Bottled Water Packaging Market to Reach USD 77.3 Billion by 2034 at 4.6% CAGR

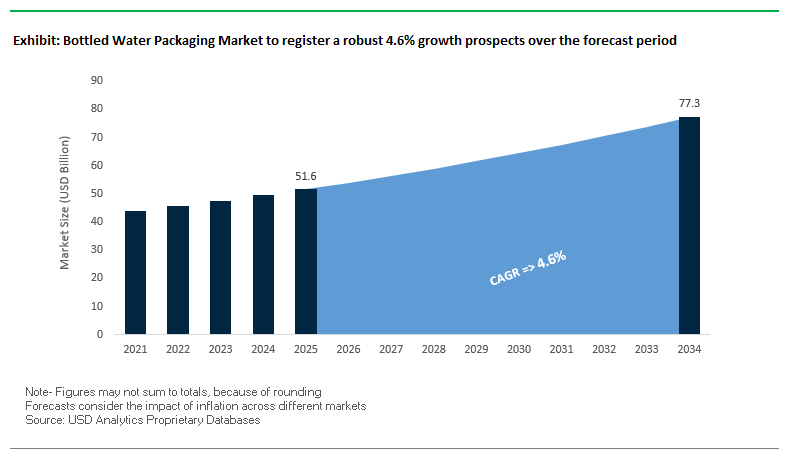

The global bottled water packaging market is projected to expand from USD 51.6 billion in 2025 to USD 77.3 billion by 2034, reflecting a steady CAGR of 4.6%. Growth is being driven by a combination of sustainability mandates, consumer preference for eco-friendly formats, and the continued dominance of PET and recycled PET (rPET) bottles. The sector is undergoing a transformative shift, where packaging is no longer just a protective medium but also a branding tool and sustainability statement.

While PET remains the leading material due to its lightweight and cost efficiency, the rise of rPET, compostable bioplastics, and alternative formats such as aluminum bottles, cartons, and glass is reshaping competitive dynamics. Major beverage brands are committing to higher recycled content, while others diversify portfolios with paper-based or plant-based solutions. This shift also addresses global concerns about microplastic contamination, with certified biodegradable packaging gaining attention as a pollution-free alternative.

Key Insights for Industry Leaders

- Market value: USD 51.6B (2025) → USD 77.3B (2034) at 4.6% CAGR.

- PET & rPET dominance: Lightweight and recyclable, yet facing regulatory pressure.

- Microplastic challenge: Compostable packaging reduces long-term contamination.

- Alternative formats rising: Aluminum, cartons, and glass meeting premium and eco demand.

- Sustainability driver: Brands are investing heavily in circular economy packaging.

Regulatory Mandates and Material Innovations Drive Bottled Water Packaging Market

The bottled water packaging industry is witnessing rapid change driven by mergers, EU policy updates, and new product launches. In August 2025, the newly merged Smurfit WestRock debuted on the New York and London exchanges, enhancing its portfolio of paper-based cartons applicable to bottled water packaging. The same month, Mondi unveiled an e-commerce packaging lineup at eCommerce EXPO UK, signaling the expansion of sustainable packaging beyond retail into direct-to-consumer beverage distribution.

Policy changes are shaping the market as well. The European Union’s Packaging and Packaging Waste Regulation (PPWR) revision in July 2025 mandated stricter recyclability requirements, accelerating the adoption of tethered caps, mono-material bottles, and higher rPET content. Innovation followed, with NatureWorks LLC (April 2025) introducing its Ingeo Extend polymer, improving biodegradability and manufacturing efficiency for bioplastic bottles. Meanwhile, Teknor Apex (March 2025) acquired Danimer Scientific, securing access to Nodax PHA biopolymers used in biodegradable bottles.

Alternative materials also gained traction. Flow Beverage Corp. (August 2024) launched sparkling mineral spring water in 70% recycled aluminum bottles, using 30% less aluminum than standard competitors. At the same time, Tetra Pak (August 2025) announced a collaboration with Danone to develop carton-based bottled water lines, pushing paper-based packaging into the mainstream.

Emerging Trends and Strategic Opportunities in the Bottled Water Packaging Market

Accelerated Adoption of 100% Recycled PET (rPET) Bottles

The bottled water packaging market is experiencing a major shift toward 100% recycled PET (rPET) bottles, driven by sustainability-focused consumers, corporate ESG commitments, and emerging government regulations mandating recycled content. Key drivers include global initiatives such as Coca-Cola’s “World Without Waste”, targeting at least 50% recycled content in packaging by 2030. In 2024, Coca-Cola completed its nationwide rollout of 100% rPET bottles for its sparkling beverages in 20-oz sizes across the U.S., marking a significant milestone in sustainable packaging adoption. Governments are reinforcing this trend; India’s EPR guidelines, effective April 2025, mandate a minimum of 30% recycled plastic content in rigid packaging, incentivizing manufacturers to adopt rPET. Leading brands like PepsiCo and FIJI Water are following suit, eliminating virgin plastic from select beverage lines and reducing carbon emissions by up to 40% per bottle. Adoption of rPET provides measurable environmental benefits, with studies indicating up to 79% reduction in carbon footprint compared to virgin PET, creating a compelling business case for brands and packaging suppliers.

Lightweighting and Material Reduction Through Advanced Bottle Design

In addition to material substitution, lightweighting has become a core trend, focusing on reducing bottle material usage without compromising functionality. Advanced manufacturing and injection molding techniques enable thinner bottle walls that maintain structural integrity while lowering environmental impact and production costs. Companies like Nestlé have reduced over 20% of virgin plastic use in water bottles since 2018 through targeted lightweighting initiatives. The dual benefits include lower material costs and decreased carbon emissions in manufacturing and transport, aligning with corporate sustainability goals. This ongoing innovation presents continuous opportunities for manufacturers and material suppliers to provide lightweight, sustainable packaging solutions in the highly competitive bottled water segment.

Development of Paper-Based Hybrid Packaging Solutions

A prominent opportunity lies in paper-based bottled water packaging, offering fiber-based alternatives that appeal to consumers avoiding even recycled plastic. Collaborative initiatives between brands and material innovators are driving this market segment. For instance, PepsiCo is part of the Pulpex consortium, developing renewable, recyclable, and biodegradable paper bottles. European examples include Paboco, which partnered with Carlsberg to create paper bottles with thin inner barriers for liquid retention. These hybrid solutions demonstrate a transitional approach toward fully sustainable packaging that integrates with existing paper recycling streams, enabling companies to differentiate products and capture a sustainability-focused consumer segment.

Integration of Digital Watermarks for Precision Recycling

Advancements in digital watermarking technology are creating opportunities for improved recycling efficiency and circularity in bottled water packaging. These imperceptible codes, part of the HolyGrail 2.0 initiative, allow high-resolution cameras in recycling facilities to sort plastics by type and food-contact suitability. Brands like PepsiCo are actively involved, enabling higher-quality rPET streams, reducing contamination, and enhancing economic viability for recycled material. Accurate sorting ensures that only food-grade PET is reused for bottled water, strengthening the circular economy. Adoption of digital watermarks has the potential to revolutionize the value chain, increasing the availability of high-quality rPET, lowering waste, and supporting sustainable growth for the bottled water packaging market.

Competitive Landscape: Leading Companies in Bottled Water Packaging Industry

The bottled water packaging market is highly competitive, with global leaders in plastics, paper, aluminum, and equipment solutions driving innovation in sustainability, design, and circularity.

Amcor PLC Expands Circular Economy with PET and Compostable Packaging

Amcor remains at the forefront of PET and rPET bottle innovation, offering lightweight, recyclable, and compostable formats. In August 2025, it launched a home-compostable coffee pod lid, underscoring its commitment to circularity. With operations across all continents, Amcor’s global R&D strength and broad material expertise make it a dominant player in sustainable bottled water packaging.

Plastipak Holdings Advances Food-Grade rPET Recycling

Plastipak is recognized for its Packaging-to-Packaging recycling technology, enabling food-grade rPET production at scale. Its PET and rPET bottles are widely adopted in the bottled water sector. By integrating design, manufacturing, and recycling in one supply chain, Plastipak provides a seamless, sustainable solution, strengthening its competitive edge in both North American and European markets.

Ball Corporation Leverages Infinitely Recyclable Aluminum Bottles

Ball Corporation is a leader in aluminum-based water packaging, promoting infinitely recyclable solutions. In August 2024, Flow Beverage Corp. adopted Ball’s 300ml recycled aluminum bottles, cutting aluminum usage by 30% versus competitors. Ball’s commitment to lightweighting and circularity, combined with a global footprint, positions it as a preferred partner for brands shifting from PET to aluminum.

Tetra Pak Expands Carton-Based Bottled Water Packaging

Tetra Pak continues to diversify into carton packaging for bottled water. In August 2025, it partnered with Danone to launch paper-based cartons for water products, integrating renewable materials into beverage packaging. Its processing-packaging ecosystem allows seamless adoption by bottlers, while its circularity-first approach enhances brand ESG credentials.

Sidel Group Innovates Lightweight PET Solutions for Bottled Water

Sidel specializes in equipment and packaging design for beverages, with PET lightweighting technology reducing plastic usage by up to 25% per bottle (June 2025 launch). Its end-to-end packaging services make it a single-source provider for beverage producers, offering energy-efficient lines and advanced bottle designs that reduce material costs while supporting brand sustainability goals.

Bottled Water Packaging Market Share Insights

Bottles Command Bottled Water Packaging Market Share by Type

Bottles overwhelmingly dominate the bottled water packaging market, projected to hold a massive 92% share in 2025, with PET and rPET bottles remaining the global standard for affordability, lightweight design, durability, and widespread recycling infrastructure. Aluminum cans, with a growing 5% share, represent the leading challenger as sustainability narratives and recyclability advantages resonate with younger, eco-conscious consumers. Pouches and bags-in-box formats collectively make up only 3%, serving specialized niches such as novelty packs, institutional water coolers, and emergency supplies. Despite emerging alternatives, bottles remain the undisputed packaging leader, balancing low production costs with consumer convenience and strong supply chain integration, though sustainability pressures are accelerating the growth of can-based formats and refill systems.

Residential Consumption Leads Bottled Water Packaging Market Share by End-Use

Residential consumption accounts for the largest share of bottled water packaging at 40% in 2025, driven by bulk multi-pack purchases of single-serving bottles and larger gallon jugs from grocery and warehouse retailers. Commercial end-use follows closely at 35%, with steady demand across offices, hospitality, and event spaces supported by a mix of single-serve bottles and large water cooler containers. Food service represents 25% of market share, defined by immediate consumption purchases in restaurants, airports, cafes, and vending machines where convenience and brand presence drive impulse sales. This segment is also leading the shift toward alternatives such as canned or filtered water as sustainability mandates reshape single-use packaging. Collectively, end-use dynamics reflect bottled water’s dual nature as both a household staple and an on-the-go convenience product, with sustainability trends increasingly influencing packaging choices.

United States Bottled Water Packaging Market Driven by Regulatory Reforms and Sustainability Investments

The U.S. bottled water packaging market is witnessing significant transformation due to stringent federal and state regulations, as well as corporate sustainability initiatives. While the FDA regulates bottled water as a food product, states like Washington and Maryland have passed Extended Producer Responsibility (EPR) bills in 2025, requiring producers to fund and manage the lifecycle of their packaging. This has accelerated the adoption of more sustainable materials such as recycled PET (rPET) and bio-based alternatives.

Corporate investments are heavily focused on sustainable and innovative packaging. In February 2025, Win Win Water launched 100% plant-based, biodegradable bottles derived from sugarcane, while Flow Beverage Corp introduced aluminum bottles with 70% recycled content. Technological advancements, including lightweighting of PET bottles and optimized designs for multi-pack and single-serve formats, are reducing material use and production costs. Sustainability is a key driver, with companies investing in recycling infrastructure and alternative materials to align with environmental expectations. The e-commerce boom is further shaping packaging strategies, requiring durable, visually appealing solutions that maintain product integrity during shipping. The EPA’s “National Strategy to Prevent Plastic Pollution” also provides a policy framework supporting these sustainability trends.

Germany Bottled Water Packaging Market Shaped by Circular Economy Regulations and Premium Innovation

Germany’s bottled water packaging industry is governed by a stringent regulatory environment, including the EU Packaging and Packaging Waste Regulation (PPWR) effective February 2025. This mandates full recyclability or reuse of all packaging by 2030, directly influencing material selection and machinery requirements. Germany’s Packaging Act (VerpackG) reinforces producer responsibility over the full lifecycle of packaging, encouraging the adoption of recyclable and reusable solutions.

Technological innovation is driving market evolution. Companies are developing machinery capable of handling sustainable materials such as high-barrier paper-based films, enabling compliance with circular economy mandates. The industry is seeing a focus on premium bottled water in glass bottles and functional waters with added nutrients. Investments in R&D from German packaging manufacturers and research institutions are promoting lighter, stronger, and more sustainable packaging solutions, while reusable and refillable bottle systems are gaining traction in response to governmental targets for waste reduction.

China Bottled Water Packaging Market Accelerates with Green Policies and Domestic Production Expansion

China’s bottled water packaging market is strongly influenced by government-led sustainability initiatives under the “dual carbon” goal. The five-year action plan (2021-2025) encourages the elimination of single-use plastics and promotes bio-based alternatives, shaping the materials and technologies used in bottled water packaging. Regulatory reforms by SAMR and updates to GB standards provide a clear framework aligned with global safety and consumer protection requirements.

Technological advancements, including AI and “5G plus industrial internet” integration, are optimizing production efficiency and flexible manufacturing capacities. Domestic manufacturers are expanding to reduce dependence on imports, meeting growing demand from the booming e-commerce and food delivery sectors. High demand for safe, convenient, and cost-effective packaging solutions drives innovation in lightweight, sustainable materials. China continues to be a major hub for packaging research and patents, reflecting ongoing investment in new materials and production methods for bottled water packaging.

India Bottled Water Packaging Market Boosted by Sustainability Regulations and Strategic Investments

India’s bottled water packaging industry is experiencing rapid growth driven by government initiatives such as “Make in India” and “Zero Effect Zero Defect,” which emphasize high-quality domestic production. The CSIR-led National Mission on Sustainable Packaging Solutions is promoting sustainable materials and recycling methods. Regulatory policies, including MoEFCC bans on single-use plastics and new mandates requiring 30% recycled content in PET bottles from April 2025, are further shaping industry practices.

Technological adoption is rising, with automated packaging systems enabling efficient production of sustainable materials. Companies are investing in equipment for biodegradable and recyclable packaging solutions. Corporate investments, such as Siegwerk’s INR 350 crore commitment to expand innovation, manufacturing, and sustainability capabilities, underscore the sector’s focus on premium and eco-friendly packaging. Key applications are concentrated in the expanding food and beverage industry, particularly ready-to-drink beverages, where consumer safety and quality standards drive demand for innovative packaging solutions.

Brazil Bottled Water Packaging Market Expands Through Regulatory Incentives and Sustainable Material Adoption

Brazil’s bottled water packaging market is strongly influenced by the National Solid Waste Policy and recent 2024 legislation, which mandates that all packaging be returnable, recyclable, or compostable by 2030. ANVISA’s RDC 843/2024 streamlines regulatory approvals, facilitating the introduction of compliant packaging solutions.

Technological advancements, including robotics and AI, are improving operational efficiency and quality control. Sustainability is a central focus, with companies exploring green materials and investing in machinery capable of processing them. Key applications in the food, beverage, and cosmetics sectors are driving demand for high-quality bottled water packaging. Governmental support, including upcoming recycling mandates (30% in 2025 and 50% by 2040), ensures continued emphasis on eco-friendly packaging. Corporate initiatives are reinforcing this trend, with investments in advanced machinery and materials enabling manufacturers to meet growing sustainability and operational efficiency goals.

Bottled Water Packaging Market Report Scope

Bottled Water Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$51.6 Billion

|

|

Market Size (2034)

|

$77.3 Billion

|

|

Market Growth Rate

|

4.6%

|

|

Segments

|

By Material Type (Plastic, Glass, Metal, Other Materials), By Packaging Type (Bottles, Cans, Pouches, Bags-in-box), By Water Type (Still Water, Carbonated Water, Flavored Water, Functional Water), By End-Use (Residential, Commercial, Food Service), By Distribution Channel (Supermarkets & Hypermarkets, Convenience Stores, Online Retail, Other Channels)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, Plastipak Holdings, Inc., Ball Corporation, Berry Global Group, Inc., International Paper Company, O-I Glass, Inc., DS Smith Plc, Crown Holdings Inc., Huhtamäki Oyj, Mondi Group, Tetra Pak International S.A., Graham Packaging Company, Greif, Inc., Silgan Holdings Inc., Sonoco Products Company

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Bottled Water Packaging Market Segmentation

By Material Type

- Plastic

- Glass

- Metal

- Other Materials

By Packaging Type

- Bottles

- Cans

- Pouches

- Bags-in-box

By Water Type

- Still Water

- Carbonated Water

- Flavored Water

- Functional Water

By End-Use

- Residential

- Commercial

- Food Service

By Distribution Channel

- Supermarkets & Hypermarkets

- Convenience Stores

- Online Retail

- Other Channels

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Bottled Water Packaging Market

- Amcor plc

- Plastipak Holdings, Inc.

- Ball Corporation

- Berry Global Group, Inc.

- International Paper Company

- O-I Glass, Inc.

- DS Smith Plc

- Crown Holdings Inc.

- Huhtamäki Oyj

- Mondi Group

- Tetra Pak International S.A.

- Graham Packaging Company

- Greif, Inc.

- Silgan Holdings Inc.

- Sonoco Products Company

* List Not Exhaustive

Methodology

USDAnalytics employs a comprehensive, data-driven research methodology to deliver in-depth insights into the global bottled water packaging market. Our approach combines primary research, including interviews with packaging manufacturers, beverage brands, sustainability experts, and regulatory authorities, with extensive secondary research sourced from corporate filings, trade journals, patent databases, and policy documents. Market sizing, CAGR projections, and trend analysis are generated by evaluating material innovations such as PET, rPET, aluminum, glass, and emerging bioplastics, alongside technological advancements in lightweighting, digital watermarks, and hybrid paper-based bottles. USDAnalytics also examines the impact of global sustainability mandates, Extended Producer Responsibility (EPR) regulations, and regional regulatory frameworks across key geographies including the U.S., EU, China, India, Brazil, and Japan. Corporate strategies, mergers, and investments by leading players like Amcor, Plastipak, Ball Corporation, Tetra Pak, and Sidel are assessed to provide actionable insights on market growth drivers, competitive dynamics, and emerging opportunities, enabling industry professionals to make informed decisions in the evolving bottled water packaging landscape.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.