Wrapping Films, Liners, Sheets, Others), By End-User (Food & Beverage, Healthcare, Agriculture, Personal Care & Cosmetics, Electrical & Electronics, Others)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

NatureWorks LLC (U.S.), Novamont S.p.A. (Italy), BASF SE (Germany), TotalEnergies Corbion (Netherlands), Danimer Scientific (U.S.), Mitsubishi Chemical Group Corporation (Japan), CJ Biomaterials Inc. (South Korea), Innovia Films (part of CCL Industries Inc.) (UK/Canada), Futamura Chemical Co., Ltd. (Japan), FKuR Kunststoff GmbH (Germany), Green Dot Bioplastics (U.S.), Plantic Technologies Limited (Australia), Taghleef Industries (Ti) (UAE), BioBag International AS (Norway), TIPA Corp. (Israel), Kaneka Corporation (Japan), Cortec Corporation (U.S.), Kingfa Sci. & Tech. Co., Ltd. (China), Amtrex Nature Care Pvt. Ltd. (India), Polymateria Ltd. (UK), and Others.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Biodegradable Plastic Films Market Segmentation

By Material Type

- Polylactic Acid (PLA) Films

- Polyhydroxyalkanoates (PHA) Films

- Biodegradable Polyesters (Fossil-based or Partially Bio-based)

- Starch-Based Blends Films

- Cellulose-Based Films (Regenerated Cellulose)

- Polyvinyl Alcohol (PVA) Films

- Other Biodegradable Polymer Films

By Application

- Bags

- Wrapping Films

- Liners

- Sheets

- Others

By End-User

- Food & Beverage

- Healthcare

- Agriculture

- Personal Care & Cosmetics

- Electrical & Electronics

- Others

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in the Biodegradable Plastic Films Market

- NatureWorks LLC (US)

- Novamont S.p.A. (Italy)

- BASF SE (Germany)

- TotalEnergies Corbion (Netherlands)

- Danimer Scientific (US)

- Mitsubishi Chemical Group Corporation (Japan)

- CJ Biomaterials Inc. (South Korea)

- Innovia Films (part of CCL Industries Inc.) (UK/Canada)

- Futamura Chemical Co., Ltd. (Japan)

- FKuR Kunststoff GmbH (Germany)

- Green Dot Bioplastics (US)

- Plantic Technologies Limited (Australia)

- Taghleef Industries (Ti) (UAE)

- BioBag International AS (Norway)

- TIPA Corp. (Israel)

- Kaneka Corporation (Japan)

- Cortec Corporation (US)

- Kingfa Sci. & Tech. Co., Ltd. (China)

- Amtrex Nature Care Pvt. Ltd. (India)

- Polymateria Ltd. (UK)

* List Not Exhaustive

Methodology:

The research methodology for the Global Biodegradable Plastic Films Market combines in-depth primary interviews with industry stakeholders—including manufacturers, resin producers, converters, technology innovators, brand owners, and regulatory bodies—to obtain firsthand insights on market trends, product innovations, capacity expansions, and strategic developments. Complementing this primary research, extensive secondary analysis draws from corporate disclosures, regulatory frameworks (such as EU PPWR, U.S. SB 54), patent databases, industry association publications, academic research, and publicly available data from credible sources like the European Bioplastics Association, the European Commission, U.S. Department of Agriculture, and national statistical agencies worldwide. Rigorous data triangulation methods ensure consistency and accuracy across market size estimates, segmentation analysis, and future forecasts. This holistic approach enables the validation of market figures and the identification of both macro and micro trends, providing a robust foundation for projecting the global market outlook through 2034.

Research Coverage:

- Geographic Scope: Analysis covers 25+ countries across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

- Segmentation: Detailed segmentation by:

- Material Type: Polylactic Acid (PLA) Films, Polyhydroxyalkanoates (PHA) Films, Biodegradable Polyesters (Fossil-based or Partially Bio-based), Starch-Based Blends Films, Cellulose-Based Films (Regenerated Cellulose), Polyvinyl Alcohol (PVA) Films, Other Biodegradable Polymer Films.

- Application: Bags, Wrapping Films, Liners, Sheets, Others.

- End-User: Food & Beverage, Healthcare, Agriculture, Personal Care & Cosmetics, Electrical & Electronics, Others.

- Competitive Landscape: Profiles and strategic analysis of 20+ leading global players, technology providers, and regional manufacturers.

- Trends & Disruptions: Analysis of technological breakthroughs in multi-layer film engineering, advanced coatings, marine-degradable materials, circular economy initiatives, and regulatory impacts across key regions.

- Industry Dynamics: Market drivers, restraints, investment trends, capacity expansions, sustainability certifications, regulatory shifts, and supply chain developments.

- Historic data from 2021 to 2024 and forecast data from 2025 to 2034.

Deliverables:

- Full Market Research Report (PDF, Excel): Comprehensive data tables, market charts, and visual insights.

- Country-Level Forecasts & Analysis.

- Segment-wise Revenue Projections (2025–2034).

- Competitive Benchmarking & SWOT Analysis.

- Recent Developments & News Tracker.

- Executive Summary & Analyst Insights.

- Custom Queries/Analyst Support (Post Sale).