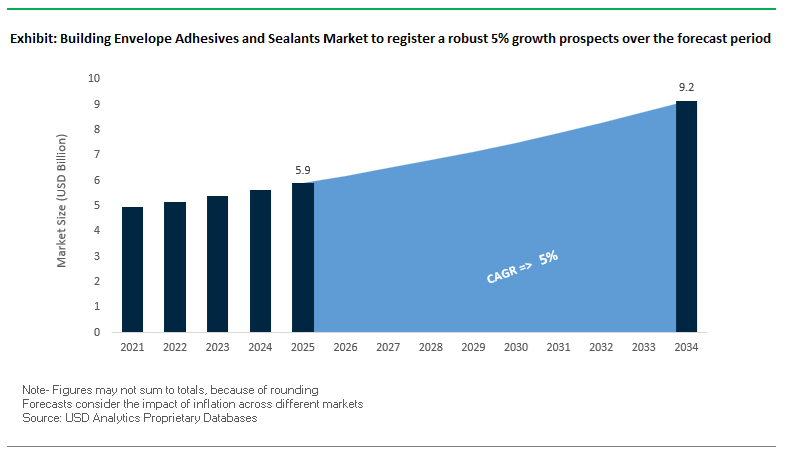

The global building envelope adhesives and sealants market has become strategically important as energy efficiency, climate resilience, and long-term durability move from design preferences to regulatory and financial imperatives. Valued at USD 5.9 billion in 2025 and forecast to reach USD 9.2 billion by 2034 at a CAGR of 5%, market growth reflects the central role of bonding and sealing systems in controlling air leakage, moisture ingress, and thermal losses across façades, roofs, and wall assemblies. For developers, façade engineers, and building owners, adhesives and sealants directly influence compliance with energy codes, operating costs, and asset lifecycle performance rather than serving as secondary construction materials.

The core structural shift reshaping demand is the tightening of building energy and performance standards alongside the adoption of engineered envelope systems. Adhesive and sealant formulations are increasingly specified to meet assembled air barrier requirements defined under ASTM E2357, where leakage rates must remain below 0.2 L/(s·m²) at 75 Pa to satisfy IECC and ASHRAE 90.1 targets. In parallel, envelope materials are being qualified against more aggressive weather-load criteria, with structural adhesives and silicone weatherproofing sealants validated under sustained positive and negative pressures up to 600 Pa and gust loads equivalent to 1200 Pa. These requirements are accelerating substitution away from traditional mechanical fastening and solvent-borne mastics toward continuous adhesive air barriers, silicone glazing sealants, and hybrid polymer systems that deliver predictable performance under thermal cycling, wind load, and long-term UV exposure.

This material transition produces measurable business outcomes across the construction value chain. Improved airtightness reduces heating and cooling demand, lowering operational energy costs and supporting green building certifications such as LEED. Silicone sealants, which continue to dominate resin usage due to superior UV stability and elastic recovery, extend joint service life in curtain walls and façade systems, reducing maintenance interventions and water-related failures. At the same time, water-based low-VOC adhesive systems have become the default choice for air barrier and insulation bonding, aligning contractor workflows with indoor air quality requirements and sustainability mandates without sacrificing adhesion reliability. Over the forecast period, competitive positioning in the building envelope adhesives and sealants market will increasingly depend on verified system-level performance, formulation consistency across global supply chains, and alignment with evolving energy codes and low-carbon construction standards that tie material selection directly to building performance outcomes.

The building envelope adhesives and sealants industry is undergoing a pivotal transformation driven by carbon-neutral materials, regulatory mandates, and high-performance system integration across global construction markets. Manufacturers are prioritizing sustainability and efficiency, aligning with zero-emission targets and circular economy initiatives shaping the future of façade and roofing systems.

In Q4 2024, Dow launched its Carbon-Neutral Silicone for Building Façades, verified under the PAS 2060 standard, marking a significant sustainability milestone. This innovation directly supports the green façade and structural glazing market by lowering embodied carbon emissions during silicone manufacturing. In early 2025, multinational producers began realigning supply chains following new U.S. tariffs on imported raw materials, prompting a surge in nearshoring strategies and localized manufacturing to mitigate costs and ensure compliance with new trade and material sourcing frameworks.

A major highlight came in May 2025, when H.B. Fuller partnered with MITER Brands and Corning Incorporated to commercialize Ködispace 4SG, a thermoplastic warm-edge spacer system for triple-pane insulating glass units (IGUs). This advancement improves thermal insulation efficiency while reducing glass unit weight — a crucial innovation for high-performance window and façade construction. Concurrently, Silicone and Polyurethane (PU) sealants continue to dominate resin demand as per Q3 2025 data, favored for their flexibility, adhesion, and weathering resistance across concrete, glass, and metal substrates.

Market growth is further supported by a surge in wall assembly applications. Industry reports from Q4 2024 show rapid adoption of prefabricated and modular wall panels that require high-bond adhesives and air-sealing materials, boosting consumption in the commercial and residential sectors. In Asia Pacific, construction investments in 2024 surged due to large-scale infrastructure projects in China, India, and Southeast Asia, solidifying APAC as the largest regional consumer of PU and silicone-based building sealants.

Regulatory evolution also plays a defining role. Ongoing green building code revisions in North America and Europe — including stricter IECC and EN 12114 air-tightness standards — are reinforcing demand for advanced sealants capable of meeting 0.2 L/(s·m²) leakage performance and high dynamic load durability. This convergence of sustainability and performance has positioned silicone, polyurethane, and silane-terminated polymer (STP) systems as the backbone of next-generation building envelope materials.

The surge in demand for high-rise buildings, coupled with architectural preferences for large-format glass and frameless façades, is fueling the widespread adoption of high-modulus structural silicone adhesives within unitized curtain wall systems. These next-generation silicones exhibit design strengths averaging around 20 psi (138 kPa) for transferring wind loads from glass panels to supporting metal frames—performance levels that make them indispensable for modern façades in high-wind and seismic zones. The strength capability allows for the replacement of conventional mechanical retention systems, transforming silicone from a sealant into a primary structural bonding medium capable of carrying dynamic loads in skyscraper and façade engineering applications.

One of the most significant performance differentiators is seismic resilience. Structural Silicone Glazing (SSG) systems, which elastically attach glass to metal frames, have been proven to outperform rigid mechanical systems during seismic events. Their ability to accommodate inter-story drift without glass breakage has positioned high-modulus silicones as the material of choice for building envelopes in earthquake-prone regions across North America, Japan, and Southeast Asia. Further, the increasing adoption of factory-controlled, unitized façade manufacturing—where panels are assembled and cured off-site—has created an additional advantage for these adhesives. Factory curing minimizes environmental variables like temperature and humidity that often cause on-site adhesion failures. The result is superior bond integrity, dimensional precision, and faster installation cycles, aligning perfectly with the construction industry’s shift toward prefabricated façade systems.

The industrial migration to high-strength, fast-curing, and durable silicone bonding systems is further supported by green building trends. Several leading manufacturers market carbon-neutral silicone sealants (verified under PAS 2060) with 20-year warranties, directly contributing to low-carbon façade design. Thus, high-modulus silicones are not merely performance materials—they are strategic enablers of sustainable façade engineering, ensuring both aesthetic excellence and structural resilience in modern urban architecture.

Energy-efficient construction is reshaping the adhesives and sealants market, driving the development of air-barrier-specific sealants that directly contribute to achieving whole-building airtightness targets set by stringent global energy codes. The 2018 and 2021 International Energy Conservation Codes (IECC), along with ASHRAE Standard 90.1, establish a maximum air leakage rate of 0.40 cfm/ft² (2.0 L/s·m²) for commercial and residential buildings. The regulation compels architects, engineers, and contractors to specify low-permeance sealants capable of sustaining building airtightness over decades of structural and environmental movement.

Field data and NIST research report that joints, penetrations, and wall-roof intersections are responsible for the majority of envelope leakage—often with average gap widths exceeding 0.095 inches, creating vulnerabilities in thermal and moisture control. Modern sealants designed for air barrier systems must not only adhere to diverse substrates but also accommodate joint movement factors of ±50% or greater while retaining flexibility. The emergence of fluid-applied elastomeric sealants that integrate with continuous air barrier membranes represents one of the fastest-growing product categories within the market.

The economic and sustainability implications are equally profound. Studies show that air leakage and infiltration can increase a building’s heating and cooling load by 10% in cooling climates and up to 42% in heating climates, directly impacting energy costs. For building owners, the selection of high-elasticity, long-life sealants translates into tangible operational savings, positioning airtightness as both a compliance mandate and an economic advantage. In parallel, the increasing global emphasis on net-zero buildings and carbon reduction under frameworks such as LEED, BREEAM, and Energy Star continues to push demand for low-VOC, high-performance air barrier sealants, solidifying their role as critical components in high-performance building envelopes.

The aging façade infrastructure of commercial buildings—especially in North America and Europe—represents a multi-billion-dollar retrofit opportunity for manufacturers of advanced adhesives and sealants. The typical service life of curtain wall systems ranges between 30 and 50 years, after which deterioration in weather seals, IG unit performance, and façade anchoring leads to moisture ingress and thermal inefficiency. Given that most commercial buildings constructed during the 1980s–1990s construction boom are reaching the renewal window, a surge in recladding and re-glazing activities is imminent.

In the U.S., renovation and retrofit projects account for nearly 50% of all architecture firm billings, underscoring that modernization—not new construction—is the dominant growth driver. Retrofit applications rely heavily on high-performance silicone and polyurethane sealants to reseal aged joints, replace perimeter gaskets, and restore glazing performance. Further, the European Union’s “Renovation Wave Strategy” under the Fit for 55 initiative aims to triple renovation rates to 3% per year by 2030, amplifying demand for energy-efficient envelope materials. These policies are supported by large-scale funding mechanisms such as the European Green Deal and national subsidy programs for façade energy retrofits.

Manufacturers are responding with specialized adhesion-boosted silicone hybrid systems tailored for non-standard substrates found in retrofit scenarios, such as aged concrete, anodized aluminum, and composite panels. The intersection of policy, aging infrastructure, and sustainability goals has therefore created a sustained, high-volume aftermarket for maintenance, repair, and overhaul (MRO) sealants and adhesives—positioning them as essential to the global building decarbonization agenda.

The rapid rise of mass timber (MT) and Cross-Laminated Timber (CLT) construction represents a transformative opportunity for adhesive and sealant suppliers. With over 2,500 mass timber projects completed or under development in the U.S. and an annual growth rate of around 20%, the structural use of engineered wood is transitioning from niche to mainstream in mid- and high-rise applications. However, mass timber’s hygroscopic behavior—its natural tendency to absorb and release moisture—creates unique challenges for adhesive bonding, fire resistance, and air sealing that conventional products cannot address.

To meet these challenges, manufacturers are formulating flexible, fire-rated sealants and adhesives specifically designed to bond to wood substrates while accommodating dimensional changes due to humidity and temperature fluctuations. The International Building Code (IBC) for mass timber types IV-A, IV-B, and IV-C explicitly mandates the use of ASTM C920-compliant sealants at abutting timber connections, ensuring both fire containment and air barrier continuity. In addition, intumescent fire protection sealants have demonstrated the ability to significantly delay thermal transfer through timber joints—reducing connector temperatures from 286°C to under 200°C after 80 minutes in full-scale fire testing.

Moisture protection during construction also remains a critical factor in mass timber performance. Without proper sealing, CLT joints can experience microbial growth due to water exposure. To address the, manufacturers are introducing factory-applied hydrophobic coatings and joint sealants with extended weather protection capabilities of up to 12 weeks. These advancements are not only critical for preserving wood integrity but also essential for meeting evolving building code fire and durability requirements. As the global market for hybrid structures—combining timber, steel, and concrete—continues to expand, suppliers of mass timber-compatible adhesives and sealants are strategically positioned to capitalize on the sustainable construction revolution.

Building Envelope Adhesives and Sealants Market Share Insights, 2025-2034

The Sealants segment commands the majority share of the global building envelope adhesives and sealants industry, accounting for an estimated 58.6% of the total market in 2025. This dominance reflects the indispensable role of sealants in maintaining weather resistance, energy efficiency, and building integrity. Sealants are the primary barrier materials used across façades, curtain walls, windows, roofs, and expansion joints to prevent air, water, and vapor ingress—key performance factors in achieving tight, durable, and energy-efficient building envelopes. High-performance weatherproofing sealants, particularly silicone, polyurethane, and hybrid MS polymer formulations, dominate this space due to their elasticity, UV resistance, and long-term durability. These products enable compliance with stringent green building codes (LEED, BREEAM) and regional energy efficiency standards. Glazing sealants remain mission-critical in curtain wall and window systems, where they ensure adhesion between glass and framing materials under dynamic load and thermal expansion. Meanwhile, firestop sealants serve as a specialized subcategory ensuring compartmentalization and life safety in compliance with fire codes. The ongoing shift toward low-VOC and high-performance hybrid technologies further reinforces sealants’ leadership position, as construction professionals demand solutions that combine environmental safety with mechanical performance.

The Adhesives segment, representing approximately 41.4% of the global market, plays an increasingly critical role in the assembly, bonding, and structural integrity of modern building envelopes. Adhesives have transitioned from being auxiliary products to becoming key enablers of design flexibility and energy-efficient construction. Structural adhesives are vital in curtain wall systems, composite panels, and cladding assemblies, offering high strength-to-weight ratios and enabling architects to replace mechanical fasteners with sleek, continuous bonded joints that enhance both aesthetics and aerodynamics. Polyurethane, epoxy, and silane-modified adhesives are gaining widespread adoption for their superior bonding to dissimilar materials such as glass, aluminum, concrete, and composite substrates. Additionally, construction adhesives—including reactive and water-based formulations—are used extensively for panel installation, insulation attachment, and subfloor bonding, ensuring cohesive structural performance. The shift toward prefabrication, modular construction, and off-site manufacturing is further accelerating adhesive demand, as pre-bonded panels and systems require robust, flexible, and durable bonding technologies. While adhesives currently trail sealants in market share by volume, they often represent a higher value per kilogram due to their specialized formulations and performance-critical applications in structural façades and hybrid building systems. The steady replacement of mechanical fixings with bonded assemblies underscores adhesives’ rising role as a transformative technology in next-generation envelope construction.

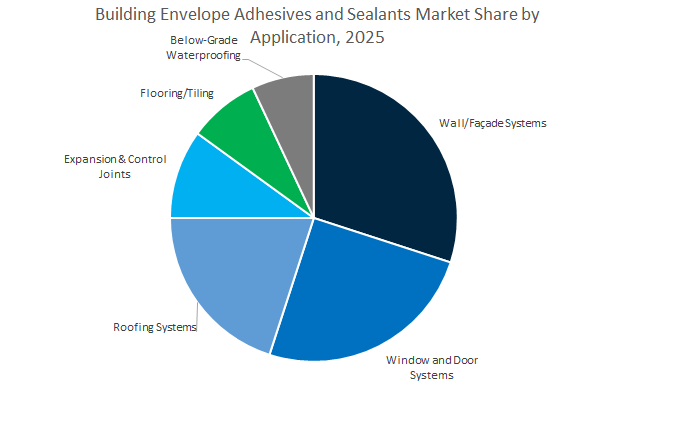

The Wall and Façade Systems segment holds the largest share of the global building envelope adhesives and sealants market, accounting for approximately 30.9% in 2025, driven by its central role in defining the thermal, moisture, and aesthetic performance of buildings. Modern façade systems—especially curtain walls, rainscreens, and ventilated façades—are highly dependent on sealants and structural adhesives for joint sealing, cladding attachment, and glazing integration. High-performance silicone and hybrid polymer sealants ensure long-term flexibility and resistance to environmental stressors such as UV exposure, wind loads, and temperature cycling. Simultaneously, structural adhesives enable the design of frameless glass façades, composite cladding panels, and façade anchoring systems, delivering both visual appeal and durability. As green building standards increasingly prioritize air and moisture control layers, demand for façade sealing and bonding materials has surged across North America, Europe, and Asia-Pacific. The growing adoption of unitized façade systems and prefabricated panels in high-rise and commercial construction further amplifies the importance of advanced adhesives and sealants that deliver consistent performance and facilitate faster installation cycles. This segment is also witnessing innovation in low-modulus, high-elongation sealants designed for complex façade geometries and energy-efficient designs.

The Window and Door Systems segment forms one of the key pillars of the market, fueled by global emphasis on energy-efficient fenestration and high-performance glazing systems. Sealants are indispensable in insulating glass units (IGUs) and perimeter joints, ensuring airtightness, watertightness, and long-term adhesion between glass, spacers, and frames. The increasing prevalence of triple-glazed and low-E coated windows in both residential and commercial construction amplifies sealant usage per unit. Structural glazing adhesives—particularly silicones and polyurethane-based systems—enable frameless designs that improve aesthetics and thermal efficiency while supporting architectural creativity. In parallel, roofing systems account for a substantial portion of demand, particularly for waterproofing membranes, flashings, and roof penetrations. These applications rely heavily on UV-resistant, elastomeric sealants and adhesives for membrane bonding, essential for preventing water ingress and extending roof life. As the adoption of cool roofs, green roofs, and solar-integrated systems increases, sealant formulations are being optimized for temperature tolerance, adhesion to new substrates, and environmental exposure.

Specialized applications—including Expansion and Control Joints, Flooring/Tiling, and Below-Grade Waterproofing—collectively form a high-value niche within the building envelope market. Expansion joints are among the most demanding applications, requiring sealants with high movement capability (±50% or greater), chemical resistance, and long-term elasticity to accommodate thermal and structural movement in concrete and steel frameworks. These sealants are mission-critical in high-rise buildings, airports, and stadiums. Flooring and tiling adhesives, particularly in commercial and industrial settings, contribute to the overall envelope’s performance by preventing vapor intrusion and ensuring cohesive bonding between substrates and finishing materials. Below-grade waterproofing—encompassing foundations, basements, and tunnels—represents a specialized segment that requires hydrophobic, chemically resistant, and pressure-tolerant sealants and adhesives to ensure water and vapor barrier integrity.

The global building envelope adhesives and sealants market is dominated by Dow Construction Chemicals, H.B. Fuller, Sika AG, Henkel AG & Co. KGaA, Arkema/Bostik, and Wacker Chemie AG. These companies are setting benchmarks in silicone and polyurethane innovations, bio-based adhesive systems, and carbon-neutral production processes, each reinforcing their technological leadership and commitment to sustainable construction materials.

Dow maintains its market leadership through DOWSIL™, a flagship brand synonymous with silicone structural glazing and weatherproofing systems. The company’s Carbon-Neutral Silicones for Building Façades, introduced in late 2024, represent a key advancement toward decarbonizing the silicone feedstock supply chain, leveraging renewable energy and verified PAS 2060 methodologies. Its extensive product line spans weatherproofing, firestopping, and insulating glass (IG) sealants, providing system-wide adhesion compatibility across multiple substrates including metal, glass, and concrete.

H.B. Fuller is strategically expanding its high-performance materials (HPM) segment to serve modern construction needs, particularly in modular and off-site prefabrication. Its innovation partnership with MITER Brands and Corning in May 2025 introduced Ködispace 4SG, a breakthrough in triple-pane insulating glass adhesive technology, enhancing energy performance and design flexibility. Through targeted acquisitions, including Beardow Adams, the company has strengthened its European presence and product diversity across polyurethane, acrylic, and thermoplastic adhesive systems.

Sika AG leads in silane-terminated polymer (STPE) technology through its Sikaflex® and Sikasil® product lines, combining the performance of silicones with the workability and paintability of polyurethanes. The company’s “Target Market” approach emphasizes sealing and bonding solutions for refurbishment and new infrastructure projects, ensuring broad adoption in commercial façades, parking structures, and bridge expansion joints. Through continuous acquisitions, Sika enhances its local compliance capabilities and expands low-VOC, high-flexibility adhesive systems worldwide.

Henkel continues to dominate in adhesive technologies through its Pattex and Loctite brands, serving both professional construction and MRO sectors. The company invests heavily in bio-based and solvent-free adhesive formulations that align with EU Green Deal and LEED certification requirements. Its focus extends to foam adhesives for cladding systems, joint fillers, and non-structural sealants engineered for thermal insulation and moisture control. Henkel’s strategic push in technical support services enhances adoption in large-scale commercial construction globally.

Arkema, through its Bostik division, is expanding its presence in construction systems such as tile adhesives, waterproofing membranes, and façade bonding solutions. Its MS Polymer and Polyurethane-based formulations are designed for high movement tolerance, direct glazing, and cladding fixation. With strategic acquisitions (e.g., LIP Bygningsartikler AS), Arkema enhances its European distribution and product certification network. The company’s smart adhesives platform ensures cohesive integration across construction materials, promoting faster, safer installations.

Wacker Chemie AG stands out for its vertical integration in silicone feedstock production, ensuring raw material stability amid volatile supply chains. Its ELASTOSIL® and GENIOSIL® brands deliver RTV silicones and STP adhesives that meet stringent GEV EMICODE EC1 Plus air quality standards. Wacker’s sealants are critical for insulating glass, joint sealing, and façade waterproofing, offering long-term flexibility and resistance to extreme thermal cycling. The company continues to lead innovation in solvent-free, low-emission building envelope adhesives for next-generation architecture.

The United States building envelope adhesives and sealants market continues to expand, supported by government-backed infrastructure spending and sustainability mandates under DOE and USGBC guidelines. A pivotal development came in June 2025, when the U.S. government earmarked $410 billion toward the Stargate project—a nationwide initiative to construct next-generation data centers. The facilities heavily rely on Sika’s advanced waterproofing and facade sealing systems, emphasizing durability, air-tight performance, and weatherproof bonding from foundation to rooftop.

The transition toward eco-friendly, water-based adhesive technologies is also reshaping the market, accounting for the largest market share in 2024, driven by compliance with evolving LEED and Green Building Council standards. Market leaders such as Tremco CPG and H.B. Fuller have expanded their U.S. manufacturing capacities to meet surging demand from both commercial and residential remodeling sectors, particularly for low-VOC hybrid sealants.

Additionally, polyurethane resins dominate U.S. adhesive usage in large-scale roofing and curtain wall applications due to their high flexibility, superior adhesion, and weather resistance. As federal and state energy codes tighten, high-performance wall joint sealing remains a crucial application area, ensuring compliance with national energy efficiency objectives. The rise of modular and prefabricated buildings has further spurred demand for fast-curing, automated-applied sealants, positioning the U.S. as a leader in energy-efficient building envelope systems.

China remains the world’s largest consumer and producer of building envelope adhesives and sealants, propelled by rapid urbanization, advanced skyscraper development, and green policy enforcement. According to industry analysis (September 2025), China’s infrastructure and residential construction boom continues to outpace other regions, with middle-class housing and commercial real estate driving record volumes of sealant consumption.

National mandates emphasizing air quality improvement and VOC reduction have accelerated the shift toward water-based, solvent-free adhesives and eco-friendly silicone formulations. Major domestic and global players—such as Sika, H.B. Fuller, and Huitian Adhesives—are expanding capacity to meet demand from the façade, curtain wall, and glazing markets.

China’s construction sector is also witnessing a technological shift, with high-rise facade projects increasingly specifying high-modulus silicone and PU-based structural glazing sealants for enhanced structural integrity, UV resistance, and energy performance. The government’s focus on green urbanization and energy-efficient buildings, under the 14th Five-Year Plan, continues to strengthen demand for smart, high-strength, and recyclable adhesives for both commercial towers and public infrastructure.

Germany’s building envelope adhesives and sealants industry is a cornerstone of Europe’s Energiewende (energy transition) strategy, emphasizing thermal insulation, low-emission construction, and sustainable material innovation. In May 2024, Dow expanded its minority equity stake in SAS Chemicals GmbH, strengthening its regional portfolio of organic, hybrid, and silicone-based insulating glass sealants for advanced European façade and window systems.

The country’s Passive House Standard, recognized globally for its ultra-low energy requirements, continues to fuel demand for high-performance airtightness adhesives and polyurethane foam sealants designed for zero-energy buildings. Moreover, government-backed renovation subsidy programs are boosting retrofit activities, creating a growing market for exterior wall, roof sealing, and air barrier applications.

Germany’s manufacturers—such as Wacker Chemie, Henkel, and Dow—are at the forefront of bio-based hybrid adhesives and low-isocyanate polyurethane chemistries, in line with EU REACH compliance and circular economy targets. The industry is also witnessing strong R&D activity in self-healing sealant materials, enabling long-term durability and reduced maintenance in façade joints and insulating glass systems.

Turkey has rapidly emerged as a strategic regional hub for building envelope sealant production, supported by its geographic advantage and strong construction growth across Eastern Europe, the Middle East, and North Africa (EMEA). In May 2024, Dow expanded its SAS Chemicals plant in Turkey to ramp up production of insulating glass sealants, catering to surging global and regional demand for façade, window, and curtain wall applications.

The country’s booming high-rise and commercial construction sector is increasingly adopting advanced silicone structural glazing systems to enhance façade durability and UV resistance under varying climatic conditions. Turkey’s strong manufacturing base and trade accessibility make it a preferred distribution hub for weatherproofing and waterproofing products, enabling faster supply to emerging Middle Eastern markets.

The UK building envelope adhesives and sealants market is undergoing major regulatory transformation driven by the upcoming Future Homes Standard (2025), which enforces the adoption of low-carbon materials, electric heat systems, and airtight construction to minimize energy consumption. The regulation is significantly increasing demand for high-efficiency airtight adhesives, hybrid sealants, and low-embodied carbon materials in both residential and commercial buildings.

In 2025, Sika Group acquired Cromar Building Products, expanding its UK presence and portfolio in building envelope waterproofing and façade bonding systems. The acquisition strengthens Sika’s position in the residential and light commercial construction segment, ensuring comprehensive product coverage from roof to foundation.

Furthermore, the UK Green Building Council (UKGBC) and national policymakers emphasize Life Cycle Assessments (LCA) in construction, prioritizing manufacturers that provide transparent, sustainable, and traceable sealant formulations. The approach is reshaping the UK adhesives market toward fully compliant, VOC-free, and recyclable product lines for high-performance façade systems.

India’s building envelope adhesives and sealants industry is expanding rapidly, propelled by government infrastructure initiatives and robust urbanization. The government’s Housing for All and National Infrastructure Pipeline (NIP) projects have significantly boosted the use of adhesives and sealants in large-scale commercial, residential, and transportation developments.

Sika India, a key player in the market, is offering end-to-end engineered solutions that provide foundation-to-roof protection, focusing on durability, waterproofing, and structural integrity in high-performance buildings and energy projects. Meanwhile, affordable housing programs are fueling demand for cost-effective, general-purpose acrylic and PU sealants, creating a dual-market dynamic—high-value engineered solutions for urban projects and volume-driven consumption for residential sectors.

As foreign investment in smart cities, airports, and logistics hubs accelerates, the adoption of advanced weatherproofing, façade adhesives, and expansion joint sealants is set to increase. India’s market trajectory is further supported by the country’s move toward local manufacturing and Make in India policies, attracting global adhesive producers to establish domestic production bases.

Building Envelope Adhesives and Sealants Market Report Scope

Building Envelope Adhesives and Sealants Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$5.9 Billion

|

|

Market Size (2034)

|

$9.2 Billion

|

|

Market Growth Rate

|

5%

|

|

Segments

|

By Product Type (Adhesives, Sealants), By Resin Type (Polyurethane, Epoxy, Acrylic, Rubber, Polyvinyl Acetate, Silane Modified Polymer, Silicone, Polysulfide), By Technology (Water-Based, Solvent-Based, Solvent-Less, UV Cured), By Application (Roofing Systems, Wall/Façade Systems, Window and Door Systems, Flooring/Tiling, Below-Grade Waterproofing, Expansion & Control Joints

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Henkel AG & Co. KGaA, Sika AG, The Dow Chemical Company, H.B. Fuller Company, Arkema S.A., 3M Company, Wacker Chemie AG, RPM International Inc., DAP Global Inc., Huntsman Corporation, Mapei S.p.A., PPG Industries, Inc., BASF SE, DuPont de Nemours, Inc., Avery Dennison Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Product Type

By Resin Type/Chemistry

- Polyurethane

- Epoxy

- Acrylic

- Rubber

- Polyvinyl Acetate

- Silane Modified Polymer

- Silicone

- Polysulfide

By Technology

- Water-Based

- Solvent-Based

- Solvent-Less

- UV Cured

By Application

- Roofing Systems

- Wall/Façade Systems

- Window and Door Systems

- Flooring/Tiling

- Below-Grade Waterproofing

- Expansion & Control Joints

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

- Henkel AG & Co. KGaA

- Sika AG

- The Dow Chemical Company

- H.B. Fuller Company

- Arkema S.A.

- 3M Company

- Wacker Chemie AG

- RPM International Inc.

- DAP Global Inc.

- Huntsman Corporation

- Mapei S.p.A.

- PPG Industries, Inc.

- BASF SE

- DuPont de Nemours, Inc.

- Avery Dennison Corporation

*- List not Exhaustive

Research Coverage

Prepared by USDAnalytics, this report investigates how high-performance building-envelope adhesives and sealants deliver airtightness, thermal continuity, and façade resilience under evolving energy codes and sustainability mandates. Our analysis reviews the adoption inflection of water-based low-VOC systems, silicone weatherproofing and structural glazing solutions, polyurethane/STP hybrids, and IGU spacer integrations that are redefining wall, window, roof, and below-grade assemblies. It highlights performance gating against ASTM/IECC/ASHRAE air-leakage thresholds, seismic/wind pressure design, and multi-substrate adhesion on glass, metal, concrete, and timber—while tracking supply-chain shifts, nearshoring, and carbon-neutral silicone initiatives. The study surfaces market breakthroughs in high-modulus structural silicones for unitized façades, air-barrier-specific elastomeric sealants, and warm-edge IG solutions that raise envelope efficiency and longevity; this report is an essential resource for façade engineers, envelope consultants, specifiers, developers, and contractors seeking code-compliant, low-carbon, and durable envelope systems.

Scope Highlights

Segmentation

- By Product Type: Adhesives; Sealants

- By Resin Type/Chemistry: Polyurethane; Epoxy; Acrylic; Rubber; Polyvinyl Acetate; Silane Modified Polymer; Silicone; Polysulfide

- By Technology: Water-Based; Solvent-Based; Solvent-Less; UV Cured

- By Application: Roofing Systems; Wall/Façade Systems; Window and Door Systems; Flooring/Tiling; Below-Grade Waterproofing; Expansion & Control Joints

Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

Time Horizon: Historic data 2021–2024 and forecasts 2025–2034.

Companies: Analysis/profiles of 15+ companies.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.