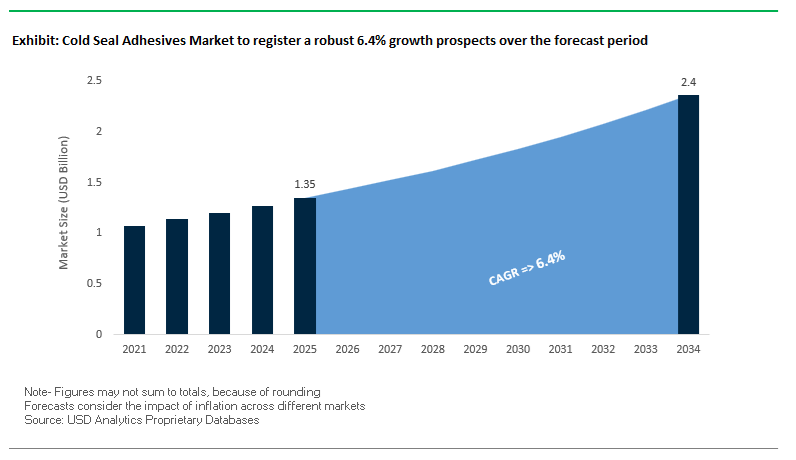

The global cold seal adhesives market, valued at USD 1.35 billion in 2025 and forecast to reach USD 2.4 billion by 2034 at a CAGR of 6.4%, is increasingly tied to high-speed flexible packaging operations in food, confectionery, pharmaceutical, and medical sectors. Cold seal adhesives have moved from niche use to strategic importance as packaging manufacturers redesign lines around energy efficiency, material sensitivity, and regulatory compliance. For brand owners and converters running continuous form-fill-seal (FFS) and flow-wrap lines, cold seal systems directly influence line speed, substrate choice, and total energy intensity rather than functioning as a secondary adhesive input.

The primary structural shift reshaping demand is the replacement of heat-activated and solvent-based sealing technologies with water-based cold seal formulations engineered for instant bond formation under pressure alone. Manufacturers are specifying these systems to protect heat-sensitive substrates such as chocolate coatings, nutraceutical films, and medical papers, where thermal sealing can compromise product integrity. By eliminating heated jaws and dwell time, cold seal adhesives allow packaging lines to operate at higher speeds while cutting sealing-related energy consumption by up to 25%, translating directly into lower operating costs and reduced Scope 1 emissions. This transition is reinforced by tightening food-contact and pharmaceutical packaging regulations, where low-VOC, non-toxic, and water-based chemistries simplify compliance across global markets.

From a substitution standpoint, cold seal adhesives are displacing conventional heat seal layers and solvent systems by delivering reliable seal strength without thermal stress, curing ovens, or solvent recovery infrastructure. In healthcare and pharmaceutical packaging, these materials are increasingly specified for tamper-evident and sterile formats compatible with coated papers and medical-grade films, supporting both safety validation and high-throughput production. As major adhesive producers invest in low-carbon manufacturing routes, renewable feedstocks, and recyclability-aligned formulations, competitive positioning in the cold seal adhesives market will hinge on consistent pressure-activated performance, food and pharma compliance credentials, and scalability across modern, energy-optimized packaging lines.

The cold seal adhesives market continues to evolve rapidly, with leading players intensifying their investments in low-carbon production, bio-based raw materials, and water-based polymer dispersions to meet sustainability mandates and performance standards in high-speed packaging lines.

In October 2025, Henkel and Dow deepened their strategic collaboration to accelerate decarbonization in adhesive manufacturing, focusing on CO₂-reduced feedstocks and renewable electricity. This partnership aims to lower the carbon footprint of adhesive production by 20–40%. Following this, in September 2025, Henkel launched a CO₂-reduced Technomelt Supra 130 Cool adhesive, achieving a verified 20% emission reduction (cradle-to-gate) — a milestone for converters seeking to align with Scope 3 emission targets in consumer goods packaging.

The trend toward sustainability was further reinforced in July 2025, when Henkel’s wash-off PSA Aquence PS 3017 RE received a FINAT Sustainability Award, showcasing its role in enabling PET recycling by allowing labels to detach cleanly during washing — a major step forward in recyclable cold seal label technology. Concurrently, BASF in June 2025 highlighted the Acronal® range of acrylic dispersions and polyurethane systems, key raw materials for water-based cold seal adhesives, underscoring its leadership in environmentally safe polymer solutions.

The industry is also witnessing regional production expansion and raw material diversification. COIM Group introduced a new range of cold seal coatings at Drupa 2024 (announced in April 2025) for confectionery and ice-cream packaging, addressing high-speed mono-film sealing requirements. Arkema’s acquisition of Dow’s flexible packaging laminating adhesives division in December 2024 further strengthened Bostik’s foothold in cold seal and flexible packaging technologies.

In May 2024, Lubrizol advanced the performance of water-based PSA additives, developing an innovative formulation that prevents whitening under moisture exposure — crucial for cold seal labels, tapes, and high-humidity packaging. Additionally, Sika’s low-monomer polyurethane (Purform®) technology launched in July 2024 has industry-wide implications for occupational safety, signaling the future of REACH-compliant, safer adhesives.

The industry’s strong pivot toward high-speed, recyclable flexible packaging has made cold seal adhesives indispensable in the transition to mono-material and sustainable packaging systems. As global brands pursue Extended Producer Responsibility (EPR) compliance and plastic waste reduction, cold seal coatings are enabling packaging engineers to design PE- and PP-based recyclable structures that eliminate the heat-seal layer, reduce material complexity, and lower carbon emissions.

Recent technological advancements have been transformative in the context. Leading chemical suppliers have introduced new cold seal coating systems compatible with over 98% of cold seal applications, covering polyolefin mono-films and full-paper substrates to support circular packaging goals. For instance, one major global adhesive producer has launched a comprehensive portfolio that includes both release lacquers and cold seal coatings explicitly designed to maintain mechanical recyclability while improving printability and process stability. In addition, the Association of Plastic Recyclers (APR) has pre-qualified certain water-based cold seal adhesives as fully compatible with flexible polyethylene (PE) recycling streams, granting them “Store Drop-off” certification — a crucial milestone in making consumer packaging both sustainable and convenient for recycling.

In addition to recyclability, cold seal systems deliver tangible energy efficiency benefits by removing the need for high-temperature sealing equipment, cutting energy consumption by up to 70% compared to traditional heat-sealing lines. The positions cold seal adhesives at the forefront of eco-efficient flexible packaging technologies, aligning with the sustainability goals of multinational FMCG and confectionery brands transitioning to low-carbon, recyclable packaging designs.

The global push toward automation, digital manufacturing, and high-speed packaging is redefining performance requirements for cold seal adhesives. Modern coating and converting lines operating at speeds exceeding 600 m/min demand synthetic, low-viscosity adhesives with unparalleled rheological stability to ensure uniform coating thickness and consistent seal performance. The shift from traditional natural rubber latex systems to synthetic polymer-based cold seals — such as acrylic copolymers and styrene-butadiene dispersions — is enabling the transition by providing enhanced precision and reproducibility in slot-die and gravure coating processes.

For instance, next-generation cold seal adhesives are engineered to maintain a stable Zahn Cup #2 viscosity between 16–40 seconds, offering predictable flow behavior essential for automated film deposition. These synthetic dispersions exhibit excellent anti-blocking characteristics and high cohesive strength, eliminating common production defects like telescoping or pattern instability during high-speed winding. In addition, advancements in polymer chemistry — including balanced soft (Tg ≈ −54°C) and hard segment polymers — ensure fast-pressure activation, maintaining bond strength even under extreme mechanical stress while supporting robotic applications that demand high repeatability.

The rise of Industry 4.0-enabled packaging lines further amplifies the role of cold seal adhesives as an integral component of precision coating systems, where viscosity, deposition rate, and adhesive film uniformity are digitally controlled. Consequently, synthetic cold seal technologies are emerging as the adhesive backbone of fully automated packaging environments, offering superior scalability, productivity, and sustainability across the global flexible packaging value chain.

The intrinsic no-heat sealing advantage of cold seal adhesives presents a major growth opportunity in temperature-sensitive and high-value packaging sectors, including fresh food, confectionery, dairy, frozen desserts, and pharmaceuticals. Traditional heat-seal systems pose risks of product degradation, melting, or texture alteration — issues entirely mitigated by cold sealing, which bonds packaging films through pressure activation at ambient conditions.

In the pharmaceutical and medical packaging domain, the adoption of cold seal adhesives is accelerating for sterile barrier systems and diagnostic kit packaging. Leading manufacturers have developed specialized cold seal coatings for sterilization-compatible medical pouches, ensuring reliable sealing without compromising barrier properties or contaminating sensitive medical devices. Similarly, in the premium food and frozen goods segment, European producers are expanding cold seal adhesive lines optimized for ice cream, chocolate, and bakery wraps, addressing both the operational need for high-speed sealing and the market demand for temperature-stable, peelable packaging that preserves product freshness.

The evolution is driven by the growing global preference for ready-to-eat and chilled convenience foods, combined with the tightening of food-contact safety regulations (e.g., EU 10/2011, FDA 21 CFR). As such, cold seal adhesives are becoming the standard for heat-labile food and pharma packaging applications, offering manufacturers a scalable route to energy-efficient, product-safe sealing systems that meet both regulatory compliance and sustainability mandates.

The global packaging industry’s shift toward smart and connected packaging technologies—such as RFID, NFC, and time-temperature indicators—is opening new frontiers for functional cold seal adhesives that support integration with printed electronics. Unlike heat-sealing methods that can distort or deactivate printed circuits due to localized heating, cold seal adhesives bond at ambient temperature, making them ideally suited for flexible electronic and smart packaging applications.

Recent R&D breakthroughs have demonstrated that cold seal formulations can be chemically engineered to coexist with conductive inks, metallic coatings, and polymeric substrates, ensuring consistent electrical performance and mechanical protection. The property is particularly valuable for intelligent food packaging, where embedded sensors monitor freshness or temperature exposure, and for pharma serialization systems, where tamper evidence and data integrity are critical. In addition, in industrial electronics, non-thermal sealing is proving essential for packaging sensitive components like sensors, flexible circuits, and microchips, where even minimal heat exposure can compromise functionality.

Manufacturers focusing on low-surface-energy cold seal adhesives with customizable tack profiles are well-positioned to capture the emerging niche. As the convergence of electronics, packaging, and materials science accelerates, functional cold seal adhesives are poised to become key enablers of the next generation of intelligent, connected, and sustainable packaging systems.

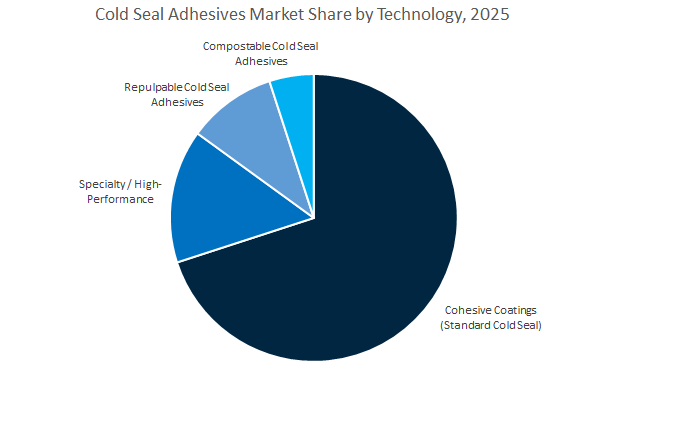

Cold Seal Adhesives Market Share Insights, 2025-2034

Cohesive coatings, also known as standard cold seal adhesives, dominate the global cold seal adhesives industry, accounting for approximately 68.9% of the projected 2025 market share. This dominance is due to their unmatched balance of cost-efficiency, reliability, and compatibility with a wide variety of packaging substrates, particularly paper and flexible films. Based primarily on natural rubber latex or synthetic rubber polymers, these coatings exhibit the key performance advantage of self-adhesion—bonding only to themselves under pressure without the application of heat. This makes them indispensable for high-speed packaging operations where thermal sealing is impractical or damaging, such as in the packaging of heat-sensitive food products like chocolates, snack bars, and frozen desserts. Their proven track record across both food and non-food applications ensures strong adoption across global packaging lines. Furthermore, ongoing innovations—such as optimized coat weight formulations, faster sealing response, and improved compatibility with multi-layer film laminates—are enhancing both the speed and efficiency of cohesive cold seal systems. The segment’s continued leadership is also supported by scalability in mass production and compatibility with existing converting equipment, making it the default technology for most high-volume flexible packaging converters worldwide.

While cohesive coatings dominate the landscape, specialty and sustainable cold seal adhesives are emerging as high-value growth segments, driven by evolving packaging regulations, sustainability imperatives, and consumer preferences for eco-friendly materials. Specialty formulations—including low-migration, non-tacky, and high-barrier compatible cold seals—are rapidly gaining traction in sensitive packaging sectors such as food and pharmaceuticals, where contamination prevention and regulatory compliance (e.g., FDA and EU standards) are non-negotiable. These adhesives are designed to maintain strong cohesive integrity even on complex multi-layer barrier films used for extended shelf life packaging. Parallelly, repulpable and compostable cold seal adhesives are expanding as packaging manufacturers transition toward circular economy materials. Repulpable cold seals allow for seamless integration into paper recycling streams, while compostable cold seals are increasingly used with bio-based films like PLA (polylactic acid), aligning with brand sustainability goals and ESG-driven initiatives.

The Food Packaging segment dominates the global cold seal adhesives market, commanding a substantial 72.3% share in 2025. This dominance is rooted in the unique ability of cold seal adhesives to deliver instantaneous bonding under pressure without the need for heat, making them ideal for packaging heat-sensitive products such as confectionery, baked goods, ice cream bars, frozen foods, and snack items. Food manufacturers rely heavily on these adhesives for their fast line speeds, energy efficiency, and superior seal integrity, which are essential for high-volume automated production. Cold seals also support lightweight packaging structures, reducing material consumption while maintaining excellent product protection and shelf appeal. In addition, they enable easy-peel, resealable, and tamper-evident designs, aligning with modern consumer preferences for convenience and sustainability. As global demand for flexible packaging continues to surge—particularly in emerging economies across Asia-Pacific and Latin America—cold seal adhesives are positioned as an essential enabler of sustainable, high-speed food packaging operations.

The Medical and Pharmaceutical Packaging segment represents a high-value, precision-driven portion of the cold seal adhesives market. Cold seal technology is indispensable for producing sterilized pouches, blister wraps, and medical device packaging where traditional heat-sealing could compromise sterile barriers or sensitive drug formulations. These applications demand consistent seal integrity, low odor, and non-migratory properties, making specialty cohesive and water-based rubber formulations the adhesives of choice. Stringent compliance with pharmacopoeial standards and ISO certifications ensures that these materials meet the most demanding health and safety criteria. The segment’s growth is further fueled by the expansion of single-use medical devices, diagnostic kits, and flexible sterile packaging, particularly in response to rising global healthcare needs and e-commerce distribution of pharmaceuticals. With the post-pandemic emphasis on hygiene, sterility, and packaging traceability, cold seal adhesives continue to gain relevance as a non-thermal, contamination-free sealing solution in the medical and pharmaceutical sectors.

The global cold seal adhesives industry is led by major chemical and adhesive companies that are aggressively expanding capacity, integrating sustainability targets, and developing specialized cold seal coating systems. Leaders such as Henkel, Dow, Ashland, BASF, and Lubrizol dominate the sector through innovation in eco-friendly, water-based, and recyclable adhesive technologies designed for flexible packaging, labeling, and medical applications.

Henkel maintains its dominant position as a top-tier provider of water-based cold seal adhesives and PSAs across flexible packaging, labeling, and food sealing applications. In 2024, its Adhesive Technologies division generated over €10.97 billion in sales, accounting for 51% of corporate revenue. The company’s innovation engine, the Inspiration Center Düsseldorf (ICD), fosters direct collaboration with packaging converters to co-develop high-speed sealing solutions. Henkel’s Aquence PS 3017 RE recyclable wash-off PSA exemplifies its R&D strength in circular packaging. Its ongoing CO₂-reduction initiatives target a 30% Scope 3 emission cut by 2030, reinforcing its leadership in low-carbon adhesive manufacturing.

Dow Corporation plays a foundational role in the cold seal adhesives value chain through its performance polymers, polyethylene resins, and acrylic additives used in water-based cold seal coatings. The company’s sustainability roadmap aims to commercialize 3 million metric tons of renewable and circular materials by 2030 and make all packaging-related products 100% recyclable or reusable by 2035. Dow’s partnership with Henkel (October 2025) underscores its proactive role in decarbonizing the adhesives supply chain. The company’s high-purity base polymers ensure consistent performance for film-to-film and film-to-foil bonding, essential for mono-material flexible packaging.

Ashland is a recognized leader in pressure-sensitive adhesive (PSA) technology serving the medical, labeling, and packaging sectors. Its Aroset™ and Arocure™ PSA lines provide high-speed converting capability, superior cohesion, and tailored tack levels for diverse packaging substrates. The company’s innovation in stress-relaxation testing allows real-time prediction of adhesive performance during high-speed processing. With a legacy strengthened by the acquisition of Air Products’ PSA division, Ashland continues to shape the next generation of solvent-free, UV-curable, and emulsion-based adhesives tailored for flexible packaging and tape systems

BASF remains a critical raw material supplier for cold seal adhesive manufacturers, providing a robust portfolio that includes Acronal® dispersions, acResin® UV-curable polymers, and Basonat® crosslinking agents. These materials form the chemical backbone of low-VOC, water-based cold seal coatings used in confectionery, healthcare, and lidding applications. Through its Mass Balance approach, BASF enables customers to source adhesives with a certified lower carbon footprint. Its recent R&D initiatives in aging-resistant polyacrylates and polyurethane dispersions position the company as a leader in sustainable raw materials for cold seal technology.

Lubrizol focuses on additive and polymer innovations for flexible packaging and lidding applications, enhancing the performance of water-based pressure-sensitive adhesives (PSAs). Its latest breakthrough technology provides moisture resistance without whitening, solving a major durability challenge for cold seal tapes and label films in humid environments. The company’s Singapore Innovation Center, opened recently, serves as a hub for Asia-Pacific R&D collaboration, advancing local development in film-to-film and paper-to-foil bonding applications. Lubrizol’s emphasis on high-solid, fast-drying polymer systems supports the global demand for efficient, sustainable, and performance-oriented packaging adhesives.

The United States composite adhesives industry is witnessing rapid evolution through large-scale investments, sustainable chemistry initiatives, and expanding applications across EVs, aerospace, construction, and medical sectors. In September 2025, Henkel completed a $30 million expansion of its Brandon, South Dakota facility—its North American flagship site for thermal management and adhesive solutions under the LOCTITE® and BERGQUIST® brands. The expansion boosts production of high-performance adhesives essential for EV battery assembly, supporting the country’s fast-growing electric mobility ecosystem.

3M Company further enhanced U.S. market competitiveness in late 2023 by launching a dual-cure polyurethane adhesive, combining UV and moisture curing to improve efficiency and reliability in automotive electronics and industrial composites. Concurrently, Hexcel Corporation expanded its carbon fiber prepreg facility in Utah (2025) to meet growing aerospace OEM demand for lightweight, fatigue-resistant bonding systems. Federal infrastructure investments by the U.S. Department of Transportation are catalyzing demand for composite structural adhesives in bridges, tunnels, and civil projects, reinforcing the country’s transition to durable, high-strength materials. Meanwhile, H.B. Fuller Company’s acquisition of medical adhesive technologies strengthens its foothold in biocompatible composite bonding, reflecting diversification into advanced healthcare composites.

Germany remains the epicenter of European composite adhesive innovation, driven by its stringent low-VOC regulations, circular economy principles, and automotive lightweighting initiatives. Henkel AG & Co. KGaA, headquartered in Düsseldorf, continues to pioneer high-performance polyurethane adhesives optimized for EV battery housings, façade systems, and structural bonding in automotive and construction applications. In October 2025, Henkel deepened its strategic partnership with Dow, targeting decarbonization in adhesive manufacturing through low-carbon feedstocks and energy-efficient production of hot melts and composite bonding agents.

Simultaneously, BASF SE has expanded polyurethane dispersion capacity at its Spanish site (2024), ensuring supply stability for sustainable adhesive raw materials across Europe. German automakers are increasingly adopting epoxy and polyurethane adhesives for carbon fiber-reinforced (CFRP) components, including lightweight EV chassis. The country’s strong emphasis on disassembly-ready adhesives aligns with the EU’s circular economy vision, enabling recyclable composite systems. Germany’s innovation leadership is also visible in bio-based adhesive formulations and R&D into triggerable polymer chemistries, setting benchmarks for next-generation composite sustainability.

China continues to dominate the global composite adhesives landscape, driven by industrial expansion, localized production, and rising demand across aerospace, wind energy, and high-speed rail applications. The country’s rapid adoption of advanced epoxy adhesives for offshore wind turbine blades and infrastructure composites reflects its commitment to energy transition and sustainable engineering. Localized investments have intensified since Sika AG’s acquisition of Crevo-Hengxin (2019), strengthening its silicone and bonding product portfolio for China’s construction and automotive sectors.

Government policies promoting high-speed rail networks and aerospace innovation have accelerated the use of two-component structural adhesives for durability and lightweighting in transportation. Moreover, domestic and multinational players are expanding R&D and manufacturing capabilities to supply high-purity electronic adhesives, essential for consumer electronics miniaturization. China’s push toward localized supply chains has reduced dependence on imported composite adhesives, as global firms like BASF, Dow, and Henkel establish R&D centers tailored for domestic EV and aerospace applications. The country’s dual focus on industrial resilience and high-performance bonding technologies ensures continued market dominance.

India’s composite adhesives market is entering a high-growth phase, propelled by defense manufacturing, infrastructure modernization, and sustainable building programs. Under the Ministry of Defence’s 2024–25 plan, India targets a ₹1.75 lakh crore turnover in aerospace and defense manufacturing by 2025, creating strong demand for aerospace-grade composite adhesives used in airframes, radomes, and lightweight armor systems. Complementing The, the Defence Testing Infrastructure Scheme (DTIS)—with an outlay of ₹400 crore—supports material qualification facilities for composite adhesives in Lucknow, strengthening domestic certification standards.

Infrastructure programs like Bharatmala Pariyojana, which saw 5,852 km of highways completed by December 2024, are driving large-scale adoption of structural bonding agents for bridge joints, façade panels, and asphalt overlays. Additionally, green construction initiatives such as Pradhan Mantri Awas Yojana are expanding demand for moisture-resistant and insulation adhesives suited to India’s tropical climate. Pidilite Industries Ltd., a regional adhesives leader, continues expanding its industrial composite portfolio to serve automotive, defense, and building sectors. India’s combination of policy-driven demand, export-oriented manufacturing, and private R&D collaboration positions it as a rising global hub for advanced composite bonding systems.

Switzerland serves as a global innovation center for sustainable and high-performance composite adhesives, led by Sika AG, headquartered in Baar. In 2024, Sika introduced a low-isocyanate polyurethane adhesive engineered for modular construction and lightweight transportation, offering enhanced flexibility and rapid curing for off-site applications. The innovation complements its strategy to provide eco-compliant, low-VOC bonding solutions for both automotive and construction composites.

Sika’s acquisition strategy, including DriTac (U.S., 2021) and Chema (Peru, 2023), strengthens its global composite adhesive network and expands its expertise in flooring and panel bonding technologies. Switzerland remains a nucleus for R&D in advanced materials, where universities and chemical firms collaborate on next-generation fatigue-resistant adhesives for CFRP (Carbon Fiber Reinforced Plastic) assemblies. The country’s strong export orientation, coupled with a commitment to sustainability, solidifies its leadership in developing structural adhesives with superior mechanical endurance and recyclability.

Japan’s composite adhesives market is marked by high-precision manufacturing, aerospace expansion, and strong integration of adhesives into electronics and EV production ecosystems. Toray Industries, a global leader in advanced materials, signed a long-term supply agreement with Boeing in 2025, ensuring continuous delivery of carbon fiber composites for next-generation aircraft, thereby stimulating demand for aerospace-grade bonding systems. Japanese manufacturers such as ThreeBond Co., Ltd. are pioneering high-durability adhesives optimized for battery assembly, providing thermal stability and vibration resistance under demanding EV conditions.

The country’s emphasis on miniaturization and advanced electronics continues to drive demand for one- and two-component epoxy and acrylate adhesives, particularly for micro-bonding applications. Additionally, Soudal’s acquisition of a majority stake in Sharp Chemicals (2024) expands product diversity, strengthening Japan’s industrial adhesive market. Japan’s expertise in precision polymer engineering, combined with a push for lightweight automotive and aerospace composites, ensures its continued leadership in high-performance, reliability-driven bonding technologies.

Cold Seal Adhesives Market Report Scope

Cold Seal Adhesives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.35 Billion

|

|

Market Size (2034)

|

$2.4 Billion

|

|

Market Growth Rate

|

6.4%

|

|

Segments

|

By Formulation (Natural Rubber Latex, Synthetic Rubber Latex, Water-Based Cold Seal Adhesives, Solvent-Based Cold Seal Adhesives), By Technology (Cohesive Coatings, Repulpable Cold Seal Adhesives, Compostable Cold Seal Adhesives, Specialty / High-Performance), By Packaging Format (Film-to-Film, Film-to-Paper, Paper-to-Paper, Foil-based), By Application (Food Packaging, Medical & Pharmaceutical Packaging, Industrial & Consumer Goods

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Henkel AG & Co. KGaA, H.B. Fuller Company, The Dow Chemical Company, Arkema Group, Sika AG, 3M Company, Ashland Global Holdings Inc., Wacker Chemie AG, Jowat SE, DIC Corporation, Kraton Corporation, Pidilite Industries Ltd., BASF SE, Covestro AG, Nan Pao Resins Chemical Group

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Formulation

- Natural Rubber Latex

- Synthetic Rubber Latex

- Water-Based Cold Seal Adhesives

- Solvent-Based Cold Seal Adhesives

By Technology/Type

- Cohesive Coatings

- Repulpable Cold Seal Adhesives

- Compostable Cold Seal Adhesives

- Specialty / High-Performance

By Substrate / Packaging Format

- Film-to-Film

- Film-to-Paper

- Paper-to-Paper

- Foil-based

By Application

- Food Packaging

- Medical & Pharmaceutical Packaging

- Industrial & Consumer Goods

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

- Henkel AG & Co. KGaA

- H.B. Fuller Company

- The Dow Chemical Company

- Arkema Group

- Sika AG

- 3M Company

- Ashland Global Holdings Inc.

- Wacker Chemie AG

- Jowat SE

- DIC Corporation

- Kraton Corporation

- Pidilite Industries Ltd.

- BASF SE

- Covestro AG

- Nan Pao Resins Chemical Group

*- List not Exhaustive

Research Coverage

Prepared by USDAnalytics, this report investigates the Cold Seal Adhesives market through a decisive lens on sustainability, energy efficiency, and next-gen water-based technologies powering flexible packaging and healthcare applications. It delivers analysis reviews of performance drivers, regulatory shifts, and application innovations; highlights manufacturing advances that enable faster lines and recyclable mono-material structures; and tracks breakthroughs in polymer dispersions, cohesive systems, and automation-ready coatings shaping converter economics and brand compliance. By connecting technical specifications (seal integrity, rheology control, migration safety) with procurement priorities (carbon reduction, recyclability, OEE gains), this report is an essential resource for packaging converters, formulators, brand owners, and operations leaders who need actionable intelligence on portfolio positioning, specification strategy, and investment decisions across food, pharma, and industrial packaging value chains.

Scope Highlights

Segmentation:

- By Formulation: Natural Rubber Latex; Synthetic Rubber Latex; Water-Based Cold Seal Adhesives; Solvent-Based Cold Seal Adhesives.

- By Technology/Type: Cohesive Coatings; Repulpable Cold Seal Adhesives; Compostable Cold Seal Adhesives; Specialty / High-Performance.

- By Substrate / Packaging Format: Film-to-Film; Film-to-Paper; Paper-to-Paper; Foil-based.

- By Application: Food Packaging; Medical & Pharmaceutical Packaging; Industrial & Consumer Goods.

Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Time Frame: Historic data 2021–2024 and forecast 2025–2034.

Companies: Analysis/profiles of 15+ companies (strategy, innovation, capacity, and product benchmarking).

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.